Chapter 59 Impact of Microfinance Bank Credit Scheme

Benjamin Chijioke Asogwa

University of Agriculture, Nigeria

Peter Iorhon Ater

University of Agriculture, Nigeria

Sani Madi Yakubu

University of Agriculture, Nigeria

ABSTRACT

The purpose of this chapter is to examine impact of microfinance bank credit scheme on maize farmers in Gombe State, Nigeria, using data from 90 randomly sampled maize farmers in Gombe State.

The study showed that majority of the respondents (53.33%) accessed amount of credit ranging between 30,000 and less than 50,000 Naira. Majority of the farmers (85.56%) used their credit for the purpose of farm production. Majority of respondents (58.89%) recorded in increase in maize output as result of the intervention of the microfinance credit scheme. Majority of the respondents (86.67%) repaid credit collected. The microfinance credit scheme intervention significantly improved the output and income of the respondents. Ineffective organizational structure of the credit institutions constituted the major constraint in accessing microfinance credits. Microfinance credit facilities extended to the farmers should be improved upon in both quantity and quality. The organizational structure of microfinance institutions should be reorganized to reduce bottlenecks in accessing credits.INTRODUCTION

The goal of this article is to provide empirical evidence that will assist the reader develop a thorough understanding of the impact of microfinance bank credit scheme on maize farmers in Gombe State, Nigeria. To accomplish this objective an attempt has been made to present the subject in

DOI: 10.4018/978-1-4666-6268-1.ch059 a manner that will be useful to the finance houses and policy makers in the microfinance industry and other stakeholders in microcredit in particular and economic development in general.

The broad objective of this study is to examine the impact of Microfinance Bank Credit Scheme on maize farmers in Gombe State, Nigeria.

The specific objectives of the study are to:.

1. Analyse the socio-economic characteristics of the maize farmers in Gombe State, Nigeria.

2. Ascertain the volume of credit acquired from the bank by the respondents.

3. Assess the level of utilization of the credit accessed by the respondents.

4. Determine the impact of credit on the output and income of the maize farmers in the study area.

5. Identify constraints to accessing credit from the bank among the respondents.

The following null hypothesis were stated and tested:

1. There is no significant difference between the output of respondents (beneficiaries) before and after the utilization of micro-credit obtained from the Microfinance B ank Credit Scheme.

2. There is no significant difference between the income of respondents (beneficiaries) before and after the utilization of microcredit obtained from the Microfinance Bank Credit Scheme.

BACKGROUND

Agriculture is a key sector in the Nigerian economy. Its importance is particularly glaring in its contribution to Gross Domestic Product (GDP), provision of food, provision of gainful employment, provision of capital and capital formation, foreign exchange for development and increasing rural welfare (Nwaru, 2005). Agriculture has remained the largest nonoil export earner and has significantly contributed above 30 percent of Gross Domestic Product (GDP) in Nigeria (RMU, 2003).

Despite these contributions, agricultural growth and productivity has been slow compared to other sectors of the economy because of low utilization of modern inputs by farmers, unavailability and inaccessibility of farmlands, non-mechanization of farming operations and insufficient fund inflows into the agricultural sector. An examination of the Nigerian agricultural sector shows that it is not in a position to finance its own development. Nwagbo (1986) reports that emphasis on the financing problem is rightly founded on the belief that agriculture for various reasons is not in a strong competitive position in relation to other sectors to acquire or obtain investment and productive credit from the usual financial institutions.

Farm credits are however, important means for improving farm capital investment in Nigeria, without which there may be no progress in the agricultural sector to adequately fulfill its expected Millennium Development Goals (MDGs) (Musa et al., 2010). Akpokodje and Olomola (2000) contend that if credits were made available to small -scale farmers, the slow growth of the agricultural sector would develop more rapidly. Phillip, Ephraim, John, and Omobowale (2008) assert that credit supply to farmers is widely seen as an effective strategy for enhancing the increase in agricultural productivity.Therefore, in order to improve the national economy, producers who are the farmers should be supported to expand their scale of production through financial resources (Akpokodje and Olomola, 2000). Akpokodje and Olomola (2000) further explained that associated with mechanization and the acquisition of agricultural inputs is the issue of credit, without which the envisaged agricultural production and development will be a mirage. in addition, the farmers will still persist old one-man hoe and cutlass system with a farm size that can only guarantee subsistence production.

