Mercantilism

1.2.1. Bullionism

We should immediately point out that a school of thought that defined itself as ‘mercantilist’ has never existed—even as a current of opinion aware of its own theoretical homogeneity.

However, there is no doubt that Adam Smith was to a degree correct in placing in the category of ‘trade or mercantile system’ the group of economic ideas that dominated European political and commercial circles in the sixteenth and seventeenth centuries and most of the eighteenth. A common theoretical core did exist, and this not only permitted debates and dialogues but also gave a certain homogeneity to the various national economic policies. What is difficult is to identify a ‘system’ in those ideas. It would be at least necessary to admit some important differences connected with national characteristics, and also to admit a minimum of historical evolution. We have insufficient space here to consider the national differences, except for a few points which will be mentioned when necessary; however, historical evolution cannot be ignored.For simplicity’s sake, we will follow Cannan’s suggestion and distinguish bullionism from mercantilism in its strict sense, even though we are well aware that this classification is a little forced.

Bullionism had dominated the opinions circulating in the European courts up to the end of the sixteenth century. It was characterized by the conviction that money, or gold, was the wealth. Now, there is obviously no doubt that money is wealth. The mistake, according to Smith, was the belief that it was the only form of wealth. However, it is doubtful that there have ever been economists who really thought in this way. Rather, there was a widespread opinion that treasure was the only type of wealth worth accumulating—an opinion which had more than a grain of truth from the point of view of the State, in an era in which wars were won with gold.

This idea also accorded well with the merchant’s point of view, for whom money was capital and, actually, the only type of capital capable of increasing in value. In fact, it was clear to almost every economist of the period that money was a means of increasing wealth and power. What many of the bullionists did not admit was the idea that that means should be used to increase the welfare of people, the wealth of nations, as Smith claimed. But why should the State and the merchants have had to pursue such an objective? In fact, the first bullionist economists, when they were not merchants, were administrators of the sovereign’s private finances rather than civil servants; in other words, they were still concerned with a household economy. This was certainly true of the German cameralists, who worked at the Kammer, or treasury, of the sovereign; and the same was true for many of the Spanish bullionists. They had good reasons, therefore, to work towards rulers’ private goals.The real mistake made by these economists, however, and the one which distinguishes them from the mercantilists of the following century, was in the methods they suggested for achieving these objectives. A wide circulation of money within the national borders was considered to guarantee an extensive tax base; therefore, the outflow of precious metals had to be prevented. The simplest way to do this was to prohibit the export of gold and silver, a method that was applied rigorously, sometimes even ferociously, in many countries. Another measure often adopted was that of raising the purchasing power of the foreign currencies by law within the national territory, so as to induce an inflow of money from abroad. Besides this, there were also attempts to force national companies to pay for imports with goods instead of money. Finally, a measure that was used above all in Spain was that of the ‘balance of contracts’: buying from each foreign country an amount of goods which did not exceed the amount exported to that country.

Another bullionist ‘mistake’ was the tendency to seek the causes of a systematic outflow of precious metals solely in monetary factors, namely, in the deviations of exchange rates from the parity determined by the metallic content. Such deviations were attributed to illegal behaviour, forgery, and manipulations by bankers and merchants. But the Crown also, often and willingly, resorted to illegal monetary techniques, such as ‘clipping’, i.e. reducing the metallic content of the currency in relation to face values, or ‘raising’, i.e. increasing, by means of a proclamation, the official value of the currency in relation to its metallic content. There were many learned investigations in this field, some of which led to the formulation of an important economic law, ‘Gresham’s Law’, according to which bad money drives out good. If, in a country, two types of currency circulate which have the same nominal value but different intrinsic values (because one of the two has a lower content of precious metal, because it is a forgery or worn), the public will tend to use the bad money for internal payments. The good will be hoarded, melted down, or used for international payments, and will therefore disappear from circulation.

In regard to the naming of this law, it is worth pointing out that in 1857 its discovery was attributed to Thomas Gresham by Henry McLeod, who later changed his mind and called it the tOresme-Copernicus-Gresham Law’. Gresham provided a precise formulation of the law in a letter to Queen Elizabeth I. Today it is known that the first formulation goes back to 1519 and is owed to Nicholas Copernicus, even if some hints of it can be found in Nicolas Oresme.

