Chapter 10 Monitoring of the Entrenchment of Managers through Board Characteristics: Insights from Gender Diversity, Background and Independence Director’s

Nadia Ben Farhat-Toumi, Nouha Ben Arfa and Rim Khemiri

Abstract

The purpose of this study is to investigate the relationship between the entrenchment managerial and board characteristics in publicly traded French firms.

These two concepts are at the intersection of corporate finance and accounting, as managerial entrenchment and board characteristics may affect earnings management, which would make investors reluctant to invest in a firm. Using data on listed firms belonging to the SBF120, over the period 2011-2018, we mainly find that: the entrenchment managerial is impacted by (1) gender diversity, (2) educational background (3) and independence directors.Keywords: managerial entrenchment, board diversity, educational background, board independence

1. Introduction

The literature on both opportunistic and autocratic behavior of executives has bent the debates on the composition and functioning of the board of directors (BOD) to better protect the interests of shareholders, as well as the stakeholders of the company [1-3]. Recently, the resurgence of scandals of financial malpractice by CEOs, such as Bernard Maddof for the Ponzi pyramid in 2009, Jeffrey Skilling for the Enron affair in 2006 and recently Carlos Ghosn for the Renault-Nissan alliance in 2018, have furthermore oriented studies towards the analysis of the impact of certain characteristics of the BoD on the managerial latitude of executives. In France, the law of May 15, 2001 on the New Economic Regulations (NER) concerning the powers and functioning of governing bodies, has highlighted the dissociation of the functions of chairman and chief executive officer as well as the limitation on the accumulation of mandates.

A board of directors is effective when management and control functions are exercised by two different people [4-7], to establish checks and balances and to avoid any personal misappropriation that is harmful to the company and its shareholders.

In practice, this rule remains uncommon, even though it allows for real separation of decision-making and control functions, thus distributing responsibilities while guaranteeing a clarified separation of powers. The accumulation of functions thus allows the manager to adopt an autocratic management style to appropriate power in his or her interest and, moreover, to extend the duration of his or her mandate. This is the phenomenon of entrenchment as defined by Shleifer & Vishny [8]. According to entrenchment theory, this behavior allows the executive to entrench himself and anesthetize the boards [9]. This phenomenon has been the subject of several questions, especially about the effectiveness of the board. The board, which must monitor and advise the executive, is composed of directors with different demographic, individual and social characteristics. Several research studies emphasize the importance of the diversity of profiles within a board. Wirtz [3] and Maati & Maati-Sauvez [2], emphasize that a diverse board reduces the opportunism of managers. In this work, we are interested in certain characteristics of the board of directors, namely the independence of board members, gender diversity and the education of directors. The choice of these variables is explained on the one hand by the importance given to the feminization of boards in France through the CopeZZimmerman law of 2011. On the other hand, the social ties between directors and executives from the Grandes Ecoles such as Ecole Nationale d’Administration (ENA) and Polytechnique, is favorable to the entrenchment of executives [2, 10, 11].Moreover, the results of studies examining the relationship between the board and executive entrenchment appear to be controversial. In particular, studies of the relationship between the social ties between executives and directors are controversial, as these relationships can both hinder and contribute to the effectiveness of boards. Another debate on the issue of the entrenchment of managers is that of the presence of women on boards.

Can this presence call into question the autocratic behavior of the CEO? Is this presence a reason for legitimacy in the face of the quota imposed by the law or can the woman face an entrenched CEO?Thus, these questions and the lack of consensus on the link between the composition of boards of directors and the entrenchment strategies of managers call into question past studies. In this article, we propose to analyze the impact of women directors, education of directors, and board independence on executive entrenchment strategies.

Our research makes both theoretical and managerial contributions. First, for the relationship between the presence of women and the presence of a rooted CEO, few studies have examined this relationship in the French context. Thus, our article contributes to the governance literature by explaining the relationship between gender diversity and executive behavior. We provide some support for the hypothesis that the presence of women can change the strategies implemented by CEOs.

Then, we apprehend the means of entrenchment of the CEO by integrating the three strategies from the literature namely the age of the CEO, the duration of his mandate and the accumulation of functions. Indeed, studies have mainly focused on the entrenchment of CEOs through his network or his mandate [2, 11].

We quantify our work using a sample of 83 listed companies comprising the SBF 120 index and observed over a period from 2011 to 2018. In this framework, we show that women can both control and be impartial to the autocratic behavior of executives and this is a function of the rooting strategy. We also identify a negative and significant impact between directors from the Grandes Ecoles (ENAZPolytechnique) and executive tenure, whereas the literature has only highlighted a positive link between these directors and executive tenure. Finally, we show that an independent board can limit the discretionary power of managers. Our results may have a managerial effect if we focus on the dissociation of the executive’s functions.

The presence of a woman as well as directors who are enarques or polytechnicians seems to be useful when the manager combines the two functions of chairman and director.The remainder of the paper is organized as follows. Section 2 reviews the literature and develops our hypotheses. Section 3 describes the methodological aspects. Empirical results are presented and discussed in Section 4. Finally, in Section 5, we conclude with implications for further research and practice.

2. Board diversity

In this section, we present the review of the literature on the relationship between gender diversity, education of directors, board independence, and management entrenchment, while developing our research hypotheses.

