Chapter 67 Determinants of Behavioral Intention to Mobile Banking in Arab Culture

Abdullah Rashed

University of Minho, Portugal

Henrique Santos

University of Minho, Portugal

ABSTRACT

Nowadays, new tools and technologies are emerging rapidly. They are often used cross-culturally before being tested for suitability and validity.

However, they would be validated to ensure that they work with all users, not just part of them. Mobile banking (as a new technology tool) has been introduced assuming that it performs well concerning authentication among all members of the society.We aim to validate mobile banking intention to use, through Technology Acceptance Model (TAM), focused on security, in Arabic countries, namely Yemen. The results confirm the previous studies that have shown the importance of perceived ease of use and perceived usefulness.

INTRODUCTION

Rapid and continuously growth of wireless and mobile technologies made it possible to banking service customers’ to access use those services at any place at any time. For that reason most banks provide mobile access to their customers (Selvan, 2011).

Internet and its related technologies have been growing exponentially (Cho, 2007). Technologies make our lives easy but not so secure

DOI: 10.4018∕978-1-4666-6268-1.ch067

(Sukhai, 1998), especially for financial applications (Rashed, 2013). Service industry has been changed the way business is conducted (Selvan, 2011). Most organizations already provide services via the Internet and mobile appliances (Segev, 1998). Furthermore, during the last ten years, the improvement of mobile communication technologies has changed the banking industry, so users are able to conduct banking services anyplace anytime (Gu, 2009). Mobile Banking provides customers many services such as: requesting the balance and the latest transactions; transferring funds between accounts; buying and selling orders, for the stock exchange; and receiving portfolio and price information (Barati, 2009).

Concerning authentication, for individuals it is known to be difficult to remember their user names and PINs. For that reason, many users select easy to remember passwords (Coventry, 2003), which is considered a security trade-off. Security specialists are looking for more advanced techniques that would improve authentication performance (Rashed, 2010c)..

Limited understanding of customer requirements, as well as lack of technology infrastructure, is considered a barrier towards innovation (Wu, 2005). In spite of the efforts of key players such as banks, mobile network operators and mobile service providers, it still lacks to study and promote customer acceptance (Eze, 2008).

Insufficient user acceptance has been an obstacle to the successful adoption of new information systems and information technologies (Wu, 2005). It is important to understand user acceptance in order to identify the factors that affect user intention to use mobile banking. This would help developers in producing more acceptable systems or help them to discover why users avoid using mobile banking (Selvan, 2011). Numerous empirical tests and studies have shown that TAM is robust to be used in variety of IT-related studies (Rashed, 2010b).

Mobile banking is still in a development phase in most countries especially middle- east, where small markets with few users have been reported. Among other reasons there are lack of customer acceptance and poor time response services (Barati, 2009). Besides, mobile payments are mainly used with popular mobile services since there are few alternative payment solutions available (Mallat, 2004). In spite of being the latest and most innovative service offered by banks, it is not studied well regarding how customers perceive it (Safeena, 2011).

Sufficient user acceptance is a main obstacle to the successful adoption of new technologies (Cho, 2007). Key players in mobile commerce must understand how to make customers satisfied to ensure market growth (Cho, 2007).

Concerning the payment models, mobile payment is not widely accepted (Eze, 2008).

Mobile banking Transactions volume in India is very low (Selvan, 2011). However, it is expected that mobile commerce will gain greater importance in the near future (Cho, 2007).

Concerning authentication methods there are three types (Coventry, 2003):

1. Something you know: A PIN; used almost by everyone.

2. Something you have: A passport, key, ATM (Automated Teller Machine) card or cell-phone (Herzberg, 2009).

3. Biometrics (something you are):

Fingerprints, signature, ear shape, keystroke, voice, finger geometry, iris, retina, DNA, hand geometry (Prashanth, 2009) and odour (Rashed, 2010a).

In this chapter we investigate the user acceptance of different authentication technologies within mobile appliances, in Arabic countries.

MOBILE BANKING

The increasing importance of mobile payment accelerates e-commerce (Mallat, 2004). Many companies in the financial sector have implemented mobile services (Safeena, 2011). As an example of a successful story, Helsinki City Transport implemented mobile subway and metro ticket. Customers buy a ticket using mobile payment. Approximately 55% of the metro tickets and nearly 10% of all individual tickets for Helsinki public transportation are currently purchased via mobile phones. This successful story shows that mobile ticket users are comfortable with the new service, which has also presented a new solution for traveling without a ticket (Mallat, 2004). In Malaysia (2006), 17.6% of mobile phone users purchase services and products using mobile phones (Eze, 2008). But a large number of projects (e.g., eCash, ePurse) have failed because of the awareness campaign focused on technical aspects which were less relevant for most users (Eze, 2008). Nokia and Master card have carried out several joint tests since 2003 (Eze, 2008).

