Bibliography

On general economic equilibrium: F. Ackerman, ‘Still Dead after all these Years: Interpreting the Failures of General Equilibrium Theory’, Journal of Economic Methodology (2002); V.

Biihm, Disequilibrium and Macroeconomics (Oxford, 1989); M. De Vroey, ‘La possibilite d’une economie decentralise: esquisse d’une alternative a la theorie de l’equilibre general’, Revue Economique (1987); D. Gale, Money: in Equilibrium (Cambridge, 1982); Money: in Disequilibrium (Cambridge, 1983); F. H. Hahn, ‘General Equilibrium Theory’, in D. Bell and I. Kristol (eds.), The Crisis in Economic Theory (New York, 1981); ‘Stability’, in K. J. Arrow andM. D. Intriligator (eds.), Handbook of Mathematical Economics, vol. I, (Amsterdam, 1982); W. Hildebrand and A. P. Kirman, Introduction to Equilibrium Analysis (Amsterdam, 1976); Equilibrium Analysis (Amsterdam, 1988); B. Ingrao and G. Israel, La mano invisibile: L'equilibrio economico nella storia della scienza (Roma, 1987);

N. Kaldor, ‘The Irrelevance of Equilibrium Economics’, Economic Journal (1972); T. J. Kehoe, ‘Intertemporal General Equilibrium Models’, in F. Hahn (ed.), The Economics of Missing Markets, Information and Games (Oxford, 1989); A. Mas Colell, The Theory of General Economic Equilibrium. A Differentiable Approach (Cambridge, 1985); T. Negishi, ‘The Stability of a Competitive Equilibrium: A Survey Article’, Econometrica (1962); R. M. Starr (ed.), General Equilibrium Models of Monetary Economies (New York, 1989).

On developments in new welfare economics and the theories of justice: F. M. Bator, ‘The Anatomy of Market Failure’, Quarterly Journal of Economics (1958); R. Coase, The Firm, the Market and the Law (Chicago, 1988); R. Cornes and T. Sandler, The Theory of Externalities, Public Goods, and Club and Goods (Cambridge, 1986); C. D’Aspremont and L. Gevers, ‘Equity and the Informational Basis of Collective Choice’, Review of Economic Studies (1977); J.

de V. Graaff, Theoretical Welfare Economics (Cambridge, 1957); J. Farrell, ‘Information and the Coase Theorem’, Journal of Economic Perspectives (1987); A. Feldman, Welfare Economics and Social Choice Theory (Boston, 1980); P. J. Hammond, ‘Equity, Arrow’s Conditions and Rawls’ Difference Principle’, Econometrica (1976); ‘On Reconciling Arrow’s Theory of Social Choice with Harsanyi’s Fundamental Utilitarianism’, in G. R. Feiwell (ed.), Arrow and the Foundations of the Theory of Economic Policy (London, 1987); J. Harsanyi, Morality and the Theory of Rational Behaviour (New York, 1977); I. M. D. Little, A Critique of Welfare Economics (Oxford, 1957); A. Sen, Choice, Welfare and Measurement (Oxford, 1982); A. Smith, The Theory of Moral Sentiments (Oxford, 1976); J. Tinbergen, ‘Welfare Economics and Income Distribution’, American Economic Review (1957); W. S. Vickery, ‘Utility, Strategy, and Social Decision Rules’, Quarterly Journal of Economics (1960); R. Wilson, ‘Social Choice Theory without the Pareto Principle’, Journal of Economic Theory (1972).On the marginalist controversy and the new theories of the firm: M. Aoki, The Co-operative Game Theory of the Firm (Oxford, 1984); W. Baumol, J. Panzar, and R. Willig, Contestable Markets and the Theory of Industry Structure (New York, 1982); A. S. Eichner, ‘P.W.S. Andrews and E. Brunner’s Studies in Pricing: Review’, Journal of Economic Literature (1978); O. Hart and B. Holmstrom, ‘The Theory of Contracts’, in T. Bewley (ed.), Advances in Economic Theory (Cambridge, 1987);

B. Holmstrom and J. Tirole, ‘The Theory of the Firm’, in R. Schmalensee and R. Willig (eds.), HandbookofIndiistrial Organization (Amsterdam, 1989); A. Jacquemin, Selection et pouvoir dans la nouvelle economie industrielle (Paris, 1985); M. Kamien, and N. Schwartz, Market Structure and Innovation (Cambridge, 1982); P. Mongin, ‘La methodologie economique aux XX siTracing Procedure’ (1975). Harsanyi introduced a more general class of games, defined as ‘Bayesian games’, in which the players may not know with certainty the structure of the game.

R. Selten, on the other hand, introduced the notion of ‘perfect equilibrium’ in ‘Re-examination of the Perfectness Concept for Equilibrium in Extensive Games’ (1975). He started from the observation that quite a number of Nash equilibria are imperfect in the sense that they are based on threats of action depending on circumstances which never occur in the equilibrium situation, and which the players would never take into consideration if they could choose. The notion of ‘perfect equilibrium’ eliminates this kind of imperfection. An important recent synthesis of these two lines of research has been made by D. Kreps and R. Wilson with the notion of ‘sequential equilibrium’.In the case of two-person zero-sum games, things are much clearer: von Neumann’s famous minimax theorem states, in fact, that, if the number of feasible pure strategies is finite, such games are determinate, or, rather, that they admit a single rational result in terms of mixed strategies. The theorem has had an enormous impact on the development of the subject (the demonstration itself of the existence of a competitive equilibrium has been obtained from a generalization of one of the demonstrations of the minimax theorem), and for a long period zero-sum games were considered as the field for the application of the theory.