Credit allows the farmers to satisfy their cash needs induced by the production cycle which characterized agriculture. Despite the general acceptance of the important role of credit and a wide appreciation by most governments of the need for credit, credit schemes for agriculture unfortunately have failed at various times and places to yield the expected and significant results. Some of these schemes have ended up prematurely as a result of high rate of loan default and corrupt practices on the part of the beneficiaries and loan officials. Where the scheme had survived, they hardly made significant effect on the production of the loan beneficiaries. This may be as a result of the fact that the loans are not large enough to make visible impact or too large as to constitute a burden on the beneficiaries (Adelakun, 1998).

The traditional microfinance institution provides access to credit for the rural and urban low income earners which is culturally rooted and dated back to several centuries (CBN, 2005). Haruna (2007) was of the view that the cost of administering large number of very small loans without collateral is considered by commercial bank to be prohibitive. As a result, poor people are being denied access to formal credit, thus the underlying objective for employing micro credits as strategies to assist the economically active poor people who cannot make savings, accumulate assets or invest in any meaningful income generating activity (like agriculture) that would help to break the prevailing cycle of poverty.

The need for microfinance scheme was further stressed by Oluyombo (2010) as he opined that microfinance institutions and banks are fast becoming household name globally due to its acceptance as a means of reaching those that were not served by conventional big banks. it therefore means that the adoption of microfinance policy in Nigeria and other countries is part of the global financial integration in the provision oftailor-made financial services to those outside the catchments of the big banks either as a result of their income, location, literacy level or descrimination. This may be the reasons for a major increase in the number of microfinance banks in Nigreria with more coverage area (Olawuyi et al., 2010).

The continuous declining status of the maize farmers who face growing levels of reduced farming activities as a result of poverty, illiteracy and subsistence nature of farming among other social and economic challenges have become an issue of concern. The normal practice has been the provision of funds assigned to finance maize farming via numerous programs and institution that have not yielded any tangible impact on the farmers whom such funds hardly get to. Therefore the broad objective of this study is to examine the impact of Microfinance Bank Credit Scheme on maize farmers in Gombe State, Nigeria.

MAIN FOCUS OF THE CHAPTER

Review of Literature

Agricultural credit has been variously defined by authors. According to Nwaru (2004), agricultural credit is the present and temporary transfer of purchasing power from a person who owns it to a person who wants it, allowing the later the opportunity to command another person’s capital for agricultural purposes but with confidence in his willingness and ability to repay at a specified future date. It is the monetization of promises and exchanging of cash in the present for a promise to repay in future with or without interest. Without the willingness and ability to repay, the promise to repay at a future date would be futile. Credit is an instrument whose effectiveness depends on the economic and financial policies that go with it (Nwaru, 2004). If well applied, credit should increase the size of farm operations, increase farm income, introduce innovations in farming, encourage capital formation, improve marketing efficiency and enhance farmers’ consumption (Nwagbo, 1989; Nwaru, 2004). However, Udoh (2005) reported that the demand for credit tends to be a derived demand, which indicates the borrowers will demand for credit based on the need for it and the satisfaction to be derived.

The demand and supply of credit is influenced by several factors such as personal attributes of the individual, area specific attributes and credit source attributes (Udoh, 2005). These attributes influence individuals differently irrespective of their gender such that what might determine the demand for credit by a particular female farmer might be different from what determines credit demand by another farmer. For instance, in studying informal lenders and formal credit groups in Madagascar, Zeller (1994) indicated that informal lenders and group members obtain information about the wealth, indebtedness and income potential of loan applicants and hence ration loan demands an in-depth view of total household wealth and leverage of the household.

In line with this, Nwaru (2004) examined rural credit markets and resource use in arable crop production in Imo State, Nigeria, using multiple regression analysis by the two stage least squares. The result revealed that credit demand was significantly influenced by interest rate, educational level of farmer, amount borrowed previously, farm size and gross savings, while gross income of lender, total cost of lending, source of loan (whether formal or informal), worth of loan application and previous loan repayment significantly influenced credit supply.Agricultural credit is considered essential to the process of improving agriculture and the transformation of the rural economy. In their own contribution, Mahmood et al. (2009) posit that delivery of easy and cheap credit is the quickest way for boosting agricultural production. Ijere (1987), in emphasizing the important role credit plays, describes credit facilities for small- scale farmers as the catalyst that activates the engine of growth enabling it to mobilize the forces within it and to advance in the direction expected or planned for it. He maintained that the greater injection of credit, the more propensity of the economy to move in the given path. Conversely, he stated, if the agricultural sector receives less than its due share of the credit inputs, the very forces, which could have been activated, would automatically dry up and become very inactive. In other words, credit to small-scale farmers must not only be adequate but timely and specific.

