Evidence on finance and growth

A substantial body of empirical work on finance and growth assesses the impact of the operation of the financial system on economic growth, whether the impact is economically large, and whether certain components of the financial system, e.g., banks and stock markets, play a particularly important role in fostering growth at certain stages of economic development.

This section is organized around econometric approaches to examining the relationship between finance and growth. Thus, the first subsection discusses cross-country studies of growth and finance. The second subsection presents evidence from panel studies, pure time-series investigations, and country case-studies. The third subsection examines industry and firm level analyses that provide direct empirical evidence on the mechanisms linking finance and growth. Then, I summarize existing work on the relationship between financial structure - the degree to which an economy is bank-based or market-based - and economic growth. Finally, I mention recent research on whether financial development influences income distribution and poverty.

The organization of the empirical evidence advertises an important weakness in the finance and growth literature: there is frequently an insufficiently precise link between theory and measurement. Theory focuses on particular functions provided by the financial sector - producing information, exerting corporate governance, facilitating risk management, pooling savings, and easing exchange - and how these influence resource allocation decisions and economic growth. Thus, I would prefer to organize the empirical section around studies that precisely measure each of the functions stressed by theory. Similarly, while empirical studies focus on measures of the size of banks or stock markets, Petersen and Rajan (1997), DemirguQ-Kunt and Maksimovic (2001), and Fis- man and (2003a, 2003b) show that firms frequently act as financial intermediaries in providing trade credit to related firms.

This source of financial intermediation may be very important, especially in countries with regulatory restrictions on financial intermediaries and in countries with undeveloped legal systems that do not effectively support formal financial development. This further advertises the sub-optimal connection between theory and measurement in the finance and growth literature.While fully recognizing this problem, many of the biggest advances in empirical studies of finance and growth have been methodological. Thus, I organize the discussion around econometric approaches. While serious improvements have been made in measuring financial development, which I discuss below, future research that more concretely links the concepts from theory with the data will substantively improve our understanding of the finance and growth link.

3.1. Cross-country studies of finance and growth

3.1.1. Goldsmith, the question, and the problems

Goldsmith (1969) motivated his path breaking study of finance and growth as follows.

One of the most important problems in the field of finance, if not the single most important one,... is the effect that financial structure and development have on economic growth. (p. 390)

Thus, he sought to assess whether finance exerts a causal influence on growth and whether the mixture of markets and intermediaries operating in an economy influences economic growth. Toward this end, Goldsmith (1969) carefully compiled data on 35 countries over the period 1860 to 1963 on the value of financial intermediary assets as a share of economic output. He assumed, albeit with ample qualifications, that the size of the financial intermediary sector is positively correlated with the quality of financial functions provided by the financial sector.

Goldsmith (1969) met with varying degrees of success in providing confident answers to these questions. After showing that financial intermediary size relative to the size of the economy rises as countries develop, Goldsmith graphically documented a positive correlation between financial development and the level of economic activity.

Goldsmith just as clearly asserted his unwillingness to draw causal interpretations from his graphical presentations. Thus, Goldsmith ultimately did not take a stand on whether financial development causes growth. In terms of the relationship between economic growth and the structure of the financial system, Goldsmith was unable to provide much cross-country evidence because of the absence of data on securities market development for a broad range of countries.Goldsmith’s (1969) work raises several problems, all of which Goldsmithpresciently stresses, that subsequent work has tried to resolve.

(1) The investigation involves only 35 countries.

(2) It does not systematically control for other factors influencing economic growth.

(3) It does not examine whether financial development is associated with productivity growth and capital accumulation, which theory stresses.

(4) The indicator of financial development, which measures the size of the financial intermediary sector, may not accurately gauge the functioning of the financial system.

(5) The close association between financial system size and growth does not identify the direction of causality.

(6) The study did not shed light on whether financial markets, non-bank financial intermediaries, or the mixture of markets and intermediaries matter for economic growth.

3.1.2. More countries, more controls, and predictability

In the early 1990s, King and Levine (1993a, henceforth KL) built on Goldsmith’s work. They study 77 countries over the period 1960-1989, systematically control for other factors affecting long-run growth, examine the capital accumulation and productivity growth channels, construct additional measures of the level of financial development, and analyze whether the level of financial development predicts long-run economic growth, capital accumulation, and productivity growth.

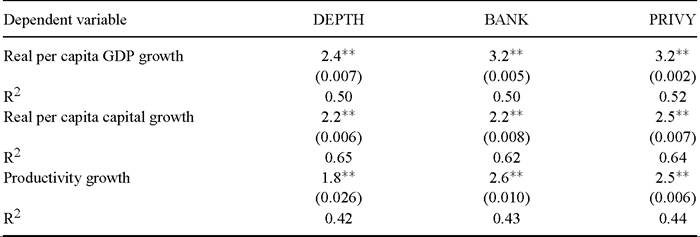

In terms of measures of financial development, KL first examine DEPTH, which is simply a measure of the size of financial intermediaries.

It equals liquid liabilities of the financial system (currency plus demand and interest-bearing liabilities of banks and nonbank financial intermediaries) divided by GDP. They also construct the variable BANK that measures the relative degree to which the central bank and commercial banks allocate credit. BANK equals the ratio of bank credit divided by bank credit plus central bank domestic assets. The intuition underlying this measure is that banks are more likely to provide the five financial functions than central banks. There are two notable weaknesses with this measure, however. Banks are not the only financial intermediaries providing valuable financial functions and banks may simply lend to the government or public enterprises. KL also examine PRIVY, which equals credit to private enterprises divided by GDP. The assumption underlying this measure is that financial systems that allocate more credit to private firms are more engaged in researching firms, exerting corporate control, providing risk management services, mobilizing savings, and facilitating transactions than financial systems that simply funnel credit to the government or state owned enterprises. While BANK and PRIVY seek to improve upon DEPTH by capturing who is doing the allocating and to whom society’s savings are flowing, these measures still do not directly proxy for the five financial functions stressed in theoretical models of finance and growth. KL find very consistent results across the different financial development indicators.KL then assess the strength of the empirical relationship between each of these indicators of the level of financial development averaged over the 1960-1989 period and three growth indicators also averaged over the 1960-1989 period. The three growth indicators are as follows: (1) the average rate of real per capita GDP growth, (2) the average rate of growth in the capital stock per person, and (3) total productivity growth, which is a “Solow residual” defined as real per capita GDP growth minus (0.3) times the growth rate of the capital stock per person.

In other words, if F(i) represents the value of the i th indicator of financial development averaged over the period 1960-1989, G(j) represents the value of the j th growth indicator (per capita GDP growth, per capita capital stock growth, or productivity growth) averaged over the period 1960-1989, and X represents a matrix of conditioning information to control for other factors associated with economic growth (e.g., income per capita, education, political stability, indicators of exchange rate, trade, fiscal, and monetary policy), then they estimated the following regressions on a cross-section of 77 countries:G(j) = α + βF(i) + γX + ε.

Table 1 is adapted from KL and indicates that there is a strong positive relationship between each of the financial development indicators, F(i), and the three growth indicators G(i), long-run real per capita growth rates, capital accumulation and productivity growth. The sizes of the coefficients are economically large. Ignoring causality, the coefficient on DEPTH implies that a country that increased DEPTH from the mean of the slowest growing quartile of countries (0.2) to the mean of the fastest growing quartile of countries (0.6) would have increased its per capita growth rate by almost 1 percent per year. This is large. The difference between the slowest growing 25 percent of countries and the fastest growing quartile of countries is about five percent per annum over this 30-year period. Thus, the rise in DEPTH alone eliminates 20 percent of this growth difference. King and Levine (1993b, 1993c) confirm these findings using alternative econometric methods and robustness checks.