The modern theory, although it has pushed the original ideas of von Neumann and Morgenstern far forward, has encountered formidable problems. For example, even in the field of co-operative games there is usually a multiplicity of possible equilibria. The number and the nature of the equilibria associated with a certain game will thus be determined by the particular interpretation of the game, the set of strategies available to the players, and the ‘rationality criteria’ to which they adhere. There is no universally valid criterion of choice. Each proposed criterion selects ‘reasonable’ equilibria for certain games; but for other games it excludes some equally ‘reasonable’ equilibria in order to choose some other less ‘plausible’ ones.

Another difficulty emerged in the 1950s and 1960s which concerned complete and perfect information games. In complete-information games, the players understand the nature of the game; in perfect-information ones, on the other hand, the players know both the nature of the game and all the preceding moves of the other players. This limited the field of the phenomena which the theory was able to tackle, and therefore restricted its possible applications in economics. The theoretical developments in the 1970s and 1980s, especially the work of Harsanyi and Selten, have partially remedied this deficiency.

A recent approach has considered repeated games, also called supergames. Strategic behaviour can change if, instead of playing ‘once and for all’, the individuals know that the game may be repeated a certain, perhaps indefinite, number of times. A typical example is the well-known ‘prisoner’s dilemma’, a non-zero-sum game which gives rise to a non-cooperative solution if it is played only once, but which can generate co-operative behaviour if it is repeated a certain number of times. R. Luce and H. Raiffa were among the first to highlight the dilemma. This consists in the fact that an egoistic choice is rational but does not lead to the best possible solution, while the co-operative choice is irrational for the person who makes it unless the reply of the other player is also co-operative. What is best for the individual is not necessarily best for the individuals taken together. The interest in repeated games is due to a theorem, known as the ‘Folk Theorem’, which establishes a basic analogy between repeated games and non-repeated co-operative games by pointing out that the emergence of factors such as ‘reputation’ or ‘credibility’, which are typical of repeated games, can naturally lead the players to explore the possibilities of co-operative solutions. This is because these factors can give efficacy to the agreements and threats that make co-operation possible. An experimental verification of the theorem was given by R.

Axelrod (The Evolution of Cooperation, 1984), who demonstrated how co-operative results tend to prevail in a game repeated an indefinite number of times.In view of the close link between ‘oligopolistic indetermination’ and game theory, it is not surprising that the conceptual apparatus of the latter has found a wide application in industrial economics. In his 1947 article, ‘Price Theory and Oligopoly’, K. W. Rothschild complained that, when dealing with oligopoly, economists let themselves be too influenced by analogies from mechanics and biology. Rothschild believed that in the study of oligopolist situations it is preferable to refer to those fields of research that study moves and counter-moves, the fight for power, and strategic behaviour. In fact, the use of game theory has led, in recent times, to the revaluation of concepts such as entry barriers and the relationship between the structure of the market and technical change. As M. Shubik has indicated in Strategy and Market Structure (1959), the most important result in this context has been the following: the causal link proceeding from the structure of the market to the behaviour and the performance has been replaced by the idea that the structure of the market, intended as the number and size of firms operating in it, is endogenously determined by the strategic interactions of the firms.

Another fruitful area of application of game theory has been that of bargaining (theories of contracts, auctions, and collective bargaining), in which two or more individuals must come to an agreement for the share of a given stake, with the constraint that, in the case of a failure to reach agreement, nobody receives anything. This problem has allowed economists to give a precise definition to a key economic notion: that of ‘contractual power’. The more one party is ‘anxious’ to conclude an agreement, the more he will be disposed to give way. Ken Binmore’s ‘Modeling Rational Players’ (1987) is an important work in this context.

In it, the traditional notion of ‘substantive rationality’ has been replaced by that of ‘algorithmic rationality’, which resumes and generalizes Herbert Simon’s famous notion of‘procedural rationality’.Finally, a very recent field of application of game theory is that of the theory of economic policy (monetary and fiscal policy and international economic co-operation), where Selten’s ‘perfection criterion’ and the notion of ‘sequential equilibrium’ have been widely used in relation to the concepts of ‘credibility’ and ‘reputation’ of players such as governments and unions. Among the most important works on this subject are R. J. Aumann and M. Kurz, ‘Power and Taxes’ (1977) and P. Dubey and M. Shubik, ‘A Theory of Money and Financial Institutions’ (1978).

The greater fertility of the economic applications of game theory by comparison with that of other mathematical instruments also depends, perhaps, on the fact that this theory was not borrowed from another discipline, but was developed within economic research, which has favoured the formulation of concepts and formal procedures well suited to the representation of social and economic interactions.

However, it is important not to forget that there are still severe limitations in the modelling within game theory. For example, the choices of the most appropriate notions of ‘individual rationality’ and ‘game equilibrium’ are multifarious and partially arbitrary. And even where a well- defined notion of equilibrium has been accepted, the problem often still remains—especially in supergames—of the multiplicity of outcomes. In any case, it remains true that game theory, because of its rigorous logical structure, enables economists to classify different types of rationality and equilibrium, and is becoming a viable alternative research approach to the neo-Walrasian one.

