Marshall and the English Neoclassical Economists

6.2.1. AlfredMarshall

By a thoroughly personal route, Marshall managed to offer the neoclassical paradigm an alternative theoretical outlet to that proposed by Jevons and, above all, a wider cultural perspective.

The method of partial-equilibrium analysis was his great invention and personal contribution to economics. Unlike Walras, and the whole Continental tradition in general, Marshall tended to favour realism and the explanatory power of the theory, rather than the logical coherence and formal elegance of its results. It is for this reason that he overlooked the interrelations among markets, in order to concentrate on the equilibrium conditions of a single productive sector. His favourite analytical instruments were the concepts of ‘industry’ and ‘representative firm’. An industry is a group of firms producing the same good; a representative firm is an ‘average’ firm endowed with the most important characteristics of the industry.Of course, Marshall was aware of the numerous relationships of interdependence that link markets to each other. Walras, on the other hand, had recognized the practical usefulness of the partial-analysis method. The fact is that the two great economists were focusing on different audiences: Marshall on the intelligent common man and, especially, on the businessman (this is why the formal mathematical aspects of his work are relegated to the appendices); Walras on colleagues and scholars in general (the notable mathematical apparatus of the Elements is accessible only to a few). It is important to point out that Marshall applied the partial-analysis method to goods markets but not to productive-factor markets. For the latter, he too, like Walras, formulated a ‘general-equilibrium’ model in which the relations between the products and the factors of production play an essential role.

Marshall is the classic example of the right economist in the right place at the right time.

Victorian England was sailing at full speed through the final years of the nineteenth century. And, with economic growth, a great optimism spread about the destiny of the industrial society. Real average wages increased constantly and technical progress gradually reduced the length of the working week.A typical Cambridge intellectual, Marshall studied theology, mathematics, and physics before finally coming to economics. He arrived just about the time when English academic circles were beginning to be influenced by the theories of Darwin and Spencer. Marshall studied Darwin’s theory of evolution, Christian moral philosophy, and Bentham’s utilitarianism, and managed to blend these three great streams of thought into an original synthesis. The result was a philosophy of evolutionary progress which implied that the whole society would tend to improve in material terms, and not only the strong and courageous few, as the social Darwinists had argued. In regard to his mathematical background, Marshall certainly benefited from being taught by the great physicist Maxwell and the mathematician Clifford. It was these influences that impelled him to introduce into economics the modern diagrammatical methods of setting out theory.

Marshall’s main contribution to economics is the Principles of Economics. The book was published in 1890, but the first draft goes back to the early 1870s, the period when the marginalist revolution was beginning. It was an enormous success and gradually, especially in England, displaced Mill’s Principles as the basic textbook in the main universities; a great deal of the methodology used in that book continues to dominate microeconomics textbooks today. In particular, the famous ‘Marshallian cross’ has preserved its mystique. With it, the great economist tried to combine the theory of production of the classical authors with the neoclassical theory of demand which he himself had formulated.

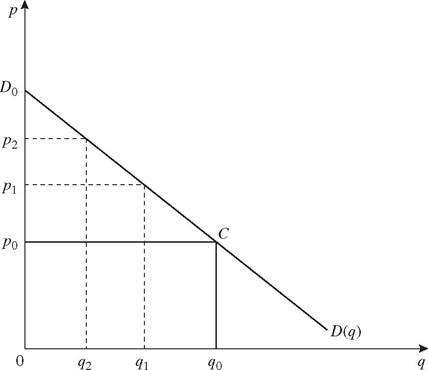

It is important here to point out that neither Jevons nor Walras had managed directly to connect the theory of utility to the theory of demand.

Instead, Marshall, with the hypothesis of a constant marginal utility of money, related the marginal-utility schedule of one good to the consumer’s demand schedule, and in so doing formulated the theory of the ‘consumer surplus or rent’.The theory offered a way of measuring the return, in terms of utility, that the consumer draws from exchange activity. The idea is to compare the marginal demand price that the subject is prepared to pay for a given quantity of good with its market price. D(q) is the demand curve, p is the current market price, and q the quantity demanded. At price p0 the consumer buys q0 by spending a sum of money equal to the area Op0Cq0. However, he would be prepared to pay p2 to obtain the quantity q2, p1 to obtain the quantity q1, and so on. This means that his actual outlay is lower than what he would be prepared to pay to obtain the desired quantity. Geometrically, this difference, which measures the consumer’s surplus, is shown by the area of the triangle D0p0C in Fig. 6.