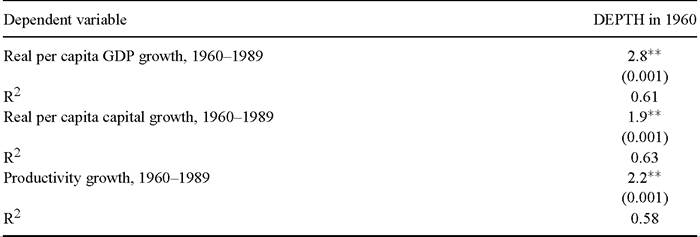

To examine whether finance simply follows growth, KL study whether the value of financial depth in 1960 predicts the rate of economic growth, capital accumulation, and productivity growth over the next 30 years. Table 2 summarizes these results. The dependent variable is, respectively, real per capital GDP growth, real per capita capital stock growth, and productivity growth averaged over the period 1960-1989.

The financial indicator in each of these regressions is the value of DEPTH in 1960. The regressions indicate that financial depth in 1960 is a good predictor of subsequent rates of economic growth, physical capital accumulation, and economic efficiency improvements over the next 30 years even after controlling for income, education, and measures of monetary, trade, and fiscal policy. The relationship between the initial level of financial development and growth is economically large. For example, the estimated coefficients suggest that if in 1960 Bolivia had increased its financial depth from 10 percent of GDP to the mean value for developing countries in 1960 (23 percent), then Bolivia would have grown about 0.4 percent faster per annum, so that by 1990 real per capita GDP would have been about 13 percent larger than it was. These examplesTable 1

Growth and financial intermediary development, 1960-1989

Source: King and Levine (1993b, Table VII).

* Significant atthe 0.10 level.

**Significant atthe 0.05 level.

(p-values in parentheses.)

Observations: 77.

Variable definitions: DEPTH = Liquid liabilities ∕GDP, BANK = Deposit bank domestic credit/[Deposit bank domestic credit + Central bank domestic credit], PRIVY = Gross claims on the private sector/GDP, Productivity growth = Real per capita GDP growth — 0.3 ∙ Real per capita capital growth.

Other explanatory variables included in each of the nine regression results reported above: logarithm of initial income, logarithm of initial secondary school enrollment, ratio of government consumption expenditures to GDP, inflation rate, and ratio of exports plus imports to GDP.

Notes: King and Levine (1993b) define 2 percent growth as 0.02. For comparability with subsequent tables, we have redefined 2 percent growth as 2.00 and adjusted the coefficients by a factor of 100.

do not consider what actually causes the change in financial development. They simply illustrate the potentially large long-term growth effects from changes in financial development.

La Porta, Lopez-de-Silanes and Shleifer (2002) use an alternative indicator of financial development. They examine the degree of public ownership of banks around the world. To the extent that publicly-owned banks are less effective at acquiring information about firms, exerting corporate governance, mobilizing savings, managing risk, and facilitating transactions, then this measure provides direct evidence on connection between economic growth and the services provided by financial intermediaries. The authors show that (1) higher degrees of public ownership are associated with lower levels of bank development and (2) high levels of public ownership of banks are associated with slower economic growth.

While addressing many of the weaknesses in earlier work, cross-country growth regressions do not eliminate them. Thus, while KL show that finance predicts growth, they do not deal formally with the issue of causality [Shan, Morris and Sun (2001)]. While researchers improve upon past measures of financial development, they only focus on

Table 2

Growth and initial financial depth, 1960-1989

Sources: King and Levine (1993b, Table VIII) and Levine (1997, Table 3).

* Significant atthe 0.10 level. **Significant at the 0.05 level. (p-values in parentheses.) Observations: 57.

Variable definitions: DEPTH = Liquid liabilities/GDP, Productivity growth = Real per capita GDP growth— 0.3 ∙ Real per capita capital growth.

Other explanatory variables included in each of the regression results reported above: logarithm of initial income, logarithm of initial secondary school enrollment, ratio of government consumption expenditures to GDP, inflation rate, and ratio of exports plus imports to GDP.

Notes: King and Levine (1993b) and Levine (1997) define 2 percent growth as 0.02. For comparability with subsequent tables, we have redefined 2 percent growth as 2.00 and adjusted the coefficients by a factor of 100.

one segment of the financial system, banks, and their indicators do not directly measure the degree to which financial systems ameliorate information and transaction costs.

3.1.3. Adding stock markets to cross-country studies of growth

There are good reasons to study the relationship between long-run economic growth and the operation of equity markets. First, as stressed above, theoretical debate exits on whether larger, more liquid equity markets exert a positive or negative influence on economic growth, capital accumulation, and productivity growth. Second, as stressed above, some theories focus on the competing roles of banks and markets in funding corporate expansion, while others stress that banks and markets may arise, coexist, and prosper by providing different financial functions to the economy, and still other theories stress complementarities between banks and markets. Thus, simultaneously considering the potential roles of banks and markets permits one to distinguish among competing theories and provide evidence to policy makers on the independent roles of markets and banks in the process of economic growth.

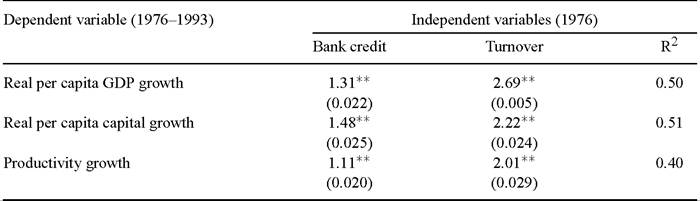

Levine and Zervos (1998a, henceforth LZ) construct numerous measures of stock market development to assess the relationship between stock market development and

Table 3

Stock market and bank development predict growth, 1976-1993

Source: Levine and Zervos (1998a, 1998b, Table 3).

* Significant atthe 0.10 level. **Significant atthe 0.05 level. (p-values in parentheses.) Observations: 42 for the real per capita GDP growth regression and 41 for the others. Variable definitions: Bank credit = Bank creditto the private sector/GDP in 1976 orthe closest date with data, Turnover = Value of the trades of domestic shares on domestic exchanges as a share of market capitalization of domestic shares in 1976 orthe closest date with data, Productivity growth = Real per capita GDP growth — 0.3 ∙ Real per capita capital growth.

Other explanatory variables included in each of regression results reported above: logarithm ofinitial income, logarithm of initial secondary school enrollment, ratio of government consumption expenditures to GDP, inflation rate, black market exchange rate premium, and frequency of revolutions and coups.

Notes: Levine and Zervos define 2 percent growth as 0.02. For comparability with subsequent tables, we have redefined 2 percent growth as 2.00 and adjusted the coefficients by a factor of 100.

economic growth, capital accumulation, and productivity growth in a sample of 42 countries over the period 1976-93.[530] They control for many other potential growth determinants, including banking sector development. Their study builds on pioneering workby Atje and Jovanovic (1993).

For brevity, I focus on only one of LZ’s liquidity indicators, the turnover ratio. This equals the total value of shares traded on a country’s stock exchanges divided by stock market capitalization (the value of listed shares on the country’s exchanges). The turnover ratio is not a direct measure of trading costs or of the ability to sell securities at posted prices. Rather, the turnover ratio measures trading relative to the size of the market. It therefore reflects trading frictions and information that induces transactions. This ratio exhibits substantial cross-country variability. Very active markets such as Japan and the United States had turnover ratios of almost 0.5 during the 1976-93 period, while less liquid markets, such as Bangladesh, Chile, and Egypt have turnover ratios of 0.06 or less.

