Neoclassical Theory in Austria and Sweden

6.4.1. The Austrian School and subjectivism

Menger left the chair of economics at the University of Vienna in 1903. He was succeeded by von Wieser, ‘the central figure of the Austrian School: central in time, in the ideas he professed, in his intellectual ability’, as Streissler described him (‘Arma virumque cano: Friedrich von Wieser, the Bard as Economist’ (1986), p.

194). His 1914 general treatise, Theorie der gesellschaftlichen Wirtschaft gave width and order to Mengerian thought. For quite some time it was used as the basic textbook of the school. Up to the beginning of the 1920s, however, Btihm-Bawerk was the most prestigious and at the same time the most controversial personality of the Austrian school. In the ten years before the First World War it was Bohm-Bawerk’s seminars, a group which included von Mises and Schumpeter, that was the main centre of theoretical formulation of the Austrian School. It is not by chance that the Marxists of the time considered Bohm-Bawerk as the intellectual enemy to defeat: it was he who represented bourgeois economics.Bohm-Bawerk became famous not only for his theory of interest but also for his frontal attack on the Marxian labour theory of value. In 1896 (volume III of Capital had been published two years before), the Viennese economist published Zum Abschluss des Marxschen Systems, an essay in which he aimed at stigmatizing the ‘great contradiction’ in Marx’s work between price calculation and the labour theory of value. A talented controversialist and at the same time a man with vast practical experience (he was three times Austrian Minister of Finance), he started that tension between Marxist scholars and the neoclassical economists of the Austrian School which was to surface again, in the inter-war period, in the controversy about the possibility of economic calculation in a centrally planned economy (see section 8.5).

Bohm-Bawerk set out to extend the Mengerian theory of subjective value to the theory of capital and interest. After having published the heavy Geschichte und Kritik der Kapitalzinstheorie in 1884, his main work, the Positive Theorie des Kapitales, came out in 1889. These two books make up the two parts of a treatise entitled Kapital und Kapitalzins. The fortunes of the Austrian School at the end of the nineteenth and the beginning of the twentieth centuries were largely due to this book. The work was to receive a mixed reception. On the one hand, the neo-Bohm-Bawerkians of the 1960s and 1970s, led by P. Bernholz and M. Faber, tried to go beyond the limits set by the analysis of their master. On the other, economists like

L. Lachmann, on the basis of a Monger’s opinion (as reported by Schumpeter), judged Bohm-Bawerk’s theory of capital as ‘one of the biggest mistakes ever made’. Bohm-Bawerk himself, however, considered his own theory of capital and interest as a simple extension of Menger’s subjective theory of value.

Bohm-Bawerk’s specific contribution lies in the idea that the fundamental characteristic of every productive activity using capital, intended as a set of reproducible means of production, is that of linking the events in timesequences. From which it ensues that the series of technologically possible changes is characterized not so much by relations of substitutability among inputs, as by relations of complementarity. One of the Austrian school’s distinctive traits was the concept of time as an irreversible succession of moments. Unlike space, the direction of time cannot be changed. It follows that the structure of capital in use at a given moment is the result of past investment decisions and their temporal profiles. This is why the Austrians tend to refer not merely to stock of capital but to its structure by age.

Bohm-Bawerk and all the first-generation Austrian economists, however, missed the point that there is another way in which time enters the production process: the duration of the interval of time in which the ‘machine’ surrenders its services.

In fact, in the Austrian conceptualization, capital is almost always circulating capital. In it there is no place for fixed capital; this explains why their favourite examples are those of production processes such as the maturing of wine or the growing and cutting of trees. According to the celebrated terminology of R. Frisch, the time structure of the productive process studied by Bohm-Bawerk is of the continuous input-point output type. In this kind of processes labour inputs are applied in different moments to obtain a final output after a certain time. We had to wait for J. Hicks’s Capital and Time (1973) for a rigorous formulation of the fixed-capital case, i.e. of the continuous input-continuous output model, where a time sequence of inputs generates a time sequence of outputs.Once Btihm-Bawerk had introduced the time element into the analysis of consumption and production decisions, he argued that it was possible to explain interest in these terms: as production requires time, and as individuals systematically prefer present to future goods, the production processes that use capital must generate a product which allows the payment of interest to those who, in preceding periods, have invested in the indirect productive processes. Unfortunately, the attempt to bend the theory of capital to the needs of demonstrating the positivity of interest was responsible for some serious difficulties which Btjhm-Bawerk never succeeded in overcoming. As von Hayek noted in The Pure Theory of Capital (1941),

