Glossary

accelerate To demand immediate repayment of debt in default, exercising thereby a right specified in the loan contract.

Accounting Principles Board (APB) Formerly, a rule-making body of the American Institute of Certified Public Accountants.

Predecessor of the Financial Accounting Standards Board (see).accrual accounting An accounting system in which revenue is recognized during the period in which it is earned and expenses are recognized during the period in which they are incurred, whether or not cash is received or disbursed.

actuarial assumptions Forecasts of the rates of phenomena such as mortality and retirements, used to determine funding requirements for pension funds and insurance policies.

APB Accounting Principles Board (see). book value The amount at which an asset is carried on the balance sheet.

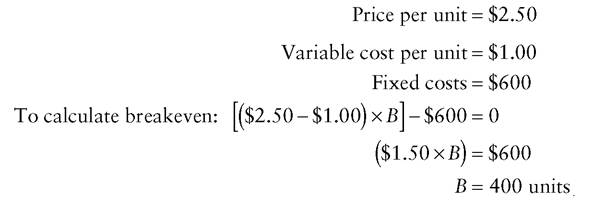

Book value consists of the asset’s construction or acquisition cost, less depreciation (see) and subsequent impairment of value, if applicable. An asset’s book value does not rise as a function of an increase in its market value or inflation. (See also historical cost accounting.) breakeven rate The production volume at which contribution (see) is equivalent to fixed costs (see), resulting in a pretax profit of zero.

Example:

Definitions of cash balance plan and defined benefit plan are adapted from descriptions provided by the Pension Benefit Guaranty Corporation.

bridge loan A temporary loan made in the expectation that it will subsequently be repaid with the proceeds of permanent financing.

business cycle Periodic fluctuations in economic growth, employment, and price levels.

Phases of the classic cycle, in sequence, are peak, recession, trough, and recovery.CAGR Compound annual growth rate (see).

capital-intensive Characterized by a comparatively large proportion of plant and equipment in asset base. The heavy depreciation charges that arise from capital intensity create a high level of fixed costs and volatile earnings.

capitalization (of an expenditure) The recording of an expenditure as an asset, to be written off over future periods, on the grounds that the outlay produces benefits beyond the current accounting cycle.

cash balance plan In the field of pensions, a type of defined benefit plan (see) in which each participant’s benefit is defined in terms of a hypothetical account balance. Each year, the account is credited with a pay credit and an interest credit specified by the plan. The interest credit may be fixed or based on a variable index such as the yield on 30-year Treasury bonds.

cash-on-cash profit In real estate, the cash flow from a property divided by the cash equity invested. Unlike conventional rate-of-return measures calculated in accordance with accrual accounting (see), cash-on- cash profit is not reduced by noncash charges such as depreciation (see). This reflects a presumption that land and buildings tend to increase in value over time, rather than lose value through wear-and-tear, as in the case of plant and equipment.

Chapter 11 Under the 1978 Bankruptcy Reform Act, a method of resolving bankruptcy that provides for reorganization of the failed firm as an alternative to liquidating it.

class-action suit A type of lawsuit filed under Federal Rule of Civil Procedure 23, which allows one member of a large group of plaintiffs with similar claims to sue on behalf of the entire class, provided certain conditions are met.

Damages awarded in certain class-action suits have been large enough to compromise the solvency of corporate defendants.comparability In accounting, the objective of facilitating financial comparisons of a group of companies, achieved by requiring them to use similar reporting practices.

compound annual growth rate (CAGR) The level, annual rate of increase that results in a stated beginning value rising to a stated terminal value.

Example:

| Year | .5pt 0cm.5pt; height:13.2pt'> |

| 0 | 377 |

| 1 | 421 |

| 2 | 414 |

| 3 | 487 |

| 4 | 541 |

| 5 | 596 |

The year-to-year increase in the asset’s value has been uneven, ranging from -1.7% in Year 2 to 17.6% in Year 4.