As summarized in Table 3, LZ find that the initial level of stock market liquidity and the initial level of banking development (Bank Credit) are positively and significantly correlated with future rates of economic growth, capital accumulation, and productivity growth over the next 18 years even after controlling for initial income, schooling, inflation, government spending, the black market exchange rate premium, and political stability. Bank credit equals bank credit to the private sector as a share of GDP.[531]

These results are consistent with the view that stock market liquidity facilitates long- run growth [Levine (1991), Holmstrom and Tirole (1993), Bencivenga, Smith and Starr (1995)], but inconsistent with models that emphasize the negative aspects of stock markets liquidity [Bhide (1993)]. Furthermore, the results do not lend much support to models that emphasize the tensions between bank-based and market-based systems. Rather, the results suggest that stock markets provide different financial functions from those provided by banks, or else they would not both enter the growth regression significantly.

The sizes of the coefficients also suggest an economically meaningful relationship. For example, the estimated coefficient implies that a one-standard-deviation increase in initial stock market liquidity (0.30) would increase per capita GDP growth by 0.80 percentage points per year (2.7 ∙ 0.3). Accumulating over 18 years, this implies real GDP per capita would have been over 15 percentage points higher by the end of the sample. Similarly, the estimated coefficient on Bank Credit implies a correspondingly large growth effect. That is, a one-standard deviation increase in Bank Credit (0.5) would increase growth by 0.7 percentage point per year (1.3 ∙ 0.5). Takentogether, the results imply that if a country had increased both stock market liquidity and bank development by one-standard deviation, then by the end of the 18-year sample period, real per capita GDP would have been almost 30 percent higher and productivity would have been almost 25 percent higher. As emphasized throughout, these conceptual experiments do not consider the underlying causes of the change in the operation of the financial sector. The examples simply illustrate the potential growth effects of financial development. LZ go onto argue that the link between stock markets, banks, and growth runs most robustly through productivity growth, rather than physical capital accumulation, which is consistent with some theoretical models [Levine (1991), Bencivenga, Smith and Starr (1995)].

LZ also find that stock market size, as measured by market capitalization divided by GDP, is not robustly correlated with growth, capital accumulation, and productivity improvements. This is consistent with theory. Simply listing on the national stock exchange does not necessarily foster resource allocation. Rather, it is the ability to trade the economy’s productive technologies easily that influences resource allocation and growth.

There are a number of weaknesses, however, associated with the LZ approach.

First, while they show that stock market liquidity and bank development predict economic growth, they do not deal formally with the issue of causality.

Second, there are difficulties in measuring liquidity as discussed by Grossman and Miller (1988). LZ do not measure the direct costs of conducting equity transactions. Furthermore, they do not control for the possibility that the arrival of information and the processing of that information may differ across countries and thereby induce crosscountry differences in trading that does not reflect liquidity as defined by theory. While LZ confirm their results using three additional measures of liquidity, measurement issues remain.[532]

Third, more broadly, the liquidity indicators measure domestic stock transactions on a country’s national stock exchanges. The physical location of the stock market, however, may not necessarily matter for the provision of liquidity unless there are impediments to cross-location transactions. Physical location will matter less - and this measurement problem will matter more - if economies become more financially integrated. Guiso, Sapienza and Zingales (2002), however, find that local financial conditions matter even in a single country - Italy. They show that local financial conditions influence economic performance across the different regions of Italy. That is, local financial development is an important determinant of the economic success of an area even within a single country. Their results suggest that international financial integration is unlikely to eliminate the importance of national financial systems in the near future.[533]

Fourth, even more generally, the link between trading and future economic growth may not represent a link between liquidity and growth as suggested by some theories [Levine (1991), Bencivenga, Smith and Starr (1995)]. The liquidity-stock market link may be generated by a third factor that produces both a surge in trading and a subsequent acceleration in economic growth, but where trading does not induce the growth acceleration. For instance, positive news about a technology shock may elicit different opinions about which sectors and firms will benefit most from the innovation. This would produce lots of trading today because of these differences of opinion. The subsequently surge in economic growth is due to the positive technology shock, not the increase in stock transactions. In this “model”, trading does not necessarily facilitate the ability of the economy to exploit the growth benefits of the technology shock. From this perspective, it is difficult to interpret the LZ results as implying that liquidity fosters economic growth.

Fifth, while LZ include measures of the functioning of stock markets and banks, they exclude other components of the financial sector, e.g., bond markets and the financial services provided by nonfinancial firms. Beck, DemirguQ-Kunt and Levine (2001) show that in many countries private bond market capitalization is more than half the capitalization of national equity markets and public bond markets are frequently larger than stock markets. Furthermore, over the period 1980-1995, new issuances of private bonds were greater than public offerings of stock in many countries. Fink, Haiss and Hristo- forova (2003) examine the impact of bond market development on real output in 13 highly developed economies over the period 1950-2000. Using Grangercausality tests and co-integration methods, the bulk of their evidence indicates that bond market development influences real economic activity. Furthermore, Beck, DemirguQ-Kunt and Levine (2001) show that life insurance and private pension fund assets rival banks in some countries, while Berger, Hasan and Klapper (2005) indicate that small, community banks boost growth in many developing countries. Thus, more work remains on incorporating bond markets and nonbank institutions into finance-growth literature.

Sixth, stock markets may do more than provide liquidity. Stock markets may provide mechanisms for hedging and trading the idiosyncratic risk associated with individual projects, firms, industries, sectors, and countries. While a vast literature examines the pricing of risk, there exists very little empirical evidence that directly links risk diversification services with long-run economic growth. While LZ do not find a strong link between economic growth and the ability of investors to diversify risk internationally, they have extremely limited data on international integration. Future work needs to more fully assess the links between stock markets, banks, and economic growth.

3.1.3. Using instrumental variables in cross-country studies of growth

While KL and LZ show that financial development predicts economic growth, these results do not settle the issue of causality. It may simply be the case that financial markets develop in anticipation of future economic activity. Thus, finance may be a leading indicator rather than a fundamental cause.

To assess whether the finance-growth relationship is driven by simultaneity bias, one needs instrumental variables that explain cross-country differences in financial development but are uncorrelated with economic growth beyond their link with financial development and other growth determinants. Levine (1998, 1999) and Levine, Loayza and Beck (2000) use the La Porta et al. (1998, henceforth LLSV) measures of legal origin as instrumental variables. In particular, LLSV (1998) show that legal origin - whether a country’s Commercial/Company law derives from British, French, German, or Scandinavian law - importantly shapes national approaches to laws concerning creditors and the efficiency with which those laws are enforced. Since finance is based on contracts, legal origins that produce laws that protect the rights of external investors and enforce those rights effectively will do a correspondingly better job at promoting financial development.[534] Indeed, LLSV (1998), Levine (1998, 1999, 2003), and Levine, Loayza and Beck (2000) trace the effect of legal origin to laws and enforcement and then to financial development. Since most countries obtained their legal systems through occupation and colonization, the legal origin variables may be plausibly treated as exogenous.

FollowingLevine, LoayzaandBeck (2000, henceforth LLB) analysis of 71 countries, consider the generalized method of moments (GMM) regression:

G(j) = α + βF(i) + γX + ε.

G(j) is real per capita GDP growth over the 1960-95 period. The legal origin indicators, Z, are used as instrumental variables for the measures of financial development, F(i). X is treated as an included exogenous variable. LLB use linear moment conditions, which amounts to the requirement that the instrumental variables (Z) be uncorrelated with the error term (ε). The economic meaning of these conditions is that legal origin may affect per capita GDP growth only through the financial development indicators and the variables in the conditioning information set, X.

LLB extend the King and Levine (1993a, 1993b) measures of financial intermediary development through to 1995, improve the deflating of the financial development indicators, and add a new measure of overall financial development.[535] The new measure of financial development, Private Credit, equals the value of credits by financial intermediaries to the private sector divided by GDP. The measure isolates credit issued to the private sector and therefore excludes credit issued to governments, government agencies, and public enterprises. Also, it excludes credits issued by central banks. Unlike the LZ Bank Credit measures, Private Credit included credits issued by non-deposit money bank. Not surprisingly, there is enormous cross-country variation in Private Credit. Private Credit is less than 10 percent of GDP in Zaire, Sierra Leone, Ghana, Haiti, and Syria, while it is greater than 85 percent of GDP in Switzerland, Japan, the United States, Sweden, and the Netherlands.