11.1.2. Evolutionary games and institutions

The theory of evolutionary games was developed within the area of biological studies, where it provided a simple and elegant formalization of Darwin’s theory of natural selection. It is based on the idea that evolution in a biological context depends on the differential reproduction of the ‘most suitable’ individuals or elements; this concept will be clarified later. John Maynard Smith summed up the first stage of research in his book, Evolution and the Theory of Games. In condensing the results of over ten years of research, the great English biologist made known outside the circle of specialists the intriguing connection between the concept of game, suitably reinterpreted for the ‘animal conflict’ context, and the more basic notions of strategic rationality developed in economic research and decision theory, primarily the notion of Nash equilibrium. After an initial period of cautious interest, from the early 1990s economists began to pay increasing attention to this new area of the discipline, to which they devoted more and more of their research efforts. Their interest can be traced back to the impasse that characterized literature on the so-called refinements of Nash equilibria in the early part of that decade, as recalled in the previous paragraph.

For the notion of Nash equilibrium to be considered a really useful instrument, in the presence of a plurality of equilibria it was necessary to come up with a convincing and practical criterion for deciding which of them to select in relation to the structure and characteristics of the game. Several refinement criteria had been proposed during the 1980s, with much use of inventiveness and technical skills, but all appeared to have substantial limits. In particular, each refinement criterion appeared to have been tailor-made for a certain type of game and was quite inadequate in contexts other than those for which it had been conceived. The monumental work of John Harsanyi and Reinhard Selten, A General Theory of Equilibrium Selection in Games, published in 1988 after a long period of gestation, purported to have the last word on the argument by putting forward a general theory that was valid for every possible type of game. But, despite the enormous effort and the important results achieved, the ‘general theory’ was so complex and intricate that it was soon clear that the research programme had substantially failed.

The advent of the evolutionary theory of games was thus hailed with much satisfaction and a certain amount of relief: thanks to this theory it was at last possible to construct a ‘social dynamics’ through which players ended by converging on the choice of a unique Nash equilibrium, based on well- defined conditions. This kind of choice, which seemed impossible in the aprioristic type of approach inherent in the theory of refinements, could be realized ex post, as the result of a process of interaction between a large number of agents. However, when it came to the point, the evolutionary approach too left problems to be solved. For instance, in the case of games with a sufficiently high number of strategies, evolutionary dynamics could easily give rise to complex behaviours that did not contemplate convergence towards a final Nash equilibrium.

This disappointment was soon overcome by another possible interpretation of evolutionary games, one that saw it in terms of bounded rationality. As Ken Binmore observed, the problem of the ‘eductionist’ approach to game theory laid precisely in the difficulty of building a priori a theory of strategic rationality that was valid in every circumstance, while through the alternative ‘evolutionary’ approach it was possible to demonstrate how and in what conditions certain a priori rational behaviours became socially diffused. They could be spread through social learning mechanisms even in the presence of players with modest calculus abilities and inflexible and substantially adaptive behavioural patterns, based on a Simon-type satisficing type of logic. Even with very simple models, the theory showed that rational behaviour, in the broadest sense, might not ensure maximum pay-offs for players. There was consequently a direct and unequivocal challenge to the Darwinian theory on which various utilitarian economists had tried to base the hypothesis of Homo oeconomicus rationality. Contrary to a longstanding belief, a superior rationality did not necessarily imply greater possibilities of profit or survival in the presence of competitive interaction. These results opened up new and important prospects particularly for those economists who were most dissatisfied with the ultimate implications of the traditional neoclassical approach.

The theory of evolutionary games puts forward an interesting static notion of equilibrium and an even more interesting specification of the dynamic selection process. The new notion of equilibrium is expressed in terms of an evolutionary stable state, a condition that calls for a robust strategy profile not only in respect of single individual deviations (as in the case of Nash equilibrium) but also in respect of deviations chosen simultaneously by an albeit small fraction of players. This significant innovation has, however, one important fault: in a given game there is no guarantee that a Nash equilibrium exists which satisfies that condition.

The most widely studied dynamic process in the evolutionary game theory is the so-called replicator dynamics, according to which the weight of a strategy in a population of players increases more the higher is the reward of that strategy compared with the mean gain. In other words, strategies that do better than the mean are rewarded at the expense of those that do worse, the more so the better they do. When replicator dynamics converge, they do so towards Nash equilibria, and possess a certain number of interesting properties, such as the tendency to eliminate any strategy that is strictly dominated in the game.

In more recent years, economists have begun to use notions of evolutionary stable state and replicator dynamics to build models that can be applied to a wide variety of contexts, with particular emphasis on phenomena which were barely considered in the past, such as the formation of social conventions, the impact and evolution of social norms and cultural evolution. Another fertile field of application concerns the classic problems of institutional change and the evolution of individual preferences. These problems can now be tackled in a new way. Today the theory of evolutionary games is becoming an alternative paradigm to the neoclassical approach, thanks also to its ability to explain endogenously crucial phenomena like the predominance of a certain level of rationality among economic agents and the survival conditions of non self-interested individual motives. Models of evolutionary games are particularly suitable for the study of cultural evolution. In The Evolution of Social Contract, Brian Skyrms showed how the rules of justice and co-operative types of rules evolve in time and in specific environmental contexts, even between self-interested subjects. Another fertile field of application deals with explaining the emergence of social rules such as those of reciprocity, sympathy and altruism. Here the reference is The Complexity of Cooperation, by R. Axelrod, in which, for the first time, a particular genetic algorithm has been applied to the theory of

evolutionary games. Genetic algorithms were initially developed in studies on artificial intelligence and reproduce the mechanisms that drive biological evolution to search for more efficient methods of ensuring adaptation to a plurality of environmental contexts. Referring to a ‘prisoner’s dilemma’ type of situation, Axelrod demonstrated that the tit-for-tat strategy which he himself ‘invented’ and expounded in his contribution of 1984, is very robust, and that cooperative and reciprocating strategies tend to prevail in a wide variety of situations.

