Introduction: neo-classical growth theory

The premise of neo-classical growth theory is that it is possible to do a reasonable job of explaining the broad patterns of economic change across countries, by looking at it through the lens of an aggregate production function.

The aggregate production function relates the total output of an economy (a country, for example) to the aggregate amounts of labor, human capital and physical capital in the economy, and some simple measure of the level of technology in the economy as a whole. It is formally represented as parameter.

parameter. The aggregate production function is not meant to be something that physically exists. Rather, it is a convenient construct. Growth theorists, like everyone else, have in mind a world where production functions are associated with people. To see how they proceed, let us start with a model where everyone has the option of starting a firm, and when they do, they have access to an individual production function

where Kp and Kh are the amounts of physical and human capital invested in the firm and L is the amount of labor. θ is a productivity parameter which may vary over time, but at any point of time is a characteristic of the firm’s owner. Assume that F is increasing in all its inputs. To make life simpler, assume that there is only one final good in this economy and physical capital is made from it. Also assume that the population of the economy is described by a distribution function Gt (W, θ), the joint distribution of W and θ, where W is the wealth of a particular individual and θ is his productivity parameter. Let G(θ), the corresponding partial distribution on θ,be atomless.

The lives of people, as is often the case in economic models, is rather dreary: In each period, each person, given his wealth, his θ and the prices of the inputs, decides whether to set up a firm, and if so how to invest in physical and human capital. At the end of the period, once he gets returns from the investment and possibly other incomes, he consumes and the period ends. The consumption decision is based on maximizing the following utility function:

1.1. The aggregate production function

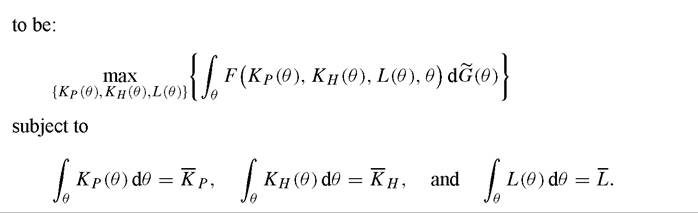

The key assumption behind the construction of the aggregate production function is that all factor markets are perfect, in the sense that individuals can buy or sell as much as they want at a given price. With perfect factor markets (and no risk) the market must allocate the available supply of inputs to maximize total output. Assuming that the distribution of productivities does not vary across countries, we can therefore define

This is the aggregate production function. It is notable that the distribution of wealth does not enter anywhere in this calculation. This reflects the fact that with perfect factor markets, there is no necessary link between what someone owns and what gets used in the firm that he owns. The fact that , does not enter as an argument of

, does not enter as an argument of  reflects our assumption that the distribution of productivities does not vary across countries.

reflects our assumption that the distribution of productivities does not vary across countries.

It should be clear from the construction that there is no reason to expect a close relation between the “shape” of the individual production function and the shape of the aggregate function.

Indeed it is well known that aggregation tends to convexify the production set: In other words, the aggregate production function may be concave even if the individual production functions are not. In this environment where there are a continuum of firms, the (weak) concavity of the aggregate production function is guaranteed as long Kp, kh, L and θ. It follows that the concavity of the individual functions is sufficient for the concavity of the aggregate but by no means necessary: The aggregate production function would also be concave if the individual production functions were S-shaped (convex to start out and then becoming concave). Alternately, the individual production function being bounded is enough to guarantee concavity of the aggregate production function. Moreover, the aggregate production function will typically be differentiable almost everywhere.

Kp, kh, L and θ. It follows that the concavity of the individual functions is sufficient for the concavity of the aggregate but by no means necessary: The aggregate production function would also be concave if the individual production functions were S-shaped (convex to start out and then becoming concave). Alternately, the individual production function being bounded is enough to guarantee concavity of the aggregate production function. Moreover, the aggregate production function will typically be differentiable almost everywhere. It is a corollary of this result that the easiest way to generate an aggregate production function with increasing returns is to base the increasing returns not on the shape of the individual production function, but rather on the possibility of externalities across firms. If there are sufficiently strong positive externalities between investment in one firm and investment in another, increasing the total capital stock in all of them together will increase aggregate output by more (in proportional terms) than the same increase in a single firm would raise the firm’s output, which could easily make the aggregate production function convex. This is the reason why externalities have been intimately connected, in the growth literature, with the possibility of increasing returns.

The assumption of perfect factor markets is therefore at the heart of neo-classical growth theory. It buys us two key properties: The fact that the ownership of factors does not matter, i.e., that an aggregate production function exists; and that it is concave.

The next sub-section shows how powerful these two assumptions can be.

construction of the aggregate production function and to suggest an alternative approach to growth theory that abandons the aggregate production.

We start by discussing, in Section 2, the two implications of the neo-classical model that are at the root of the convergence result: Both rates of returns and investment rates should be higher in poor countries. We show that, in fact, neither rates of returns nor investment are, on average, much higher in poor countries. Moreover, contrary to what the aggregate production approach implies, there are large variations in rate of returns within countries, and large variation in the extent to which profitable investment opportunities are exploited.

In Section 3, we ask whether the puzzle (of no convergence) can be solved, while maintaining the aggregate production function, by theories that focus on reasons for technological backwardness in poor countries. We argue that this class of explanations is not consistent with the empirical evidence which suggests that many firms in poor countries do use the latest technologies, while others in the same country use obsolete modes of production. In other words, what we need to explain is less the overall technological backwardness and more why some firms do not adopt profitable technologies that are available to them (though perhaps not affordable).

In Section 4, we attempt to suggest some answers to the question of why firms and people in developing countries do not always avail themselves of the best opportunities afforded to them. We review various possible sources of the inefficient use of resources: government failures, credit constraints, insurance failure, externalities, family dynamics, and behavioral issues. We argue that each of these market imperfections can explain why investment may not always take place where the rates of returns are the highest, and therefore why resources may be misallocated within countries.

This misallocation, in turn, drives down returns and this may lower the overall investment rate. In Section 5, we calibrate plausible magnitudes for the aggregate static impact of misallocation of capital within countries. We show that, combined with individual production functions characterized by fixed costs, the misallocation of capital implied by the variation of the returns to capital observed within countries can explain the main aggregate puzzles: the low aggregate productivity of capital, and the low Total Factor Productivity in developing countries, relative to rich countries. Non-aggregative growth models thus seem to have the potential to explain why poor countries remain poor.The last section provides an introduction to an alternative growth theory that does not require the existence of an aggregate production function, and therefore can accommodate the misallocation of resources. We then review the attempts to empirically test these models. We argue that the failure to take seriously the implications of non-aggregative models have led to results that are very hard to interpret. To end, we discuss an alternative empirical approach illustrated by some recent calibration exercises based on growth models that take the misallocation of resources seriously.

2.