To attain agricultural policy objective, programmes such as the National Accelerated Food Production Programme (NAFPP), the Agricultural Development Programmes (ADP), River Basin and Rural Development Authorities (RBDA), Operation Feed the Nation (OFN), the Green Revolution (GR), the National Agricultural Land Development Authority (NALDA), Agricultural Credit Guarantee Scheme Fund (ACGSF), etc were launched (ADP, 2005). Mention should also be made of Nigeria Agricultural and Cooperative Bank (NACB) now Nigerian Agricultural, Co-operative and Rural Development Bank (NA- CRDB). Yet agricultural policy objectives have not been achieved, as evidenced by the general food scarcity in Rivers State and in the whole country (Olawuyi et al., 2010).

Among the factors responsible for this lack of significant effect of credit schemes are insufficient loan amount, poor loan repayment and corrupt practices of loan beneficiaries and loan officials (Okorie, 1986; Balogun, 1986; Mejeha and Nnanna, 2010). Supporting this view, Nwaru (2005) and Omeh (2006) stated that Nigerian small-scale farmers are known to be economically weak with little or no capital investment. Consequently, they use low technology tools and methods in their production activities, which in turn lead to reduced output and productivity. In its own contribution, IFAD (2002) opined that causes of food insecurity and famine were not so much failures in food production, but structural problems relating to poverty and to the fact that the majority of the developing world’s poor population are concentrated in the rural areas.

Summing up all these views, Okerenta (2005) and Tasie (2008) identified insufficient extension or delivery of production credit to the poor farmers as the most critical factor responsible for the declining trend in agricultural production. It is therefore an irony of circumstance that the small-scale farmers who produce about 85% of food consumed in the country and the agricultural exports are perpetually handicapped by lack of production credit and bedeviled with poverty.

According to Nweze (1990), it was to obviate this sordid situation that successive Nigerian governments have attempted to bridge the credit gap in the agricultural sector through the establishment of various credit programmes. Those supply-led rural finance institutions include the Nigerian Agricultural, Cooperative and Rural Development Bank (NACRDB) and Community Banks.

Due to reforms by the Federal Government of Nigeria, the Central Bank of Nigeria (CBN) set up the Microfinance Banks to take over from Community Banks, with a mandate to making credit facilities available to small-scale enterprise operators including farmers. The policy framework establishing microfinance institutions in the country, saddles them with the responsibility of providing easy, cheap and affordable financial services to resource poor farmers, in a timely and competitive manner. This would enable them to undertake and develop long-term, sustainable entrepreneurial skill, mobilizing loans and creating employment opportunities and increase the productivity of these rural farmers, thereby increasing their farm income and output and uplifting their standard of living (Olawuyi et al., 2010).

The role of microfinance bank is the provision of financial services to the poor small and medium enterprises and maize farmers who are traditionally not served by the conventional financial institution in the urban and rural areas (MPRSF, 2007). Increase in production and establishment of new farm is achieved by making credit facilities and extension services available to small crop farmers, which leads to marketable surplus and increased income which enable small crop farmers to expand farming enterprises and become commercial farmers at the long run.

METHODOLOGY

The Study Area

Gombe State is located in the northeastern part of Nigeria. It is one of the country’s 36 states and its capital is Gombe. Gombe State shares common borders with Borno State, Yobe State, Taraba State, Adamawa State and Bauchi State. Gombe State has an area of 20,265 km2 and a population of around 2,353,000 people as of2006 (NPC, 2007). Gombe has two distinct climates, the dry season (November-March) and the rainy season (April-October). It has an average rainfall of 850mm. Gombe State has 11 Local Government Areas.

Agriculture is the main occupation of the people of Gombe State with more than 60% of the population engaged in agricultural occupation. Gombe State soil is reached for the cultivation of maize, cotton, groundnut, beans and other assorted grains.

Sampling Technique

The population for the study comprised the entire maize farmers who are beneficiaries of the microcredit scheme of Microfinance Banks in Gombe State, and must have utilised credit obtained in the last five years. A multistage sampling technique was used in selecting the respondents (maize farmers who are beneficiaries of the micro-credit scheme of Microfinance Bank in the area of study) for this study.