To conclude, in the theoretical scenario opened up by the theory of evolutionary games, there is growing convergence among research undertaken by biologists, economists and sociologists. The foundations are being laid down for a science of social behaviour which goes far beyond the old disciplinary boundaries of positivist ascendancy.

11.1.3. The theory of endogenous growth

To understand the reasons behind the great success of the endogenous growth theory in macroeconomics over the last decade, it is necessary to begin from the so-called ‘Solow residue’. This expression indicates all those determinants of the growth processes that cannot be reduced to labour and capital contributions. With hindsight it can be said that one of the chief merits of Solow’s 1956 model (see section 9.2.4) was the idea that economic growth cannot be completely explained by increases in the stock of productive factors. Nonetheless, his theory left various questions unanswered: given that technical progress lies at the base of labour and capital productivity increases, how can this phenomenon be modelled? How can an endogenous explanation be given for the long-run growth rate?

Despite the objective importance of these questions and the innovative contributions made by economists such as Kenneth Arrow and Nicolas Kaldor, in the 1960s the neoclassical students’ concern with growth problems waned, preference being given to business cycle theory. However, this period of oblivion was not to last for long. As N. Foss showed, beginning in the early 1980s, economists gradually shifted their interest in the business cycle to include the study of real growth factors, to the detriment of monetary factors. The work of F. Kydland and E. Prescott is an example of this shift; the trend hailed the arrival of a change of climate which soon proved to be extremely favourable to the advent of the ‘new growth theory’.

The theory of endogenous growth officially came to light in 1986, the year of publication of P. Romer’s fundamental article Increasing Returns and Long-Run Growth. It describes a model of competitive equilibrium in which the growth process is guided by Marshall type increasing returns. The aggregate production function has the following characteristics: output depends on the capital stock, on labour and on the costs of R&D activities; in addition, the spillover from private research brings improvements in the stock of public knowledge. Knowledge is intended as an input with an increasing marginal productivity. The model therefore combines two basic hypotheses: competitive equilibrium and endogenous technological change. Romer pointed out that there are different forms of knowledge: at the one extreme we have basic scientific knowledge, at the other, knowledge intended as a set of specific instructions relating to a determined operation. Romer observed that ‘there is no reason to expect the accumulation determinants of these different types of knowledge to be the same [... ] There is, therefore, no reason to expect a unified theory of knowledge growth’ (p. 1009).

One fundamental aspect shared by the numerous endogenous growth models is their characterization of knowledge as a public good: knowledge has in fact, at least to a certain extent, precisely the characteristics of nonexcludability and non-rivalry of these goods. The idea is that the nonexcludability from the use of new knowledge created by an individual firm generates positive effects on the production possibilities of other firms.

The hypotheses of increasing returns and non-excludability of knowledge were already present in the work on learning by doing published by Arrow over two decades earlier. Arrow had put forward the idea that increasing returns appear to be a direct effect of the discovery of new knowledge. This was the basic idea developed later by Romer.

One of the most important implications of Romer’s model is the following: the per capita outputs of different countries do not necessarily converge: less developed countries may well grow at a lower rate than more advanced countries or indeed may not grow at all. Later, in a model elaborated in 1990, Romer considered an economy divided into three sectors (research, intermediate goods and final goods), and characterized by monopolistically competitive markets. He furthermore assumed that while the stock of technological knowledge was non rival, human capital was. The model predicts that economies endowed with a higher stock of human capital grow at a faster rate than the others. There will be an acceleration in growth also as a consequence of opening up to international trade.

In 1988 Robert Lucas presented a model similar to Romer’s 1986 version, but assumed that two different sectors and two different types of investment (in physical capital and human capital) are to be taken into account. The only exogenous magnitude hypothesized was the population growth rate. While physical capital would accumulate through the usual neoclassical mechanism, the growth of human capital would be regulated by the following ‘law’: independently of the stock already achieved, a steady level of effort corresponds to a steady rate of growth of the stock. Lucas held that one of the chief merits of the ‘new growth theory’ lies in its capacity to elaborate formal models to explain both the growth of advanced countries and developing countries. On the contrary, in the 1960s, the idea that it is necessary to resort to distinct theories prevailed. There are, furthermore, significant political implications, since public authorities appear to have greater ‘room for manoeuvre’ in situations of endogenous growth. Solow’s model, where the long-run growth rate depends exclusively on exogenous technological change, ended by not assigning any role to institutional subjects outside the market; conversely, endogenous growth models admit, for example, that changes in tax regime can influence the growth rate.