The most important scientific approach of the period in which Marshall was educated was that of Newtonian physics, an approach whose logical coherence and theoretical strength nobody doubted. The task Marshall set himself was to make economic science conform to the dominant scientific method, highlighting the robustness of its foundations, the continuity of its growth, and the universality of its principles. This helps us to understand why he was opposed to the controversies about fundamental questions: he

Fig. 6

believed that these could weaken the scientific status of the discipline. It was for this reason that Marshall did not accept Jevons’s attack on Ricardo, going so far as to argue that it was only because of an inappropriate use of language that Ricardo could have given the impression of not considering demand as a determinant of value.

At the same time, Marshall maintained that the theory of supply and demand was not the scientific basis of economics. The central problem of economics, according to him, is not the allocation of given resources, but rather how the resources become what they are. The ‘science of activities’, as he called it, should have been a necessary supplement to the ‘science of wants’, but—as he stated in the Principles—if one of the two ‘may claim to be the interpreter of the history of man... it is the science of activities and not that of wants’ (p. 90). Furthermore, the positive functions of competition were not defined by Marshall in terms of efficient allocation of resources, but rather in terms of the stimulus competition gives to the discovery of improved methods of production.6.2.2. Competition and equilibrium in Marshall

The invention of the theory of perfectly competitive equilibrium has been traditionally attributed to Cournot. Cournot developed a notion of partial equilibrium by studying a market isolated from the rest of the economy. He distinguished between two kinds of equilibrium: single-producer markets and many-producer markets—in other words, a monopoly equilibrium and a competitive equilibrium. The competitive equilibrium was seen as a limiting situation, namely as the state of the market that would be realized if none of the economic agents had monopolistic power. As we saw in Chapter 5, this way of conceptualizing the competitive equilibrium was rejected by Walras. The Walrasian system assumes that the agents formulate their own plans and implement their own choices by taking prices as given. Marshall’s conception of competition and equilibrium is completely different from that of Walras, and rather nearer to that of Cournot.

First of all, Marshall clearly distinguished between market behaviour and normal behaviour. The former concerns the quantity of goods actually bought and sold at a given moment and at a given price. The latter, instead, reflects what the single agent decides to buy or sell ‘normally’ over a certain time-span.

The normal decisions depend on the ‘normal’ level of prices the agent expects to prevail during the period considered. Knowing, from experience, that the market price is usually different from the normal price, the agent will base his own daily decisions (if the day is the unit of time under consideration) on the current market price. However, his final aim is to realize, within the time span considered, his own normal decisions.The gap between market price and normal price will induce the agent to anticipate or delay the buying or selling of a certain good, but will not change his own ideas of what normal behaviour is, the latter constituting a sort of fixed reference point. Marshall considered normal prices to be subjective evaluations of the prices that are expected to prevail on the market at a particular time in the future; it is on the basis of these expected prices that the single entrepreneur decides on the size and type of plant to adopt. Marshall was very reticent about the mechanism of formation and revision of normal prices, but denied that these could be obtained in a direct way from observed market prices, as their average or by extrapolating from their past trend. If there is a causal link between market and normal prices, it seems to run from normal to market prices and not vice versa.

Second, there is a marked difference between Walras and Marshall in regard to their definitions of competition. In the Walrasian conceptualization, the agent in perfect competition is a price-taker: he considers the prices as given and not capable of being directly influenced by his own behaviour. Marshall, on the other hand, believed that a perfectly competitive market is one in which a large number of agents operate; each has objectives which conflict with those of the others, and will try to pursue them without entering into coalitions or blocs and without using special bargaining powers. Marshall’s ‘perfect competition’ does not presuppose that each agent takes the price of goods as given, nor that the firms are identical (even though they must be ‘similar’).

The small differences among firms play, in Marshall’s system, the same role as that of the genetic variations in Darwinian theory.Marshall distinguished between demand price, pd, i.e. the maximum price at which the demand reaches a pre-determined level, and supply price, ps, i.e. the minimum price that induces the sellers to offer a quantity equal to that predetermined. Given a certain level of demand, the market is in

202 disequilibrium if the demand price differs from the supply price. A disequilibrium situation tends to trigger the following reactions. If pd > ps, the sellers will react by increasing the volume of supply either by an increase in the production levels or by a reduction in the levels of inventories; vice versa, in the case in which pd < ps. In this way the existence of a disequilibrium produces first a variation in the quantities and only later, and as a consequence of these changes, a variation of prices. In general, Marshall’s sellers prefer to increase their own profits by acting on quantities rather than on prices, for the obvious reason that price manoeuvres may be difficult in situations close to perfect competition.