The LLB results indicate a very strong connection between the exogenous component of financial intermediary development and long-run economic growth. They use various measures of financial intermediary development and different conditioning information sets, i.e., different X’s. They find that the exogenous component of financial development is closely tied to long-run rates of per capita GDP growth. Furthermore, the data do not reject the test of the over-identifying restrictions. The inability to reject the orthogonality conditions plus the finding that the legal origin instruments (Z) are highly correlated with financial intermediary development indicators (i.e., the null hypothesis that the legal origin variables does not explain the financial intermediary indicators is rejected at the 0.01 significance level), suggest that the instruments are appropriate. These results indicate that the strong link between financial development and growth is not due to simultaneity bias. The estimated coefficient can be interpreted as the effect of the exogenous component of financial intermediary development on growth.

LLB’s (2000) instrumental variable results also indicate an economically large impact of financial development on growth. For example, India’s value of Private Credit over the period 1960-95 was 19.5 percent of GDP, while the mean value for developing countries was 25 percent of GDP. The estimated coefficients in LLB suggest that an exogenous improvement in Private Credit in India that had pushed it to the sample mean for developing countries would have accelerated real per capita GDP growth by an additional 0.6 of a percentage point peryear.[536] Similarly, if Argentina had moved from its value of Private Credit (16) to the developing country sample mean, it would have grown more than one percentage point faster per year. This is large considering that growth only averaged about 1.8 percent per year over this period. As emphasized throughout, however, these types of conceptual experiments must be treated as illustrative because they do not account for how to increase financial intermediary development.

While LLB interpret their results as implying that financial development boosts steady-state growth, Aghion, Howitt and Mayer-Foulkes (2005) challenge that conclusion. They first develop a model of technological change that predicts that countries with levels of financial development above a critical, threshold level will converge in growth rates. Among these countries, financial development positively influences the rate of convergence, so the financial development exerts positive but diminishing influence on steady-state levels of real per capita output. They find empirical support for the model’s predictions. Financial development explains (i) whether there is convergence or not, and (ii) the rate of convergence (when there is convergence), but Aghion, Howitt and Mayer-Foulkes (2005) find that financial development does not exert a direct effect on steady-state growth.

3.2. Panel, time-series, and case-studies of finance and growth

Studies of finance and growth have also employed panel data techniques, pure timeseries methodologies, and case-studies to ameliorate a number of statistical problems with pure cross-country investigations. This section discusses the panel approach in some depth and finishes with shorter discussions of pure time-series and case-study approaches.

[1] The within-country standard deviation is calculated using the deviations from country averages, whereas the between-country standard deviation is calculated from the country averages.

exogenous, the following moment conditions hold.

This difference estimator consists of the regression in differences plus Equation (3).

The third benefit from moving to a panel is that it permits the use of instrumental variables for all regressors and thereby provides more precise estimates of the financegrowth relationship. As discussed, researchers use legal origin instruments to extract the exogenous component of financial development. These pure cross-sectional estimators, however, do not control for the endogeneity of all the other explanatory variables. This can lead to inappropriate inferences on the coefficient on financial development.

Building on this difference panel estimator, Arellano and Bover (1995) propose a system estimator that jointly estimates the regression in levels (Equation (1)) and the equation in differences (Equation (2)) in order to (i) re-incorporate the cross-country variation from the levels regression and (ii) reduce the likelihood that weak instruments bias the estimated coefficients and standard errors.

3.2.2. Dynamic panel results on financial intermediation and growth

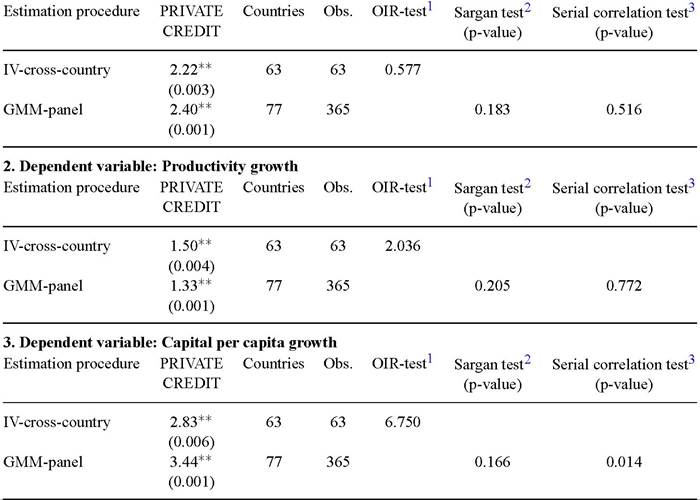

LLB use the system estimator to examine the relationship between financial intermediary development and growth, while BLL examine the relationship between financial development and the sources of growth, i.e., productivity growth, physical capital accumulation, and savings. They examine an assortment of indicators of financial intermediary development and also use a variety of conditioning information sets to assess the robustness of the results [Levine and Renelt (1992)]. Here, we summarize the results in Table 4 using the Private Credit measure of financial development described above and a simple set of control variables.

The results indicate a positive relationship between the exogenous component of financial development and economic growth, productivity growth, and capital accumulation. The regressions pass the standard specification tests. Table 4 presents both (1) instrumental variable results using a pure a cross-sectional analysis where the legal origin variables are the instruments and (2) the dynamic panel results just described. Remarkably the coefficient estimates are very similar using the two procedures and economically significant. Thus, the large, positive relationship between economic growth and Private Credit does not appear to be driven by simultaneity bias, omitted countryspecific effects, or the routine use of lagged dependent variables in cross-country growth regressions. While BLL go on to argue that the finance-capital accumulation link is not robust to alternative specifications, they demonstrate a robust link between financial development indicators and both economic growth and productivity growth.

The regression coefficients suggest an economically large impact of financial development on economic growth. For example, Mexico’s value for Private Credit over the period 1960-95 was 22.9% of GDP. An exogenous increase in Private Credit that had

Table 4

Growth, Productivity growth, and Capital accumulation, panel GMM and OLS, 1960-1995

1. Dependent variable: Real per capita GDP growth

Source: Beck, Levine and Loayza (2000).

* Significant atthe 0.10 level.

**Significant atthe 0.05 level.

(p-values in parentheses.)

IV-cross-country: Cross-country instrumental variables with legal origin as instruments, estimated using GMM.

GMM-panel: Dynamic panel (5-year averages) generalized method of moments using system estimator. Other explanatory variables: logarithm of initial income per capita, average years of schooling.

PRIVATE CREDIT: Logarithm(credit by deposit money banks and other financial institutions to the private sector divided by GDP).

1 The null hypothesis is that the instruments used are not correlated with the residuals from the respective regression. Critical values for OIR-Test (2 d.f.): 10% = 4.61; 5% = 5.99.

2 The null hypothesis is that the instruments used are not correlated with the residuals from the respective regression.

3The null hypothesis is that the errors in the first-difference regression exhibit no second-order serial correlation. brought it up to the sample median of 27.5% would have resulted in a 0.4 percentage point higher real per capita GDP growth per year.[537]

While BLL and LLB examine linear models, recent research suggests that the impact of financial development on capital accumulation, productivity growth, and overall real per capita GDP growth may depend importantly on other factors. Using the same econometric methods and data, Rioja and Valev (2004a) find that finance boosts growth in rich countries primarily by speeding-up productivity growth, while finance encourages growth in poorer countries primarily by accelerating capital accumulation. Furthermore, Rioja and Valev (2004b) find that the impact may be nonlinear. They find that countries with very low levels of financial development experience very little growth acceleration from a marginal increase in financial development, while the affect is larger for rich countries and particular large for middle-income countries. It would be nice to know, however, what produces these nonlinearities. Finally, Rousseau and Wachtel (2002) show that the positive impact of financial development on growth diminishes with higher rates of inflation.