Another important contribution to the theory of endogenous growth was made by P. Aghion and P. Howitt, who attempted to demonstrate that firms may accumulate knowledge through numerous channels from formal education to product innovations. Great importance is attached to industrial innovations which improve product quality. The Schumpeterian view underlying Aghion and Howitt’s endogenous growth model can be summarized as follows: growth is the effect of technological progress which, in turn, depends on competition between firms that undertake research and create innovations. Every innovation gives rise to the production of a new type of intermediate good, as a result of which a final product can be produced in conditions of greater efficiency. From the individual firm’s point of view, the incentive to invest in research comes from the prospect of building up monopoly rents through the legal protection granted by innovations. On the other hand, in a dynamic context, those very rents are made fruitless by subsequent innovations, which render the old products obsolete almost as soon as they are produced. This analytical scheme also contemplates the existence of a strong relationship between the innovative firm’s market power and the degree of excludability of knowledge. This excludability in turn depends critically on the presence of legal institutions responsible for protecting ownership rights as well as on the very nature of knowledge.

11.2. The Theory of Production as a Circular Process

11.2.1. Activity analysis and the non-substitution theorem

In Chapter 8 we spoke of a tradition in input-output analysis that originated at the beginning of the twentieth century in Russia with Dmitriev, and then emigrated to Germany, with von Charasoff and von Bortkiewicz. There, in the second half of the 1920s, this tradition inspired the work of Leontief and Remak. In the same chapter we also spoke of Menger’s Viennese Kolloquium, and of the work of Schlesinger and Wald on the problem of the existence of solutions in the general-equilibrium model, and we also mentioned von Neumann’s movements between Berlin and Vienna.

This line of thought was transplanted to America in the 1930s and there, after the Second World War, bore diverse and notable fruits. We have already mentioned von Neumann’s contribution to the birth of game theory and of the balanced-growth models. We have also presented Leontief ’s research in input-output analysis. Finally, in Chapter 10 we spoke of the influence exerted by these lines of thought on the development of the neo- Walrasian approach. Now we should like to examine another two important theoretical developments which also began after the Second World War, and which can be interpreted as developments and extensions of Leontief’s and von Neumann’s models: activity analysis and the non-substitution theorem. The classic work for both these theoretical developments is undoubtedly Activity Analysis of Production and Allocation (1951), a book edited by Tjalling Charles Koopmans.

Activity analysis is a generalization of von Neumann’s model in terms of linear programming—a generalization consisting of the introduction of diverse scarce resources and the use of the model to solve the problem of their efficient allocation. The first ideas on linear programming, as already mentioned, go back to Kantorovic’s 1939 study. But the theory only took off in 1947, after the discovery of the simplex method, an efficient way of solving a linear-programming problem. The author was George Bernard Dantzig, who had discovered linear programming independently of Kantorovic. His first important work on the argument was Programming in a Linear Structure (1948). A second was published in the above-mentioned 1951 book edited by Koopmans.

The practical applications of linear programming have been especially important at the level of the firm. Here, however, we are interested in the theoretical applications, and the most important of these is activity analysis. An activity is a technically feasible combination of inputs, that is, a technique. It is assumed that there are more activities than resources. The so-called ‘primal’ problem consists in choosing a vector of activity levels which maximizes the level of final output, given the prices of final goods, in such a way that no more than the resources available are used. The ‘dual’ problem, on the other hand, consists of the determination of prices which minimize the costs of the utilized resources in such a way that the production cost of each good produced is not lower than its price. The latter condition ensures that there are no profits.

The solution of the programming problems ensures several results: the determination of equilibrium levels of prices and production; the maximization of national output; the minimization of production costs; the choice of efficient techniques. In other words, we have not just an equilibrium but an optimal solution.

The work edited by Koopmans also included four articles on the so-called ‘non-substitution theorem’. The authors were Georgescu-Roegen, Arrow, Koopmans, and Samuelson. Initially, this theorem was formulated as a theoretical application of Leontief ’s model. It is based on the following hypotheses: there is only one primary input, let us say labour; that input is indispensable for the production of all goods; each production process produces only one output; there are constant returns to scale and perfect competition. The problem is to choose the most profitable activity, i.e. that which minimizes costs. Now, under these hypotheses, prices and activity levels are independent, and the set of activities chosen as the most profitable to obtain a given vector of final demand remains the most profitable for the production of any other vector.

This latter result is of crucial importance. The activities are chosen by the entrepreneurs with the aim of minimizing costs; if there are no other primary inputs besides labour, there will be a unique set of activities which is the most profitable; as there are constant returns to scale, a technique which is most profitable at a certain level of activity is also so at any other level; therefore the choice of techniques does not change with variations in the composition of demand and the quantities produced, and prices depend solely on technical conditions of production.

There are two different interpretations of the relevance of this theorem. The first to be advanced interprets the term ‘substitution’ as a synonym for ‘change of techniques’. In this case the theorem serves to demonstrate the robustness of Leontief’s and similar models. The hypothesis of fixed coefficients, which appears in such models, is not restrictive, as was argued by some of Leontief ’s critics. In fact, the theorem demonstrates that the prevailing coefficients can be interpreted as those that have been chosen by the entrepreneurs from a vast range of technical possibilities, and that this choice is not modified by changes in final demand.

