Anatomy of the Crisis

The financial crisis began in the most financially murky part of the financial world, the ABCP market, which has been termed “shadow banking” (Gorton, 2010; Lowenstein, 2010). That market had for many years been the place where banks and firms had gone to borrow money to fund their activities short term.

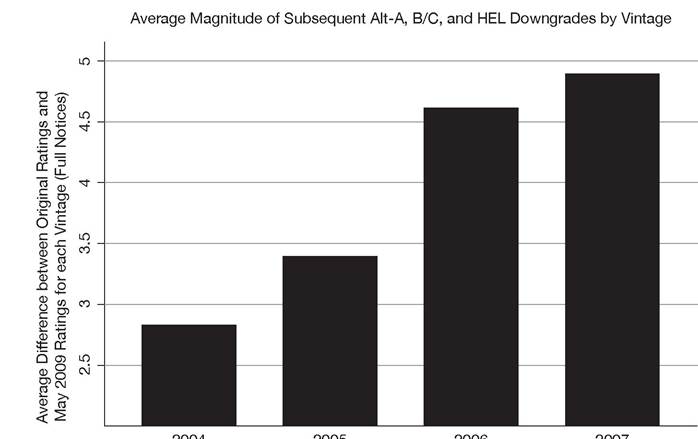

But when the mortgage market shifted from conventional to nonconventional mortgages, the use of the ABCP exploded to provide the capital to produce and fund the purchase of MBSs and CDOs. Whereas previously this market provided funding for the production of securities, after 2004, financial institutions began to use the market to fund their holdings of these instruments (Acharya et al., 2013). They were thus not borrowing money long term but borrowing short term to fund their investments in MBS and CDO structured investment vehicles.Many observers have sought to locate the cause of the financial crisis in one or another part of the chain that produced mortgages and ended up placing them with investors (see the papers in Lounsbury and Hirsch [2010] for different views of this process). But my analysis shows that this misunderstands the nature of the system that was built. By 2007, the largest players in all of these markets had become vertically integrated. Investment banks purchased originators, and savings and loans, commercial banks, and mortgage banks produced securities. All of them bought and sold those securities for their own accounts. By being vertically integrated, banks were able to maximize their profits by making sure that all of the gains in the process accrued to them (Wilmarth, 2009). Countrywide Financial pioneered this model in the 1990s, and every bank that followed them profited greatly. One of the reasons this business model was so successful was the extremely large size of the mortgage market. With originations over $2.5 trillion from 2002 until 2007, up from $1 trillion in 2001, the opportunities to make huge profits were available to all who participated.

But like many business models that are built for one set of market conditions, this business model failed miserably when the number of mortgages for origination decreased and the ability of mortgagors to keep paying those mortgages declined. Because banks were locked into the model of vertical integration, it proved impossible for them to shift their businesses when house prices declined, mortgagors began to be delinquent on their payments, and foreclosures spiked. But as the mortgages failed, the MBSs and CDOs that required people to pay their mortgages every month to produce cash flow started to fail as well. This forced ratings companies to begin to downgrade all tranches of all bonds. For most banks that were holding these instruments using borrowed money, this meant that they had to either increase their collateral by putting down more money or else seek out new funding. The market for MBSs and CDOs that were being produced eventually dried up as well. Banks who were producing and holding these instruments found themselves running short of funds (i.e., a liquidity crisis) and eventually becoming insolvent. Because many of these banks held their MBSs and CDOs in SIVs that were off books and therefore did not need to be protected by the holding of additional capital, they found that their capital quickly ran out.

It follows that the banks that were most at risk in this process were those who were involved in all phases of mortgage securitization (Goldstein and Fligstein, 2017). After all, if you were making profits off of originating mortgages, producing securities, and holding them using borrowed money off books, and all of these businesses went into decline, you were more at risk than if you were in only one of these businesses. Even more important, given that your entire organization depended on the throughput of mortgages, it became very difficult to shift your business activities as mortgages became harder to find and riskier.

It is useful to document the events as they unfolded from 2003 to 2008.

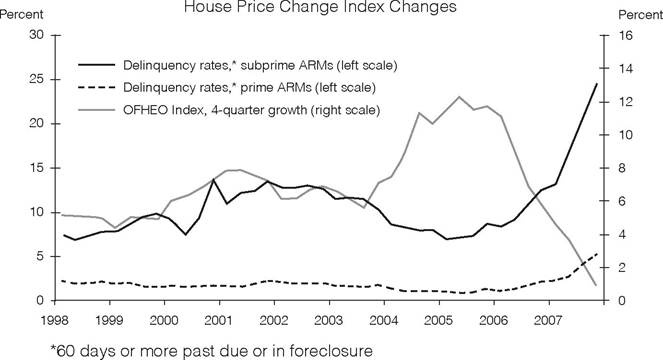

Beginning in January 2003, the Federal Reserve began to raise interest rates. This meant that households that wanted to refinance their home or buy a new one had to borrow at higher interest rates to do so. By January 2007, these rates peaked at 6.25 percent. While the higher rates would eventually affect the availability of new mortgages, mortgage originations fell from their peak in 2003 of almost $4 trillion to $3 trillion from 2004 to 2006 and to $2.5 trillion in 2007. The big dropoff in 2003-2004 was caused not by interest rate changes but by the dropping off of refinancing. Even as interest rates were rising from 2003 until the end of 2007, the total size of the mortgage origination market remained large by historic standards. The biggest change in the composition of these mortgages after 2003 wasMortgage Deliquency Rates and OFHEO