1.2.2. Mercantilist commercial theories and policies

Bullionist doctrines were still professed in the seventeenth century. For example, Gerald de Malynes sought the basic causes of a disequilibrium in the balance of trade in the alterations in the exchange rate. The most interesting part of Malynes’s arguments, however, is not bullionist, and can be summarized in the following way.

An exchange rate which is higher than the metal parity leads to an outflow of precious metals which diminishes the amount of money in circulation in the country under consideration. This reduces prices and worsens the terms of trade. Consequently, the trade deficit increases. There are two interesting aspects to this way of thinking: the use (albeit in an approximate way) of the quantity theory of money, and the implicit hypothesis of a low price elasticity of imports and/or exports. We will consider this later. Less interesting is the solution proposed: the intervention of the ‘royal exchanger’ against illegal practices and monetary manipulations, which had, according to Malynes, the sole responsibility for the fluctuations of the rate of exchange.Counter-arguments were advanced by two learned merchant adventurers who disdained neither science nor politics: Edward Misselden and Thomas Mun. Misselden overturned the theories of Malynes: it is the surplus or the deficit on the balance of trade which makes the rate of exchange vary, and not the other way round. Rather than worry about the exchange rate, the State should encourage exports and discourage imports. This is the gist of the mercantilist doctrine, a doctrine which was expressed perhaps more systematically by Mun than by any other contemporary economist. While Malynes placed great emphasis on the particular trade balances of one country with each other country, taken singly, Mun showed that what really mattered was the overall balance of trade. The inflow and outflow of gold depends on the general balance of trade, and the State should pay direct attention to this. Thus it was permissible to maintain a commercial deficit with some countries, such as those from which raw materials were imported, if this was conducive to the increase of the national production of industrial goods. Many of these goods could be sold abroad at high prices, because of the monopolistic advantages associated with the superior technology required to produce them.

From the point of view of the birth of political economy, the identification of the interests of one particular social class, the merchant class, with those of the collectivity, was extremely important. In this way, economics ceased to be ‘domestic economy’ and became ‘political’. The profits of that class, profits upon alienation, were obtained from an excess of the value of sales over purchases. This gap gave rise to the accumulation of money. The entire nation was considered as a great commercial company. Its net inflow of gold corresponded to the excess of its foreign sales over and above its foreign purchases. And, as with the merchant, the nation would also have to avoid keeping its stock of money idle. It had to reinvest it in the form of stock, in order to buy (import) the goods necessary to produce new goods; with these it would be able to increase sales (exports) and profits (trade surplus). Although production, and therefore the transformation of the imported raw materials, played an important role in this way of thinking, it was still only the excess of sales over purchases which was seen as the source of profits, for the collectivity as well as for the individual.

The theory of economic policy that sprang from this doctrine was simple. Commercial policy had to be protectionist. Export duties had to be abolished and import duties raised. Moreover, exports should be encouraged by incentives and imports hindered as far as possible and even forbidden in certain cases. These principles were rigidly followed by the French customs tariffs instituted by Colbert in 1644. England moved in this direction especially towards the end of the seventeenth century. However, certain very important exceptions were made: the import of raw materials, which were considered useful to the national industries, was not to be obstructed, while the export of important raw materials such as wool should be forbidden.

Mercantilist commercial policy also favoured national shipping; and many measures were taken aimed at reinforcing the merchant navy.

The 1651 English Navigation Act, for example, prohibited the importation of goods on non-British ships. This cultural attitude also influenced colonial expansion policy, in relation especially to the demand for the mother country’s products and for the supply of low-cost raw materials that were expected to come from the colonies. Finally, it is important to mention the policy of conceding privileges and monopoly rights to the great national commercial companies. The British East India Company was founded in 1600, and the Dutch in 1602.The mercantilist industrial policy aimed at encouraging productive activity within the national territories by the concession of monopolistic privileges, State subsidies, and tax exemptions to national enterprises, as well as by the importation of advanced technology, the acquisition of manufacturing secrets, and the encouragement of the immigration of skilled workers. The industrial policy even included the creation of State factories. In this field French mercantilism again excelled: Colbert brought industrial policy to obsessive levels, to the point of administrative prescription of measures relating to production and quality control.

1.2.3. Demographic theories and policies

Mercantilist theories and policies were also worked out in regard to demography. The problem was how to ensure an abundant labour supply to satisfy the expansion needs of the emerging industries; the policy aimed at increasing the population (we are still a long way from the Malthusian obsessions of the nineteenth century). This policy was put into practice with particular effectiveness in Germany, with the abolition of pre-existing prohibitions on some types of marriage and the awarding of prizes for large families.