In another interpretation, the ‘non-substitution theorem’ aims to point out that, with variations in the composition of demand, there is no substitution among the primary factors. On the other hand, it is obvious that there cannot be substitution among primary factors when there is only one. Therefore, the relevance of the theorem would seem to lie in the fact that, when there is more than one primary factor, substitution is possible and takes place each time there is a change in consumer tastes. This seems to confirm the traditional neoclassical view that, in general, if the demand increases for a good with a high intensity of a certain factor, there will be an increase in the price of that good, but also in the demand and the remuneration of the factor in question, and, consequently, the prices of all the other goods will change. In general, therefore, prices depend on the demand for final goods and the scarcity of primary inputs. We will see in the next section how much caution is needed to sustain an argument of this type.

Meanwhile, we should like to point out that there are cases in which the non-substitution theorem does not hold, and in which the substitution of primary factors plays no role at all. One of these is where the returns to scale are not constant. Here it is clear that variations in demand will have relevant effects on the cost of the goods and therefore also on their prices. But this has nothing to do with the substitution among primary factors. Another case is that of joint production. Here, generally, variations in demand change the convenience conditions for the activation of different processes, as a certain good can be produced jointly with some other by using different activities. Thus, variations in demand can cause changes in the techniques activated and therefore in the costs and the prices of goods. But, again, this has nothing to do with substitution among primary factors.

Finally, we should like to mention three studies of the 1960s, one by P. A. Samuelson, one by J. A. Mirrlees and one by J. E. Stiglitz, in which the theory was generalized with the introduction of an interest rate, and with a special case of joint production. The introduction of the interest rate modifies the results of the theorem in the sense that there is a different price system for each different value of the interest rate. The ‘dynamic’ character of the theorem would consist of the possibility of applying it to an economy which is growing in steady-state.

11.2.2. The debate on the theory of capital

Although the possibility of substitution among primary factors is excluded under the hypotheses of the non-substitution theorem, it would seem possible to argue for another type of substitution: that between capital and labour. Even excluding the effects of final demand on prices, is it not possible that a significant relationship exists between demand for the ‘productive factors’, labour and capital, and their remunerations? If the prices of the factor services are indexes of scarcity, then the following should occur: with an increase in the wage-interest ratio, there should be an increase in the demand for the services of capital in relation to that of the services of labour. Under perfect competition the real compensations to factors should equal their marginal productivity; therefore, a decreasing function should link the capital intensity of the techniques to the relative cost of capital; a decrease in the marginal productivity of capital in relation to that of labour should be caused by the substitution of labour by capital.

This is the neoclassical theory of distribution. Already Wicksell, as we mentioned in Chapter 6, had noticed the strangeness of certain phenomena (later called ‘Wicksell effects’), and pointed out the possibility of some ‘paradoxes’ in the relationship between the capital intensity of the techniques and the remuneration of capital. However, it was only in the debate of the 1950s and 1960s that the problem was solved. The debate was opened by J. V. Robinson with the article ‘The Production Function and the Theory of Capital’ (1953-4), in which she put forward an argument inspired by Sraffa’s ‘Introduction’ (1951) to Ricardo’s Principles: that the ‘degree of mechanization’ of a productive technique can increase, rather than decrease, following an increase in the interest-wage ratio. Robinson also noted that the origin of this strange effect is to be found in the impossibility of measuring capital in physical terms, given its heterogeneous composition, and the consequent necessity to measure it in value. Then D. Champernowne, in a comment on Robinson’s article, while acknowledging the importance of the problem, suggested that it could be solved by measuring capital by means of an index of his own construction, although he admitted that his index might not work in some ‘strange’ cases. Robinson counter-attacked, especially in a section of The Accumulation of Capital (1956), where she pointed out that the strange relationship existing between the prices of factor services and the capital intensity of techniques is not due to purely ‘financial’ phenomena, as Champernowne seemed to suggest, but can be generated by real technical change.

In that year, by a strange historical quirk, the first neoclassical aggregate growth models came to light: those of Solow and Swan, already discussed in Chapter 9. These models used exactly the same aggregate production function and the same theory of capital which had been criticized by Robinson. This certainly helped to liven up the party. In 1960 Sraffa’s Production of Commodities by Means of Commodities was published, a book which contained, albeit in very concise form, all the elements needed to clarify the question. At the same time, Garegnani’s Il capitale nelle teorie della distri- buzione was published, a book in which criticism of the neoclassical theory of capital was explicitly formulated.

Robinson’s criticism was accepted without resistance by many neoclassical economists—for example by Morishima and Hicks. As late as 1962 and 1965, however, Samuelson and Levhari made attempts to resolve the problem in a different way from that suggested by Robinson. The debate reached its climax in 1966, when the Quarterly Journal of Economics published a special issue dedicated to capital theory. Decisive were Pasinetti’s and Garegnani’s contributions. But the most important one was Samuelson’s ‘Summing Up’, in which he acknowledged the validity of the criticisms and, while trying to minimize their importance, he admitted the error inherent in the neoclassical theory of aggregate capital. This closed the debate, even if the aftermath continued until the early 1970s. The final word on this problem was given by Garegnani in ‘Heterogeneous Capital, the Production Function and the Theory of Distribution’ (1970).