If the increase had been 9.6% in each year, however, the value would have grown from the beginning figure of $377 to the terminal figure of $596. Computation of the compound annual growth rate is a standard function on sophisticated hand-held calculators. CAGRs can also be derived from compound interest tables.consolidation (of an industry) A reduction in the number of competitors in an industry through business combinations.

contribution Revenue per unit minus variable cost (see) per unit.

convertible With reference to bonds or preferred stock, redeemable at the holder’s option for common stock of the issuer, based on a specified ratio of bonds or preferred shares to common shares. (See also exchangeable.) cost of capital The rate of return that investors require for providing capital to a company. A company’s cost of capital consists of the cost of capital for a risk-free borrower, a premium for business risk (the risk of becoming unable to continue to cover operating costs), and a premium for financial risk (the risk of becoming unable to continue covering financial costs, such as interest). The risk-free cost of capital is commonly equated with the prevailing interest rate on U.S. Treasury obligations.

cumulative dividend A characteristic of most preferred stocks whereby any preferred dividends in arrears must be paid before dividends may be paid to common shareholders.

default The failure of a debt obligor to make a scheduled interest or principal payment on time. A defaulting issuer becomes subject to claims against its assets, possibly including a demand by creditors for full and immediate repayment of principal.

defined benefit plan A type of pension plan in which the level of beneficiaries’ retirement income is established contractually, generally based on such factors as age, earnings, and years of service.

The pension plan sponsor bears the risk of earning a return on investment assets sufficient to meet the contractual payments. (See also cash balance plan, defined contribution plan.)defined contribution plan A type of pension plan in which the amounts contributed to the plan by its sponsor are established contractually. The retirement income paid to the beneficiaries is determined by the investment returns on the pension assets. (See also defined benefit plan.)

depreciation A noncash expense meant to represent the amount of capital equipment consumed through wear and tear during the period.

dilution A reduction in present shareholders’ proportional claim on earnings. Dilution can occur through the issuance of new shares in an acquisition if the earnings generated by the acquired assets are insufficient to maintain the level of earnings per share previously recorded by the acquiring company. Existing shareholders’ interest is likewise diluted if the company issues new stock at a price below book value. In this circumstance, a dollar invested by a new shareholder purchases a larger percentage of the company than is represented by a dollar of net worth held by an old shareholder.

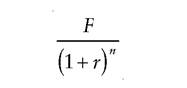

discount rate The interest rate used to equate future value (see) with present value (see). Also referred to as cost of capital (see).

discounted cash flow A technique for equating future cash flows to a present sum of money, based on an assumed interest rate. For example, $100 compounded annually at 8% over three years will cumulate to a sum of $125.97, ignoring the effect of taxes. This figure can be calculated via the equation

P × (l + r)n = F

where P = Principal value at beginning of period (Present value)

r = Interest rate

n = Number of periods

F = Principal value at end of period (Future value)

In this case, $100 × (1.08)3 = $125.97.

(Note that this formula implicitly assumes reinvestment of cash interest received at the original rate of interest throughout the period.)If $125.97 three years hence is equivalent to $100 today—given the assumed discount rate (see) of 8% per annum—then the ratio $100.00/$125.97, or 0.794, can be used to determine the present value (see) of any other amount discounted back from the same date and at the same rate.

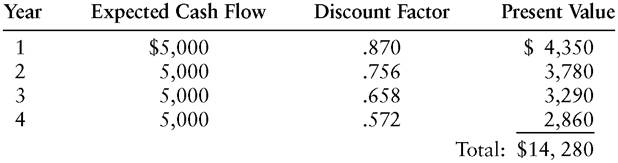

By using the same general formula, it is possible to assign a value to an asset, based on a series of cash flows it is expected to generate. By way of illustration, suppose the right to distribute a particular product is expected to generate cash flow of $5,000 a year for four years, then expire, leaving no terminal value. At a discount rate of 15%, the distribution rights would be valued at $14,820, derived as follows:

discretionary cash flow Cash flow that remains available to a company after it has funded its basic operating requirements. There is no universally accepted, precise definition of discretionary cash flow, but conceptually it includes funds from operations less required new investment in working capital and nondiscretionary capital expenditures. The latter figure is difficult to quantify with precision, but it exceeds the required “maintenance” level required to keep existing plant and equipment in good working order. Ordinarily, some additional expenditures, which may be designated “semidiscretionary,” are necessary to keep a company competitive with respect to capacity, costs, and technology. Only a portion of the total capital budget, including expansion-oriented outlays that can be deferred in the event of slower-than-expected growth in demand, can truly be considered discretionary. In a similar vein, mandatory principal repayments of debt, by definition, cannot be regarded as discretionary. Still, a company with strong cash flow and the assurance, as a practical matter, of being able to refinance its maturing debt, has considerable freedom in the disposition even of amounts that would app ear to be earmarked for debt retirement.

size=2 color=black face="Times New Roman">diversification In portfolio management, the technique of reducing risk by dividing one’s assets among a number of different securities or types of investments. Applied to corporate strategy, the term refers to participation in several unrelated businesses. The underlying premise is often countercyclicality, or the stabilization of earnings over time through the tendency of profits in certain business segments to be rising at times when they are falling in others.

double-entry bookkeeping A system of keeping accounts in which each entry requires an offsetting entry. For example, a payment to a trade creditor causes both cash and accounts payable to decline.

Dow Jones Industrial Average A widely followed index of the U.S. stock market composed of the common stocks of 30 major industrial corporations.

EBIT Earnings before deduction of interest expense and income taxes.

EBITDA Earnings before deduction of interest expense, income taxes, depreciation, and amortization. (Also referred to as EBDIT, an acronym for “earnings before depreciation, interest, and taxes.”)

economies of scale Reductions in per unit cost that arise from large- volume production. The reductions result in large measure from the spreading of fixed costs (i.e., those that do not vary directly with production volume) over a larger number of units than is possible for a smaller producer.

economies of scope Reductions in per unit cost that arise from applying knowledge or technology to related products.

exchangeable In reference to a security, subject to mandatory replacement by another type of security, at the issuer’s option. (See also convertible.) external growth Revenue growth achieved by a company through acquisition of other companies.

externally generated funds Cash obtained through financing activities such as borrowing or the flotation of equity. (See also internally generated funds.)

factor A financial institution that provides financing to companies by buying accounts receivable at a discount.

FASB Financial Accounting Standards Board (see).

Financial Accounting Standards Board (FASB) A rule-making body for the accounting profession. Its members are appointed by a foundation, the members of which are selected by the directors of the American Institute of Certified Public Accountants.

financial derivative A financial instrument with a return linked to the performance of an underlying asset, such as a bond or a currency.

financial flexibility The ability, achieved through such means as a strong capital structure and a high degree of liquidity, to continue to invest in maintaining growth and competitiveness despite business downturns and other financial strains.

financial leverage (See leverage (financial).)

fixed costs Costs that do not vary with the volume of production. Examples include rent, interest expense, senior management salaries and, unless calculated by the units-of-production method, depreciation (see).

fixed-rate debt A debt obligation on which the interest rate remains at a stated level until the loan has been liquidated. (Compare floating-rate debt.)

floating-rate debt A debt obligation on which the interest rate fluctuates with changes in market rates of interest, according to a sp ecified formula. (Compare fixed-rate debt.)

fundamental analysis A form of security analysis aimed at determining a stock or bond’s intrinsic value, based on such factors as the issuer’s expected earnings and financial risk. In contrast, technical analysis aims to predict a security’s future value based on its past price changes.

class=a7 style='margin-left:18.0pt;text-indent:-18.0pt;line-height:105%'>funding Replacement of short-term debt with long-term debt. Funding increases a company’s financial flexibility by reducing the near-term risk of insolvency through inability to roll over or replace maturing debt.future value The amount to which a known sum of money will accumulate by a specified future date, given a stated rate of interest. For example, $100 compounded annually at 8% over three years will cumulate to a sum of $125.97, ignoring the effect of taxes. This figure can be calculated via the formula

![]()

where P = Principal at beginning of period

r = Interest rate

n = Number of periods

In this case, $100 × (1.08)3 = $125.97. (This formula implicitly assumes that cash interest received will be reinvested at the original rate of interest throughout the period.)