It is possible to speak of a mercantilist psychosis in regard to population scarcity. Even in countries like Italy, in which there was no real scarcity of population, the demographic mania spread—so much so that the first hints of the ‘population principle’, later to be called ‘Malthusian’, did not cause a great deal of concern. For example, Giovanni Botero outlined the tendency of the ‘generative power’ of mankind to grow more rapidly than the ‘nutritive power’ of the nations, but concluded that this was just one more reason to develop production; in the worst case, emigration could be used as an escape valve.

This obsession with demographic growth can be explained only partially by the continual and thirsty demand for soldiers in a period of permanent warfare. There was also an economic motivation which had a certain theoretical importance. The mercantilists had a rather peculiar wage theory, according to which maximum labour supply occurs at subsistence wagelevel. If wages increase above this level, the supply will diminish rather than increase. The most ingenious justification of this theory was given in terms of ‘morals’: workers were considered to be depraved people, attracted by vice and excesses in eating and drinking: if they were paid more than subsistence wages, this would encourage depravity and laziness and thus reduce the labour supply.

A less ideological explanation of the phenomenon should be based on an understanding of the working conditions in the emerging industries and the difference in living conditions between the countryside and the town. The first point can be simply dealt with. Only a problem of physical survival would induce the workers to accept working 13-14 hours per day. In these conditions it was understandable that an increase in the daily wage could cause an increase in the demand for leisure, and perhaps for alcohol. What could be a worse crime against Christian morality? This is the first cause of the strange shape of the labour-supply curve which the mercantilist economists had in mind. The second cause was that the rural-urban migration was of a ‘push’ type (caused, for example, by the enclosures) rather than ‘pull’ (due to the attraction of the towns), for the living conditions in the towns were worse than in the countryside. Therefore, a slight increase in industrial wages would not encourage any significant increase in the

Fig. 1

industrial-labour supply. This second factor could account for the low elasticity in the labour supply. But the supply curve would even become negatively sloped owing to the former factor.

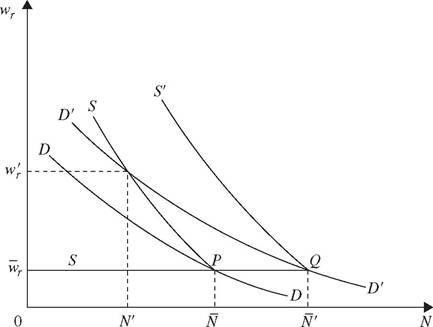

The theory can be illustrated by making use of a supply curve such as SS in Fig. 1. wr is the real wage, wr the subsistence wage, N the quantity of labour, and N the full employment level. The labour supply curve is infinitely elastic at the subsistence wage-level: at that wage, all the available labour power will offer itself in order to guarantee survival. A lower wage is not possible, simply because it would not ensure survival. Once full employment has been reached, each increase in wages would allow the workers to take some time off, and the supply curve would become negatively sloped.

Let us begin from point P, a full-employment situation at the subsistence wage-level and with a demand curve such as DB. An increase of accumulation would cause the demand curve to move to D'D'. The wages would increase to w'r and the labour supply would be reduced to N'. In conclusion, if the enrichment of the nation is not to be slowed down by the depravity of the workers, it is necessary to ensure that the population grows at least as fast as the stock (of capital). If the supply curve shifts to SS', employment rises to N', and the wages return to wr; the new equilibrium point will be Q.

The problem of the labour market, in the period of primitive capital accumulation, was not so much that of high wages, as the manufactured products were mostly sold in imperfectly competitive markets, and therefore at remunerative prices, but rather that of a labour supply that had difficulty in keeping pace with the expansion of industry and trade. For example, Josiah Child was extremely worried about the demographical problem, as were all the mercantilists, but he was not so concerned about the problem of wages. Although he was not against a low-wage policy, Child also maintained that high wages were not generally a bad thing; or, rather, that they should be seen as a consequence of the high level of wealth of a country, while low wages would be indicative of poverty.

1.2.4. Monetary theories and policies

Let us now consider monetary theory. The mercantilists made the first formulations of the quantity theory of money. The price revolution which occurred in Europe after the discovery of America, and which caused a century-long inflationary process, could not pass unnoticed. The relationship between the increase in prices and the increase in the amount of gold in circulation had already been noticed by the early Spanish mercantilists. The first hints at this relationship were made by some students of the Salamanca School, to whom we will return in section 1.2.6.

