Introduction

1.1. Thequestion

The most trite yet crucial question in the field of economic growth and development is: Why are some countries much poorer than others? Traditional neoclassical growth models, following Solow (1956), Cass (1965) and Koopmans (1965), explain differences in income per capita in terms of different paths of factor accumulation.

In these models, cross-country differences in factor accumulation are due either to differences in saving rates (Solow), preferences (Cass-Koopmans), or other exogenous parameters, such as total factor productivity growth. In these models there are institutions, for example agents have well defined property rights and exchange goods and services in markets, but differences in income and growth are not explained by variation in institutions.The first wave of the more recent incarnations of growth theory, following Romer (1986) and Lucas (1988) differed in the sense that they emphasized that externalities from physical and human capital accumulation could induce sustained steady-state growth. However, they also stayed squarely within the neoclassical tradition of explaining differences in growth rates in terms of preferences and endowments. The second wave of models, particularly Romer (1990), Grossman and Helpman (1991) and Aghion and Howitt (1992), endogenized steady-state growth and technical progress, but their explanation for income differences is similar to that of the older theories. For instance, in the model of Romer (1990), a country may be more prosperous than another if it allocates more resources to innovation, but what determines this is essentially preferences and properties of the technology for creating ‘ideas’.[CCLVII]

Though this theoretical tradition is still vibrant in economics and has provided many insights about the mechanics of economic growth, it has for a long time seemed unable to provide a fundamental explanation for economic growth.

As North and Thomas (1973, p. 2) put it: “the factors we have listed (innovation, economies of scale, education, capital accumulation, etc.) are not causes of growth; they are growth” (italics in original). Factor accumulation and innovation are only proximate causes of growth. In North and Thomas’s view, the fundamental explanation of comparative growth is differences in institutions.What are institutions exactly? North (1990, p. 3) offers the following definition: “Institutions are the rules of the game in a society or, more formally, are the humanly devised constraints that shape human interaction”. He goes on to emphasize the key implications of institutions since, “In consequence they structure incentives in human exchange, whether political, social, or economic”.

Of primary importance to economic outcomes are the economic institutions in society such as the structure of property rights and the presence and perfection of markets. Economic institutions are important because they influence the structure of economic incentives in society. Without property rights, individuals will not have the incentive to invest in physical or human capital or adopt more efficient technologies. Economic institutions are also important because they help to allocate resources to their most efficient uses, they determine who gets profits, revenues and residual rights of control. When markets are missing or ignored (as they were in the Soviet Union, for example), gains from trade go unexploited and resources are misallocated. Societies with economic institutions that facilitate and encourage factor accumulation, innovation and the efficient allocation of resources will prosper.

Central to this chapter and to much of political economy research on institutions is that economic institutions, and institutions more broadly, are endogenous; they are, at least in part, determined by society, or a segment of it. Consequently, the question of why some societies are much poorer than others is closely related to the question of why some societies have much “worse economic institutions” than others.

Even though many scholars including John Locke, Adam Smith, John Stuart Mill, Arthur Lewis, Douglass North and Robert Thomas, and recently many papers in the literature on economic growth and development, have emphasized the importance of economic institutions, we are far from a useful framework for thinking about how economic institutions are determined and why they vary across countries. In other words, while we have good reason to believe that economic institutions matter for economic growth, we lack the crucial comparative static results which will allow us to explain why equilibrium economic institutions differ (and perhaps this is part of the reason why much of the economics literature has focused on the proximate causes of economic growth, largely neglecting fundamental institutional causes).

This chapter has three aims. First, we selectively review the evidence that differences in economic institutions are a fundamental cause of cross-country differences in prosperity. Second, we outline a framework for thinking about why economic institutions vary across countries. We emphasize the potential comparative static results of this framework and also illustrate the key mechanisms through a series of historical examples and case studies. Finally, we highlight a large number of areas where we believe future theoretical and empirical work would be very fruitful.