(See also discounted cash flow, net present value, and present value.) GAAP Generally Accepted Accounting Principles (see).

GDP Gross Domestic Product (see).

Generally Accepted Accounting Principles Rules that govern the preparation of financial statements, based on pronouncements of authoritative accounting organizations such as the Financial Accounting Standards Board, industry practice, and the accounting literature (including books and articles).

goodwill A balance sheet item arising from purchase method (see) accounting for a business combination, representing the excess of the purchase price over the acquired company’s tangible asset value.

Gross Domestic Product The value of all goods and services that residents and nonresidents provide in a country.

historical cost accounting An accounting system in which assets are recorded at their original value (less any applicable depreciation or other impairment of value), notwithstanding that the nominal dollar value of the assets may rise through some cause such as inflation or increased scarcity. (See also book value.)

hostile takeover An acquisition of a corporation by another corporation or by a group of investors, typically through a tender for outstanding shares, in the face of initial opposition by the acquired corporation’s board of directors.

internal growth Revenue growth achieved by a company through capital investment in its existing business.

internally generated funds Cash obtained through operations, including net income, depreciation, deferred taxes, and reductions in working capital. (See also externally generated funds.)

investor-relations officer An individual designated by a corporation to handle communications with securities analysts.

involuntary inventory accumulation An unintended increase in a company’s inventory levels, resulting from a slowdown in sales that is not offset by a reduced rate of production.

LBO Leveraged buyout (see).

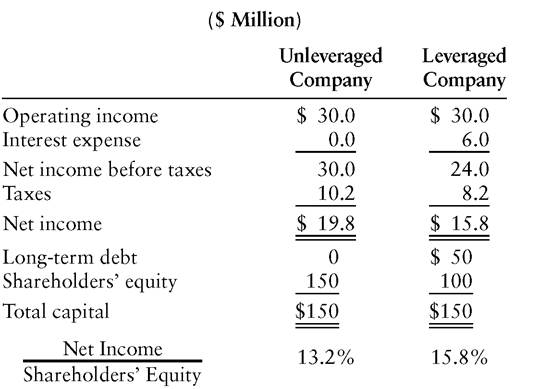

leverage (financial) lang=EN-US>The use of debt financing in hopes of increasing the rate of return on equity. In the following example, the unleveraged company, with no debt in its capital structure, generates operating income of $30.0 million, pays taxes of $10.2 million, and nets $19.8 million for a return on equity (net income divided by shareholders’ equity) of 13.2%. The leveraged company, with an equivalent amount of operating income, relies on long-term debt (at an interest rate of 12%) for one-third of its capital. Interest expense causes its net income before taxes to be lower ($24 million) than the unleveraged company’s ($30 million). After taxes, the leveraged company earns less (15.8 million) than the unleveraged company ($19.8 million), but on a smaller equity base ($100 million vs. $150 million) provides shareholders a higher rate of return ($15.8% vs. 13.2%).

