AN ARTFUL DEAL

On October 25, 1999, Trump Hotels & Casino Resorts reported a year- over-year rise in its third-quarter earnings per share, from $0.24 to $0.63, excluding a one-time charge related to the closing of the Trump World’s Fair Casino Hotel.

The net exceeded analysts’ consensus forecast of $0.54 a share,2 resulting in a jump in the Trump’s share price from $4 to $45/16. Also up on the day were the bonds of one of the company’s casinos, Trump Atlantic City, which climbed about one point to 84¼.“Our focus in 1999 was threefold,” said president and chief executive officer Nicholas Ribis, in explaining the profit surge, which surprised industry analysts. “First, to increase our operating margins at each operating entity; second, to decrease our marketing costs; and third, to increase our cash sales from our non-casino operations. We have succeeded in achieving positive results in each of these three categories.”3

The company’s self-congratulatory press release contained no mention of another important contributor to the third-quarter surge in revenues, and by extension, net income. As the subsequently filed Quarterly Report on Form 10-Q finally acknowledged, $17.2 million of the period’s revenue arose from bankrupt restaurant operator Planet Hollywood’s abandonment of its lease on the All Star Cafe at Trump’s Taj Mahal casino. With the termination of the lease, all improvements and alterations, along with certain other assets, became the property of Trump, which took over the restaurant’s operation. An independent appraisal valued the assets received by Trump at $17.2 million. Without that boost, the company’s revenues would have declined, year over year, and net income would have undershot, rather than exceeded, analysts’ expectations.

The discrepancy between the October 25 disclosure and the fuller accounting in the 10-Q “became an embarrassment” to Trump Hotels & Casino Resorts, according to the Wall Street Journal.4 Moreover, the timing was unfortunate.

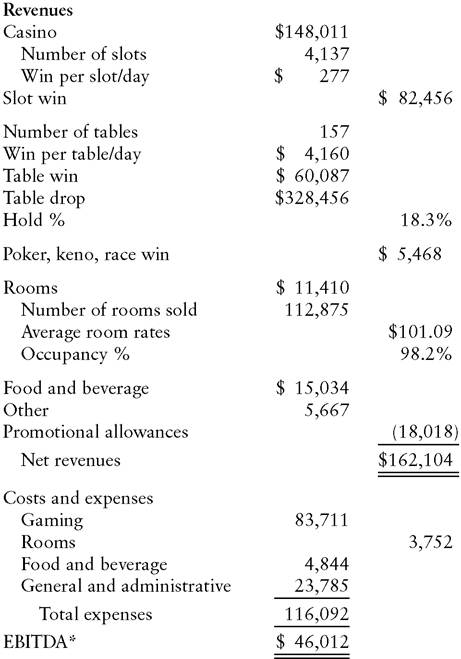

The incident occurred as management was making a round of investor presentations aimed at generating support for its plans to develop a new resort on the Atlantic City, New Jersey, site of the shuttered World’s Fair casino.Worse yet, from the company’s standpoint, the fact that Trump had omitted some rather useful information was detectable. Bear, Stearns & Co. bond analyst Tom Shandell noticed that the company’s press release reported mysteriously large revenues for the Trump Taj Mahal. The unit’s revenues increased by $4.9 million over the comparable 1998 quarter, even though the New Jersey Casino Control Commission reported a $12.1 million decline in the Taj Mahal’s casino revenues. Shandell was correct in suspecting that some other large, unspecified item was buried in the numbers; the difference between the purported $4.9 million increase and the Commission’s reported decline of $12.1 million was essentially identical to the $17.2 million of All Star Cafe assets that later came to light. No such inference or backing-out of numbers would have been required if Trump’s third-quarter 1999 press release had provided as much detail on the Taj Mahal’s operations as the corresponding 1998 release. That was not the case, however, as Exhibit 9.1 demonstrates.

Was the drastic cutback in disclosure in Trump’s third-quarter 1999 earnings release part of a deliberate attempt to conceal the fact that the year- over-year revenue gain was solely attributable to a nonrecurring event? Not to hear the company’s president tell it. “It was never hidden,” Ribis insisted.

EXHIBIT 9.1 Disclosure of Trump Taj Mahal Results in Trump Hotels and Casino Resorts Earnings Release Three Months Ended September 30, 1998 ($000 omitted)

[1]EBITDA reflects earnings before depreciation, interest, taxes, Casino Reinvestment Development Authority writedown, and nonoperating income.

Three Months Ended September 30, 1999

($000 omitted)

Revenues $167.7

Operating profit 41.4

EBITDA 51.0

Margin 30.4%

Sources: Trump Hotels and Casino Resorts Press Releases dated October 7, 1998 and October 25, 1999.

“When there was a specific question about it, we broke it out.”5 The gain on the All Star Cafe simply got lost in the shuffle, he maintained, when the lawyers pressed him to put out third-quarter earnings before commencing the roadshow for the proposed new casino.

“As soon as I learned of the accounting treatment we spoke with all of our investors and analysts,” added Ribis.6By apparently claiming that he discovered the true source of his company’s year-over-year earnings increase only after the quarterly results had been released, Ribis did not burnish his reputation as a details man. That professed shortcoming may not explain why, seven months later, Trump Hotels & Casino Resorts decided not to renew Ribis’s expiring contract as CEO. Perhaps it had more to do with the 56% drop in Trump’s stock price in the 12 months ending May 2000. One thing is certain, however. Investors who relied solely on the company’s disclosure were burned if they bought into the rally that followed the bullish-sounding press release. After analyst Shandell’s inquiries uncovered the All Star Cafe’s contribution to third- quarter results, the stock promptly sagged from $45/i6 to $378, while the Trump Atlantic City bonds slid from 84¼ to 80. On January 16, 2002, Trump Hotels and Casinos agreed to settle SEC charges that it “recklessly” misled investors in this incident, without admitting or denying the commission’s findings.7