The treatment of the theory of capital as an adjunct to the theory of interest has had somewhat unfortunate effects on its developments, [since] the attempts to explain interest, by analogy with wages and rent, as the price of the services of some definitely given ‘factor’ of production has nearly always led to a tendency to regard capital as a homogeneous substance the quantity of which could be regarded as a ‘datum’. (p. 5) This was a notable proposition, which anticipated the essential terms of the great debate on capital theory of the 1960s.

6.4.2. The Austrian School joins the mainstream

The Austrian theoretical approach joined the mainstream of the neoclassical system in the 1920s and 1930s. In order not to break our narration, and even at the cost of being a little repetitive, we will describe in this section how this happened.

At the end of the First World War the third generation of Austrian economists came on to the scene. There were two groups of scholars, one of which gathered around the key figure of Hans Mayer, the other around that of Ludwig von Mises. In addition, we must recall two important figures who, albeit students of the second generation economists, came into a class of their own and did not share the Austrian way of thinking. The first was Karl Menger, son of Carl, who applied mathematics to problems of economic theory, in particular to that of the existence of a general economic equilibrium; we shall return to this in Chapter 8. The second was Joseph Alois Schumpeter, whom we shall deal with at length in Chapter 7.

Mayer, who held the chair that had been Wieser’s until the Second World War, endeavoured to work out the problems that Menger’s theory of imputation had left unsolved, by proposing—albeit with little success—a barely outlined ‘genetic-causal’ method for determining market prices. Of far greater import was the contribution made by von Mises, creator and advocate of the celebrated Privatseminar which met at the Vienna Chamber of Commerce. This seminar had catalysed the attention of a group of promising young economists which included Friedrich von Hayek, Gottfried Haberler, Fritz Machlup, Oskar Morgenstern, Paul Rosenstein-Rodan, as well as philosophers and sociologists of the calibre of Felix Kaufmann, Alfred Schutz, and Erik Voegelin. This group was responsible for the first settlement of the Austrian approach to economic theory and, above all, for the diffusion of this school outside Viennese circles. However, the methodological and theoretical position of its founder, Menger, was not always defended from the attacks of critics with the necessary argumentative force.

An impulse that carried a certain weight in spreading Austrian thought came from Lionel Robbins, founder of the London School of Economics, who came in touch with the Viennese group and subscribed to its ideas. In 1931 Robbins invited von Hayek to teach at the LSE. A sound intellectual association developed, from which Robbins derived great benefit for his celebrated book An Essay on the Nature and Significance of Economic Science, written in 1932, a work that attempted to arrange the schemes of Austrian thought so as to make them compatible with the positions of other neoclassical scholars. One example will suffice for all. The origin of what was to become the ‘official’ definition of economic science—the science ‘that studies human conduct as a relation between ends, classifiable in order of importance, and scarce means applicable to alternative uses’ (p. 15), had already appeared in Menger’s Grundsatze, with however one variation, of no small entity: the word ‘needs’ was substituted with ‘ends’. The Essay did not meet with immediate success, judging by the frontal attack that Souter made on it in a critique published the following year in the Quarterly Journal of Economics. The shameful accusation was that it had broken away from the tradition of Marshallian thought: ‘The Essay is a scanty and worthy account of the main assertions of the Austrian School; it is the creed of Prof. Robbins, as a supporter of that school’ (p. 377).