Emphasizing that not all indicators of financial development measure the same forces, Benhabib and Spiegel (2000) examine the relationship between an assortment of financial intermediary development indicators and economic growth, investment, and total factor productivity growth. While they use a panel estimator, they do not use the system estimator described above that allows for the endogeneity of all the regressors and the routine use of lagged dependent variables. They find that the indicators of financial development are correlated with both total factor productivity growth and the accumulation of both physical and human capital. Their paper raises an important qualification, however. Different indicators of financial development are linked with different components of growth (total factor productivity, physical capital accumulation, and human capital accumulation). Their findings reiterate an important qualification running throughout this survey: it is difficult to measure financial development and link empirical constructs with theoretical concepts.

Loayza and Ranciere (2002) extend this line of empirical inquiry by differentiating between the long-run and short-run relationships connecting finance and economic activity. They note that short-run surges in bank lending can actually signal the onset of financial crises and economic stagnation. They stress that it is therefore crucial to consider simultaneously the short-run and long-run effects of financial development. For instance, while finance is positively associated with economic growth in a broad cross-section of countries, this relationship does not hold in Latin America, which has been subject to severe and repeated banking crises. Using a panel, Loayza and Ranciere (2002) estimate an encompassing model of long-run and short-run effects. Using the LLB measure of financial intermediary development (Private Credit), they find that a

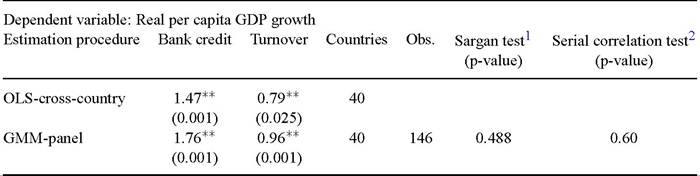

Table 5

Stock markets, banks, and growth: Panel GMM and OLS, 1975-1998

Source: Beck and Levine (2004, Tables 2 and 3).

* Significant atthe 0.10 level.

**Significant atthe 0.05 level.

(p-values in parentheses.)

OLS: Ordinary Least Squares with heteroscedasticity consistent standard errors.

GMM: Dynamic panel Generalized Method of Moments using system estimator.

Bank credit = logarithm(credit by deposit money banks to the private sector as a share of GDP).

Turnover = logarithm(value of the trades of domestic shares on domestic exchanges as a share of market capitalization of domestic shares).

Other explanatory variables included in each of the regression results reported above: logarithm of initial income and logarithm of initial secondary school enrollment.

1 The null hypothesis is that the instruments used are not correlated with the residuals.

2 The null hypothesis is that the errors in the first-difference regression exhibit no second-order serial correlation.

positive long-run relationship between financial development and growth co-exists with a generally negative short-run link.[538]

3.2.3. Dynamic panel results and stock market and bank development

Rousseau and Wachtel (2000) examine the relationship between stock markets, banks, and growth, using annual data and the difference estimator. Beck and Levine (2004) use data averaged over five-year periods to focus on longer-run growth factors, use the system estimator to mitigate potential biases associated with the difference estimator, and extend the sample through 1998 (from 1995).[539]

Table 5 indicates that the exogenous component of both stock market development and bank development help predict economic growth. As shown, the coefficient estimates from the two methods are very similar. The panel procedure passes the standard specification tests, which increases confidence in the assumptions underlying the econometric methodology. While not shown, stock market capitalization is not closely associated with growth. Thus, it is not listing per se that is important for growth; rather, it is the ability of agents to exchange ownership claims on an economy’s productive technologies that is relevant for economic growth.

Table 5 estimates are economically meaningful and consistent with magnitudes obtained using different methods. If Mexico’s Turnover Ratio had been at the average of the OECD countries (68%) instead of the actual 36% during the period 1996-98, it would have grown 0.6 percentage points faster per year. Similarly, if its Bank Credit had been at the average of all OECD countries (71%) instead of the actual 16%, it would have grown 2.6 percentage points faster per year. These results suggest that the exogenous components of both bank and stock market development have an economically large impact on economic growth.

3.2.4. Time series studies

A substantial time-series literature examines the finance-growth relationship using a variety of time-series techniques. These studies frequently use Granger-type causality tests and vector autoregressive (VAR) procedures to examine the nature of the financegrowth relationship [e.g., Arestis and Demetriades (1997)]. Research has progressed by using better measures of financial development, employing more powerful econometric techniques, and by examining individual countries in much greater depth.

Some initial time-series studies emphasize the importance of measuring financial development accurately, suggesting that studies that use more precise measures of financial development tend to find a growth-enhancing impact of financial development. Jung (1986) and Demetriades and Hussein (1996) use measures of financial development such as the ratio of money to GDP. They find the direction of causality frequently runs both ways, especially for developing economies. However, Neusser and Kugler (1998) use measures of the value-added provided by the financial system instead of simple measures of the size of the financial system. They find that finance boosts growth. Furthermore, Rousseau and Wachtel (1998) conduct time-series tests of financial development and growth for five countries over the past century using measures of financial development that include the assets of both banks and non-banks. They document that the dominant direction of causality runs from financial development to economic growth. Finally, Arestis, Demetriades and Luintel (2001) augment time-series studies of finance and growth by using measures of both stock market and bank development. They find additional support for the view that finance stimulates growth but raise some cautions on the size of the relationship. They use quarterly data and apply time series methods to five developed economies and show that while both banking sector and stock market development explain subsequent growth, the effect of banking sector development is substantially larger than that of stock market development. The sample size, however, is very limited and it is not clear whether the use of quarterly data and a vector error correction model fully abstract from high frequency factors influencing the stock market, bank, and growth nexus to focus on long-run economic growth.

Additional econometric sophistication has also been brought to bear on the finance and growth question. In a broad study of 41 countries over the 1960-1993, Xu (2000) uses a VAR approach that permits the identification of the long-term cumulative effects of finance on growth by allowing for dynamic interactions among the explanatory variables.[540] Xu (2000) rejects the hypothesis that finance simply follows growth. Rather, the analyses indicate that financial development is important for long-run growth. More recently, Christopoulos and Tsionas (2004) note that many time-series studies yield unreliable results due to the short time spans of typical data sets. Thus, they use panel unit root tests and panel cointegration analyses to examine the relationship between financial development and economic growth in ten developing countries to yield causality inferences within a panel context that increases sample size. In contrast to Demetriades and Hussein (1996), Christopoulos and Tsionas (2004) find strong evidence in favor of the hypothesis that long-run causality runs from financial development to growth and that there is no evidence of bi-directional causality. Furthermore, they find a unique cointegrating vector between growth and financial development, and emphasize the long-run nature of the relationship between finance and growth.

There has also been a movement away from applying time-series methods to a variety of countries and toward examining individual countries, which allows research to design country-specific measures of financial development and expand the time-series dimension of the analyses in some cases. Rousseau and Sylla (1999) expand Rousseau’s (1998) examination of the historical role of finance in U.S. economic growth to include stock markets. They use a set of multivariate time-series models that relate measures of banking and equity market activity to investment, imports, and business incorporations over the 1790-1850 period. Rousseau and Sylla (1999) find strong support for the theory of “finance led growth” in United States. Moving beyond the U.S., Rousseau and Sylla (2001) study seventeen countries over the period 1850-1997. They also find evidence consistent with the view the financial development stimulated economic growth in these economies. In a study of the Meiji period in Japan (1868-1884), Rousseau (1999) uses a variety of VAR procedures and concludes that the financial sector was instrumental in promoting Japan’s explosive growth prior to the First World War. In a different study, Rousseau (1998) examines the impact of financial innovation in the U.S. on financial depth over the period 1872-1929. Innovation is proxied by reductions in the loan-deposit spread. The impact on the size of the financial intermediary sector is assessed using unobservable components methods. The paper finds that permanent reductions of 1% in the spread of New York banks are associated with increases in financial depth that range from 1.7% to nearly 4%. While not a direct link to growth, these findings develop a direct link running from financial innovation to increases in financial depth, which is commonly associated with economic growth in other studies.