A cognisant formulation of the quantity theory was proposed by Jean Bodin. It was stimulated by a thesis of Jehan Cherruyt de Malestroict, who had asserted that the increase in prices which had occurred in France was only apparent. Prices, according to him, had increased in terms of the monetary unit, because of ‘clipping’; but, as the precious-metal content of the coinage had diminished, prices had not increased at all in terms of gold. Bodin pointed out that this argument only partially explained the inflationary process: prices had increased in terms both of the monetary unit and of precious metal, and the latter factor was more important. He demonstrated, with the aid of quantitative data, that the main cause of the increase in prices was to be found in the increase in the amount of gold in circulation. After Bodin the quantity theory was adopted by many other mercantilists. There are clear expressions of it in John Hales, Bernardo Davanzati, and Antonio Serra.

However, from the middle of the seventeenth century there was an important theoretical change. The quantity theory was still widely accepted by the mercantilists; yet it was no longer interpreted as an explanation of price levels, but rather as a theory of the level of transactions. This belief became so common that the few economists who did not accept it and remained faithful to the old quantity theory were considered almost as revolutionaries. We will treat this point in the next section, when we outline the theories of some of the forerunners of classical economics.

This change in point of view was probably connected to the end, between 1620 and 1640, of the century-long inflationary process that had begun with the discovery of America. The trend of increasing prices, which had started at the beginning of the sixteenth century, levelled out in the seventeenth and remained so until after the middle of the eighteenth. The second half of the seventeenth and the first half of the eighteenth century also represented a period of depression. The flow of gold and silver from the Americas was drastically reduced, and the struggle among the European countries to obtain precious metals almost became a ‘zero sum’ game.

Economists and merchants were no longer worried about inflation but about the lack of the availability of money to finance trade. A widespread idea was that ‘money stimulates trade’. The increase in the inflow of precious metals caused by a surplus in the balance of trade, in a period in which it was only possible to increase internal monetary circulation by a reduction in external spending, was seen above all as the necessary condition for an increase in production and, therefore, in wealth—to the extent that protectionist policies were often linked to the advice, specifically directed to the sovereign, not to hoard money: to increase the State treasury would do nothing but take money out of circulation.

Two mechanisms were indicated by means of which the increase in the money supply would have stimulated the levels of activity. The first is a direct mechanism, consisting of the rise in incomes and consumption caused by the increase in the money supply. This argument was supported, for example, by Jacob Vanderlint and by John Law. The latter clearly identified the hypothesis on which that argument was based, which was that prices do not vary in a substantial way with variations in demand (although Law limited the validity of this hypothesis to non-durable goods). In other words, the supply curve was assumed to be almost horizontal. With this, inflation, if it exists, is creeping, while its effects are in any case positive, because the increase in profits encourages further production and capital accumulation.

The other mechanism was indirect, and consisted of the reduction of the interest rate caused by the increase in the quantity of money. Some mercantilists had (as Keynes has pointed out) a monetary theory of production and interest: money is used to stimulate production and trade; interest is the price that is paid to obtain this use. It is also worth noting that the old term for ‘interest’ is ‘use’, a term which John Locke, at that time, still adopted as a synonym for ‘interest’. This price depends on the supply and demand of money. Thus ‘the abundance of money reduces usury’, argued Malynes. Misselden, his main critic, did not disagree with him on this point when he suggested that ‘the remedy for usury may be the abundance of money’. Cantillon observed, in his Essai sur la nature du commerce en general, that ‘it is a common idea, received of all those who have written on Trade, that the increased quantity of currency in a State brings down the price of interest, because when Money is plentiful it is more easy to find some to borrow’ (p. 213).

Thus, an increase in the quantity of money, ceteris paribus, allows for a reduction in the price of credit and therefore in the cost of financing investments, in this way encouraging economic expansion.