1.2. The argument

The basic argument of this chapter can be summarized as follows:

1. Economic institutions matter for economic growth because they shape the incentives of key economic actors in society, in particular, they influence investments in physical and human capital and technology, and the organization of production. Although cultural and geographical factors may also matter for economic performance, differences in economic institutions are the major source of cross-country differences in economic growth and prosperity. Economic institutions not only determine the ag-

gregate economic growth potential of the economy, but also an array of economic outcomes, including the distribution of resources in the future (i.e., the distribution of wealth, of physical capital or human capital).

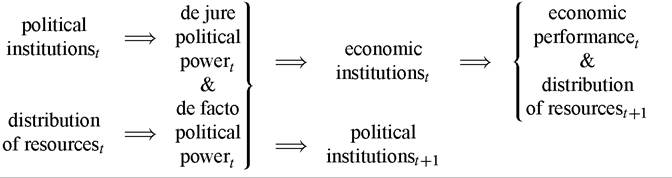

In other words, they influence not only the size of the aggregate pie, but how this pie is divided among different groups and individuals in society. We summarize these ideas schematically as (where the subscript t refers to current period and t + 1 to the future):economic institutionst =⇒

economic performancet distribution of resourcest+1

2. Economic institutions are endogenous. They are determined as collective choices of the society, in large part for their economic consequences. However, there is no guarantee that all individuals and groups will prefer the same set of economic institutions because, as noted above, different economic institutions lead to different distributions of resources. Consequently, there will typically be a conflict of interest among various groups and individuals over the choice of economic institutions. So how are equilibrium economic institutions determined? If there are, for example, two groups with opposing preferences over the set of economic institutions, which group’s preferences will prevail? The answer depends on the political power of the two groups. Although the efficiency of one set of economic institutions compared with another may play a role in this choice, political power will be the ultimate arbiter. Whichever group has more political power is likely to secure the set of economic institutions that it prefers. This leads to the second building block of our framework:

political powert =⇒ economic institutionst.

3. Implicit in the notion that political power determines economic institutions is the idea that there are conflicting interests over the distribution of resources and therefore indirectly over the set of economic institutions. But why do the groups with conflicting interests not agree on the set of economic institutions that maximize aggregate growth (the size of the aggregate pie) and then use their political power simply to determine the distribution of the gains? Why does the exercise of political power lead to economic inefficiencies and even poverty? We will explain that this is because there are commitment problems inherent in the use of political power.

Individuals who have political power cannot commit not to use it in their best interests, and this commitment problem creates an inseparability between efficiency and distribution because credible compensating transfers and side-payments cannot be made to offset the distributional consequences of any particular set of economic institutions.4. The distribution of political power in society is also endogenous, however. In our framework, it is useful to distinguish between two components of political power, which we refer to as de jure (institutional) and de facto political power. Here de jure political power refers to power that originates from the political institutions in society. Political institutions, similarly to economic institutions, determine the constraints on and the incentives of the key actors, but this time in the political sphere. Examples of political institutions include the form of government, for example, democracy vs. dictatorship or autocracy, and the extent of constraints on politicians and political elites. For example, in a monarchy, political institutions allocate all de jure political power to the monarch, and place few constraints on its exercise. A constitutional monarchy, in contrast, corresponds to a set of political institutions that reallocates some of the political power of the monarch to a parliament, thus effectively constraining the political power of the monarch. This discussion therefore implies that:

political Institutionstz =⇒ de jure political power,.

5. There is more to political power than political institutions, however. A group of individuals, even if they are not allocated power by political institutions, for example as specified in the constitution, may nonetheless possess political power. Namely, they can revolt, use arms, hire mercenaries, co-opt the military, or use economically costly but largely peaceful protests in order to impose their wishes on society. We refer to this type of political power as de facto political power, which itself has two sources.

First, it depends on the ability of the group in question to solve its collective action problem, i.e., to ensure that people act together, even when any individual may have an incentive to free ride. For example, peasants in the Middle Ages, who were given no political power by the constitution, could sometimes solve the collective action problem and undertake a revolt against the authorities. Second, the de facto power of a group depends on its economic resources, which determine both their ability to use (or misuse) existing political institutions and also their option to hire and use force against different groups. Since we do not yet have a satisfactory theory of when groups are able to solve their collective action problems, our focus will be on the second source of de facto political power, hence:distribution of resources, =⇒ de facto political power,.