2.1 Gender diversity

Since the constitution and implementation of the policy on quotas for women’s representation on boards, several European countries such as Spain, Norway, Belgium and Italy have adopted legislative measures for the implementation of this policy in companies. Since 2011, France has introduced a law requiring listed companies to increase the number of women on their boards. This law sets a mandatory quota of 40% of the underrepresented gender on boards of directors by January 1, 2017 in listed companies. It also requires companies that do not have any women on their Boards at the time of its enactment to appoint women within the following 6 months.

The activism that has focused on the gender balance in corporate governance bodies bears witness to the pitfalls of the feminization of boards. Beyond the regulatory and institutional framework, several researchers have stressed the importance of increasing the appointment of women to boards of directors. The arguments put forward for increasing the number of women on boards of directors are numerous [12,13]. Two perspectives can be mobilized.

First, consistent with Fama & Jensen’s agency theory [14], board members should monitor managers to minimize agency costs and maximize firm value for shareholders.

Researchers have investigated the relationship between board feminization and firm financial performance [15-19]. Other empirical studies highlight the importance of the latter in strengthening governance practices, including the board of directors. Harford et al. [20] and Wang et al. [21], specify that firms with an effective board reduce managerial opportunism and authority. In addition, Adams and Ferreira [15], show that board feminization impacts CEO departure rates at the head of the lowest- performing firms.Second, the other stream of literature on gender diversity, which focuses on women’s human capital, has shown a positive relationship between the feminization of boards and the quality of governance. Huse & Solberg [22] as well as Spell & Bezrukova [23] find a positive and significant relationship between the human factor of women (skills, attitudes, behavior...) and managerial manipulation (financial fraud).

In the same spirit, another group of researchers highlights the importance of appointing women to boards [24, 25]. They argue that a board with one or more women is less prone to manipulation by managers. However, the Maati and Maati-Sauvez [2] study find that executives are more influential in the presence of increased board feminization.

Given the conflicting results on the relationship between women’s presence and CEOship manipulation, we propose the following hypothesis:

Hypothesis 1: CEO is less entrenched when the percentage of women present on the board is high.

2.2 Education of directors

As suggested by some authors such as Hambrick & Mason [26] and Barro & Lee [27], human capital is the body of knowledge and skills that each individual has been able to acquire through education and training. The human capital theory assumes that individuals’ knowledge and skills enable them to be productive in their assignments [28]. A highly educated board will be better able to advise and monitor the CEO [21]. Several research studies highlight the importance of the level of director education on the effectiveness of the board and strategic choices.

Rosenkopf & Nerkar [29], highlight a significant and positive relationship between the quality of director education and organizational decision making.Gales & Kesner [30] as well as other researchers point out that a board with scientific directors allows for more innovative strategies, and can advise and monitor a research project [21]. Other work has examined the relationship between board member education and firm performance. The results reveal that the level of education of directors is positively associated with financial performance and enhances the monitoring role of the board [31, 32]. Thus, an educated board improves corporate governance. These ideas could therefore lead us to assume that good corporate governance requires an effective board composition.

The education of its members is a decisive criterion in the composition of the latter, thus reducing the opportunism of the CEOs. Hence the following hypothesis:

Hypothesis 2: The nature of the education of directors reduces the entrenchment of CEO.

Several empirical studies define the quality of education by the prestige of the schools attended [33, 34]. Despite the importance of educational background in the recruitment of directors, the prestige of the institution they attend, as well as the networks developed within that school, have a very important impact on the selection of board members. The social capital built up within these prestigious institutions contributes not only to the development of human capital but also to the company’s social network [35, 36]. Work on the sociology of education and the elite has highlighted the importance of schools in the construction of elite identity [37]. Most empirical studies emphasize that administrators from elite schools possess a social network that allows them easy access to even government resources [38] and possesses greater control to monitor CEOs [39].

In France, the Grandes Ecoles (GE), notably ENA and Polytechnique play a similar role as Ivy Leagues in the US or Cambridge and Oxford in the UK [40]. Several research studies argue that this elite network, which allows easier access to the board of directors, weakens the latter’s monitoring role [41, 42].

However, the existence of these social relationships can also be a key factor in the governance structure. For Kramarz & Thesmar [41], CEOs may use their social networks to make advice and monitoring more effective. Examining these results does not provide a general framework, which leads us to test the following hypothesis:

Hypothesis 3: A predominantly elitist board of directors impacts executive entrenchment.

2.3 Board independence

For the proponents of the agency theory, the presence of independent directors on the board of directors makes it possible to restrict the opportunistic behavior of the managers. Fama & Jensen [14] emphasize that these independent members must work in the interest of the shareholders.

Several empirical studies have tested the relationship between board independence and management entrenchment. The results obtained are not conclusive and do not show a consensus concerning this relationship. Indeed, Chen & Jaggi [43] and Ben Ali [44], show that boards dominated by independent members are likely to better monitor the executive and protect shareholders’ interests. In this sense, Jensen [6] and Patelli & Prencipe [45] emphasize that independent directors must fulfill their oversight role to build their reputation. The results of Chen [46], show that an independent board reduces agency conflicts. According to the same authors, investment opportunities are higher in firms with a more independent board. Thus, managerial incentives are better controlled in the presence of independent members [47-49]. The results of Ma & Khanna [48] show that reputation strongly motivates independent directors, who for their own interest must disapprove of executive strategies and decisions that may lead to a bad decision. However, Parrat [50] does not confirm the monitoring role of independent directors. Indeed, the author explains that the latter are chosen by the manager according to personal criteria. Therefore, they cannot oppose the decisions of the latter [51].