The first stage involves purposively selecting Gombe Local Government Area, which has the highest concentration of maize farmers who are beneficiaries of micro-credit scheme of Microfinance Banks in Gombe State. The second stage involves randomly selecting one (1) Microfinance Bank in Gombe Local Government Area of Gombe State. The third stage involves making use of the list (record) obtained from the selected Microfinance Bank to randomly select five (5) communities where the beneficiaries reside. The fourth stage involves making use of proportionate size technique to select the respondents (beneficiaries) as follows: Dawaki- 20, Bolari- 20, Shamaki- 20, Pantami- 15 and Kumbiya-Kumabiya- 15. Hence a total of 90 respondents (beneficiaries) were used for the study focusing specifically on the maize farmers.

Data Collection

The data for the study were collected mainly from primary sources. The primary data were collected using a structured questionnaire, copies of which were administered to the 90 beneficiaries selected for the study.

Method of Data Analysis

Data collected for this study were analyzed using descriptive statistics such as frequency distribution and percentages as well as inferential statistics such as t-test analysis. Specific objectives i, ii, iii and v were analyzed using frequency distribution and percentages while specific objective iv was analyzed using t-test analysis. The null hypotheses were analysed using t-test.

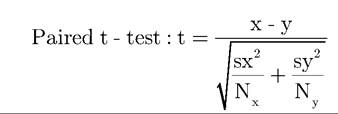

Test Statistic Specification

where t=t-statistic, x=mean of output (or income) after microfinance bank credit intervention, y = mean of output (or income) before microfinance bank credit intervention; sχ2= standard deviation of output (or income) after microfinance bank credit intervention; s = standard deviation of output (or income) before microfinance bank credit intervention; Nx = number of observation after microfinance bank credit intervention; Ny = number of observation before microfinance bank credit intervention.

RESULTS AND DISCUSSION

Socio-Economic Characteristics of Respondents

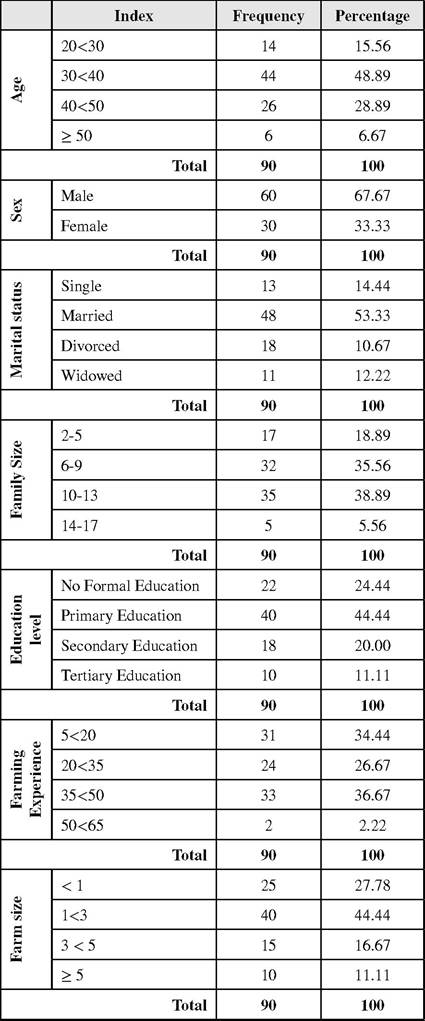

The socio-economic characteristics of the respondents include Age, Sex, Marital status, family size and Educational level, farming experience and farm size.

Age

The result in Table 1 shows that majority of the farmers (48.89%) are within the age bracket of 30 years and less than 40 years. This result suggests that majority of the maize farmers in the study area are young farmers who can make meaningful impact in agricultural production when adequately motivated with the needed credit facilities.

Sex

The result in Table 1 shows that majority (66.67%) of the respondents were males while 33.33% were females. Males own and control more farms than females. The reason could be that females are often married to the males and so might not out rightly own their lands. U sually they have a negligible portion compared to their male counterparts. Single females and widows owning and controlling their farms do not have the desired collaterals to satisfy the lending institutions to attract loans as only very few of them have the capacity to influence the institutions with the collaterals to get loans.