6. This brings us to the evolution of one of the two main state variables in our framework, political institutions (the other state variable is the distribution of resources, including distribution of physical and human capital stocks, etc.). Political institutions and the distribution of resources are the state variables in this dynamic system because they typically change relatively slowly, and more importantly, they determine economic institutions and economic performance both directly and indirectly. Their direct effect is straightforward to understand. If political institutions place all political power in the hands of a single individual or a small group, economic institutions that provide protection of property rights and equal opportunity for the rest of the population are difficult to sustain. The indirect effect works through the channels discussed above: political institutions determine the distribution of de jure political power, which in turn affects the choice of economic institutions. This framework therefore introduces a natural concept of a hierarchy of institutions, with political institutions influencing equilibrium economic institutions, which then determine economic outcomes.

Political institutions, though slow changing, are also endogenous. Societies transition from dictatorship to democracy, and change their constitutions to modify the constraints on power holders. Since, like economic institutions, political institutions are collective choices, the distribution of political power in society is the key determinant of their evolution. This creates a tendency for persistence: political institutions allocate de jure political power, and those who hold political power influence the evolution of political institutions, and they will generally opt to maintain the political institutions that give them political power. However, de facto political power occasionally creates changes in political institutions. While these changes are sometimes discontinuous, for example when an imbalance of power leads to a revolution or the threat of revolution leads to major reforms in political institutions, often they simply influence the way existing political institutions function, for example, whether the rules laid down in a particular constitution are respected as in most functioning democracies, or ignored as in current- day Zimbabwe. Summarizing this discussion, we have:

political power, =⇒ political institutions/+1.

Putting all these pieces together, a schematic (and simplistic) representation of our framework is as follows:

The two state variables are political institutions and the distribution of resources, and the knowledge of these two variables at time, is sufficient to determine all the other variables in the system. While political institutions determine the distribution of de jure political power in society, the distribution of resources influences the distribution of de facto political power at time,. These two sources of political power, in turn, affect the choice of economic institutions and influence the future evolution of political institutions. Economic institutions determine economic outcomes, including the aggregate growth rate of the economy and the distribution of resources at time, +1. Although economic institutions are the essential factor shaping economic outcomes, they are themselves endogenous and determined by political institutions and distribution of resources in society.

There are two sources of persistence in the behavior of the system: first, political institutions are durable, and typically, a sufficiently large change in the distribution of political power is necessary to cause a change in political institutions, such as a transition from dictatorship to democracy. Second, when a particular group is rich relative to others, this will increase its de facto political power and enable it to push for economic and political institutions favorable to its interests. This will tend to reproduce the initial relative wealth disparity in the future. Despite these tendencies for persistence, the framework also emphasizes the potential for change. In particular, “shocks”, including changes in technologies and the international environment, that modify the balance of

(de facto) political power in society and can lead to major changes in political institutions and therefore in economic institutions and economic growth.

A brief example might be useful to clarify these notions before commenting on some of the underlying assumptions and discussing comparative statics. Consider the development of property rights in Europe during the Middle Ages. There is no doubt that lack of property rights for landowners, merchants and proto-industrialists was detrimental to economic growth during this epoch. Since political institutions at the time placed political power in the hands of kings and various types of hereditary monarchies, such rights were largely decided by these monarchs. Unfortunately for economic growth, while monarchs had every incentive to protect their own property rights, they did not generally enforce the property rights of others. On the contrary, monarchs often used their powers to expropriate producers, impose arbitrary taxation, renege on their debts, and allocate the productive resources of society to their allies in return for economic benefits or political support. Consequently, economic institutions during the Middle Ages provided little incentive to invest in land, physical or human capital, or technology, and failed to foster economic growth. These economic institutions also ensured that the monarchs controlled a large fraction of the economic resources in society, solidifying their political power and ensuring the continuation of the political regime.