Advantages of mobile banking are stated as follows (S afeena, 2011; Cho, 2007; Selvan, 2011):

• It is a self-service delivery channel that provides bank service in convenience way.

• Many applications are possible due to the availability of wireless and secure approach.

• It enables customers to transfer money, check balance and make bill payment.

• Mobile banking increases both efficiency and reduces transaction costs.

• Broad reach at any time and portability.

• Mobile technologies provide capabilities that continuously expand.

• Mobile commerce satisfies user requirements for time response.

• Mobile banking inherits some characteristics from digital world such as flexibility in time and place.

Disadvantages of mobile banking are stated as follows (Cho, 2007):

It is difficult to conduct banking operations with small mobile devices.

Depending on culture and experience, users don not trust mobile devices.

Business strategies and values are not fully understood.

Limited and insufficient information about transactions and constraints of mobile terminals.

RELATED WORK

Khanfar et al. (2005) conducted a survey about customer satisfaction with internet banking web site for a bank. The covered factors were: customer support, security, ease of use, digital products/ services, transaction and payment, information content, and innovation. They found that all factors have a positive impact on the customer satisfaction. Moreover, they found that there was no relation between demographic data and customer satisfaction due to the high computer literacy among customers (Khanfar et al., 2005).

AlZomai (2008) discussed the authentication problems in online banking using SMS for transactions. Their experiment aimed to simulate the online bank using website to do the transactions. They suggest enhancing online banking security by focusing on usability more than security technics and mechanisms. They suggested SMS authorization scheme. They attacked their approach to make sure that it would work properly (AlZomai, 2008).

Gu et. al. (2009) examined and validated the determinants of users’ intention to use mobile banking.

They used a structural equation modeling (SEM) to test the causalities in the proposed model. They verified the effect of perceived usefulness, trust and perceived ease-of-use. The results indicated strong support for the validity of proposed model with 72.2% of the variance in behavioral intention to use mobile banking. The study also found that self-efficiency was the strongest pillar of perceived ease-of-use, which directly and indirectly affected behavioral intention through perceived usefulness in mobile banking. In addition, they found that structural assurances* were the strongest pillar of trust, which could increase behavioral intention to use mobile banking (Gu et al., 2009).Hua and Prashant (2009) investigated the factors affecting mobile commerce adoption in China and the United States. They conducted a survey on 190 individual mobile commerce users. Results showed that there are several significant cultural differences impacting on consumer intention to use mobile commerce (Hua & Prashant, 2009).

Yaseen and Zayed (2010) used the TAM model to study the m-commerce technology deployment in Jordan. They distributed 210 questionnaires among mobile commerce users in Stock Exchange for Brokers and Investors. They test trust, perceived usefulness, perceived ease of use, social and cultural values and economic issues, as fundamental influence factors of a decision maker to adopt this type of technology. Their results showed that all factors had significant association with intention to use mobile commerce technology while economic issues are not significant (Yaseen & Zayed, 2010).

Maiyaki and Mokhtar (2010) studied determinants of consumer behavioral intention in Nigerian commercial banks. They investigated the influence of perceived service quality, perceived value, corporate image and switching cost on the consumer behavioral intention in the context of commercial banks in Nigeria. They found that the quality of service, customer perceived value and image of the corporate had significant influence on customer behavioral intention (Maiyaki & Mokhtar, 2010).

Barati and Mohammadi (2009) studied the factors that affect acceptance of mobile banking. They presented a set of factors that could positively affect the success of mobile banking and should be taken into account by banks while adopting mobile technology. They found that perceived usefulness and perceived ease of use are significant. Moreover they found that facilitating conditions in acceptance of mobile services have a very important role (Barati & Mohammadi, 2009).

Ramayah et al. (2010) studied and examined the intention to use an online bill payment among part time MBA students in University Sciences of Malaysia, Penang. They developed and modified the extended TAM and Social Cognitive Theory to identify factors that would determine and influence the intention to use an online bill payment system. They conducted a survey that involved 120 students. They found that perceived ease of use and perceived usefulness are the significant drivers of intention to use the online bill payment system. In addition, they found that subjective norm, image, result demonstrability and perceived ease of use were the key determinants of perceived usefulness, whereas perceived risk was found to be negatively related to usefulness. Moreover, computer self-efficacy played a significant role in influencing the perceived ease of use of the online bill payment system (Ramayah et al., 2010).