Why were price increases so high in these states, and why when they fell did households stop paying their mortgages and enter into foreclosure? The answers to these questions can be understood by returning to the shift to nonconventional mortgages (Mayer et al., 2009). Banks were looking to find customers for nonconventional mortgages after 2003. By examining zip code data, they discovered that the four states mentioned above had had the highest rates of home appreciation. They decided to focus their attention on those states by sending out salespeople to get potential customers interested in buying a house. They sold to people who had less good credit and not enough of a down payment the idea that the housing market was the source of wealth. They did so by pointing out how their local area had seen the most appreciation. They encouraged people to join in with their neighbors to buy into the housing market.

Many of these new mortgagors were sold nonconventional mortgages, particularly mortgages with adjustable rates or interest-only loans, or else given mortgages where they put down very little money (as low as 3 percent and in some cases 0 percent).

If they had adjustable-rate mortgages, when the teaser rate adjusted, mortgagors could face a steep rise in their monthly payments. In the case of interest-only loans, mortgagors could quickly find themselves owing more than the mortgage they had bought as unpaid principal and interest were added to the loan amount. If mortgagors did not have much equity in their homes, then when house prices started to fall in their zip codes, their houses were suddenly worth less than they paid. When prices were rising, mortgagors who could not afford their payments would turn around and sell the house. But as prices dropped, this was not an option. If the house payment adjusted quite a bit higher, it made a lot of sense for mortgagors to just walk away from their homes. Once house prices started to drop and houses were abandoned, prices for existing homes would continue to spiral down. Such negative price spirals meant that more and more people walked away from their mortgages. In the end, prices dropped as much as 50 percent in some areas.The massive growth of nonconventional mortgage securitization had spread at least $3.8 trillion of assets directly linked to these mortgages to financial institutions around the world by the beginning of 2007 (Fligstein and Habinek, 2014). Nonetheless, it is clear that the markets, the credit rating agencies, the regulators, and most of the large banks all registered comparatively little response when housing prices started to stall out and mortgage default rates began to rise in late 2006. As already has been documented, several large banks such as Merrill Lynch and Citibank continued expanding their nonprime businesses aggressively during the first two quarters of 2007. In March 2007, Federal Reserve chairman Ben Bernanke stated in congressional testimony that “at this juncture, the impact on the broader economy and financial markets of the problems in the subprime market seems likely to be contained” (New York Times, 2007a).

The credit rating agencies also continued to maintain an implausibly upbeat outlook through the first two quarters of 2007. Only after they faced widespread mocking on the financial blogosphere, congressional questioning, and an overall crisis of legitimacy did the agencies take serious steps to adjust MBS bond ratings to reflect the deteriorating conditions in the mortgage market. Their reasons for reticence were clear. First, they had a vested interest in hoping the situation would improve, since their reputations and a significant portion of their revenues rested on a strong MBS market. Second, they knew what downgrades would mean. Moody's CEO Raymond McDaniel justified its cautious approach to downgrades, noting that “because we are an influential voice, we can create a self-fulfilling prophecy by saying that there are risks in the market ahead of those risks being revealed” (New York Times, 2007c).

By July 2007, the credit supply for nonconventional mortgages ground to a halt as the secondary market demand plummeted and banks became wary of the quickly weakening housing market. The volume of subprime originations declined by 90 percent between the first and second half of 2007 (Fligstein and Goldstein, 2010). The drying up of credit to fund nonconventional originations began hampering attempts by borrowers with adjustable-rate mortgages—even those whose houses had not yet declined in value—to refinance before their mortgage got reset to a higher rate. It also imperiled the business of large mortgage specialists such as Ameriquest and Countrywide and began eating into the revenue streams of the commercial and investment banks, which had come to rely on fee revenues from their vertically integrated mortgage finance franchises.

Bond defaults were initially concentrated among the lower-rated equity tranches that were the first in line to lose in the event of revenue losses. But the rising tide of subprime delinquencies and foreclosures soon put pressure on the supposedly safe “AAA” tranches as well.