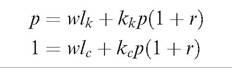

In order to explain this subject in the simplest way, we will use a model of an economy in which only two goods are produced, a consumer and a capital good, by means of capital and labour:

The price of the consumer good is taken as numeraire, w is the real wage, p the price of the capital good, r the rate of profit, which is equal to the rate of interest, lk and lc the labour coefficient in the two industries, and kc and kk the capital coefficients. With a few simple algebraic passages it is possible to obtain, from the two equations, a decreasing function linking wages and profit:

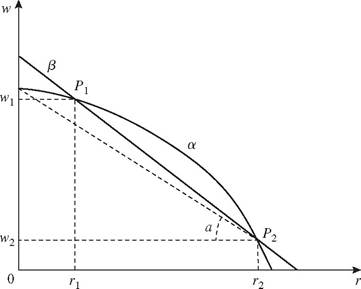

Fig. 19

Two different wage-profit curves have been drawn in Fig. 19. They represent two different productive techniques (two different systems of equations); let us call them a and β. The techniques differ in the ways in which capital and labour are combined, but it is also possible that one (or some) capital good(s) is (are) physically different in the two cases.

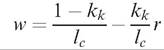

The concavity of curve a implies that in the technique a it holds kk∕lk > kc∕lc, whereas curve β is linear because kk∕lk = kcllc. In technique a the capital-labour ratio varies with variations in the price of capital and, therefore, with variations in the distribution of income, even without a change in the productive technique. In technique β, on the other hand, the aggregate capital-labour ratio does not vary with variations in the distribution of income, as prices do not change. Graphically, the capital-labour ratio is measured, for technique β, by the slope of line β. In fact, in the case in which kkllk = kc∕lc the preceding formula can be reduced to:

in which kk∕lc measures the slope of line β. For technique a, instead, the capital-labour ratio is measured, for example at point P2, by the width of angle a, and is different for every different point on curve a.

Let us now compare the two techniques in correspondence to different distributive patterns. At the points to the left of r1, the capitalists will choose technique β as, with respect to a, it gives higher profits in relation to each wage. Technique a will be preferred at the points between r1 and r2, while at those to the right of r2 technique β will be preferred again. This is the phenomenon of the ‘reswitching of techniques’: technique β, which had been abandoned following an increase in the rate of profit around r1, is preferred again when the rate of profit becomes still higher, i.e. higher than r2. At each of points P1 and P2 the two techniques are equally profitable and have the same price systems. Passing from technique β to a around point P1 there is a decrease in the capital-labour ratio. Such a change in the capital intensity of the techniques has purely real causes, as at point P1 the two techniques have the same price system. This phenomenon is known as the positive ‘real Wicksell effect’. In the movement from technique a to β around point P2, there is, therefore, a negative real Wicksell effect. In this case, with an increase in the rate of profit, the capital-labour ratio increases rather than decreases; and this occurs because of a real technical change. Also at the points between P1 and P2, the capital-labour ratio increases when the interest rate increases, but this occurs, in this case, only because the price of capital changes. This is the ‘price Wicksell effect’. The phenomenon of the increase in the capital-labour ratio following an increase in the interest rate is called ‘capital reversal’.

Broadly speaking, the root of the problem is that, if the economy produces heterogeneous goods, capital must be measured in value terms. When the real wage varies, the cost of labour changes in every industry and, since the incidence of labour input varies from one industry to another, the prices of goods change. As a consequence, the value of capital varies, not because techniques change, but as a simple consequence of the change in relative prices. This is the Wicksell price effect. In general, the capital-labour ratio may change in any direction and it may increase when the interest-wage ratio increases. This means that the capital intensity of techniques may increase when the capital ‘factor’ becomes dearer than the labour factor: the reverse of what marginalist theory predicts. In this case the phenomenon is caused by a perverse price Wicksell effect.

But things may be worse. When the real wage changes, capitalists are forced to change techniques, not only because the cost of labour varies, but also because, following the change in the price of goods, all production costs change. As a consequence, the quantities of capital goods used and the value of capital will change. This is the real Wicksell effect, and may be either positive or negative. If it is negative, the aggregate capital-labour ratio rises as the interest-wage ratio increases. Again: the reverse of what is envisaged by the marginalist theory. In this case the phenomenon occurs as a consequence of a genuine change in techniques and the physical quantities of capital goods used.

An old marginalist prejudice was propagandized by telling the following parable. When the employment of labour increases, given the employment of other production factors, its marginal productivity is reduced. Firms will be prepared to increase employment only if wages are reduced. In competitive equilibrium, the wage corresponds to the marginal productivity of labour, so it can be said that labour is remunerated according to its production contribution. In the same way, when employment of the ‘capital’ factor increases, its marginal productivity is reduced. Therefore, firms will be prepared to adopt more intensively capitalist techniques only if the interest rate is reduced. In competitive equilibrium the rate of interest remunerates the productive contribution of capital, corresponding to its marginal productivity, and is reduced when its use is increased. Well, this parable can no longer be told, because the use of capital may increase when its cost increases instead of when it decreases.

The conclusion can be generalized: it does not apply to capital alone, but also to all primary factors, land, for instance. The relation between the use of land and the use of labour may increase when the rent-wage ratio increases. This is also a result which came out of Sraffa’s work. However, it was explicitly brought to light by his followers, and most clearly in the essay by J. S. Metcalfe and I. Steedman, ‘Reswitching and Primary Input Use’ (1972).