Marital Status

The result in Table 1 shows that majority of the respondents (53.33%) were married while 27.78% were unmarried.The high percentage of the married is as a result of the fact that farming communities believes in marriage, since farming occupation requires labour, their wives and families will assist in the farm work.

Family Size

The result in Table 1 shows that majority of the respondents (38.89%) had family size of 10-13. This result suggests that farmers in the studied area have large household sizes. The high household size of the majority of the respondents suggests that there is abundant supply of family labour in the studied area, which can be harnessed for increased farming activities.

Educational Level

The result in Table 1 shows that majority of the respondents (44.44%) had primary education, 21.5% had secondary whereas 15.4% had tertiary education. The implication of this result is that maize farmers in the studied area are literate enough to appreciate the important role credit faclities can play in helping to expand their farm enterprises.

Farm Experience

The result in Table 1 shows that majority of the farmers (36.67%) have been farming for between 35 years and less than 50 years. This result suggests that the farmers have long farming experience which can enhance efficient use of scare resources.

Table 1. Percentage distribution of respondents by socio-economic characteristics

Source: Field Survey, 2012

Farm Size

A large proportion of the farmers (44.44%) had farm size between 1 and less than 3 hectares (Table 1). This suggests that most of the respondents are small to medium scale farmers who should be adequately motivated with the necessary credit facilities in order to expand their agricultural productions.

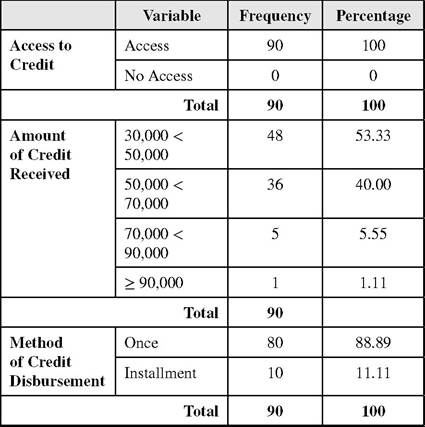

Access to Microfinance Banks Credit

Access to Microfinance

Banks Credit Facility

Table 2 shows that all the respondents (100%) interviewed had access to microfinance banks credit facility, suggesting that maize farmers in the study area benefitted in one way or the other from the Micro Finance Bank Credit Scheme.

Amount of Credit Accessed

The result in Table 2 shows that majority of the respondents (53.33%) accessed amount of credit ranging between 30,000 and less than50,000 Naira while 40% of the respondents accessed between 50,000 and less than 70,000 Naira of credit. This suggests that the credit extended to maize farmers in the study area is mostly small credit facility.

Method of Credit Disbursement

Table 2 shows that majority of the credits accessed by the farmers (88.89%) were disbursed to them at once, suggesting that the farmers were given the credit facility in one disbursement. The implication is the farmers would be able to have the money in bulk and hence an effective investment of the credit in their farm productions.

Credit Utilization

Utilization of Agricultural Credit

The result in Table 3 shows that majority of the farmers (85.56%) used their credit for the purpose of farm production. This implies that majority of the respondents in most cases appropriately utilized acquired credit for the purpose of Agricultural production.

Changes in Farming Activities due to Intervention from Microfinance Banks Credit Scheme

The result in Table 3 shows that majority of respondents (58.89%) recorded in increase in maize output as result of the Microfinance Banks Credit Scheme intervention. This implies that the intervention of the Microfinance B anks Credit Scheme has improved maize production in the study area.

Table 2. Percentage distribution of respondents by access to microfinance banks credit facility

Source: Field Survey, 2012

Repayment of Credit

Table 3 shows that majority of the respondents (86.67%) repaid credit collected while a few (13.33%) did not repay credit accessed. This suggests the ability to repay credit collected is high among the respondents while recording only a few cases of outright default.

Promptness of Repayment of Credit

The result in Table 3 shows that majority of respondents (60%) did not repay credit collected as at when due while 40% of respondents repaid credit collected in due time. This result implies