The method that Marshall adopted led him inevitably to an analysis of the conditions of supply: in the movement towards equilibrium he admitted variations in quantities, not only of the products but also of the factors, if these are reproducible. This is a point of contact with Ricardian economics, but it is only a partial contact. Marshall did not accept the producibility point of view to the point of accepting the Ricardian theory of value. He adopted a theory based on real costs, but these were reduced to labour and ‘waiting’, as in the work of Senior and Mill. It is not by chance that Schumpeter considered Marshall’s theory of real costs as ‘the olive branch presented to his classical predecessors’ (History of Economic Analysis, p. 1057).

6.2.3. Marshall's social philosophy

In The Present Position of Economics, his inaugural lecture for the 1885-6 academic year, Marshall put forward the view that the main duty of economics is the calculation of benefits of social and industrial change, bearing in mind the fact that the same amount of money measures a greater pleasure for the poor than for the rich. This is the same as saying that overall welfare increases if the the distribution of the ‘social dividend’ is adjusted in favour of the poor, up to the point of levelling marginal utilities for all subjects. The defence of redistributive economic policies proceeds, according to Marshall, from the utilitarian principle that the ultimate goal of economic activity is the maximization of collective welfare.

As a good student of Mill, Marshall was the initiator, within the neoclassical stream of thought, of that tendency which tried to reconcile a moderate laissez-faire with a reformist programme; and, just like Mill, he rejected the argument, put forward by the most determined free-traders of the period, that the only way to improve the conditions of the poor was to stimulate the egoism of the rich. His compromise position induced him to introduce into his system of thought principles and norms which were in clear contradiction with the dominant Spencerian ideology, and which brought him more than a little criticism. In Marshall, unlike Walras, there is

an inextricable interweaving among the economic, social, and cultural spheres of human activity, and a strong link between material and moral facts—a link that had important consequences for his way of conceiving, for example, State intervention in the economy.

Marshall was concerned to consider the main bearings in economics of the law of the struggle for existence, according to which ‘those organisms tend to survive which are best fitted to utilize the environment’ (p. 242). In particular, he was concerned to defeat the argument, put forward by the Social Darwinists of the period, that the State should not intervene in any way to modify the process of natural selection. From Social Darwinism however, he borrowed the evolutionist conception of history, a conception well summarized in the quotation appearing on the first page of the Principles: ‘Natura non facit saltus.’ Human progress is slow, and moves forward in small steps. Attempts to change society quickly are doomed to failure and, if pursued, only produce misery. Marshall admitted that over the course of the slow evolution of the social institutions a particular structure could emerge which would lend itself to the exploitation of one social group by another. However, the survival of such a structure through time would prove that its merits outweighed its defects.

This argument would apply especially to modern capitalism. Notwithstanding all its social costs and injustices, capitalism ensures productive and allocative efficiency and contributes to the elevation and progress of mankind. Marshall thought that human nature, as it had developed over centuries of war and violence, and of ‘sordid and gross pleasures’, could not be changed in the course of a single generation. In fact, when Marshall spoke of ‘sordid and gross pleasures’ he had already abandoned the pure utilitarian premisses. As we have seen with Mill, a social philosophy that discriminates between healthy and sordid pleasures is basically incompatible with utilitarian philosophy.

Marshall believed that the social and political dimensions of human action should always be taken into account by economics. The implications of this view for economic policy are notable. The State has the right and the duty to intervene in the economic sphere to regulate the market mechanism and to correct its distortions. His proposals for the introduction of corrective mechanisms such as co-operative movements, profit-sharing, arbitration on wages, and similar mechanisms into the English political-economic system seemed very modern to his contemporaries.

6.2.4. Pigouandwelfareeconomics

The principal aim of economics in Marshall’s Cambridge was understood in terms of welfare economics. The study of economic welfare must include, according to Marshall, the study of situations in which the market mechanism ceases to produce the beneficial effects expected from it, i.e. the study of ‘market failures’. This was the main interest of Arthur Pigou, Marshall’s successor as professor of economics at the University of Cambridge. In the Economics of Welfare (1920), Pigou stated that the object of welfare economics is represented by the circumstances most conducive to the increase of economic welfare of the world or of a specific country. The hope was to discover which type of intervention, by the government or by private bodies, would most favour such circumstances. However, Pigou made an important change in emphasis: the analysis of the operation of the competitive process and the historical perspective, which were such important elements in Marshall’s system, gave way to formal analysis.