11.2.3. Production of commodities by means of commodities

All the above is in Sraffa’s book, but only sketched out in its essentials; it is not surprising that orthodox theory needed several years of debate in order to bring out its theoretical implications. The fact is that this late product of the years of high theory is a concise, compact, and pared-down book which is not at all easy to understand. Nor is it easy to find the correct place for it, a place which it undisputedly occupies in the history of economic thought, given the scarcity of references supplied by Sraffa in regard to his sources.

The core of the model can be presented with the equation

where A is a matrix of technical coefficients of dimension n x n, lk a vector of labour coefficients and p a vector of relative prices. If the wage, w, is known, the system of n equations simultaneously determines the rate of profit and the relative prices of n — 1 goods.

With changes in w, the conditions of relative cost of the different commodities change, as the proportions of the utilization of labour and means of production in the diverse industries are different. Therefore, all the relative prices change. There is a decreasing function linking profit and wages. Profit is not related to a productive contribution of capital; in fact, the latter cannot even be defined in Sraffa’s model. In regard to distribution, the model simply states that, if one of the distributive variables is known, the other is determined residually.

Profit cannot be explained by the productive contribution of the capital ‘factor’ and its scarcity, but remains a surplus, the size of which depends solely on the social and technical relationships with which a given final output is produced capitalistically.

It is necessary to begin with this result to evaluate Sraffa’s work in a historical perspective. In this way it is possible immediately to reject the interpretations of Sraffa’s model which consider it as a special case of the

neo-Walrasian general-equilibrium model. These interpretations have little meaning, not because they lack an analytical basis, but because, by concentrating on the formal aspects of the model, they overlook its theoretical content. According to this point of view, Sraffa’s model corresponds to that special case of the inter-temporal-equilibrium model in which a uniform rate of profit is obtained.

What makes Sraffa’s model substantially different from the neoclassical approach is a series of important theoretical characteristics, for instance: the absence of the full-employment hypothesis; the refusal to consider prices as determined by supply and demand; the rejection of the notion of capital as a factor of production.

This leads us into the world of the classical economists and Marx, as also suggested by the theory of profit as a surplus. The classical economists and Marx made use of a dynamic which evolves through historical time. They assumed as given, at a certain moment, or over a very brief period of time (e.g. a productive cycle), the technique in use and the composition of the final demand. They did not study change by assuming that at every moment there is the possibility of choosing between the techniques and the final consumptions prevailing in different stationary-state economies. They believed that techniques and demand change through time and differ from one period to another; but also that, in each period, in each productive cycle, there is only one technique and only one final demand. So prices can change through time; and this can also be caused by changes in the final demand, as changes in the latter induce changes in techniques. Almost all of Sraffa’s book can be read from this point of view.

Therefore, to grasp the essence of the Sraffian revolution it is necessary to define more clearly Sraffa’s position in regard to the classical and Marxian approach. The point is that a ‘classical-Marxian approach’ does not exist, if it is true that Marx considered himself to be a critic of Ricardo and Smith. In other words, was Sraffa a ‘neo-Ricardian’, as some orthodox Marxists and some orthodox neoclassical economists have argued? Or was he a Marxist, as many of his followers have maintained?

The level of abstraction of Sraffa’s model is defined, albeit with the usual cryptic conciseness, by Sraffa himself, in the subtitle of his book: Prelude to a Critique of Economic Theory. It is the same as the first chapter of Capital, which is entitled ‘The commodity’, and which is the real prelude to the Critique of Political Economy. In that chapter, Marx tackled the analysis of the commodity and its value, and laid down the theoretical bases of all his successive work; he attacked the ‘vulgar economists’, whom he accused of looking for the explanation of the value of goods in exchange relations; and he linked himself explicitly to Ricardo in looking for it, instead, in the production sphere.

However, even though Marx had clearly pointed out that value is a social phenomenon, Ricardo’s influence induced him to determine the value of goods by ignoring the capitalist form in which they are produced. Value, according to the theory set out in the chapter on ‘Commodities’, depends solely on the quantity of labour employed in its production, its social determination being reduced to the way in which society allocates working activity among the various industries. In other words, value is not influenced by the way in which production is socially structured, nor by the way in which the social classes face each other in the production sphere. Thus, for example, the value of the social product does not depend on the way in which the product is distributed—a clear reminder of the Ricardian claim to measure value by making it independent from the variations in distribution. It is obvious that, in order to reach such a result, Marx had to rely on a high level of abstraction, and it is almost paradoxical that a book on ‘capital’ opens with a chapter in which capital is ignored. Now, it is almost as if Sraffa had rewritten that chapter, trying to reach the maximum level of abstraction, from returns to scale, growth, disequilibrium adjustments, even from the specific institutional structure to which the type of capitalist set-up may conform historically—exactly as in the chapter on ‘Commodities’. However, he made it clear once and for all that the only thing which it is impossible to ignore in determining the value of the commodities produced in a capitalist economy, is the fact that they are produced in capitalist conditions: that it is meaningless to abstract from the wage, as Marx did in that chapter. In other words, Sraffa took Marx seriously in his treatment of value as a social phenomenon—so seriously that he distanced himself from Ricardo more than Marx did himself.

It seems possible to conclude that, while on the subject of the determination of profit, Sraffa’s theory does not bring to light any basic analytical differences between Ricardo and Marx, on the subject of value his work can be read in only one way: the Prelude to a Critique of Economic Theory seems to us just like a first chapter of Capital which Marx would have written if he had been a little less Ricardian and a little more Marxist.

11.3.