Eze et al. (2008) studied the security factors that affect the user acceptance of mobile payment in Malaysia. Their conceptual design examined the impact of security dimensions on trust and their influence on user intention to use mobile payment systems. Their results highlight the importance of perceived security of mobile payments on consumer intention to use mobile payment. They recommended creating massive awareness campaigns to inform potential consumers about the safety of transactions. Besides, they expected that internet security protocols like SET (Secure Electronic Transaction) should be exploited to build more secure mobile payment systems. Their security worries can be overcome by awareness campaigns (Eze et al., 2008).

Cho et al. (2007) studied the limiting factors of new technologies in order to understand and manage e-commerce activities. They focused on the trust and other factors. Using TAM, their results showed that mobile commerce should be differentiated from e-commerce. They found that it is important for users to perceive security of mobile payment. They recommended awareness campaigns by key players, to show that all security mechanisms are robust. Moreover, they recommended using subjective measures for assessing the effectiveness of security mechanisms, to enforce trust and convenience when developing and advertising the mobile payment schemes (Cho et al., 2007).

Safeena et al. (2011) studied five factors: ease of use, perceive usefulness, subjective norms, perceive associated risks and customer awareness.

They found that all factors have strong positive effect on customer decision.

Most of these studies show the importance of security and, simultaneously, the ease of use perception. However, when we try to enforce security most of the time we end up with a less flexible and more annoying system, which is difficult to accept by users. Authentication mechanism is determinant for security and so it is pertinent to find out how much authentication enforcement users are ready to accept.

METHODOLOGY

We developed a survey questionnaire and distributed it via web. The survey questions use a five- point Likert-type scale as follows: 1: extremely dislike, 2: slightly unlikely, 3: neither, 4: slightly likely and 5: extremely likely. The survey questions include participant profile: gender, age, nationality, job, major and education.

The research hypotheses are:

H1: Customers’ intention to use mobile banking is positively influenced by certain perceptual factors, in Yemen such as:

Ha: Perceived usefulness of mobile banking application

Hb: Perceived ease of use of mobile banking application

H2: Customers’ intention to use mobile banking is positively influenced by certain personal factors such as:

Ha: Prior experience with mobile banking Hb: Prior experience with ATM Hc: Customer’s educational level

H3: Demographic factor (such as gender, age...) will have a positive effect on the intention to use mobile banking.

H4: Perceived usefulness is influenced by certain perceptual factors such as:

◦ Perceived performance

◦ Perceived saving time and effort

Perceived increase in the productivity

Social and cultural factors

Perceived performance is the degree to which users expect the target system would support the performance perceive. Saving time and effort is defined as the degree to which the users expect that the target system would save the time and effort when comparing with the old method. Social and cultural factors affect the decision to use the target system (Al-Eryani et al., 2010). We directly asked the respondents about the mentioned factors to measure their impact on behavioral intention.

DISCUSSION

We aim to measure the general trend towards mobile banking. We use descriptive statistics to describe the basic features of the data in this study. We use both descriptive statistics and simple graphics as the basis of virtually every quantitative data analysis. Due to the sample size, it should be noted that it is difficult to generalize the results.

Overview

Our sample, including a total of 100 individuals, consisted of 76% males and 24% females. The majority of the respondents were young people, 54% of them were within the interval [15-30]; 6% were less than 21; and 33% were within the interval [31-40] (Table 1). 47% of the respondents have a post graduate degree, 41% have a bachelor degree and most of them (54%) are proficient IT users. 89% of the respondents use ATMs and 98% prefer to use it rather than interacting with a human being clerk. 74% of the respondents consider mobile bank easy to use, 10% consider it difficult and 16% have no opinion.

87% of the respondents pointed mobile banking as a brilliant idea whereas 8% were neutral about this concept. 5% of the respondents considered it as a stupid idea. 45% intended to use mobile

Table 1. Sample profile

| Variable | Frequency | |

| Gender | Male | 76 |

| Female | 24 | |

| Race | Yemenis | 79 |

| Arab | 21 | |

| Age | 15-20 | 6 |

| 21-30 | 48 | |

| 31-40 | 33 | |

| More than 41 | 13 | |

| Specializations | IT | 54 |

| Finance | 5 | |

| Administration | 10 | |

| Medicine | 7 | |

| Engineering | 13 | |

| Others | 11 | |

| Jobs type | Public Sector | 23 |

| UN and international organizations | 5 | |

| Private Organization | 41 | |

| Family business | 3 | |

| Other | 28 |

banking whereas 46% were indecisive about using it. 9% of the respondents clearly stated that they would not use it.