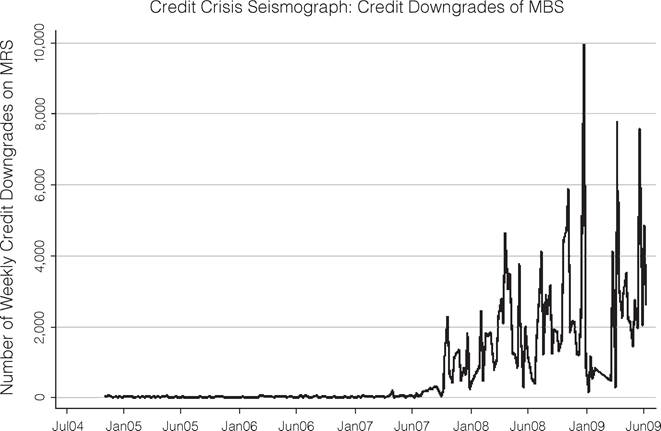

Figure 6.2 shows weekly counts of negative credit actions taken by one of the big three rating agencies against nonagency MBSs and mortgage-related CDOs. Aside from a few small blips of activity in April and July 2007, there were few downgrades on MBSs until they increased rapidly in September. Credit downgrades throughout 2008 averaged about three hundred a week. In September and October 2008, with the collapse of Lehman Brothers, credit downgrades spiked to nearly one thousand.The downgrade plot's resemblance to a seismograph image is apt. Each round of mass downgrades sent tremors through the financial system. The significance of credit downgrades was that they forced leveraged banks that had taken loans to buy MBSs to either pay off those loans or post additional collateral with their

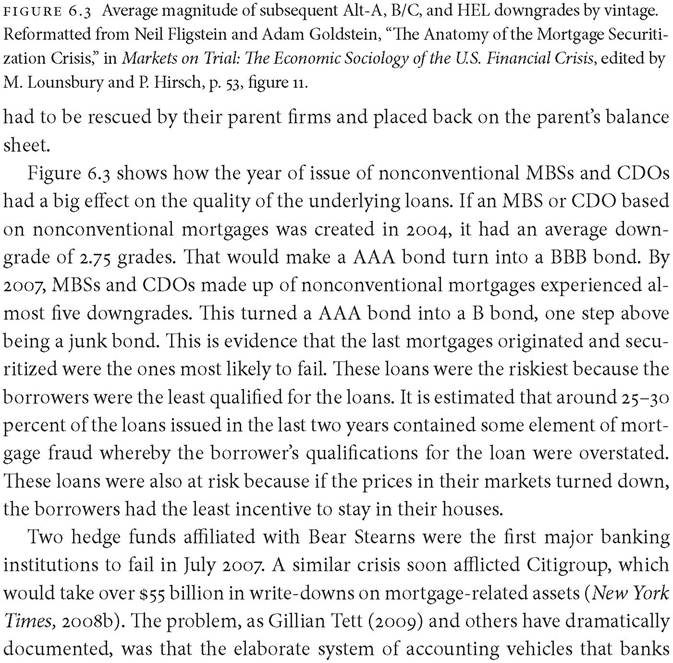

Table 6.1 : What happened to the main players in the market

| Lehman Brothers | Bankrupt (2008) |

| Bear Stearns | Bankrupt (2008) |

| Indy Mac | Bankrupt (2008) |

| Merrill Lynch | Sold to Bank of America (2008) |

| Salomon Brothers | Sold to Citibank |

| Government bailout | |

| Bank of America | Government bailout |

| Countrywide | Sold to Bank of America (2007) |

| Citibank | Government bailout (2008) |

| Wachovia | Sold to Wells Fargo (2008) |

| Morgan Stanley | Reorganized as commercial bank (2008) |

| Goldman Sachs | Reorganized as commercial bank (2008) |

| New Century Financial | Bankrupt (2008) |

| Washington Mutual | Sold to JPMorgan Chase (2008) |

| Fannie Mae | Government takeover (2008) |

| Freddie Mac | Government takeover (2008) |

built to hide their leverage from regulators and the elaborate network of credit default swaps they created to hedge their risks made it impossible for the market to discern which banks were exposed to the worst of the nonconventional mortgage securities, what came to be called “toxic assets.” The financial crisis escalated throughout the summer of 2008 in spite of efforts by the Federal Reserve to make emergency capital available.

Table 6.1 looks at what happened to the top banks that were leaders in the mortgage securitization business circa 2005 by 2010. Seven of the ten largest subprime lenders in 2005 were either out of business or absorbed by merger. Eight of the ten top subprime-MBS-issuing firms in 2005 were either out of business or merged into other entities. The collapse of the subprime market essentially wiped out all of the firms that had grown large on that business. Fannie and Freddie were taken over by the government. The big investment banks at the core of the subprime MBS market no longer existed, except Morgan Stanley and Goldman Sachs. Citibank, Bank of America, JPMorgan Chase, and Wells Fargo emerged as large conglomerate banks, having absorbed many of the subprime losers, while both Goldman Sachs and Morgan Stanley reorganized themselves to become commercial banks in order to avail themselves of cheap loans from the Federal Reserve. Most of the institutions that survived only did so on account of the Troubled Asset Relief Program (TARP) bailout, and most took massive write-downs on MBS assets.