Bekaert, Harvey and Lundblad (2001, 2005) examine the effects of opening equity markets to foreign participation.[541] One statistical innovation in their work is the use of over-lapping data. Many time-series studies use annual observations and even quarterly data to maximize the information included their analyses. Bekaert, Harvey and Lundblad (2005), however, use data averaged over five-year periods to focus on growth rather than higher frequency relationships, but they use over-lapping data to avoid the loss of information inherent in using non-over-lapping data. Specifically, one observation includes data averaged from 1990-1995 and the next period includes data averaged from 1991-1996. They adjust the standard errors accordingly and conduct an array of sensitivity checks, though the procedure does not formally deal with simultaneity bias. Consistent with Levine and Zervos (1998a), Bekaert, Harvey and Lundblad (2001, 2005) show that financial liberalization boosts economic growth by improving the allocation of resources and the investment rate.

3.2.5. Novel case-studies

Jayaratne and Strahan (1996) undertake a fascinating examination of the impact of finance on economic growth by examining individual states of the United States. Since the early 1970s, 35 states relaxed impediments on intrastate branching. They estimate the change in economic growth rates after branch reform relative to a control group of states that did not reform. They use a pooled time-series, cross-sectional dataset to assess the impact of liberalizing branching restrictions on state growth.

Jayaratne and Strahan (1996) show that branch reform boosted bank-lending quality and accelerated real per capita growth rates, while Dehejia and Lleras-Muney (2003) confirm and extend these findings by also examining the impact of deposit insurance. By comparing states within the United States, the paper eliminates problems associated with country-specific factors. The paper also uses a natural identifying condition, the change in branching restrictions, to trace through the impact of financial development on economic growth. Importantly, the paper finds little evidence Ihatbranchreformboosted lending. Rather, branch reform accelerated economic growth by improving the quality of bank loans and the efficiency of capital allocation.[542] Some issues remain, however. While Jayaratne and Strahan (1996) control for state investment and tax receipts, it is difficult to control fully for other factors influencing growth in the individual states. Similarly, while the authors show that (i) there is no correlation between the business cycle and the timing of regulation and (ii) deregulation does not forecast a boom in lending, it is difficult to rule out the possibility that states liberalize banking due to expected growth-enhancing structural changes in the economy that do require more lending but better lending. Dehejia and Lleras-Muney (2003) also examine the growth experiences of states across the U.S. They too find that financial development boosts growth, but they also show that deposit insurance frequently induced indiscriminate credit expansions with adverse effects on growth. Again, the results suggest that it is the quality, not the quantity, of lending that matters. In sum, these innovative studies provide empirical support for the view that well-functioning banks improve the allocation of capital and hence economic growth.

In terms of the early years of the United States, Wright (2002) provides a lucid and detailed examination of how the U.S. financial system drove America’s transformation after 1780 from an agricultural economy to a thriving industrial power. The book’s core thesis is that.. the U.S. financial system created the conditions necessary for the sustained domestic economic growth... that scholars know occurred in the nineteenth century”. Most impressively, Wright’s (2002) research is filled with specific examples of the emergence of new financial arrangement to facilitate the acquisition of information about firms (pp. 26-50), to monitor managers and to align the interests of creditors and firm insiders (pp. 37-41), and to facilitate the trading, hedging, and pooling of risk (pp. 51-75). For example, in response to principal-agent problems, U.S. corporations in the 18th century increasingly forced managers to hold large quantities of stock in the corporation to align their personal financial interests with those of the firm (p. 39). As another example, after suffering through high default rates, U.S. bankers quickly learned to monitor borrowers more carefully by continuously reviewing the cash-flows of borrowers to identify unusual activity, forcing debtors to report their actions at regular board meetings and granting additional privileges only to debtors demonstrating good behavior, and forcing borrowers to allocate funds toward very specific investments along with other very restrictive covenants (pp. 34-35). While the book does not provide formal statistical evidence that financial development accelerated economic growth in the early decades after U.S. independence, Wright (2002) make a different, distinguishing contribution: He documents how specific financial contracts, markets, and institutions arose to ease information and transactions costs and hence influence the resource allocation decisions of a country.

Guiso, Sapienza and Zingales (2002) examine the individual regions of Italy. Using an extraordinary dataset on households and financial services across Italy, they examine the effects of differences in local financial development on economic activity across the regions of Italy. Guiso, Sapienza and Zingales (2002) find that local financial development (i) enhances the probability that an individual starts a business, (ii) increases industrial competition, and (iii) promotes the growth of firms. These results are weaker for large firms, which can more easily raise funds outside of the local area. This study ameliorates many of the weaknesses associated with examining growth across countries.

Consider also Haber’s (1991, 1997) impressive comparison of industrial and capital market development in Brazil, Mexico, and the United States between 1830 and 1930. Using firm-level data, he finds that capital market development affected industrial composition and national economic performance. Specifically, Haber shows that when Brazil overthrew the monarchy in 1889 and formed the First Republic, it also dramatically liberalized restrictions on Brazilian financial markets. The liberalization gave more firms easier access to external finance. Industrial concentration fell and industrial production boomed. While Mexico also liberalized financial sector policies, the liberalization was much more mild underthe Diaz dictatorship (1877-1911), which.. relied on the financial and political support of a small in-group of powerful financial capitalists” (p. 561). As a result, the decline in concentration and the increase in economic growth were much weaker in Mexico than it was in Brazil. Haber (1997) concludes that (1) international differences in financial development significantly impacted the rate of industrial expansion and (2) under-developed financial systems that restrict access to institutional sources of capital also impeded industrial expansion.

In a recent firm-level study of China, Allen, Qian and Qian (2005) find that the linkages between the law, finance and growth are complex. Consistent with broad crosscountry findings discussed above, they find that poor legal protection of minority shareholder rights hinders the growth of publicly listed firms (as well as state-owned firms). However, private firms and firms owned by local governments have grown rapidly in absence of sound formal rules governing shareholder rights. This suggests the existence of effective alternative governance and financing mechanisms that promote firm growth. Additional evidence comes from Cull and Xu (2004), who find that private ownership is associated with firm reinvesting a greater proportion of their earnings than in firms with greater public sector ownership.

Firm-level evidence from France also suggests the importance of well-functioning financial intermediaries for economic growth. Bertrand, Schoar and Thesmar (2004) examine the impact of deregulation in 1985 that eliminated government intervention in bank lending decisions and fostered greater competition in the credit market. They find that after deregulation, banks bailed out poorly performing firms less frequently, increased the cost of capital to poorly performing firms, and induced an increase in allocative efficiency across firms. This lowered industry concentration ratios and boosted both entry and exit rates for firms. While not directly tied to growth, the paper suggests that better functioning banks not only influence bank-firm relations they also exert a first-order impact on the structure and dynamics of product markets.