The analysis of this research does not allow for a consensus due to the diversity of the results, which leads us to formulate the following hypothesis:

Hypothesis 4: Board independence impacts CEO entrenchment.

3. Research methodology

3.1 Sample and data

The initial sample is composed of French companies belonging to the SBF120 index over the 2011-2018 period[5]. The choice of this period for our empirical study is justified by the entry of the Cope-Zimmerman law adopted in 2011.

The data was collected from several sources. Data on the education of directors was collected manually from the companies’ annual reports. When not available, we used the Who’s Who database[6]. We used Bloomberg for data on corporate governance and executives and Datastream for accounting and financial data.

To create our sample, we first excluded firms belonging to the finance sector. Then, we selected firms for which annual reports and data on directors and officers

are available. After applying these selection criteria, the final sample was reduced to 82 companies.

3.2 Measures

Dependent variables: these are the three following variables.

• AGEDIR: is measured by a binary variable equal to 1 if the age of the manager is close to retirement, 0 otherwise.

• ANCDIR: since the average seniority of managers is 4 years, we have retained 4 as the binarization threshold.

• CUMDIR: is measured by a binary variable equal to 1 if the manager has been at the head of the company for 8 years or more, 0 otherwise.

Explanatory variables: to test our models, we retain the following explanatory variables that constitute governance variables.

• INDEP: is measured by the proportion of independent directors on the Board.

• WEF: measured by the proportion of women on the Board.

• STRP: is measured by directors with a management background.

• ING: is measured by directors with an engineering background (all schools combined).

• JUR: measured by directors with a legal background.

• GE: measured by directors coming from ENA or Polytechnique.

Control variables: our models include control variables that may influence executive entrenchment. As a result, we included variables controlling for the effects of industry (ICB) [52], firm size (CA), firm performance (ROA). Listing seniority (ANCOT) is likely to influence managerial entrenchment [8, 53]. We also used ownership concentration (CONCAC), which is measured by the percentage of voting rights of the largest shareholder.

3.3 Descriptive statistics

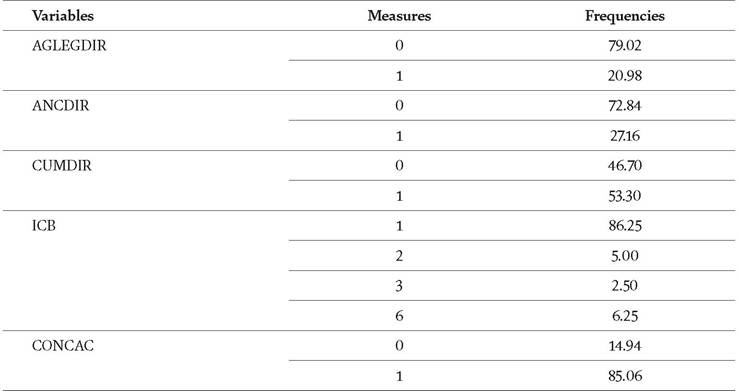

Descriptive statistics for the period 2011-2018 are presented in Table 1. It can be seen that, on average, 21% of the French managers in our sample are over the legal retirement age (60 years). We observe that 27% of firms have an executive with more than 8 years of service. About 53% of firms have an executive who combines the two functions of executive and chairman of the board. A separation is implemented by 46% of listed companies[7]. This observation can be explained by the opening of the

Table 1.

Descriptive statistics of the dichotomous explanatory variables.

market to foreign investors, who are in favor of the separation of functions. About 93.75% of the companies in our sample belong to the industrial sector and 6.25% to the technological sector. We find that 85% of the companies have a concentrated shareholding structure[8].

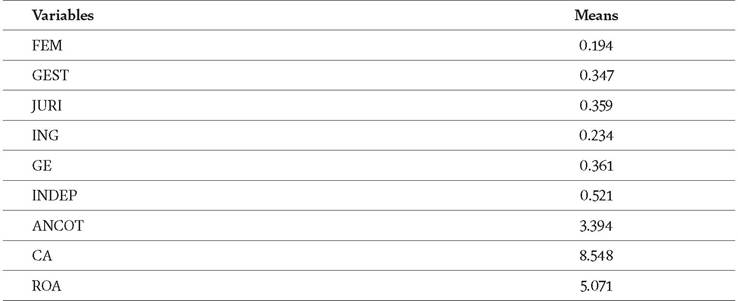

Table 2 also shows that on average 19%[9] of women hold a position on the board of directors, an average that has risen slightly according to the study by Hollandts et al. [54]. This tiny increase can be explained by the quota requirement introduced

Table 2.

Descriptive statistics for continuous explanatory variables.