Customers' Intention to Use Mobile Banking Due to the Impact of Perceptual Factors

83% of the respondents perceived mobile banking as useful, while 15% were indecisive about it. Only 2% of the respondents did not perceive it as useful. Besides, 90% of the respondents think that using mobile banking will improve their live performance. 89% considered the idea would save them time.

Customers' Intention to Use Mobile Banking Due to the Impact of Personal Factors

Experience variable measures the users’ familiarity with mobile banking. We found that experience was a significant factor since most of the respondents who used mobile banking before, reported that they found it easy and acceptable. 23% of the respondents have used mobile banking before. However, 77% have not tried mobile banking yet.

Customers' Intention to Use Mobile Banking Due to the Impact of Demographic Factors

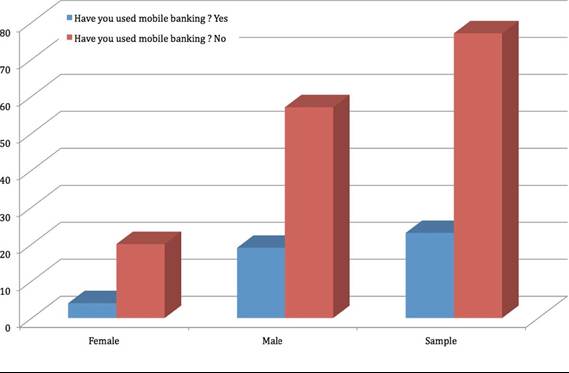

Figure 1 shows that 83% of females have not used mobile banking before whereas 75% of male respondents had prior experience with mobile banking.

When the findings were analyzed due to the professions of the respondents, it was found out that “administration” category scored the highest in perceived ease of use, usefulness and intention to use (Table 2).

Age correlates with the intention to use, indicating that older participants are less willing to use the mobile banking than the younger ones. Furthermore, mobile banking was accepted more by master degree holders than Ph.D. and undergraduates.

The Impact of Performance, Time, Effort, and Productivity on the Customers' Intention to Use Mobile Banking

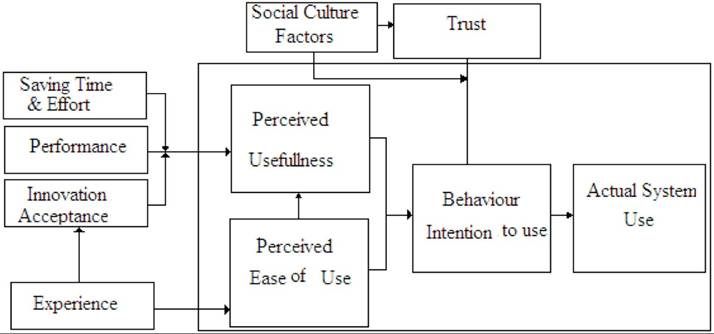

This study proposes a revised version of the Technological Acceptance Model (TAM).Six key variables have been included in the model proposed. These variables are saving time and effort, performance, experience, trust, innovation acceptance and social - cultural factors.

Figure 1. Prior mobile banking experience

Table 2. Effect of major factor

| Administration | Finance | IT | Engineering | Medicine | |

| The Idea of Using Mobile Banking | 100% | 100% | 89% | 92% | 86% |

| Ease-of-Use Mobile Banking | 70% | 60% | 78% | 77% | 57% |

| Performance of Mobile Banking | 100% | 80% | 89% | 92% | 86% |

| Intention to Use Mobile Banking | 60% | 60% | 44% | 54% | 57% |

| Like/Dislike the Idea of Using Mobile Banking | 90% | 60% | 72% | 85% | 86% |

| Using Mobile Banking Would Save Time and Effort | 90% | 80% | 87% | 100% | 86% |

| Using Mobile Banking Would Increase the Productivity | 100% | 100% | 83% | 92% | 57% |

Figure 2 shows the proposed model for mobile banking acceptance. The experience of using mobile platforms would affect the responses and similar technologies would help users to perceive both ease of use and usefulness.