Intwo classic studies, Cameronetal. (1967) and McKinnon (1973) study respectively (1) the historical relationships between banking development and the early stages of industrialization for England (1750-1844), Scotland (1750-1845), France (1800-1870), Belgium (1800-1875), Germany (1815-1870), Russia (1860-1914), and Japan (18681914) and (2) the relationship between the financial system and economic development in Argentina, Brazil, Chile, Germany, Korea, Indonesia, and Taiwan in the post World War II period. This research does not use formal statistical analysis to resolve causality issues. Instead, the researchers carefully examine the evolution of the political, legal, policy, industrial, and financial systems of the country. The country-case studies document critical interactions among financial intermediaries, financial markets, government policies, and the financing of industrialization. While well-aware of the analytical limitations, these authors bring a wealth of country specific information to bear on the role of finance in economic growth. Cameron (1967b) concludes that especially in Scotland and Japan, but also in Belgium, Germany, England, and Russia, the banking system played a positive, growth-inducing role.[543] McKinnon (1973) interprets the mass of evidence emerging from his country-case studies as suggesting that better functioning financial systems support faster economic growth. Disagreement exists over many of these individual cases, and it is extremely difficult to isolate the importance of any single factor in the process of economic growth. Nonetheless, the body of country-studies suggests that, while the financial system responds to demands from the nonfinancial sector, well-functioning financial systems have, in some cases during some time periods, importantly spurred economic growth.

3.3. Industry andfirm level studies offinance and growth

To better understand the relationship between financial development and economic growth, researchers have employed both industry-level and firm-level data across a broad cross-section of countries. These studies seek to resolve causality issues and to document in greater detail the mechanisms, if any, through which finance influences economic growth.

3.3.1. Industry level analyses

Consider first the influential study by Rajan and Zingales (1998, henceforth RZ). They argue that better-developed financial intermediaries and markets help overcome market frictions that drive a wedge between the price of external and internal finance. Lower costs of external finance facilitate firm growth and new firm formation. Therefore, industries that are naturally heavy users of external finance should benefit disproportionately more from greater financial development than industries that are not naturally heavy users of external finance. From this perspective, if researchers can identify which industries are “naturally heavy users” of external finance - i.e., if they can identify which industries rely heavily on external finance in an economy with few market frictions -

then this establishes a natural test: Do industries that are naturally heavy users of external finance grow faster in economies with better developed financial systems? If they do, then this supports the view that financial development spurs growth by facilitating the flow of external finance.

RZ assume that (1) financial markets in the U.S. are relatively frictionless, (2) in a frictionless financial system, technological factors influence the degree to which an industry uses external finance, and (3) the technological factors influencing external finance are constant (or reasonably constant) across countries. They then examine whether industries that are technologically more dependent on external finance - as defined by external use of funds in the U.S. - grow comparatively faster in countries that are more financially developed. This approach allows RZ (1) to study a particular mechanism, external finance, through which finance operates rather than simply assessing links between finance and growth and (2) to exploit within-country differences concerning industries.

RZ develop a new methodology to examine the finance-growth relationship. Consider their formulation.

Growthiy is the average annual growth rate of value added or the growth in the number of establishments, in industry k and country i, over the period 1980-90. Country and Industry are country and industry dummies, respectively. Shareiy is the share of industry k in manufacturing in country i in 1980. Externalk is the fraction of capital expenditures not financed with internal funds for U.S. firms in the industry k between 1980-90. FDi is an indicator of financial development for country i. RZ interact the external dependence of an industry (External) with financial development (FD), where the estimated coefficient on the interaction, S1, is the focus of their analysis. Thus, if S is significant and positive, then this implies that an increase in financial development (FDi) will induce a bigger impact on industrial growth (Growthi,k) if this industry relies heavily on external finance (Externalk) than if this industry is not a naturally heavy user of external finance. They do not include financial development independently because they focus on within-country, within-industry growth rates. The dummy variables for industries and countries correct for country and industry specific characteristics that might determine industry growth patterns. RZ thus isolate the effect that the interaction of external dependence and financial development/structure has on industry growth rates relative to country and industry means. By including the initial share of an industry, this controls for a convergence effect: industries with a large share might grow more slowly, suggesting a negative sign on γ. RZ include the share in manufacturing rather than the level to focus on within-country, within-industry growth rates.

RZ use data on 36 industries across 42 countries, though the U.S is dropped from the analyses since it is used to identify external dependence. To measure financial development, RZ examine (a) total capitalization, which equals the summation of stock market

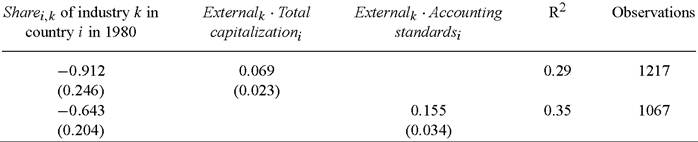

Table 6

Industry growth and financial development

Dependent variable: Growth of value added of industry k in country i, 1980-1990

Source: Rajan and Zingales (1998, Table 4). The table reports the results from the regression:

Two regressions are reported corresponding to two values of FDi, Total capitalization and Account standards respectively.

(Heteroscedasticity robust standard errors are reported in parentheses.) Externalk is the fraction of capital expenditures not financed with internal funds for U.S. firms in industry k between 1980-90.

Total capitalization is stock market capitalization plus domestic credit. Accounting standards is an index of the quality of corporate financial reports.

capitalization and domestic credit as a share of GDP and (b) accounting standards. As RZ discuss, there are problems with these measures. Stock market capitalization does not capture the actual amount of capital raised in equity markets. Indeed, some countries provide tax incentives for firms to list, which artificially boosts stock market capitalization without indicating greater external financing or stock market development. Also, as discussed above, stock market capitalization does not necessarily reflect how well the market facilitates exchange. The accounting standards indicator is a rating of the quality of the annual financial reports issued by companies within a country. The highest value is 90. RZ use the accounting standards measure as a positive signal of the ease with which firms can raise external funds, while noting that it is not a direct measure of the actual amount of external funds that are raised. Beck and Levine (2002) confirm the RZ findings using alternative measures of financial development.

As summarized in Table 6, RZ find that the coefficient estimate for the interaction between external dependence and total capitalization measure, Externalk ∙ Total capitalizationi, is positive and statistically significant at the one-percent level. This implies that an increase in financial development disproportionately boosts the growth of industries that are naturally heavy users of external finance.27

27 Fisman and Love (2003b) critique the Rajan and Zingales (1998) methodology, arguing that it does not accurately test whether financial development boosts growth in externally dependent industries. They argue

RZ note that the economic magnitude is quite substantial. Compare Machinery, which is an industry at the 75th percentile of dependence (0.45), with Beverages, which has low dependence (0.08) and is at the 25th percentile of dependence. Now, consider Italy, which has high total capitalization (0.98) at the 75th percentile of the sample, and the Philippines, which is at the 25th percentile of total capitalization with a value of 0.46. Due to differences in financial development, the coefficient estimates predict that Machinery should grow 1.3 percent faster than Beverages in Italy in comparison to the Philippines.28 The actual difference is 3.4, so the estimated value of 1.3 is quite substantial. Thus, financial development has a substantial impact on industrial growth by influencing the availability of external finance. RZ conduct a large number of robustness checks and show that financial development influences industrial growth both through the expansion of existing establishments and through the formation of new establish- ments29

Instead of examining the impact of banking sector development on the growth of externally dependent firms, recent work studies the impact of banking market structure and bank competition on industrial development. Cetorelli and Gambera (2001) examine the role played by banking sector concentration on firm access to capital. Using the RZ methodology, they show that bank concentration promotes the growth of industries that are naturally heavy users of external finance, but bank concentration has a depressing effect on overall economic growth. Claessens and Laeven (2005) disagree, however. They note that industrial organization theory indicates that market concentration is not necessarily a good proxy for the competitiveness of an industry. Consequently, they estimate an industrial organization-based measure of banking system competition. Claessens and Laeven (2005) then show that industries that are naturally heavy users of external finance grow faster in countries with more competitive banking systems. They find no

that the method simply tests whether financial intermediaries allow firms to respond to global shocks to growth opportunities, rather than the extent to which financial systems foster the growth of industries with an inherent financial dependence.