CONCAC

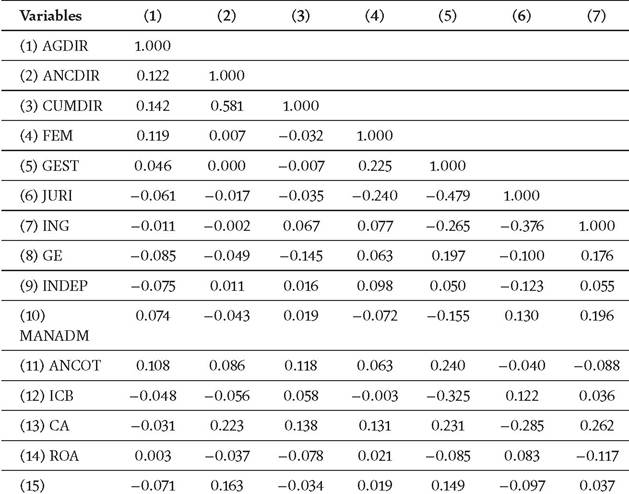

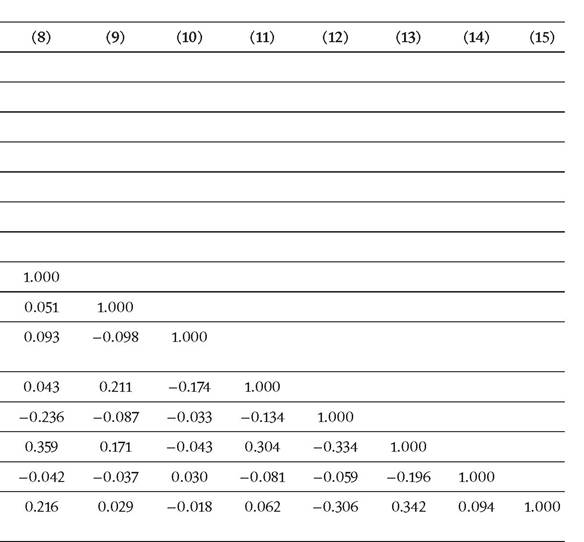

Table 3.

Pearson correlation matrix.

Banking and Accounting Issues

6 The percentage of women on boards according to the study by Hollandts et al. [54] is 13% with a study period from 2002 to 2014. Our period is from 2011 to 2018.

7 Managers outside ENA/Polytechnique.

8 In our study, we define the Grandes Ecoles by the institutions: ENA and Polytechnique, institutions that reflect the ties of friendship between the CEOs and an elite [55].