The level of interest was, understandably, another of the mercantilists’ obsessions, due to their strong identification with the merchant’s point of view. Any policy aimed at reducing the level of interest was positively evaluated, while any theory able to justify this was considered useful—so much so that many mercantilists, while adopting monetary theories of interest, did not hesitate to accept points of view from scholastic thought in order to justify measures against usury and to request state intervention aimed at lowering the rate of interest by law. Keynes found value in this mixture of theories. If value there is, it is perhaps to be found in the fact that such theories form the embryo of a monetary-institutional theory which was to be elaborated by Marx and to which the theory of Keynes himself can be traced back. If interest depends on monetary forces, its long-term trend is not an equilibrium value determined by real variables but simply an average of short-term values, an average which basically depends on institutional factors.

1.2.5. Hume’s criticism

One of the principal criticisms of mercantilist thought was put forward by David Hume in the Political Discourses (1752). Hume’s idea was that an increase in the circulation of money in a country with a trade surplus would increase prices (while it would reduce them in countries with a deficit). The consequent loss of competitiveness would rebalance, sooner or later, the balance of payments and halt the outflow of gold. Therefore, mercantilist commercial policies would have been, in the best of cases, short-lived. In the long run they would have been useless. From the theoretical point of view, they seemed to ignore the quantity theory of money.

The adjustment mechanism of the balance of payments theorized by Hume, and known as the price-specie-flow mechanism, was also described with a certain precision by Joseph Harris. Later, it was accepted by the classical economists and even by Marx, not only as a criticism of mercantilism but also as a description of a general economic law. All this is rather strange, as the mercantilists were aware of the problem raised by Hume. Cantillon, for example, had clearly defined the problem thirty years before, even if, and significantly, he had limited the loss of competitiveness caused by internal inflation to the industrial sector. Moreover, he had pointed out that the increase in the imports of consumer goods directly caused by an increase in monetary incomes could also contribute to reduce a trade surplus.

Mercantilist thought, however, contained all the elements necessary to rebut Hume’s criticism; they had been clearly formulated even by Cantillon himself. First, the mercantilist economists were aware of the relationship that links the quantity of money to the value of transactions. As we have mentioned above, in most cases, especially in the seventeenth and eighteenth centuries, they interpreted it, not as a theory of the level of prices, but rather as a theory of the level of output. Second—and this is the argument put forward by Cantillon but already present in the work of Malynes and many other mercantilist writers—even if an increase in the quantity of money in a country with a trade surplus causes, at least partially, an increase in the level of prices, this could cause, owing to an improvement in the terms of trade, a further increase in the trade surplus rather than a rebalancing effect. The implicit hypothesis in this way of thinking is that of a low price elasticity of imports and exports. Under such conditions, an increase in internal prices with respect to international prices would cause an increase in the value of exports rather than causing changes in the quantities of imports and exports. Thus, an improvement in the terms of trade would reflect positively on the balance of payments.

Therefore, the mercantilist theories were robust from the logical point of view, although the realism of the hypotheses on which they were based should be verified. Obviously, this is not the right place to undertake such an analysis. However, there is reason to believe that behind the theoretical jump made by Hume there was a real historical change. Probably, in the preindustrial period the elasticity of exports was not very high, given the marked productive specialization of the various countries. In particular, the elasticity of imports of the imperialist countries must have been low, as imports mainly consisted of food supplies, raw materials, and luxury goods, which were not produced internally. However, it is probable that, as manufacturing production developed in the main capitalist countries, a certain amount of price competition gathered steam, at least for that type of production; and this could have increased the elasticity of exports and imports. It is significant that Cantillon, in 1730, limited the effects of the monetary price-specie-flow mechanism to manufacturing production. Perhaps at the time of Hume and, later, of Smith, this effect had become dominant.

1.2.6. Theories of value

The mercantilists also had, to a certain degree, a common point of view on the subject of value, at least in the sense that almost all the authors concerned with this problem in the sixteenth and the first half of the seventeenth century looked for the solution in the same direction: namely, towards utility. It was only at the end of the seventeenth century that some scholars with partially mercantilist backgrounds, such as Petty and Locke, decidedly distanced themselves from the dominant view on value and looked for the solution of the problem in the costs of production. We will say more about this later.

It is not surprising that the mercantilists looked mainly to exchange as the real source of wealth and profit. In fact, the merchant earns profits, not because he controls the productive process (a control which, at least in the first phase of industrial development, was still in the hands of the craftsman), but rather because of the power he manages to exercise on the market. The merchant’s profit originates from the difference between the selling and buying prices of goods. He believes, therefore, that it originates from the trading process. Thus, a knowledge of the determinants of market prices is crucial in order to understand the origin and the growth of profits. Attention must be mainly focused on the forces that determine the demand for the goods, and demand is easily linked to utility.

