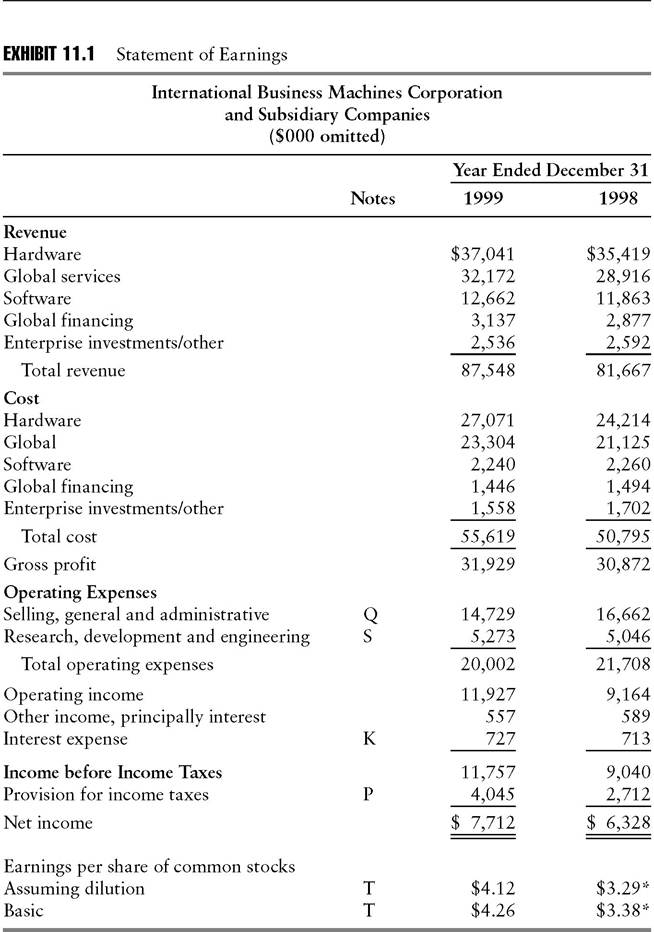

In 1999, International Business Machines (IBM) reported operating income of $11,927 billion. Of that amount, $799 million, or 6.7%, had nothing directly to do with the sale of computers.

Instead, it represented investment returns on the computer manufacturer’s pension plans.

Under SFAS No.

87, “Accounting for Pensions,” the investment returns on a corporate pension plan’s investment portfolio flow into the sponsoring company’s operating income. Management can elect to capitalize all or a portion of the year’s net pension benefit (cost) as part of inventory and then run it through cost of goods sold. Alternatively, the company can recognize the pension-related income by reducing its selling, general, and administrative expenses.As Exhibit 11.1 shows, IBM’s income statement for 1999 does not break out this component of earnings. The statement highlights several Notes to Financial Statements (indicated by the letters K, P, Q, S, and T), but not Note W (“Retirement Plans”). Neither does IBM mention the impact of pension-related income in the 1999 Management Discussion. To ascertain the pension plans’ $799 million contribution to the bottom line, analysts must be diligent in plucking from Note W the net p eriodic pension benefit of $638 million for U.S. plans and $161 million for non-U.S. plans.

By contrast, the Management Discussion in General Electric’s 1999 annual report explicitly refers to pension-related income, which represented a smaller portion (4.1%) of GE’s operating income than IBM’s.1

Principally because of the funding status of the GE Pension Plan (described in Note 5) and other benefit plans (described in Note 6), principal U.S. postemployment benefit plans contributed cost reductions of $1,062 million and $703 million in 1999 and 1998, respectively.2

There is a good reason why General Electric does, and analysts should, take careful note of pension-related income, even though IBM makes no effort to draw attention to it.

During any given year, net pension cost or benefit depends importantly on the short-run return that the pension plan

The indicated notes appear on pages 69 through 92 of the IBM document. *Adjusted to reflect a two-for-one stock split effective May 10, 1999. Source: IBM 1999 Annual Report.

earns on its assets. As explained in Exhibit 11.2, the plan’s expected return increases if the market-related value of plan assets increases.

The 1996-1999 period was a bull market for stocks. Not surprisingly, a growing portion of IBM’s reported earnings reflected the rising value of the pension plan’s investment portfolio, as opposed to management’s effectiveness in producing and marketing competitive products. From 1.8% of operating income in 1996, net pension benefit grew to 6.7%, as already noted, in 1999. When projecting IBM’s future earnings, it is important to segregate genuinely business-related income from profits on retirement plans. Otherwise, the analysis will give management undeserved credit for a general rise in stock prices.

lang=EN-US style='font-size:10.0pt'>Accounting specialists within investment bank Bear Stearns’s research department used the IBM example to underscore further the importance of scrutinizing pension plan disclosures in the Notes to Financial Statements. They stripped IBM’s 1999 operating income of all pension and retiree health effects except service cost, which represents the present value of future benefits earned by employees in the current year. This purer measure of earnings from operations grew at a compound annual growth rate (CAGR) of 38%, far below the 97% CAGR for the version of operating income that IBM reported.3 No other company in the Standard & Poor’s 500 index had as wide a disparity in CAGR, calculated in terms of reported and adjusted operating income for the period.

Considering the key role that compound annual growth rates play in stock valuations (see Chapter 14), it behooves analysts to scrutinize the impact of net pension cost (benefit) on operating income, even if the reporting company does not remind them to explore that subtlety.Analysts should also note that the accounting rules for pension income allow management, within certain bounds, to divert earnings from the nonoperating to the operating category. Such a transfer involves form more than substance. Nevertheless, it may raise the company’s stock price because investors value operating income more highly than the non-operating variety.