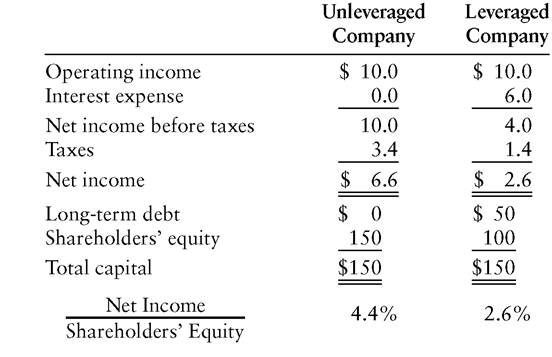

Note, however, that leverage works in reverse as well. In the following scenario operating income declines by two-thirds (to $10 million) at both companies. With no interest expense, the unleveraged company

manages to net $6.6 million for a 4.4% return on equity. The leveraged company, obliged to pay out 60% of its operating income in interest expense, suffers a sharper decline in return on equity (to 2.6%). Incurring financial leverage increases the risk to equity holders, whose returns become more subject to fluctuations. The greater the percentage of the capital structure that consists of debt, the greater is the potential for such fluctuations.

($ Million)

leverage (operating) The substitution of fixed costs (see) for variable costs (see) in hopes of increasing return on equity. In the following example, Company A’s cost structure is dominated by variable expenses, of which labor represents a substantial portion. A 5% increase in sales volume (from 500,000 to 525,000 units) raises the rate of return on shareholders’ equity from 11.0% to 13.7%. Company B, on the other hand, has installed labor-saving equipment that sharply reduces manhours per unit of production. Its variable costs are lower than Company A’s ($50.00 versus $30.00 per unit), but as a function of its greater depreciation (see) charges, its fixed costs are higher ($30 million versus $25 million per annum). The benefit of Company B’s higher operating leverage is that a 5% increase in its unit sales raises its return on shareholders’ equity from 11.0% to 14.7%, a larger boost than Company A receives from a comparable rise in volume. By the same token, Company B’s return on shareholders’ equity will fall more sharply than Company A’s if unit volume at both companies subsequently recedes from 525,000 to 500,000 units.

Company A Company B

| Sales (units) | 500,000 | 525,000 | 500,000 | 525,000 |

| Price per unit | $100.00 | $100.00 | $100.00 | $100.00 |

| Fixed costs ($ million) | $25.0 | .5pt 0cm.5pt; height:14.15pt'> $30.0 | $30.0 | |

| Variable cost per unit | $50.0 | $50.0 | $30.0 | $30.0 |

($ Million)

| Sales | $50.0 | $52.5 | $50.0 | $52.5 |

| Fixed costs | 25.0 | 25.0 | 30.0 | 30.0 |

| Variable costs | 25.0 | 26.3 | 15.0 | 15.8 |

| Income before taxes | 5.0 | 6.2 | windowtext 1.0pt; background:white;padding:0cm.5pt 0cm.5pt;height:13.45pt'> 6.7 | |

| Taxes | 1.7 | 2.1 | 1.7 | 2.3 |

| Net income | $ 3.3 | $ 4.1 | $ 3.3 | $ 4.4 |

| Shareholders’ equity | $30.0 | $30.0 | $30.0 | $30.0 |

| Net Income | 11.0% | 13.7% | 11.0% | 14.7% |

Shareholders’ Equity

leveraged buyout (LBO) An acquisition of a company or a division, financed primarily with borrowed funds. Equity investors typically hope to profit by repaying debt through cash generated by operations (and possibly from proceeds of asset sales), thereby increasing the net value of their stake.

leveraged recapitalization A corporate strategy involving the payment of a large, debt-financed cash dividend. The strategy is often employed as a defense against an attempted hostile takeover, for two reasons. First, by increasing the company’s financial leverage (see), the transaction reduces the potential for a raider to use borrowed funds, lest the posttakeover company become excessively debt-laden. Second, the recapitalization increases the concentration of ownership in the hands of those attempting to retain control.

liquidity The ability of a company to meet its near-term obligations when due.

macroeconomic Pertaining to the economy as a whole or its major subdivisions, e.g., the manufacturing sector, the agricultural sector, the government. (See also microeconomic.)

market capitalization The aggregate market value of all of a company’s outstanding equity and debt securities. Also used loosely to represent the product of a company’s share price and number of shares outstanding. (See also total enterprise value.)