The seventeenth century, however, witnessed major changes in the economic and political institutions that paved the way for the development of property rights and limits on monarchs’ power, especially in England after the Civil War of 1642 and the Glorious Revolution of 1688, and in the Netherlands after the Dutch Revolt against the Haps- burgs. How did these major institutional changes take place? In England, for example, until the sixteenth century the king also possessed a substantial amount of de facto political power, and leaving aside civil wars related to royal succession, no other social group could amass sufficient de facto political power to challenge the king. But changes in the English land market [Tawney (1941)] and the expansion of Atlantic trade in the sixteenth and seventeenth centuries [Acemoglu, Johnson and Robinson (2005)] gradually increased the economic fortunes, and consequently the de facto power of landowners and merchants. These groups were diverse, but contained important elements that perceived themselves as having interests in conflict with those of the king: while the English kings were interested in predating against society to increase their tax incomes, the gentry and merchants were interested in strengthening their property rights.

By the seventeenth century, the growing prosperity of the merchants and the gentry, based both on internal and overseas, especially Atlantic, trade, enabled them to field military forces capable of defeating the king. This de facto power overcame the Stuart monarchs in the Civil War and Glorious Revolution, and led to a change in political institutions that stripped the king of much of his previous power over policy. These changes in the distribution of political power led to major changes in economic institutions, strengthening the property rights of both land and capital owners and spurred a process of financial and commercial expansion. The consequence was rapid economic growth, culminating in the Industrial Revolution, and a very different distribution of economic resources from that in the Middle Ages.

It is worth returning at this point to two critical assumptions in our framework. First, why do the groups with conflicting interests not agree on the set of economic institutions that maximize aggregate growth? So in the case of the conflict between the monarchy and the merchants, why does the monarchy not set up secure property rights to encourage economic growth and tax some of the benefits? Second, why do groups with political power want to change political institutions in their favor? For instance, in the context of the example above, why did the gentry and merchants use their de facto political power to change political institutions rather than simply implement the policies they wanted? The answers to both questions revolve around issues of commitment and go to the heart of our framework.

The distribution of resources in society is an inherently conflictual, and therefore political, decision. As mentioned above, this leads to major commitment problems, since groups with political power cannot commit to not using their power to change the distribution of resources in their favor. For example, economic institutions that increased the security of property rights for land and capital owners during the Middle Ages would not have been credible as long as the monarch monopolized political power. He could promise to respect property rights, but then at some point, renege on his promise, as exemplified by the numerous financial defaults by medieval kings [e.g., Veitch (1986)]. Credible secure property rights necessitated a reduction in the political power of the monarch. Although these more secure property rights would foster economic growth, they were not appealing to the monarchs who would lose their rents from predation and expropriation as well as various other privileges associated with their monopoly of political power. This is why the institutional changes in England as a result of the Glorious Revolution were not simply conceded by the Stuart kings. James II had to be deposed for the changes to take place.

The reason why political power is often used to change political institutions is related. In a dynamic world, individuals care not only about economic outcomes today but also in the future. In the example above, the gentry and merchants were interested in their profits and therefore in the security of their property rights, not only in the present but also in the future. Therefore, they would have liked to use their (de facto) political power to secure benefits in the future as well as the present. However, commitment to future allocations (or economic institutions) was not possible because decisions in the future would be decided by those who had political power in the future with little reference to past promises. If the gentry and merchants would have been sure to maintain their de facto political power, this would not have been a problem. However, de facto political power is often transient, for example because the collective action problems that are solved to amass this power are likely to resurface in the future, or other groups, especially those controlling de jure power, can become stronger in the future. Therefore, any change in policies and economic institutions that relies purely on de facto political power is likely to be reversed in the future. In addition, many revolutions are followed by conflict within the revolutionaries. Recognizing this, the English gentry and merchants strove not just to change economic institutions in their favor following their victories against the Stuart monarchy, but also to alter political institutions and the future allocation of de jure power. Using political power to change political institutions then emerges as a useful strategy to make gains more durable. The framework that we propose, therefore, emphasizes the importance of political institutions, and changes in political institutions, as a way of manipulating future political power, and thus indirectly shaping future, as well as present, economic institutions and outcomes.