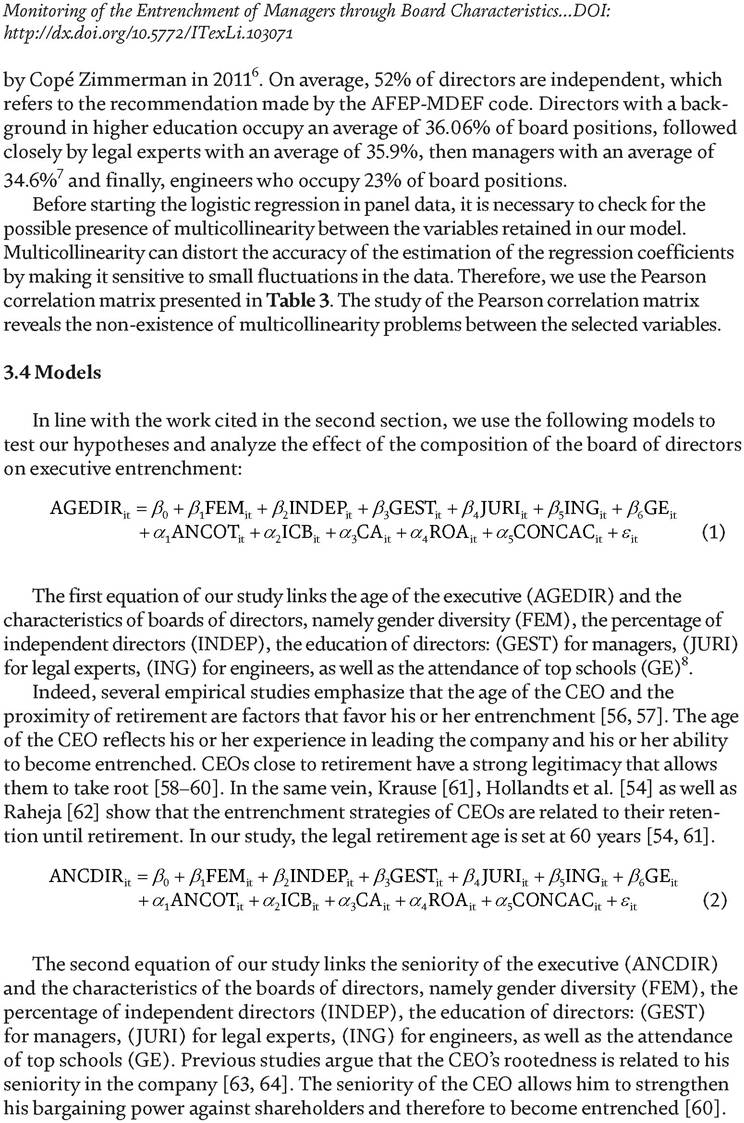

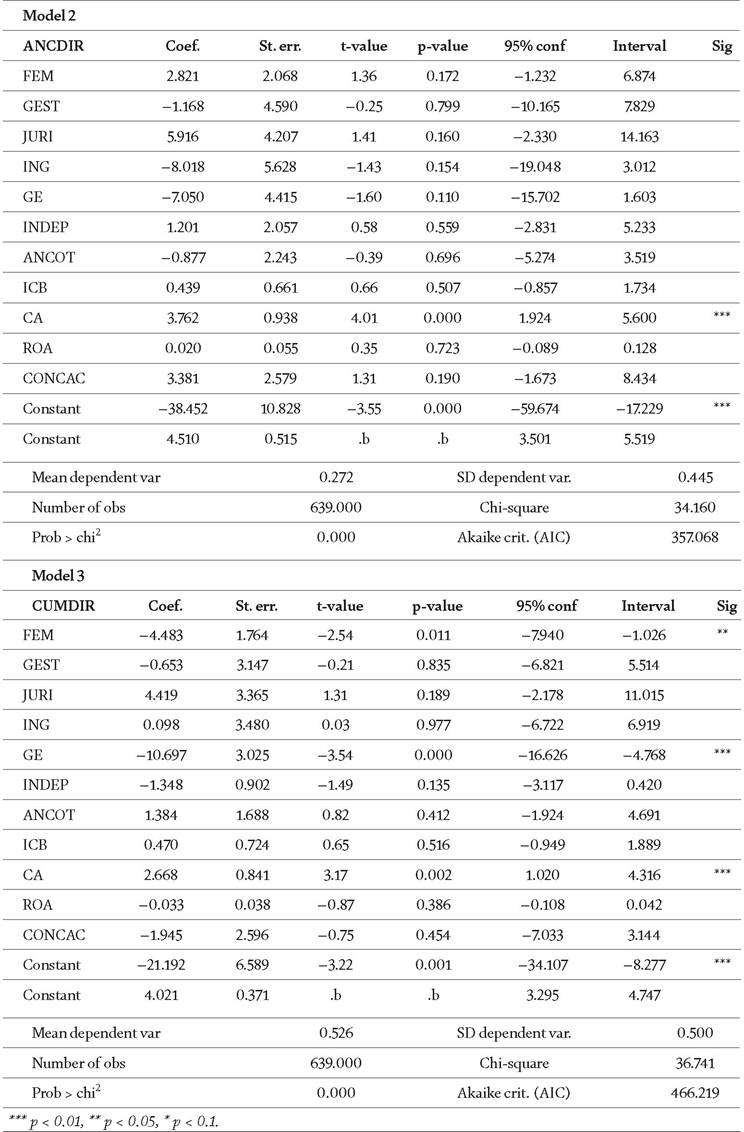

4. Results and discussion

The results of the different estimates are presented in Table 4. The association between gender diversity and the rootedness of managers is represented by a double effect, which may be related to the observation period, which includes the

Model 1

Table 4.

Regression results.

introduction and application of the Cope-Zimmerman Act. The first Model 1 presented below shows the positive and significant effect of the gender diversity variable on the age variable (AGEDIR), at the 1% threshold, which partially refutes hypothesis 1. Model 3 reveals a negative and significant effect of the gender diversity variable on multiple job titles (CUMDIR), at the 5% threshold, which partially confirms hypothesis 1. This overall effect may be linked to the increase in the number of women on boards following the Cope-Zimmerman Act (2011, 2014). The presence of women thus reinforces the retention of the executive until the legal retirement age. However, this presence also allows dissociation of the manager’s functions.

The first result could be explained by the pressure on women directors to conform to the choices of an entrenched CEO and therefore with some discretionary power. Our results are in line with the findings of Eagly and Carli [69] who point out that women face discriminatory barriers mainly in male-dominated environments. These include her exclusion from the executive’s networks and moreover from the board of directors [70]. Our finding also corroborates the conclusions of Pige [60] who considers that an executive with a high level of seniority, especially those beyond retirement age, benefits from an external legitimacy that gives him significant weight in front of the different members of the board.

This limits women’s access to information and board decisions and negatively biases judgments about their performance as directors. However, this discriminatory disadvantage may give the appearance of a female competence advantage [71], and these barriers encourage women to be more competent and overcome prejudice. According to Eagly et al. [72], Yoder [73] and Fortier [74], this effect plays an important role in women’s access and development within high responsibility positions. This may explain the result of Model 3 concerning the accumulation of the manager’s functions. Indeed, our tests show the influence of women in the entrenchment of the CEO especially in the separation between the functions of chairman and CEO. This result is consistent with the agency theory. The presence of women thus constitutes a disciplinary lever in the control of entrenched CEOs [15].

Regarding the independence of the board of directors, our results show a negative and significant relationship between the presence of independent directors and the age of the managers, which confirms hypothesis 4. This result is consistent with agency theory, which assumes that the board of directors must be sufficiently independent to best supervise the manager [14]. Our results corroborate those of Hermalin and Weisbach [47] who point out that the effectiveness of control increases with the level of independence of the board. On the one hand, companies apply to the letter the new recommendations concerning the independence and control of the board. The academic literature has often criticized the proximity between managers and directors. By avoiding appointing directors who are close to management, companies gain a certain legitimacy with investors. Our results thus contradict these previous studies [42]. On the other hand, independent directors become opportunistic by seeking to enhance and improve their reputation [50]. They put aside their feelings towards the executive and carry out their monitoring mission objectively, thus avoiding a bad image of their status in the director market. This can explain our results and confirms the agency theory [14].