mature With respect to a product, firm, or industry, at a stage of development at which the rate of sales growth remains positive but no longer exceeds the general growth rate of the economy.

microeconomic Pertaining to a small segment of the economy, e.g., an individual industry, a particular firm. (See also macroeconomic.)

multiple With respect to a common stock, the ratio of the share price to earnings per share. Similarly, the price paid in an acquisition can be viewed as a multiple of the acquired company’s earnings, cash flow, or EBITDA (see).

multivariate In the field of quantitative modeling, having the characteristic of employing more than one explanatory factor.

mutual fund An investment vehicle consisting of a portfolio of securities, shares of which are sold to investors. The firm that organizes the fund collects a fee for managing the portfolio, while shareholders enjoy a diversification (see) benefit that would be more costly to obtain via direct purchase of individual securities.

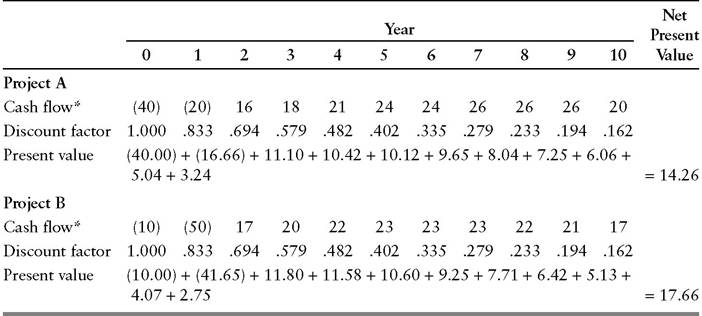

net present value The present value (see) of a stream of future cash inflows, less the present value of an associated stream of current or future cash outflows. This calculation is useful for comparing the attractiveness of alternative investments, as shown in the following example. Both proposed capital projects require an expenditure of $60 million during the first year. Project A generates a higher cash flow, without trailing off in the latter years as Project B is projected to do. Residual value in year 10 is likewise superior in Project A. Even so, Project B is the more profitable investment, based on a higher net present value ($17.7 million vs. $14.3 million for Project A).

Net Present Value Illustration (Presumed Discount Rate = 20%) ($000,000 omitted)

*Figures in parentheses represent projected outflows, i.e., construction costs. Figures for years 2-9 represent projected inflows, i.e., net income plus noncash expenses. Year 10 figure represents expected residual value of equipment.

nominal dollar A monetary sum expressed in terms of its currency face amount, unadjusted for changes in purchasing power from a designated base period. (See also real dollar.)

operating leverage (See leverage (operating).)

payment-in-kind security (PIK) A security (generally a bond or preferred stock) that gives the issuer an option to pay interest or dividends in the form of additional fractional bonds or shares, in lieu of cash.

payout ratio Dividends per share divided by earnings per share. In financial theory, a low payout ratio (other than as a result of a dividend reduction forced on the company by financial distress) is generally viewed as a sign that the company has many opportunities to reinvest in its business at attractive returns. A high payout ratio, in contrast, is appropriate for a company with limited internal reinvestment opportunities. By distributing a large percentage of earnings to shareholders, the company enables them to seek more attractive returns by investing elsewhere.

PIK lang=EN-US>Payment-in-kind security (see).

pooling-of-interests method A method of accounting for a business combination accomplished through an exchange of stock. No goodwill (see) is created in accounting for the transaction, even if the price paid for one of the parties exceeds its tangible asset value. In 2001, the Financial Accounting Standards Board forbade the further use of pooling-of- interests accounting, leaving the purchase method (see) as the only acceptable approach to business combinations.

portfolio A group of securities. Barring the unlikely circumstance that all securities contained in a portfolio produce identical returns in all p eri- ods, it generally produces a steadier return than a single security. The comparative stability arises from the tendency of declines in the prices of certain securities to be offset by rises in the prices of others during the same period. (See diversification.)

present value The sum that, if compounded at a specified rate of interest, or discount rate (see), will accumulate to a particular value at a stated future date. For example: To calculate the present value of $500, five years hence at a discount rate of 7%, solve the equation.

where F = Future value

r = Interest rate

n = Number of periods p = Present value

In this case $500/(1.07)5 = $356.49.