In 1588 Bernardo Davanzati made an interesting attempt to construct a utility theory of value. He had been impressed by a passage from the Natural History by Plinius in which a story is told of a mouse sold at a very high price during the siege of a city. Davanzati explained the phenomenon by arguing that the value of goods depends on their utility and rarity. It is not absolute utility that counts, but rather utility in regard to the quantity available. The effect of greater scarcity would be to increase the use value of the goods and therefore the price at which they can be sold. This theory was taken up again in 1680 by Geminiano Montanari, a disciple of Galileo who had been influenced by the solution Galileo himself had given to the paradox of water and diamonds. Montanari argued that ‘it is the desires of men which measure the value of things’, so that the prices of goods will vary, ultimately, according to changes in tastes. Desires must be related to the rarity of the objects desired. With the same amount of money, or—as we would say—given demand, the greater the scarcity of the objects the higher they will be valued. Besides this, Montanari also made an interesting attempt to establish, by making use of the principle of communicating jars, the ‘law of the levelling of price’ of a good in different markets, a law which was later to be called Jevons’s Law.

A few years later, Nicholas Barbon summarized mercantilist thought on the subject of value in the following way. First, the natural value of goods is simply represented by their market price. Second, the forces of supply and demand determine the price. Finally, the use value is the main factor on which the price depends. The conditions of supply play a role only in the sense that, given the demand, the price tends to rise when the supply is insufficient and vice versa.

It is understandable that, in this period, the great trading companies tried to obtain State help to ensure themselves monopoly positions. Competition among merchants reduced their market power or, in other words, their ability to control the conditions of demand (on the purchase markets) or supply (on the sales markets). Less understandable may seem the inclination of the governments to concede such privileges, or even the tendency, especially strong in France under Colbert, to bring the highest possible number of economic activities under the monopolistic control of the State. However, it is important to realize that it was precisely from the beginning of the seventeenth century that the sovereigns of the great nations began to prefer to take advice from merchants rather than from nobles. It was also the century in which the merchants began to present the principles that underpinned their own private economic activity as the principles of ‘public economics’. It was in this way that economic science began.

This is perhaps the right place to say something about the so-called ‘Salamanca school’, a group of theologians and jurists who revived the Thomistic doctrine in economics to the point that Schumpeter was tempted to consider them the true founders of this science. We will recall at least the names of the two who made the most interesting contributions to the theory of value and money: Martin de Alzpilcueta Navarro and Luis de Molina. These scholars cannot be likened to mercantilists, because they expressly condemned many bullionist practices that were common in Spain in the sixteenth century and also because they dealt with economic problems from a moral point of view typical of medieval scholasticism. Nevertheless, compared with the prevailing ideas of the times, their innovative attitude made them appear quite modern.

Research into the subjects of value and money was stimulated by the price revolution triggered in Spain by the influx of gold from America following the discovery of the new continent; and particularly by the problems of ethics and canon law raised by the enormous profits earned by arbitrage operations between gold and money—profits that were made possible by the depreciation of the Spanish Maravedi. Various arguments were put forward in an attempt to bend the Thomistic communis aestimatio doctrine to serve a subjectivist theory of value. The theory that traced the causes of value to cost conditions was rejected and replaced by one that attributed them to utility, while the ‘paradox of value’ was tackled with the idea that utility should be gauged by taking scarcity of the commodity into account. In this perspective, a ‘just price’, is determined by communis aestimatio fori; in other words, by a common assessment of the market, and coincides with pretium currens, the current price. Moreover, it was generally believed that profits and losses deriving from exchanges at market prices were premiums and penalties for the degree of efficiency, a conviction that appeared to anticipate an evolutionist theory of competition. It is worth noticing that this idea was accompanied by disapprobation of monopolistic practices and public policies of price fixing.

On the value of money, Molina anticipated the quantity theory, particularly in his observation that it is the excess supply of goods that lowers their prices, given the quantity of money and the number of merchants (an adumbration of the velocity of circulation), while an excess supply of money raises them. Moreover, Molina did not go along with the prevailing theory on the intrinsic value of money, nor with the opinion that reduces the causes of depreciation to clipping and other illegal practices. Instead, he opted for a theory that attributed greater importance to the exchange value of ingots, where fluctuations were put down to changes in supply and demand.

1.3.