This framework, though abstract and highly simple, enables us to provide some preliminary answers to our main question: why do some societies choose “good economic institutions”? At this point, we need to be more specific about what good economic institutions are. A danger we would like to avoid is that we define good economic institutions as those that generate economic growth, potentially leading to a tautology. This danger arises because a given set of economic institutions may be relatively good during some periods and bad during others. For example, a set of economic institutions that protects the property rights of a small elite might not be inimical to economic growth when all major investment opportunities are in the hands of this elite, but could be very harmful when investments and participation by other groups are important for economic growth [see Acemoglu (2003b)]. To avoid such a tautology and to simplify and focus the discussion, throughout we think of good economic institutions as those that provide security of property rights and relatively equal access to economic resources to a broad cross-section of society. Although this definition is far from requiring equality of opportunity in society, it implies that societies where only a very small fraction of the population have well-enforced property rights do not have good economic institutions. Consequently, as we will see in some of the historical cases discussed below, a given set of economic institutions may have very different implications for economic growth depending on the technological possibilities and opportunities.

Given this definition of good economic institutions as providing secure property rights for a broad cross-section of society, our framework leads to a number of important comparative statics, and thus to an answer to our basic question. First, political institutions that place checks on those who hold political power, for example, by creating a balance of power in society, are useful for the emergence of good economic institutions. This result is intuitive; without checks on political power, power holders are more likely to opt for a set of economic institutions that are beneficial for themselves and detrimental for the rest of society, which will typically fail to protect property rights of a broad cross-section of people. Second, good economic institutions are more likely to arise when political power is in the hands of a relatively broad group with significant investment opportunities. The reason for this result is that, everything else equal, in this case power holders will themselves benefit from secure property rights.[258] Third, good economic institutions are more likely to arise and persist when there are only limited rents that power holders can extract from the rest of society, since such rents would encourage them to opt for a set of economic institutions that make the expropriation of others possible. These comparative statics therefore place political institutions at the center of the story, as emphasized by our term “hierarchy of institutions” above. Political institutions are essential both because they determine the constraints on the use of (de facto and de jure) political power and also which groups hold de jure political power in society. We will see below how these comparative statics help us understand institutional differences across countries and over time in a number of important historical examples.

1.3. Outline

In the next section we discuss how economic institutions constitute the basis for a fundamental theory of growth, and we contrast this with other potential fundamental theories. In Section 3 we consider some empirical evidence that suggests a key role for economic institutions in determining long-run growth. We also emphasize some of the key problems involved in establishing a causal relationship between economic institutions and growth. We then show in Section 4 how the experience of European colonialism can be used as a ‘natural experiment’ which can address these problems. Having established the central causal role of economic institutions and their importance relative to other factors in cross-country differences in economic performance, the rest of the paper focuses on developing a theory of economic institutions. Section 5 discusses four types of explanation for why countries have different institutions, and argues that the most plausible is the social conflict view. According to this theory, bad institutions arise because the groups with political power benefit from bad institutions. The emphasis on social conflict arises naturally from our observation above that economic institutions influence the distribution of resources as well as efficiency. Different groups or individuals will therefore prefer different institutions and conflict will arise as each tries to get their own way. Section 6 delves deeper into questions of efficiency and asks why a political version of the Coase Theorem does not hold. We emphasize the idea that commitment problems are intrinsic to the exercise of political power. In Section 7 we argue that a series of historical examples of diverging economic institutions are best explained by the social conflict view. These examples illustrate how economic institutions are determined by the distribution of political power, and how this distribution is influenced by political institutions. Section 8 puts these ideas together to build our theory of institutions. In Section 9 we then consider two more extended examples of the theory in action, the rise of constitutional rule in early modern Europe, and the creation of mass democracy, particularly in Britain, in the nineteenth and twentieth centuries. Section 10 concludes with a discussion of where this research program can go next.

2.