Pigou’s most relevant contribution concerned his famous distinction between private and social costs. The main reason for the difference between the two categories was identified in the absence of constant returns. Pigou observed that, while industries with decreasing returns tend to become larger than is socially desirable, the industries enjoying increasing returns tend to remain too small. This led him to the conclusion that government intervention in the form of taxes and subsidies is necessary.

Marshall himself intervened to criticize the conclusions reached by his student in 1912. He pointed out that the apparent inefficiency of industries with decreasing returns was due to the fact that Pigou was using static analysis to deal with dynamic questions. In fact, Marshall defined the law of increasing returns in terms of the improvements in the organization which usually accompany an increase in demand. And this is the meaning of the famous proposition according to which the part played by nature in production shows a tendency towards decreasing returns, whilst the part played by man shows a tendency to increasing returns; which is tantamount to saying that man continually fights to find new ways to loosen or overcome the bonds of nature. In theoretical terms, this implies a clear distinction between a static analysis, in which costs increase as a direct function of output, and a dynamic analysis, in which costs change through time owing to talent and human effort. This is exactly the road that led Marshall to admit the irreversibility of the long-run supply curve: it is not likely that economies of scale, once attained by means of general economic progress, will disappear, even if the output of the sector decreases. This implies the impossibility of moving backwards and forwards along the same supply curve, and explains his suggestion that the curve should be redrawn each time ‘great additional economies are introduced’. On the other hand it is important to point out that, with irreversible supply curves, the usual textbook description of the long-run equilibrium of a sector no longer makes sense. Marshall must have been aware of this, as in the fourth edition of the Principles he wrote: ‘The Static Theory of equilibrium is only an introduction to economic studies; and it is barely even an introduction to the study of the progress and development of industries which show a tendency of increasing return’ (p. 461). This insistence on growth and competition as the agents of progress is an important part of Marshall’s thought—a part which was not, however, perceived by his follower, obsessed as he was with the need to confer formal rigour on his master’s work.

So Pigou, in his attempt to give an authorized interpretation of Marshall, ended up by translating his long-run analysis into the language of static competition, and this was later to pass into microeconomic textbooks. In the course of this translation, Pigou redefined the Marshallian representative firm as one in search of an equilibrium position, and identified the Marshallian equilibrium as the perfect competitive equilibrium. Moreover, the long-run equilibrium position of the firm was made to coincide with the minimum point of the famous U-shaped long-run average-cost curve, with which the whole problem of increasing returns was reduced to a mere question of external economies. By placing the concept of the equilibrium of the firm at the centre of his analysis, Pigou was finally led to define an industry as a collection of firms in static equilibrium. It was in this way that the most interesting parts of Marshall’s work, those concerned with dynamics, were left aside. All this was the work, not of an enemy, but rather of a ‘loyal but faithless Marshallian’, in the brilliant words of Robertson.

6.2.5. Wicksteed and ‘the exhaustion of the product’

Wicksteed’s name is irrevocably linked, not so much to his most ambitious work, An Essay on the Co-ordination of the Laws of Distribution (1894). This work contains the first explicit definition of the production function. There is also the first explicit formulation of the problem of the exhaustion of the product. We have already noted that we owe to Menger the idea of explaining all the distributive shares in terms of marginal productivity, but we recalled that Menger’s theoretical system, at that time, fell on deaf ears in England. While it is true that there are traces of the problem in the first edition of Marshall’s Principles, Wicksteed was the first scholar to treat the matter systematically. The same subject was tackled a few years later by Clark, Barone, and others, whom we will discuss later.

Unlike the Ricardian approach, which adopts diverse theories to explain the different distributive shares, marginalist thought uses a single law, that of decreasing marginal productivity. All the factors are considered in the same way: they all receive a share of the national income which is proportional to their respective marginal productivities. The quantity produced is determined by the sum of the resources employed, and depends on technological causes, while the remunerations of the factors are determined by the forces of supply and demand and depend on the structure of the markets. Produced income and distributed income are therefore independent magnitudes and determined according to different rules, so that there is no reason to expect them to be always equal. On the other hand, a situation in which the sum of the distributive shares is higher or lower than unity would be unacceptable from a logical point of view. In the first case, in fact, after having paid for each resource according to its own marginal productivity, there would be a residue without an owner; in the second case, it would seem that the resources employed do not produce enough to receive a remuneration proportional to their own marginal productivity. In both cases, the logical coherence of the theory is irremediably compromised, unless one is prepared to re-introduce a non-marginalist concept to explain some type of remuneration. This is why it is necessary to prove that the product is ‘exhausted’ in the factor shares.