Table 3. Percentage distribution of respondents by credit utilization

| Variable | Frequency | Percentage | |

| Credit Utilization | Farm Production | 77 | 85.56 |

| Domestic/ Social Purpose | 7 | 7.78 | |

| Combination | 6 | 6.67 | |

| Total | 90 | 100 | |

| Change in Farming Activities | Increase in maize output | 53 | 58.89 |

| Increase in Farm Size | 6 | 6.67 | |

| Establishment of New Farm | 9 | 10.00 | |

| Use of Improved Farm Input | 16 | 17.78 | |

| Processing of Farm Output | 6 | 6.67 | |

| Total | 90 | 100 | |

| Repayment of Credit | Repaid | 78 | 86.67 |

| Not Repaid | 12 | 13.33 | |

| Total | 90 | 100 | |

| Promptness of Repayment of Credit | In time | 36 | 40.00 |

| Not in time | 54 | 60.00 | |

| Total | 90 | 100 | |

Source: Field Survey, 2012

that credit repayment made by respondents in most cases lagged behind the scheduled time for repayment. This means that though there was low level of outright default in credit repayment among the respondents, the repayment was chatracterised by high level of delay in repayment.

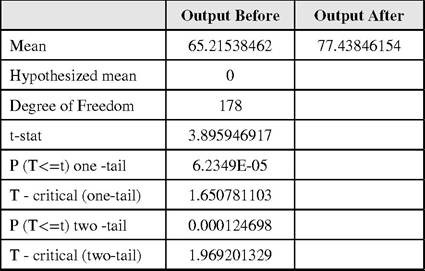

Impact of Microfinance Bank Credit Scheme on the Output and Income of Respondents

Impact of Credit on Output of Farmers

The result of the t-test in Table 4 rejects the null hypothesis that there is no significant difference between the output of respondents (beneficiaries) before and after the utilization of micro-credit obtained from the Microfinance Bank Credit Scheme. This suggests that the agricultural credit accessed by the maize farmers in the study area from the Microfinance Bank Credit Scheme significantly improved their maize output.

Impact of Credit on Income of Farmers

The results of the t-test in Table 5 reject the null hypothesis thatthere is no significant difference between the income of respondents (beneficiaries)

Table 4. The t-test of no significance difference between output of respondents before and after utilization of credit

Source: Field Survey, 2012

before and after the utilization of micro-credit obtained from the Microfinance B ank Credit Scheme. This suggests that the agricultural credit accessed by the maize farmers in the study area from the Microfinance Bank Credit Scheme significantly improved their income and hence their welfare.

Constraints to Accessing Microfinance Bank Credit

Problems Faced in Accessing Credit

The result in Table 6 shows that majority of the respondents (34.44%) faced problem of administrative bottleneck in the course of accessing credits. This implies that an ineffective organizational structure of the credit institutions constitutes the major problem faced by the respondents in accessing credits.

Problems Faced Hindered

Access to Credit

The result in Table 6 shows that majority of the respondents (71.11%) agreed that problems encountered in the course of accessing credit hindered access to credits, suggesting that problems encountered made access to credit practically difficult and in some cases impossible.

Problems Faced in

Repayment of Credit

The result in Table 6 shows that majority of the respondents (46.67%) refered to inadequate loan as major hindrance in repayment of credits. This implies that inability to access adequate credits that guarantee quality investments and hence quality returns made it difficult for the farmers to repay credits timely or even outright default.

Table 5. The t-test of no significance difference between income of respondents before and after utilization of credit