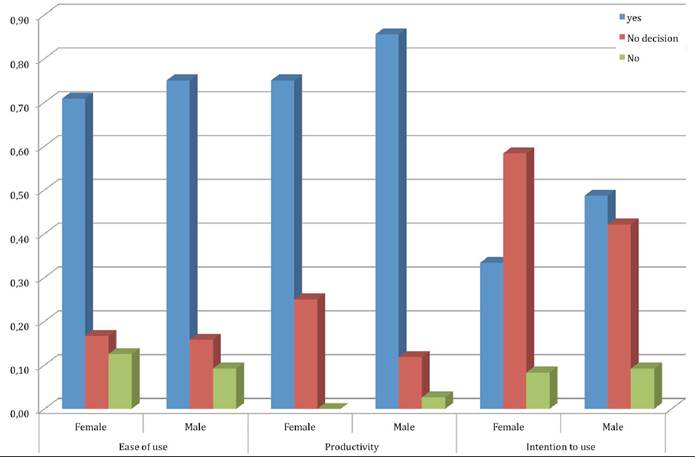

The literature review concerning demographic characteristic like age, gender and experience of mobile use emphasize the impact on technology adoption. However, our findings support the notion that age has no effect on intention to use mobile in financial transactions. Furthermore, we found that gender has significant effect as males have strong intention to use the new technologies more than females (Figure 3). Experience factor is significant. Social and cultural factors are important in acceptance of mobile banking. In this context, it is probable that mobile services might face resistance of consumers. 83% of the respondents who found mobile banking very easy have experienced ATMs before. Moreover, 97 % of the respondents who found mobile banking very easy preferred using an ATM instead of dealing with human clerk at the bank.

This study aims to validate mobile banking intention to use, through Technology Acceptance Model (TAM), focused on security, in Arabic countries, namely Yemen.

Our sample consisted of young educated individuals. Moreover, most of them were frequent users of ATMs and preferred to use new technologies rather than conventional banking methods.

Figure 2. Proposed framework

Figure 3. Gender and intention to use

Our results are mostly inline with the findings of the previous studies, but also present some contradictory findings in some cases as well. Our results reveal that both perceived ease-of-use and perceived usefulness are significant factors that impact the customers’ intention to use online banking.

Findings of this study support the notion that mobile banking is accepted mostly for reasons such as saving time and efforts as well as for improving the performance in the lives of the users. Most of participants find mobile banking easy-to-use whereas some still think that they need help in using these platforms. This finding can be interpreted as a strong factor to support deploying mobile bank. However, it should also be mentioned that the intention to use mobile banking is only 45% and 40% of the participants are still indecisive about mobile banking. It is evident that there is still a gap between the acceptance of a new platform and the actual use of it.

It should also be noted that the relative small size of the sample limits the generalization of the findings. However, it is believed that the study will provide contributions for further studies concerning the use of mobile banking in local cultures.

References

Abdullah, S., & Date, H. (2010). Customer Perspectives on E-business Value: Case Study on Internet Banking. Journal. Internet Bank. Com- mer., 15(1), 1-13.

Al-Eryani, A., & Rashed, A. (2012). The impact of the culture on the e-readiness for e-government in developing countries (Yemen). The 2012 International Arab Conference on Information Technology. Zarqa, Jordan.

AlZomai, M., AlFayyadh, B., Audun J0sang, A., & cCullagh, A.(2008). An Experimental Investigation of the Usability of Transaction Authorization in Online Bank Security Systems. Proceedings of the sixth Australasian conference on Information security - Volume 81 (pp:65-73). Wollongong, Australia.

Barati, S., & Mohammadi, S. (2009). An Efficient Model to Improve Customer Acceptance of Mobile Banking. Proceedings of the World Congress on Engineering and Computer Science 2009. San Francisco, CA.

Cho, D., Kwon, H., & Lee, H. (2007). Analysis of Trust in Internet and Mobile Commerce Adoption. Proceedings of the 40th Hawaii International Conference on System Sciences 2007. Hawaii.

Coventry, L., De Angeli, A., & Johnson, G. (2003). Usability and Biometric Verification at the ATM Interface. Proceedings of the SIGCHI conference on Human factors in computing systems (pp. 153 - 160). Ft. Lauderdale, FL.

Davis, F. (1989). Perceived Usefulness, Perceived Ease of Use and User Acceptance of Information Technologies. Management Information Systems Quarterly, 13(3), 319-240. doi:10.2307/249008

Eze, U., Gan, G., Ademu, J., & Tella, S. (2008). Modeling User Trust and Mobile Payment Adoption: Conceptual Framework. Communication of the IBIMA, 3, 224-230.