(See also discounted cash flow, future value, and net present value.) pro forma Describes a financial statement constructed on the basis of sp ecified assumptions. For example, if a company made an acquisition halfway through its fiscal year, it might present an income statement intended to show what the combined companies’ full-year sales, costs, and net income would have been, assuming that the acquisition had been in effect when the year began.

purchase method A method of accounting for business combinations in which goodwill (see) is created if the acquisition price exceeds the tangible asset value of the acquired company.

rationalization In reference to a business or an industry, the process of eliminating excess capacity and other inefficiencies in production.

real dollar A monetary sum expressed in terms of its purchasing-power equivalent, relative to a designated base period. For example, at the end of the third quarter of 2001, $500 (face amount) had only 56.1% of the purchasing power that $500 had in the base period 1982-1984. The erosion reflected price inflation during the intervening years. The real value of $500 in September 2001 was therefore $280.50 in 1982-1984 dollars. This calculation employs a series of the purchasing power of the consumer dollar, published by the United States Bureau of Labor Statistics. See the Bureau’s Web site, www.bls.gov. (See also nominal dollar.) reinsurance A transaction whereby one insurance company takes over the risk of a policy originally issued by another company.

reorganization proceedings A procedure under Chapter 11 of the Bankruptcy Reform Act that permits a bankrupt company to continue in operation, instead of liquidating, while restructuring its liabilities with an aim toward ensuring its future financial viability.

reported earnings A company’s profit or loss for a specified period, as stated in its income statement. The figure may differ from the company’s true economic gain or loss for the period for such reasons as delayed recognition of items affecting income, changes in accounting practices, and discrepancies between accruals and actual changes in asset values.

Disparities between reported and economic earnings can also arise from certain nuances of inventory accounting. For example, under the last-in, first-out (LIFO) method, a company’s inventory account may include the historical acquisition costs of goods purchased several years earlier and unaffected (for book purposes) by inflation in the interim period. To the extent that a surge in sales causes a company to recognize the liquidation of older inventories during the current period, revenues will reflect post-inflation (i.e., higher) values but expenses will not. The mismatch will produce unusually wide reported profit margins in the current period, even though the nominal dollar (see) gains arising from inflation are in reality benefits that accumulated over several preceding periods.

sale-leaseback A transaction in which a company sells an asset and immediately leases it back. The lessee thereby obtains cash while retaining use of the asset. An additional motivation for the transaction may be a difference in the marginal tax rates of the lessee and lessor. The tax shelter provided by depreciation charges on the asset are more valuable to the party paying the higher tax rate.

scale economies (See economies of scale.) SEC Securities and Exchange Commission (see).

Securities and Exchange Commission (SEC) An agency of the federal government that regulates the issuance and trading of securities, the activities of investment companies and investment advisers, and standards for financial reporting by securities issuers.

senior debt Borrowings that have preference in liquidation over subordinated debt (see). In the event of a bankruptcy, senior lenders’ claims must be satisfied before consideration can be given to subordinated lenders or equity investors.

sensitivity analysis The testing of “what-if” scenarios in financial statement analysis. Typically, sensitivity analysis measures the potential impact (on earnings, cash flow, etc.) of a change of a stated amount in another variable (sales, profit margins, etc.). In connection with financial forecasting, sensitivity analysis may be used to gauge the variation in projected figures that will occur if a particular assumption proves either too optimistic or too pessimistic by a given amount.