Concerning the social network of directors, a negative and significant influence of a curriculum at ENAZPolytechnique on the rooting of executives is highlighted (H3 validated). Contrary to the studies of Nguyen [42] and Kramarz and Thesmar [41], the network of Grandes Ecoles does not favor the rooting of executives. A possible explanation for this result is possible concealment of the proximity between managers and directors. Indeed, to avoid any suspicion of elitism between the CEO, the director, the latter may control the decision-making and management functions of the BOD to take over the function itself. In the literature, the CEO can be replaced by a successor but cannot be ousted [75]. Indeed, Table 4 shows that the variable (GE) negatively and significantly influences Model 3 (Cumulative tenure), but does not influence the age of the CEO (Model 1). This effect can be explained by the possibility of a succession of the same polytechnician or enarque. Elite directors do not oppose executives who are close to retirement and intervene when they hold multiple directorships to obtain a potential succession.

Our results also show that directors with an engineering background have a significant and negative impact on the age of managers. This result is consistent with the results of Johnson et al. [76] who suggest that directors with technical qualities and higher-level are likely to control the strategic decisions of a board. Their level and cognitive experience give them certain personal importance within the board [77,78]. This gives them the power to reduce the CEO’s entrenchment strategies, particularly by preventing him or her from maintaining the position until retirement. For our control variables, our results show a positive and significant relationship between firm size and managerial tenure and multiple job titles. A possible interpretation of this result is that the manager’s anchoring is associated with turnover. Specifically, the executive has an interest in making profits to legitimize his position and maintain his tenure. This finding is consistent with the entrenchment theory. Indeed, by improving the performance of the company, the CEO acquires a capital of reputation that allows him to be irreplaceable and to acquire an important latitude within the company [79].

5. Conclusion

The purpose of this article is to examine the impact of women directors, director training, and board independence on the entrenchment of managers. First, the presence of women is significantly and negatively related to the age of the director. Women seem to favor the retention of the executive until retirement. But secondly, their presence reduces the number of functions they hold. Thus, women are more assiduous in applying the law concerning the dissociation of functions, but when it comes to their seniority through their legal retirement age, they do not have an impact, probably because of the age limit set by the law for managers, which remains flexible.

Our results also demonstrate the positive and significant impact of independent members as well as directors coming from top schools such as ENA and Polytechnique on executive entrenchment. From a theoretical point of view, our results corroborate those of previous research arguing that a diversified board contributes to the control of executive strategies. From a managerial point of view, our results should encourage companies to take more into account the recommendations of the AFEP-MEDEF regarding the diversity of the organization of management and control powers and the diversity of boards to guarantee certain objectivity in decision-making.

Our findings also highlight that the diversity of boards is an important governance mechanism that can limit the manipulation of managers. Moreover, this study is in line with the recommendations of the High Council for Equality between Women and Men on the need to have more diversity on boards of directors.

In particular, it might be interesting to include other characteristics, such as the education of women directors and the presence of foreign directors, in future studies to explain executive entrenchment.

Banking and Accounting Issues

References

[1] Anderson R, Reeb D, Upadhyay A, Zhao W. The economics of director heterogeneity. Financial Management. 2011;40 (1):5-38

[2] Maati J, Maati-Sauvez C. Uheterogeneite des administrateurs des entreprises cotees en France: Influence de la complexite de la firme et de la latitude manageriale et consequences sur la performance financiere. Finance, Controle, Strategie. 2016;19(4):53-79

[3] Wirtz P. Competences, conflits et creation de valeur: Vers une approche integree de la gouvernance. Finance Controle Strategie. 2006;9(2):187-201

[4] Abad D, Lucas-Perez ME,

Vera A, Yague J. Does gender diversity on corporate boards reduce information asymmetry in equity markets? Business Research Quarterly. 2017;20(3):192-205

[5] Godard L, Schatt A. Caracteristiques et Fonctionnements des conseils d’Administration Franςais: Un etat

des lieux. Revue Franςaise de Gestion. 2005;31(158):69-87

[6] Jensen MC. The modern industrial revolution, exit, and the failure of internal control systems. The Journal of Finance. 1993;48(3):831-880

[7] Mfouapon GK, Feudjo JR. Les determinants de l’efficacite du conseil d’administration (CA): Une exploration a partir des caracteristiques du president du CA? Recherches en Sciences de Gestion. 2015;106(1):25-44

[8] Shleifer A, Vishny RW. Management Entrenchment: The case of managers’ specific investments. Journal of Financial Economics. 1989;25:123-139

[9] Mard Y, Marsat S, Roux F. Structure de l’actionnariat et performance financiere de Tentreprisede cas franςais. Finance Controle Strategie. 2014;17(4):59-83

[10] Pan Y, Wang TY, Weisbach MS. CEO investment cycles. Review of Financial Studies. 2016;29(11):2955-2999

[11] Vanappelghem C, Blum V, Nguyen P. La proximite entre dirigeant et administrateurs peut-elle favoriser la performance de l’entreprise Can CEO- directors ties enhance firm performance? Finance Controle Strategie. 2018;20(4):2 7-68. Available from: revues.org

[12] Huse M, Nielsen S, Hagen I. Women and employee-elected board members, and their contributions to board control tasks. Journal of Business Ethics. 2009;89(4):581-597

[13] Hillman AJ, Shropshire C, Cannella Jr AA. Organizational predictors

of women on corporate boards. Academy of Management Journal. 2007;50(4):941-952

[14] Fama E, Jensen M. Separation of ownership and control. Journal of Law and Economics. 1983;26(2):301-325

[15] Adams RB, Ferreira D. Women in the boardroom and their impact on governance and performance. Journal of Financial Economics. 2009;94(2):291-309