Assume for simplicity that there are only two factors of production, labour and capital. By indicating with w and r the unit prices at which their services are paid and with L and K the quantities employed, the problem is to prove that: pY = wL + rK, where Y denotes the volume of output and p its price, w the wage rate and r the rate of interest. The quantity produced, Y, is determined by the amount of the employed resources according to the production function Y=f(K, L); the factor remunerations are determined according to the rule which states that w = pY'L and r = pY'κ, where pY'L is the value of marginal productivity of labour and pY'κ is the value of marginal productivity of capital.

The problem can be solved if it is possible to express Y in the following way: Y = Y'lL + Y'κK. In this case, in fact, multiplying both sides of the equation by p we obtain: pY = pY'LL + Y'κK. Now, a sufficient and necessary condition for Y = Y'lL + Y'κK is that the production function is homogeneous of first degree, i.e. that it exhibits constant returns of scale. Under these conditions it is possible to apply the famous Euler theorem. But it is obvious that this solution, made to save the formal rigour of the theory, excessively restricts its field of application. However, Wicksteed did not share this point of view; on the contrary, he was so convinced of the plausibility of the hypothesis of constant returns of scale that he did not even attempt to justify it. And it was precisely against the empirical relevance of Wicksteed’s conclusion that Pareto was to launch his 1897 attack: the theory is not universally valid, both because there are cases of productive processes with decreasing or increasing returns of scale and because the processes are often characterized by fixed proportions in the employment of factors, so that it is impossible to define their marginal productivities. Note that this kind of criticism does not undermine the logical structure of the theory but only its empirical relevance. In any case, apart from problems of realism, Wicksteed’s solution cannot be considered adequate, as it is incomplete. It assumes a fact that is not proved: that the market laws allow for the factors to be paid according to their marginal productivities, i.e. that w = pYL and r = pYK. What kind of market structure would guarantee this result? We had to wait first for Wicksell and then for Robinson for a decisive step forward towards a complete solution of the problem.

An important aspect of Wicksteed’s thought has recently come back into vogue: his thesis that economic theory need not accept the assumption of self-interested behaviour on the part of the agent, as Jevons, Walras, Edgeworth, and others had believed. In his opinion, the ‘specific characteristic of any economic relation is not its underlying egoism, but its non-tuism’. (The Common Sense, p. 180). With this latter expression, Wicksteed meant that in an economic relation, A’s lack of interest in the aims of B and vice versa, does not imply that A acts solely out of self-interest. In fact, ‘the economic relation does not exclude from my mind everyone else but me; it potentially includes everyone else but you’ (p. 174). Thus, ‘it is only when my conduct is guided by tuism that it ceases to be fully economic. It is therefore senseless to consider egoism as the characteristic trait of economic life’ (p. 179). He concluded that ‘the proposal to exclude benevolent or altruistic motives from the study of economics is... utterly irrational’ (p. 180). In other words, the economic sphere is defined by the impersonality of relations rather than by the self-interest of economic agents—a conclusion which today is more than ever at the centre of the debate on the anthropological foundations of economic discourse.

6.2.6. Edgeworth and bargaining negotiation

Edgeworth was a remarkable figure in the theoretical scene of those years. Thanks to his exceptional analytical ability and his mathematical background, much more solid than the standard of the period, he was undoubtedly one of the ‘founding fathers’ of econometrics in its original meaning of ‘systematic application of mathematics to economics’. In this he played a prophetic role, anticipating what has become the undisputed research line to follow in recent years.

His main work, Mathematical Psychics (1881), is a short book in which he tackles, in incredible depth, some of the burning questions in economics. To understand its meaning it is necessary to recall Edgeworth’s great admiration for classical mechanics, from which economics should ‘learn’ the style of argument and logical reasoning so as to obtain results of the same exactness and elegance. Such admiration was perhaps, at least in part, due to the intellectual exchanges Edgeworth probably had with the great Irish physicist, William Hamilton, a friend of his father. In the years in which Edgeworth was educated, Hamilton had already been working for some time on an elegant and unitary ordering of mechanics which still carries his name today. Edgeworth’s arguments are difficult, as they make extensive use of techniques, such as the calculus of variations, that are still today not widely applied. Moreover, his literary style, which is rich and full of quotations but also often obscure, coupled with his natural humility and shyness, explain why, despite the consideration he enjoyed during his life, the full value of his work were only understood several decades after his death.