28 More specifically, let I indicate Italy, P indicate the Philippines, M indicate machinery, B indicate beverages, and g represent the growth of an industry in a country, then the differential growth rate of machinery and beverages in Italy from the difference in growth rate of machinery and beverages in the Philippines is as follows: [{g(I, M)}-{g(P, M)}] — [{g(I, B)} — {g(P, B)}]. Now, inserting estimates one obtains

29 Beck (2002, 2003) extends the work by RZ to examine the linkages between financial development and international trade patterns. Beck (2002) develops a theoretical model in which higher levels of financial development provide countries with a comparative advantage in sectors with greater scale economies and presents econometric evidence consistent with this prediction. Using cross-industry and cross-country data on trade flows, Beck (2003) finds that countries with more developed financial systems tend to be net exporters in industries that are heavy users of external finance. The results of both papers are consistent with the view that financial development influences the structure of trade balances.

evidence that banking industry concentration explains industrial sector growth. The results support the view that banking sector competition fosters the provision of growth enhancing financial services.

Building on RZ, Claessens and Laeven (2003) examine the joint impact of financial sector development and the quality of property rights protection on the access of firms to external finance and the allocation of resources. In particularly, they show that financial sector development hurts growth by hindering the access of firms to external finance and insecure property rights hurts growth by leading to a suboptimal allocation of resources by distorting firms into investing excessively in tangible assets. Thus, even when controlling for property rights protection, financial development continues to influence economic growth. This conclusion is different, however, from Johnson, McMillan and Woodruff’s (2002) study of post-communist countries. They find that property rights dominate access to external finance in explaining the degree to which firms reinvest their profits.

Extending the RZ approach, Beck, DemirguQ-Kunt and Maksimovic (2004) highlight another channel linking finance and growth: removing impediments to small firms. They examine whether industries that are naturally composed of small firms grow faster in financially developed economies. More specifically, as in RZ, they assume that U.S. financial markets are relatively frictionless, so that the sizes of firms within industries in the U.S. reflect technological factors, not financial system frictions. Based on the U.S., they identify the benchmark average firm-size of each industry. Then, comparing across countries and industries, Beck, DemirguQ-Kunt and Maksimovic (2004) show that industries that are naturally composed of smaller firms grow faster in countries with better-developed financial systems. This result is robust to controlling for the RZ measure of external dependence. These results are consistent with the view that small firms face greater informational and contracting barriers to raising funds than large firms, so that financial development is particularly important for the growth of industries that, for technological reasons, are naturally composed of small firms.

Using a different strategy, Wurgler (2000) also employs industry-level data to examine the relation between financial development and economic growth. Using industrylevel data across 65 countries for the period 1963-1995, he computes an investment elasticity that gauges the extent to which a country increases investment in growing industries and decreases investment in declining ones. This is an important contribution because it directly measures the degree to which each country’s financial system reallocates the flow of credit. Wurgler (2000) uses standard measures of financial development. He shows that countries with higher levels of financial development both increase investment more in growing industries and decrease investment more in declining industries than financial underdeveloped economies.

3.3.2. Firm level analyses of finance and growth

DemirguQ-Kunt and Maksimovic (1998, henceforth DM) examine whether financial development influences the degree to which firms are constrained from investing in profitable growth opportunities. They focus on the use of long-term debt and external equity in funding firm growth. As in RZ, DM focuses on a particular mechanism through which finance influences growth: does greater financial development remove impediments to the exploitation of profitable growth opportunities. Rather than focusing on the external financing needs of an industry as in RZ, DM estimate the external financing needs of each individual firm in the sample.

DM note that simple correlations between firms’ growth and financial development do not control for differences in the amount of external financing needed by firms in the same industry in different countries. These differences may arise because firms in different countries employ different technologies, because profit rates may differ across countries, or because investment opportunities and demand may differ. To control for these differences at the firm-level, DM calculate the rate at which each firm can grow using (1) only its internal funds and (2) only its internal funds and short-term borrowing. They then compute the percentage of firms that grow at rates that exceed each of these two estimated rates. This yields estimates of the proportion of firms in each economy relying on external financing to grow.

The firm-level data consist of accounting data for the largest publicly traded manu- factoring firms in 26 countries. Beck, DemirguQ-Kunt and Levine (2001) confirm the findings using an extended sample. DM estimate a firm’s potential growth rate using the textbook “percentage of sales” financial planning model [Higgins (1977)]. This approach relates a firm’s growth rate of sales to its need for investment funds, based on three simplifying assumptions. First, the ratio of assets used in production to sales is constant. Second, the firm’s profits per unit of sales are constant. Finally, the economic deprecation rate equals the accounting depreciation rate. Under these assumptions, the firm’s financing need in period t of a firm growing at gt percent per year is given by  where EFNt is the external financing need and BT is the fraction of the firm’s earnings that are retained for reinvestment at time t. Earnings are calculated after interest and taxes. While the first term on the right-hand side of Equation (5) denotes the required investment for a firm growing at gt percent, the second term is the internally available funds for investment, taking the firms’ dividend payout as given.

where EFNt is the external financing need and BT is the fraction of the firm’s earnings that are retained for reinvestment at time t. Earnings are calculated after interest and taxes. While the first term on the right-hand side of Equation (5) denotes the required investment for a firm growing at gt percent, the second term is the internally available funds for investment, taking the firms’ dividend payout as given.

The short-term financed growth rate STFGt is the maximum growth rate that can be obtained if the firm reinvests all its earnings and obtains enough short-term external resources to maintain the ratio of its short-term liabilities to assets. To compute STFGt, we first replace total assets in (5) by assets that are not financed by new short-term credit, calculated as total assets times one minus the ratio of short-term liabilities to total assets. STFGt is then given by

STFGt = ROLTCt∕(1 - ROLTC t) where ROLTCt is the ratio of earnings, after tax and interest, to long-term capital. The definition of STFG thus assumes that the firm does not access any long-term borrowings or sales of equity to finance its growth.[544]

(6)

DM then calculate the proportion of firms whose growth rates exceed the estimate of the maximum growth rate that can be financed by relying only on internal and shortterm financing, PROPORTION_FASTER.

To analyze whether financial development spurs firm growth, DM run the following cross-country regression

where FD is financial development, CV is a set of control variables, and ε is the error term. To measure financial development, DM use (a) the ratio of market capitalization to GDP (Market Capitalization/GDP), (b) Turnover, which equals the total value of shares traded divided by market capitalization, and (c) Bank Assets/GDP, which equals the ratio of domestic assets of deposit banks divided by GDP Thus, DM include all domestic assets of deposit banks, not just credit to the private sector. As control variables, DM experiment with different combinations of control variables, including economic growth, inflation, the average market to book value of firms in the economy, government subsidies to firms in the economy, the net fixed assets divided by total assets of firms in the economy, the level real per capita GDP, the law and order tradition of the economy.

As summarized in Table 7, DM (1998) find that both banking system development and stock market liquidity are positively associated with the excess growth of firms. Thus, in countries with high Turnover and high Bank Assets/GDP a larger proportion of firms is growing at a level that requires access to external sources of long-term capital, holding other things constant. Note, consistent with LZ, the size of the domestic stock markets is not related to the excess growth of firms. After conducting a wide- array of robustness checks, DM conclude that the proportion of firms that grow at rates exceeding the rate at which each firm can grow with only retained earnings and shortterm borrowing is positively associated with stock market liquidity and banking system size.

Love (2003) and Beck, DemirguQ-Kunt and Maksimovic (2004) also use firm level data to examine whether financial development eases financing constraints, though they do not explicitly examine aggregate economic growth. Love finds that the sensitivity of investment to internal funds is greater in countries with more poorly developed financial

Table 7

Excess growth of firms and external financing

Source: Demirguc-Kunt and Maksimovic (1998, Table V).

(White’s heteroscedasticity consistent standard errors in parentheses.)

* * * Indicates statistical significance at the 1 percent level.