Gu, J., Lee, S., & Suh, Y. (2009). Determinants of Behavioral Intention to Mobile Banking. Expert Systems with Applications: An International Journal, 36(9), 11605-11616. doi:10.1016/j. eswa.2009.03.024

Herzberg, A. (2003). Payments and Banking with Mobile Personal Devices. Communications of the AC, 46(5), 53-58. doi:10.1145/769800.769801

Hua, D., & Prashant, P. (2009). Mobile Commerce Adoption in China and the United States: A Cross- Cultural Study. ACM SIGMIS Database, 40(4), 43-61. doi:10.1145/1644953.1644958

Khanfar, K., Rashed, A., Elzamly, A., & Elmasri, A. (2005). Customer Satisfaction with Internet Banking Web Site (Case study on the Arab Bank). the 4th International Multiconference on Computer Science and Information Technology. Amman, Jordan.

Maiyaki, A., & Mokhtar, S. (2010), Determinants of Consumer Behavioural Intention in Nigerian Commercial Banks, International Conference on Business and Economic Research (ICBER 2010), (15 - 16 March 2010) Malaysia.

Mallat, N., Rossi, M., & Tuunainen, V. (2004). Mobile Banking Services. Communications of the ACM, 47(5), 42-46. doi:10.1145/986213.986236

Prashanth, C., Ganavi, S., Mahalakshmi, T., Raja, K., Venugopal, K., & Patnaik, L. (2009). Iris Feature Extraction Using Directional Filter Bank, for Personal Identification. Proceedings of the 2nd Bangalore Annual Compute Conference on 2nd Bangalore Annual Compute, Article No. 6, India.

Ramayah, T., Chin, Y. L., Norazah, M., & Amlus,

I. (2005). Determinants of Intention to Use an Online Bill Payment System among MBA Students. E-Business, 9, 80-91.

Rashed, A., & Santos, H.(2010a). User Acceptance OTM Machine: In the Arab Culture. International Journal on Electronic Security and Digital Forensics, Inderscience.

Rashed, A., & Santos, H. (2010b). Validating TAM with Odour Interface in ATM Machines. Global Journal of Computer Science and Technology, 10(7), 2-6.

Rashed, A., & Santos, H. (2010c). OTM Machine Acceptance: In the Arab Culture. ICGS3 6th International Conference for on Global Security, Safety and Sustainability. Braga, Portugal.

Rashed, A., & Santos, H. (2010d). Multimodal Biometrics and Multilayered IDM for Secure Authentication. ICGS3 6th International Conference for on Global Security, Safety and Sustainability. Braga, Portugal.

Rashed, A., & Santos, H. (2013). Biometrics Acceptance in Arab Culture: An Exploratory Study. ICCAT'2013. Tunisia: Sousse.

Segev, A., Porra, J., & Roldan, M. (1998). Internet Security and the Case of Bank of America. Internet Security and the Case of Bank of America, 41(10), 81-87.

Selvan, N., Arasu, B., & Kirloskar, M. (2011). Behavioral Intention Towards Mobile Banking in India:The Case of State Bank of India (SBI). [IJESMA]. International Journal of E-Services and Mobile Applications, 3(4), 1-20. doi:10.4018/ jesma.2011100103

Sukhai, N. (1998). Access Control & Biometrics. Proceedings of the 1st Annual Conference on Information Security Curriculum Development (pp. 124 - 127). Kennesaw, Georgia.

Yaseen, S., & Zayed, S. (2010). Exploring Critical Determinants in Deploying Mobile Commerce Technology. American Journal of

Applied Sciences, 7(1), 120-126. doi:10.3844/ ajassp.2010.120-.126

KEY TERMS AND DEFINITIONS

Arabic Culture: It is the culture in the countries in which the official language is Arabic. It spread in countries located Western Asia and North Africa, from Morocco to the Persian Gulf.

Mobile Banking: It is a system that allows customers to conduct a number of financial transactions through a mobile device such as a mobile phone or personal digital assistant.

Technology Acceptance Model (TAM): TAM is used to predict the acceptability of a tool (e.g. information technology) in a specific environment and to identify the modifications which must be brought to the system in order to make it acceptable to users. It depends upon two pillars: perceived ease to use and perceived usefulness.

This work was previously published in Research and Design Innovations for Mobile User Experience, edited by Kerem Rizva- noglu and Gorkem Cetin, pages 139-149, copyright 2014 by Information Science Reference (an imprint of IGI Global).