The theoretical influence of the Austrian school reached its height in the early ‘thirties, although it was to be short-lived. The advent of Nazism and the Anschluss gave rise to an unprecedented diaspora. Von Mises himself emigrated in 1934 to Geneva and then to New York. But there was another, as it were, intrinsic reason. By now, almost all the members of the Privat- seminar were convinced that the basic ideas of their school had already become part of orthodoxy and there was no further need to fight to affirm the Austrian point of view in economic theory.

A statement made by von Mises in 1932 testifies to this conviction. Referring to the division, at that time quite usual, into three schools of thought, the Austrian, the Anglo- American and Lausanne schools, von Mises referred to Morgenstern who held that these groups of economists ‘differ only in their way of expressing the same fundamental idea and appear divided more on account of the terminology they use and the peculiarity of their presentation than over the substance of their teaching’ (Epistemological Problems, p. 214).It was only after the Second World War that the work of von Mises at New York University generated the neo-Austrian school which today is associated with the names of Murray Rothbard, Ludwig Lachmann, Israel Kirzner, Mario Rizzo, Gerald O’Driscoll, and various others. We shall deal with them in Chapter 12.

6.4.3. Wicksell and the origins of the Swedish School

Wicksell in many ways is the Scandinavian Marshall. He was honest in acknowledging the contributions of others, humble in recognizing the limits of his own analysis, intelligent in avoiding illicit generalizations, and had an extraordinary ability to anticipate successive developments. Unlike Marshall, however, Wicksell did not receive great acclaim during his life, not even in his own country. It was only during the 1930s, when, on the initiative of Kahn and Keynes, Geldzins und Gueterpreise (1898) and the two volumes of Vorlesungen uber die Nationaloekonomie (1901 and 1906) were translated

219 into English, that Wicksell’s name, and especially his thought, began to circulate among a wider circle of economists, so much so that in the period between Keynes’s Treatise on Money (1930) and the General Theory (1936) many economists declared themselves to be neo-Wicksellian.

With Ueber Wert, Kapital und Rente (1893), the great Swedish economist produced a notable work of synthesis. Beginning from the theories of value and marginal utility of Jevons and Menger, he tried to blend Bohm-Bawerk’s analysis of capital and interest with the Walrasian general-equilibrium theory. He formulated a model in which the product increases with the timeinterval between the introduction of inputs and the production of output. His explanation of the positivity of the rate of interest, based on the argument of the marginal productivity of waiting, is almost as important as Fisher’s reformulation. He was heavily indebted, intellectually speaking, to Austrian thought and was well aware of this. In 1921 he even wrote: ‘Since Ricardo’s Principles there has been no other book—not even excepting Jevons’ brilliant but somewhat aphoristic and Walras’ unfortunately difficult work—which has had such a great influence on the development of economics as Menger’s Grundsatze’ (quoted by C. G. Uhr, ‘Knut Wicksell: A Centennial Evaluation’, 1951, p. 834).

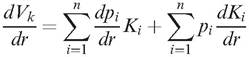

In the first volume of the Lectures, Wicksell completed the reformulation of Bohm-Bawerk’s theory of capital and interest, abandoning the measurement of capital in terms of ‘average period of production’ and substituting a theory in which capital is reduced to the time-structure of the inputs employed at different periods. Then he argued that this structure can undergo variations in at least two dimensions: width and height. Finally, he tried, with partial success, to develop a theory of the ways in which the timestructure of the production process changes with variations in wage-level and rate of interest. As Wicksell himself recognized with reference to the process of ageing wine, only for very special technologies is the value of the capital stock Vk = ∑-- 1 PrK (where Ki represents the quantity of the ith capital good and pi its price) an appropriate measure of the aggregate capital stock intended as a factor of production. That is so because Vk is a function of the rate of interest, r. The Wicksell effect is precisely the change in the value of the capital stock which occurs with variations in r, i.e. dVkldr. The expression ‘Wicksell effect’ was introduced by Uhr in 1951, but its importance was not appreciated until the contributions of Joan Robinson and Piero Sraffa. There is a price Wicksell effect—which is the revaluation of capital goods due to variations in prices—and a real Wicksell effect—which is the sum of the changes, expressed in value, in the physical quantities of the diverse capital goods. Their sum is:

Basically, when r varies, both the prices and the physical quantities change. Now, if there were only one good (n = 1), the price Wicksell effect could be ignored by posing p = 1, while the real effect would always be negative. To this one could give the usual interpretation that the capital intensity of techniques increases with a decrease in the rate of interest. But when there are diverse capital goods (n > 1), both Wicksell effects can be positive or negative, and so can their sum. And no common sense interpretation can be given to this case. In particular one could no longer maintain that the capitallabour ratio rises when the interest rate decreases and then that the latter is determined by the productivity and scarcity of capital.

Shortly before his death, Wicksell tried to introduce fixed capital in the Austrian model—an objective that he would have been able to achieve if, rather than introducing linear depreciation, he had used the formula of exponential depreciation; but he did not have time.

Wicksell’s contribution to the marginalist theory of distribution is of great importance. We have already mentioned this in the sections dedicated to Wicksteed and Clark. In his formulation Wicksell used a simple generalequilibrium model with only one good, Q, produced by means of labour, L, and homogeneous capital, K. What was later to become famous as the Cobb-Douglas production function, Q = LaK1 ~ a, was already present in the writings of the young Wicksell. Special attention should be paid to Wicksell’s approach to the problem of the exhaustion of the product. Barone, in ‘Studi sulla distribuzione’ (1896), had already realized that, in order to obtain the exhaustion of the product, it is sufficient for firms to activate production up to the attainment of minimum average costs. In such cases there is no need to assume first-degree homogeneity of the production function. Wicksell integrated this argument with the explicit recognition of the fact that the existence of such a minimum is the necessary condition for the existence of a long-run competitive equilibrium. In fact, only at the point of long-run minimum cost is it possible to have zero profits. Unlike Barone and Walras, who considered this solution as an alternative to that of Wicksteed, Wicksell realized that it was a generalization, since the minimum of the long-run average-cost curve is characterized by ‘locally’ constant returns of scale. This means that competitive equilibrium implies that, at least locally, Wicksteed’s technical conditions apply.

Wicksell’s solution was based on the theory of the entrepreneur, according to which the entrepreneur contributes to the production process by means of the services of his own factors. In equilibrium these services have the same remuneration, whether they are employed by the entrepreneur in his own firm or passed on to other firms. The labour employed to organize and co-ordinate the firm will be remunerated in the same way exactly as the labour of the same quality employed in other activities and in any other firm. In fact, if the entrepreneur received a higher remuneration, everybody would wish to employ their own labour in organizational tasks and nobody would wish to be a subordinate. Obviously, in order for zero profit to be reached in this way, the number of those who possess entrepreneurial skills must be high. Even if he did not say so himself, it is plausible to think that Wicksell had in mind a stationary-state equilibrium in which the entrepreneur has no real decision-making role, and in which the organizational work is reduced to mere supervision.

Geldzins und Gtiterpreise and the second volume of the Lectures include Wicksell’s most important work on monetary theory. He was one of the first to use the aggregate supply-and-demand approach to explain variations in the value of money. In most versions of the quantity theory of money the price level varies in proportion to the variations in the quantity of money; but in these versions there is no relationship between the variations in the quantity of money, including bank credit, and the entrepreneurs’ production decisions. Wicksell brought out this relationship and advanced the hypothesis that, in the absence of exogenous disturbances (those over which the central bank has no control, such as variations in the production of gold or the necessity to finance huge government deficits), the fluctuations in price level would be caused by a persistent gap between the bank (or market) rate of interest and the real (or ‘natural’) rate—the latter being defined as the expected rate of returns on newly produced capital goods. Wicksell came to the conclusion that, contrary to the implication of the simple quantity theory, it is the quantity of money that adjusts to the price-level movements. In his analysis, monetary equilibrium requires the satisfaction of the three following conditions:

(1) equality between the natural and the bank rate of interest; or rather, since the natural rate is not an observable variable, the prevalence of a market interest rate capable of guaranteeing;

(2) equality between the supply of savings and the demand for investment loans and ‘real’ cash balances;

(3) price stability.