[16] Toumi N, Ben KR, HamrouniI A. Board director disciplinary and cognitive influence on corporate value creation. Corporate Governance: The International Journal of Business in Society. 2016;16(3):564-578

[17] Campbell K, Minguez-Vera A. Gender diversity in the boardroom and firm financial performance. Journal of Business Ethics. 2008;83(3):435-451

[18] Ferrary M. Les femmes influencent- elles la performance des entreprises ? Une etude des entreprises du CAC 40 sur la periode 2002-2006. Travail, genre et societes. 2010;23:181-190

[19] Francoeur C, Labelle R, Sinclair- Desgagne B. Gender diversity in corporate governance and top management. Journal of Business Ethics. 2008;81 (1):83-95

[20] Harford J, Li K, Zhao X. Corporate boards and the leverage and debt maturity choices. International Journal of Corporate Governance. 2008;1(1):3-27

[21] Wang MJ, Su XQ, Wanh HD, Chen YS. Directors’ education and corporate liquidity: Evidence from boards in Taiwan. Review of Quantitative Finance and Accounting. 2017;49(2):463-485

[22] Huse M, Solberg AG. Gender related boardroom dynamics: How women make and can make contributions on corporate boards. Women in Management Review. 2006;22(2):113-130

[23] Spell CS, Bezrukova K. Genre, prise de decision et performance. Travail, genre et societes. 2010;23:191-199

[24] Nielsen S, Huse M. The contribution of women on boards of directors:

Going beyond the surface. Corporate Governance: An International Review. 2010;18(2):136-148

[25] Srinidhi B, Gul FA, Tsui J. Female directors and earnings quality. Contemporary Accounting Research. 2011;28(5):1610-1644

[26] Hambrick DC, Mason PA. The organisation as a reflection of its top managers. Academy of Management Review. 1984;9(2):193-206

[27] Barro RJ, Lee JW. A new data set of educational attainment in the world,

1950-2010. Journal of Development Economics. 2013;104(1):184-198

[28] Becker GS. Human Capital. 3rd ed. Chicago: University of Chicago Press; 1993

[29] Rosenkopf L, Nerkar A. Beyond local search: Boundary-spanning, exploration, and impact in the optical disk industry. Strategic Management Journal. 2001;22(4):287-306

[30] Gales LM, Kesner IF. An analysis of board of director size and composition in bankrupt organizations. Journal of Business Research. 1994;30(3):271-282

[31] Akpan EO, Amran NA. Board characteristics and company performance: Evidence from Nigeria. Journal Finance Accounting. 2014;2(3):81-89

[32] Haniffa RM, Cooke TE. Culture, corporate governance and disclosure in Malaysian corporations. Abacus. 2002;38:317-349

[33] Gottesman AA, Morey MR. Does a Better Education Make for Better Managers? An Empirical Examination of CEO Educational Quality and Firm Performance. April 21, 2006. Pace University Finance Research Paper No. 2004/03. DOI: 10.2139∕ssrn.564443. Available at SSRN: https://ssrn.com/ abstract=564443

[34] Terrence J, Rao R, Jalbert M. Does school matter? An empirical analysis of CEO education, compensation and firm performance. International Business & Economics Research Journal. 2002;1(1):83-98

[35] Belliveau MA, O’Reilly CA,

Wade JB. Social capital at the top: Effects of social similarity and status on CEO compensation. Academy of Management Journal. 1996;39(6):1568-1593

[36] Burt RS. Structural Holes. Cambridge: Cambridge University Press; 1992

[37] Van Zanten A. Promoting equality and reproducing privilege in elite educational tracks in France. In: Maxwell C, Aggleton P, editors. Elite Education. International Perspectives. London/New York: Routledge; 2015

[38] Goldman E, Jorg R, So J. Do politically connected boards affect firm value. Review of Financial Studies. 2009;22(1):2331-2360

[39] Dass N, Kini O, Nanda V, Onal B, Wang J. Board expertise: Do directors from related industries help bridge the information gap? Review of Financial Studies. 2014;27 (5):1533-1159

[40] Brezis ES, Crouzet F. The Role of Higher Education Institutions: Recruitment of Elites and Economic Growth. December 2004. DOI: 10.2139/ ssrn.641302. Available at SSRN: https:// ssrn.com∕abstract=641302

[41] Kramarz F, Thesmar D. Social networks in the boardroom. Journal of the European Economic Association. 2013;11:780-807

[42] Nguyen-Dang B. Does the rolodex matter? Corporate elite’s small world and the effectiveness of boards of directors. Management Science. 2012;58 (2):236-252

[43] Chen C, Jaggi B. Association between independent non-executive directors, family control and financial disclosures in Hong Kong. Journal of Accounting and Public Policy. 2000;19(4-5):285-310

[44] Ben Ali C. Qualite de la publication financiere et mecanismes de gouvernance en France. Management & Avenir. 2013;3(61):109-128

[45] Patelli L, Prencipe A. The relationship between voluntary disclosure and independent directors in the presence of a dominant shareholder. European Accounting Review. 2007;16(1):5-3

[46] Chen HL. Does board independence influence the topmanagement team? Evidence from strategic decisions toward internationalization. Corporate Governance; An International Review. 2011;19(4):334-350

[47] Hermalin BE, Weisbach MS. The determinants of board composition. RAND Journal of Economics. 1988;19:589-606

[48] Ma J, Khanna T Independent directors’ dissent on boards: Evidence from listed companies in China. Strategic Management Journal. 2016;37:1547-1557