SFAS Statement of Financial Accounting Standards. Designation for a numbered series of statements of accounting rules promulgated by the Financial Accounting Standards Board (see).

shakeout A reduction in the number of competitors (through failures or through mergers) that typically occurs as a rapidly growing industry begins to mature. Factors that may contribute to a firm’s survival during a shakeout include advantages in raising new capital, economies of scale (see), and superior management.

short interest ratio The ratio between the number of a company’s shares that are sold short and remain uncovered and the stock’s average daily trading volume. A high ratio indicates a widespread expectation that the stock’s price will decline.

slack Unutilized productive capability within a company. Although the term ordinarily connotes inefficiency, management may have a conscious strategy of maintaining a certain amount of slack. For example, a company may benefit from keeping skilled employees on the payroll during recessions, when demand can be met with a reduced workforce. The cost savings entailed in laying off the workers may be offset by the costs of replacing them with equally skilled employees during the next boom. Another example is a backup trading floor maintained by a company engaged in trading securities or commodities. The associated cost may be justified by the potentially devastating loss of business that could result in a shutdown of the primary trading floor because of a natural disaster or civil disturbance.

standard error of estimate A measure of the scatter of the observations in a regression analysis. In statistical terms, the standard error of the estimate is equivalent to the standard deviation of the vertical deviations from the least-squares line.

statement of stockholders’ equity A financial statement that details changes in components of stockholders’ equity, including capital stock, paid-in capital, retained earnings, treasury stock, unrealized loss on long-term investments, and gains and losses on foreign-currency translation. The basic problem addressed by the statement of stockholders’ equity is that it may not be possible to reconcile one year’s equity account with the next year’s using only the income statement and statement of cash flows. Certain adjustments to equity are included neither in earnings nor in cash flows from financing activities.

statutory tax rate The percentage of pretax income that would be recorded as income tax if all of a company’s reported income were subject to the corporate tax rate specified by federal law. Disparities between the statutory rate and the effective rate (that which is actually recorded) arise from such reasons as tax credits and differences between U.S. and foreign tax rates.

straight-line method A depreciation method that charges off an equivalent portion of the asset in each period. During inflationary periods, straight-line depreciation may understate the true economic impact of capital consumption. That is, as the replacement cost of the asset rises in nominal terms, the dollar amount required to offset wear and tear during a period grows to exceed a pro rata write-off based on the original acquisition cost. In these circumstances, accelerated methods of depreciation, which result in larger amounts being written off in earlier than in later years, represent more conservative reporting of expenses.

subordinated debt Borrowings that have a lesser preference in liquidation vis-a-vis other, senior, debt (see). In the event of a bankruptcy, subordinated lenders’ claims cannot be provided for until senior claims have been satisfied.

synergy An increase in profitability arising from a merger or acquisition, relative to the stand-alone profitability of the companies involved. Synergy may result from economies of scale (see) or economies of scope (see).

total enterprise value The value that a business would fetch if put up for sale, commonly estimated as a multiple of its sales, earnings, or EBITDA (see). (See also market capitalization.)

units-of-production method A depreciation method that is based on the estimated total output of an asset over its entire life. The asset’s cost is divided by the estimated number of units to be produced. Depreciation for the period is then calculated by multiplying the cost per unit by the number of units produced during the period. The units-of-production method appears, on its face, to match revenues and expenses rather precisely. While a piece of equipment sits idle, however, it generates no depreciation expense—even though its value may be decreasing as a result of the introduction of technologically more advanced, lower-cost equipment by competing firms. In this light, adoption of the units-of- production method by a firm that formerly employed a straight-line or accelerated method should generally be viewed as a switch to a more liberal accounting practice.

variable costs Costs that increase as the volume of production rises. Examples include materials, fuel, power, and wages.

working capital Current assets minus current liabilities. Working capital is commonly employed as an indicator of liquidity, but care must be taken in interpreting the number. The balance sheets of some corporations that are strong credits by all other methods ordinarily have little (or even negative) working capital. These companies manage inventories closely and extract generous terms from creditors, including long payment periods, which result in chronically high trade payable balances. In such cases, no threat of illiquidity is implied by the fact that more liabilities than assets will be liquidated during the current operating cycle.