We will consider the mechanism that ensures equality between the two rates of interest in section 7.1.3. Here we would like to point out that banks would be able to make a decisive contribution to the re-establishment and the maintenance of equilibrium by increasing the rate of interest in periods of inflation and decreasing it in periods of deflation.

The study of these three conditions of monetary equilibrium was to receive a great deal of attention in the late 1920s and throughout the 1930s, especially by Lindahl, Myrdal, and Ohlin. The work of these scholars together with that of some of their younger colleagues such as Lundberg and Svennilson, contributed to extending Wicksell’s economic theory and to forming the Swedish (or Stockholm) School, which we will treat in more detail in Chapter 7.

Here it is important to emphasize a central characteristic of Wicksell’s analysis: that for which the gap between the two rates of interest produces effects that will only be felt on the price level. This gap will not modify relative prices (because all prices and incomes will increase to the same degree), nor will it have any relevant effects on the accumulation of capital. Wicksell did not exclude the possibility that changes in the monetary rate of interest would induce the adoption of more or less capital-intensive techniques, but he maintained that these effects would be of secondary importance. In any case, the natural rate of interest could be considered constant during the cumulation process.

Another important aspect of Wicksell’s thought concerns the theory of public finance and optimal taxation. In Finanzteoretische Untersuchungen (1896), Wicksell applied marginal-utility theory to the public sector of the economy, reaching, on the one hand, the formulation of the well-known principle of benefit and contributive ability as the fundamental criterion of taxation, and, on the other, the proposal to set the prices of the services of public firms according to the criterion of marginal cost. In fact, it was his 1896 work that initiated the Wicksell-Lindahl-Musgrave-Samuelson line of thought on the theory of public goods. According to this line of thought, the production of public goods should be pushed forward, to the point at which the marginal cost equals the sum of the marginal rates of substitution between public goods and private goods of all individuals interested in the public goods. With a little too much faith in honesty and in the principle of consensus, typical of the Scandinavian culture, Wicksell did not seem to realize what was later to become the problem of free-riders: each individual in a Lindahl-type market is motivated to declare that he does not draw any utility from the public good, with the aim of avoiding contributions to financing it.

Wicksell was decidedly reformist. He fought for programmes of redistribution of wealth from the rich to the poor, and this brought him quite a few problems in his academic career. No writer in the Edwardian period was nearer to the New Deal ideology than Wicksell. He rejected Marxism both as an instrument to understand the laws of movement of capitalism and as a guide to the action aimed at improving the conditions of the working class. In a rather more sophisticated manner than Marshall, Wicksell realized that a competitive equilibrium does not necessarily lead to a state of maximum social welfare, nor to a fair state. However, he anticipated the neoclassical argument that makes perfect competition a condition for Pareto optimality; and he understood that, by operating on the initial endowments of individuals, it is possible to lead the system towards a state which, besides being efficient, is also ethically acceptable. In any case, Wicksell forcefully emphasized the argument that the attainment of efficiency in no way constitutes a morally incontrovertible objective, so that there is no space in economic theory for a defence of the capitalist system.

Wicksell’s anti-conformism helps us understand his fierce rivalry with Gustav Cassel, the King’s tutor and a leading light in the Swedish intelligentsia. Before the 1930s, Cassel, the real pillar of Swedish conservative economics, was the economist most often quoted in the international press. In 1918 he published Theoretische Sozialoekonomie, a work that developed an interesting general-equilibrium model without making any reference to Walras. It also contained an important novelty: it did not use any utility functions. Cassel was a tenacious critic of the concept of marginal utility. By using the demand function as a primary concept and thus breaking the link between the utility functions and the demand functions, Cassel placed prices at the centre of his theory of resource allocation. This is perhaps why his work had such an enormous influence on economics literature up to the 1930s. Schumpeter, however, perhaps a little naughtily, was to define Cassel as ‘90 per cent Walras and 10 per cent water’.

6.5.