[49] Liu Y, Miletkov Mihail K, Wei Z, Yang T. Board independence and firm performance in China. Journal of Corporate Finance. 2015;30(C):223-244

[50] Parrat F. Theories et pratiques de la gouvernance d’entreprise: Pour les conseils d’administration et les administrateurs. France: Maxima; 2015

[51] Caby J, Koehl J. La gouvernance d’entreprise apres la crise financiere: Soft Law ou Hard Law. Post-Print halshs-02024651. France: HAL; 2009

[52] Bebchuk LAM, Fried J. Executive compensation as an agency problem. Journal of Economic Perspectives. 2003;17(3):71-92

[53] D’Arcimoles C-H, Trebucq S. Etude de l’influence de la performance societale sur la performance financiere et le risque des societes franςaises cotees (1995-2002); Colloque interdisciplinaire Audencia Nantes, Ecole de Management Nantes. France; 16-17 octobre 2003

[54] Hollandts X, Borodak D, Tichit A. La dynamique de changement des formes de gouvernance: Le cas franςais (2000-2014). Finance, Controle et Strategie. 2018;21(3):129-158

[55] Kadushin C. Friendship among the French financial elite. American Sociological Review. 1995;60 (2):202-221

[56] Davidson WN, Xie B, Xu W, Ning Y. The influences of executive age, career horizon and incentives on pre- turnover earnings management. Journal of Management Science. 2007;11:45-60

[57] Matta E, Beamisch PW. The accentuated CEO career horizon problem: Evidence from international acquisitions. Strategic Management Journal. 2008;29 (7):683-700

[58] Hill C, Phan PH. CEO tenure as a determinant of CEO pay. Academy of Management Journal. 1991;34 (3):21-23

[59] Paquerot M. Strategies denracinement des dirigeants, performance de la firme et structure de controle. In: Le gouvernement des entreprises. France: Economica; 1997

[60] Pige B. Enracinement des Dirigeants et Richesse des Actionnaires. Finance Controle Strategie. 1998;1(3):131-158

[61] Krause R. Being the CEO’s boss: An examination of board chair orientations. Strategic Management Journal. 2017;38(3):697-713

[62] Raheja CG. Determinants of board size and composition: A theory of corporate boards. Journal of Financial and Quantitative Analysis. 2005;40(02):283-306

[63] Di Meo F, Garcia Lara JM, Surroca J. Managerial entrenchment and earnings management. Journal of Accounting and Public Policy. 2017;36(5):399-414

[64] Hambrick DC, Geletkanycz MA, Fredrickson JW. Top executive commitment to the status quo: Some tests of its determinants. Strategic Management Journal. 1993;14:401-418

[65] Mallette P, Fowler KL. Effects of board composition and stock ownership on the adoption of “poison pills”. Academy of Management Journal. 1992;35:1010-1035

[66] Booth JR, Millon C, Tehranian H. Boards of directors, ownership, and regulation. Journal of Banking and Finance. 2002;26:1973-1996

[67] Kang E, Zardhoohi A. Board CEOship structure and firm performance. Corporate Governance An International Review. 2005;13(6):785-799

[68] Lee SK, Lam TY. CEO duality and firm performance: Evidence from Hong Kong. Corporate Governance International Journal of Business in Society. 2008;8(3):299-316

[69] Eagly AH, Carli LL. The female CEOship advantage: An evaluation of the evidence. The CEOship Quarterly. 2003;14(6):807-834

[70] Fitzsimmons SR. Women on boards of directors: Why skirts in seats aren’t enough. Business Horizons. 2012;55(6):557-566

[71] Sharpe R. As Leaders, Women Rule: New Studies Find That Female Managers Outshine Their Male Counterparts in Almost Every Measure. Business Week, p. 74. Available from: http://www. businessweek.com/commonframes/ ca.htm?/2000/0047/b3708145.htm [Accessed December 15, 2000]

Monitoring of the Entrenchment of Managers through Board Characteristics...

DOI: http://dx.doi.org/10.5772/ITexLi.103071

[72] Eagly AH, Wood W, Diekman AB.

Social role theory of sex differences and similarities: A current appraisal.

In: Eckes T, Trautner HM, editors. The

Developmental Social Psychology of

Gender. Mahwah, NJ: Erlbaum; 2000.

pp. 123-174

[73] Yoder JD. Making CEOship work more effectively for women. Journal of

Social Issues. 2001;57:815-828

[74] Fortier I. Les femmes et le CEOship.

Gestion. 2008;3(33):61-67

[75] Chikh S, Filbien J. Acquisitions and CEO power: Evidence from French networks. Journal of Corporate Finance. 2011;17(5):1221-1236

[76] Johnson RA, Hoskisson RE,

Hitt MA. Board of director involvement in restructuring: The effects of board versus managerial controls and characteristics. Strategic Management Journal. 1993;14:33-50

[77] D’Aveni RA. Top managerial prestige and organizational bankruptcy. Organization Science. 1990;1(2):121-142

[78] Finkelstein S. Power in top management teams: Dimensions, measurement, and validation. Academy of Management Journal. 1992;35:505-538

[79] Finet A. Chapitre 1. Pourquoi le gouvernement dentreprise? Introduction et mise en place d’un cadre theorique d’analyse Dans Gouvernement d’entreprise. De Boeck Superieur. France; 2005. pp. 15-38