Edgeworth made a passionate plea for mathematical economics; a plea based on the observation that economics, unlike mechanics, generally works, not with exact functional forms, but with indefinite forms of which only a few properties are specified. In other words, he considered mathematical economics as essentially a qualitative discipline.

Edgeworth is probably remembered today with more admiration for the second part of his book. In it, after having defined the economic agents as being driven only by self-interest, he exposed the famous theory of bargaining negotiation, in which the process of exchange is seen as a series of negotiations and renegotiations which only stops at the moment when the individuals are no longer motivated to revise the agreements already made. Unlike the Walrasian tatonnement, in which it is the auctioneer, an almost metaphysical being, who co-ordinates the choices of the individuals, in Edgeworth’s bargaining process it is the individuals themselves who, by trying very hard to reach an optimum, end by bringing the system to equilibrium. It is easy to see that this analysis is enormously more complicated than that of Walras. In particular, the problem of the uniqueness of the equilibrium becomes very delicate. Edgeworth showed that in an exchange economy with two individuals, given the initial endowments, there may be a continuum, the famous ‘contract curve’, of attainable Pareto-optimal points. He also noted that this curve shrinks with the increase in the number of economic agents, but that nothing definite can be concluded about its asymptotic behaviour when the number of agents changes. His contemporaries did not realize the importance of Edgeworth’s bargaining theory, which was too far ahead of its times. Only later, with the work of Shubik, Scarf, Debreu, and Aumann, has Edgeworth’s bargaining theory flourished, giving life to ‘core’ theory. With this development it has been possible to determine the asymptotic structure of the set of equilibria (the multiplicity can persist asymptotically) and to prove that bargaining can generate equilibria which cannot be obtained by means of Walras’s tatonnement. Besides this, the two sets of equilibria tend generally to coincide asymptotically only under certain regularity conditions.

Walras himself was convinced of the possibility of situations in which the competitive equilibrium is not unique; but Edgeworth’s bargaining theory turned out to be more suitable for tackling the problem of the disequilibrium. In Edgeworth’s world, where single individuals make the adjustments, the system can never reach equilibrium, even in not too unusual cases, or can jump sharply from one equilibrium to another, even with small disturbances. Furthermore, the bargaining theory also shows that the adjustment mechanism can drastically modify the set of possible outcomes of the market process, an idea which only today has been fully understood, mostly thanks to the analytical apparatus of game theory.

The third and final part of Edgeworth’s book deals with the classic problem of the behaviour of economic agents. Going back to Bentham, Edgeworth assumed that behaviour is aimed at the maximization of

209 individual satisfaction and that it can be described as a procedure of constrained maximization of a utility function, for which he proposed some possible specifications. In his work he derived direct inspiration from the work of physio-psychologists such as Fechner and Helmholtz. However, the problem in which he was most interested was this: how to infer the best social distribution of resources from the individual preferences, once these have been specified. He also assumed, not only that utility can be cardinally measured, but also that it is not necessary, in order to do this, to resort to a measurement scale with an arbitrary origin, such as the one used for temperature. He was coherent with his premisses and concluded that, in order to maximize collective welfare, it was precisely those individuals who had the greatest ability to ‘experience satisfaction’ who should receive the greatest quantity of resources. And some limiting cases could even occur in which one individual should receive all the available resources. It is only a short step from here to the conclusion that the individuals who are at the top of the scale of evolution should be privileged, even if Edgeworth observed that, generally, the analysis of this problem cannot lead to a well-defined and fully satisfactory answer from a logical point of view.

Still today the ingenuous utilitarianism of that reasoning is not considered too implausible, and modern welfare theory is still firmly based on utilitarian foundations of this type, just a little more sophisticated. However, the shades of eugenics in Edgeworth’s analysis do have a sinister sound, and certainly represent the most dated parts of his work. On the other hand, it could be said that Edgeworth, rather than trying to prove the scientific nature of some of his ideological prejudices, wished to demonstrate that even the most complex social phenomena can be described in an ‘exact’ way in terms of certain pseudophysical laws. Two interesting curiosities arise here. The famous ‘Edgeworth’s box’ was not invented by the English economist at all. It was sketched for the first time in Pareto’s Manuale of 1905. On the other hand, it was Edgeworth who put forward the notion which was later to be known as ‘Pareto- optimality’. He did it for the first time in his Mathematical Psychics (1881).

6.3.