| Income Before | Income After | |

| Mean | 10890.76923 | 14619.23077 |

| Hypothesized mean | 0 | |

| Degree of Freedom | 178 | |

| t-stat | 5.55912655 | |

| P (TIn Commercial Agriculture, Banking Reform and Economic Downturn: Setting a New Agendafor Agricultural Development in Nigeria. Proceedings of the 11th Annual National Conference of National Association of Agricultural Economists (NAAE) (pp.66-71), Minna: Federal University of Technology. Ministry of Finance Nigeria. (2007). The Nigeria microfinance newsletter. International Year of Microfinance, 4, 1-33. Musa, S. A., Hanisu, A. T., & Yakubu, S. A. (2010). Performance of the agricultural credit guarantee scheme fund (ACGSF) in Kano State. In Commercial Agriculture, Banking Reform and Economic Downturn: Setting a New Agenda for Agricultural Development in Nigeria. Proceedings of the 11th Annual National Conference of National Association of Agricultural Economists (NAAE) (pp. 114-120). Nigeria: Federal University of Technology. National Population Commission. (2007). The 2006 population census. Official Gazette, 94(24). Nwagbo, E. C. (1986). The credit institution in managing agricultural development in Nigeria. ARMTI Seminar. Nwagbo, E. C. (1989). Impact ofinstitutional credit on agriculture in Funtua local government area of Katsina state. Samaru Journal of Agricultural Research, 6, 79-86. Nwaru, J. C. (2004). Rural credit market and resource use in arable crop production in Imo state of Nigeria. (PhD Dissertation). Nigeria: Michael Okpara University of Agriculture. Nwaru, J. C. (2005). Determinants of farm and off-farm incomes and savings of food crop farmers in Imo state, Nigeria: Implication for poverty alleviation. NigerAgricultural Journal, 36, 26-42. Nweze, N. J. (1990). The structure, functioning and potentials of indigenous cooperative credit associations infinancing agriculture: The case of Anambra and Benue states, Nigeria. (Unpublished PhD Dissertation). Department of Agricultural Economics, University of Nigeria. Okerenta, S. I. (2005). Evaluation of the effects of microfinance programmes on rural life of farmers in the Niger delta region of Nigeria. (Unpublished PhD Dissertation). Department of Agricultural Economics, Federal University of Technology Owerri, Imo State, Nigeria. Okorie, A. (1986). Commercial bank lending to agriculture in performance of formal financial institutions infinancing agriculture in Abia State. (Unpublished PhD Dissertation). Department of Agricultural Economics, University of Nigeria, Nsukka, Nigeria. Olawuyi, S. O., Olapade-Ogunwole, F., Fabiyi, Y. L., & Ganiyu, M. O. (2010). Effects of microfinance bank credit scheme on crop farmers’ revenue in Ogbomoso south L.G.A of Oyo state. In Commercial Agriculture, Banking Reform and Economic Downturn: Setting a New Agenda for Agricultural Development in Nigeria. Proceedings of the 11th Annual Conference of National Association of Agricultural Economists (NAAE) (pp. 12-16), Nigeria: Federal University of Technology. Oluyombo, O. O. (2010). Assessment of rural sustainable development by micro finance banks in Nigeria. De Montfort University. Omeh, N. G. (2006). Determinants of commercialization of cassava production in Abia State, Nigeria. Unpublished. Phillip, D., Ephraim, N., John, P., & Omobowale, A. O. (2008). Constraints to increasing agricultural productivity in Nigeria. International Food and Policy Research Institute. Raw Material Update. (2003). Cassava: An important food and industrial crop. A Bi-Annual Publication of the Raw Material Research Development Council, 4(1), 10-23. Tasie, C. M. (2008). An evaluation of the effects of credit supply on rural farmers in Rivers state: The case of international fund for agricultural development (IFAD). (Unpublished M.Sc Thesis). Department of Agricultural Economics Federal University of Technology, Nigeria. Udoh, E. J. (2005). Demand and control of credit from informal sources by rice producing females of Akwa Ibom State, Nigeria. Journal of Agricultural and Food Science, 1(2), 152-155. United Nations Capital Development Fund (UNCDF). (1999). Microfinance: Building on lessons learned. New York: United Nations. Zeller, M. (1994). Determinants of credit rationing: A study of informal lenders and formal credit groups in Madagascar. Washington, DC: International Food Policy Research Institute. doi:10.1016/0305-750X(94)90181-3 KEY TERMS AND DEFINITIONS Agricultural Credit: A credit financing vehicle, such as a loan, banker’s acceptance or letter of credit, that is designed specifically for agriculture producers. Beneficiaries: A person who derives advantage from something, especially a trust, will, or life insurance policy. Credit: The ability to obtain goods or services before payment, based on the trust that payment will be made in the future: “unlimited credit.” Impact: Measure ofthe tangible and intangible effects (consequences) of one thing’s or entity’s action or influence upon another. Maize Farmers: Farmers involved in producing maize. Maize Production: Conversion or transformation of maize inputs to maize output. Microcredit: The lending of small amounts of money at low interest to new businesses in the developing world. Microfinance: Microfinance is usually understood to entail the provision of financial services to micro-entrepreneurs and small businesses, which lack access to banking and related services due to the high transaction costs associated with serving these client categories. This work was previously published in Global Strategies in Banking and Finance, edited by Hasan Dinyer and Umit Hacioglu, pages 158-171, copyright 2014 by Business Science Reference (an imprint of IGI Global).

More financial literature on Economics.Studio

More on the topic Chapter 59 Impact of Microfinance Bank Credit Scheme:

-

Conflictology -

Ecology -

Economy -

Finance -

History -

Law -

Medicine -

Philosophy -

Religious studies -

|