To illustrate, suppose that a company accumulates more cash than its business requires. If management leaves the cash in the current assets section of its balance sheet and invests it, the dividends and interest thereby generated must be recorded as other income. By using the cash to step up the funding of the pension plan, however, management can produce operating income under SFAS No. 87, as explained previously. Fortunately for unwary investors, the exploitation of this quirk is limited by Internal Revenue Service rules that discourage excessive funding of pension plans.

Another matter meriting close attention involves the multiple opportunities for earnings management that pension accounting provides. To begin

EXHIBIT 11.2 Components of Net Pension Cost (Benefit)

Service cost

Present value of retirement benefits earned by employees working during the current year.

Interest cost on the benefit obligation

Interest cost arising from deferred payment of previously earned retirement benefits. (The benefit obligation consists of all earned and unpaid service cost.)

Amortization of net deferred gains and losses

Deferred recognition of actual earnings on the pension portfolio above or below the expected return and changes in the benefit obligation that arise from changes in the assumptions (including such items as the discount rate, employee turnover, and mortality) used to estimate it.

Amortization of prior service cost

Recognition over several periods of an increase or decrease in the benefit obligation that results from the employer deciding to increase or reduce the amount that it expects to pay retired employees for services already performed.

Amortization of the transition amount

Amortization of the difference (either positive or negative) between the benefit obligation and the fair value of the assets in the fund at the time the company adopted FAS No.

87 (sometime between January 1, 1985 and January 1, 1987).Gain or loss recorded due to a settlement or curtailment

Current recognition of some or all previously deferred gains and losses and prior service costs. A settlement occurs when an employer takes an irrevocable action to relieve itself of primary responsibility for the benefit obligation. A curtailment occurs when an employer significantly reduces the expected years of service of existing employees or eliminates the accrual of defined benefits for some or all of existing employees’ future service.

Expected return on plan assets

A deduction from the other components of pension cost that is a surrogate for the annual return on the fund’s assets. Defined as the product of an expected long-term rate of return and a market-related value of plan assets. Expected return is used in lieu of actual return to minimize annual fluctuations in net pension cost (benefit) resulting from volatility in stock and bond prices.

Adapted from Pat McConnell, Janet Pegg, and David Zion, “Retirement Benefits Impact Operating Income,” Bear Stearns, September 17, 1999, pp. 21-22. with, GAAP specifies no period for amortizing the deferred amounts by which the plan’s actual earnings exceed or fall short of expected earnings. Five-to-seven-year amortization is typical, but management may abruptly alter the period to boost or restrain reported earnings as desired.

Furthermore, SFAS No. 87 provides little guidance on determining the expected rate. In principle, one would expect a company to base its assumption on the long-run rates of return observed in stocks, bonds, and other types of investments. Once in a great while, the plan might overhaul its long- range investment strategy.

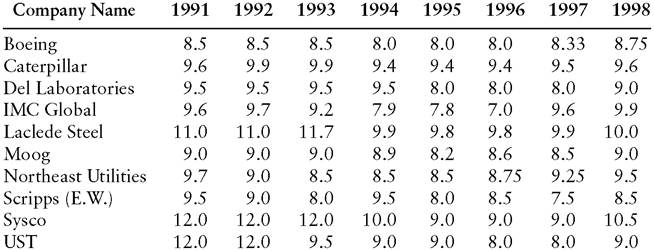

The plan’s trustees might deemphasize bonds in favor of a heavier concentration in common stocks, which entail greater risk but have historically provided higher returns. On still rarer occasions, the pension plan’s actuaries might conclude that a profound structural change in the financial markets warranted a revision of the expected return. Under no reasonable scenario, however, would the plan’s expected return rise or fall with each annual report. Implicit in the long-run expectation is an assumption that returns will fluctuate from one year to the next.In light of this reasoning, some companies’ expectations for long-run return change with remarkable frequency. Two of the corporations in Exhibit 11.3 (IMC Global and E.W. Scripps) revised their expected returns seven years in succession. Boeing displayed extraordinary confidence in fine-tuning its forecast of investment performance, raising its expected return by 0.33% in 1997 and nudging it up another 0.42% the following year. Note, too, that the companies did not simply grow steadily more optimistic or pessimistic over the period shown. Instead, they lowered

EXHIBIT 11.3 Expected Return on Plan Assets (Percent)—Selected Companies

Source: Standard & Poor’s Compustat.

their expected returns during the mid-1990s, by and large, then raised them again toward the end of the decade. Skeptical analysts are bound to suspect corporate managers of ratcheting expected returns up and down to smooth reported operating earnings, rather than to reflect profound, long-lasting changes in the financial markets.

A final point to keep in mind regarding pension plans is that management cannot invariably modulate their impact on reported earnings as desired.

Among the effects described in Exhibit 11.2 is the gain or loss that may arise from settlement of a pension liability. Such events may be large enough to spoil attempts to fine-tune the bottom line.Westinghouse Electric’s 1994 performance represented a case in point. Management cut 1,200 jobs as part of a corporate restructuring. As a result, the company was obliged to distribute pension benefits in lump sums to the employees eliminated in the program. Under SFAS No. 88 (“Employers’ Accounting for Settlements and Curtailments of Defined Benefit Pension Plans and for Termination of Benefits”), management had no choice but to recognize a $308 million loss. This was a highly material item, considering that pretax income from continuing operations, before minority interest, came to only $157 million in 1994.