Innovations in Processing

During the 1980s, the most important innovations in processing were facilitated by advances in computer technology (Frame and White, 2010; LaCour-Little, 2000). The rapid expansion of financial markets was possible only with the growing speed, size, and data storage capacity of computers.

Without computers, it would have been impossible for banks to get larger, ATMs to spread, and credit card operations to expand. All of the important process innovations in the 1980s and 1990s in the mortgage industry were based on the ability to use computers to collect and process massive amounts of information about consumers, mortgagors, and mortgages.But this is not a story of technological determinism. The real story is that process innovations that were necessary to produce new financial products could work only with the ability to transact more rapidly. Indeed, financial institutions had pushed innovation in the gathering, processing, and storage of large amounts of data beginning in the early twentieth century (Yates, 2005). They were among the first customers of modern computers, and the large mainframe computer is still at the core of data processing for financial institutions.

But computers need to be told what to do. To make sense of all of these transactions, financial institutions had to produce a set of tools or devices that allowed them to process information in a meaningful fashion. Indeed, without processes to structure what the computers were doing, nothing interesting would have happened. A useful way of thinking about a process innovation is what might be called a market device (Callon et al., 2007). Callon et al. (2007: 2) define market devices as “material and discursive assemblages that intervene in the construction of markets. From analytic techniques to pricing models, from purchase settings to merchandising tools, from trading protocols to aggregate indicators, the topic of market devices includes a wide array of objects.” The innovation of these devices wove together computer technology, computer programming, and the use of quantitative data to produce processes that transformed the mortgage industry.

In the case of mortgage finance, I focus on a small set of such innovations: computer programs to enter data and approve mortgages, credit scores, and securitization.2 The most important of these innovations was securitization, which was the technique used to create securities out of financial instruments that were generating some kind of cash flow. There are three aspects to securitization that are necessary to explore: the creation of legal vehicles called special-purpose vehicles (SPVs) and relatedly the real estate mortgage investment conduit (REMIC) that “owned” the security being produced, the use of tranching to divide the security into pieces that could be sold to buyers, and the use of ratings to evaluate the riskiness of the tranches. My goal here is to explore how the process of making securities out of mortgages evolved and pushed the innovations forward. By the late 1990s, these market devices were well known and had widely diffused across the mortgage securitization industry.

Innovation in Loan Processing

Beginning in the 1980s, it became possible to automate the process of loan origination (Frame and White, 2010). But the relative fragmentation of the industry and the presence of the savings and loan model of origination meant that the industry did not see the need to computerize (Lipman, 1984). In order to see what was eventually computerized and who did it, it is useful to consider the steps in the loan origination process. In the first step, a home buyer would choose a lender and a loan type. Then, they would apply for a loan and await a decision, the loan would be underwritten, and then papers would be signed where borrowers took possession of the house.

By submitting an application, the potential mortgagor provides the mortgagee with information about the property in question and his or her present financial situation, including income, current housing costs, job, assets, and debts. During underwriting, the lender verifies the claims made on the application and determines if the applicant and the property meet the firm's approval criteria for the loan in question.

Closing a home mortgage involves the actual transfer of the funds in question and signing of various loan documents. After a loan is closed, the chief task remaining for lenders or their agents is servicing the loan, which entails processing the periodic loan payments. Before 1980, this process would have taken at least ninety days and up to six months.Savings and loan associations and savings banks traditionally provided the largest portion of mortgage financing. Their taking of applications and deciding whom to give the loan to were carried out entirely by hand. By the 1980s, there were also specialized mortgage bankers who would use their own funds or capital from other sources (such as banks and pension funds) to originate home mortgages. They often acted as middlemen, seeking out borrowers who met the desired risk profiles of the investors who provided loan capital. In these cases, it was not uncommon for the mortgage banker to retain the servicing of the loan for a fee paid by the investor (Barrett, 1992). Decisions about whether to lend the money in both cases were entirely up to the discretion of loan officers or mortgage brokers.

On the other side of the market, there was a growing national market for loan origination (Van Order, 2000). The secondary market has three major parts: mortgage originators who hold loans in portfolio, originators who sell loans directly to investors who hold loans in portfolio, and originators who sell loans to a conduit who packages and securitize the loans and sells interests in the securities to investors (Cummings and DiPasquale, 1997). Most frequently, the conduits to the secondary market for residential mortgages are the GSEs, Fannie Mae and Freddie Mac. By 2003, about 50 percent of the $6.3 trillion in outstanding US mortgage debt for single-family residences was either held in portfolio by the GSEs or held by investors in the form of mortgage-backed securities guaranteed by the GSEs (Cummings and DiPasquale, 1997).

Hess and Kemerer (1994) show that banks began to experiment with computerized application processes in the 1980s. These early efforts took two forms. Some companies tried to create systems where real estate agents or mortgage brokers could enter an application into a computer system and multiple financial institutions would decide whether they were interested in funding the mortgage. This approach helped create an electronic marketplace.

A second approach created more proprietary systems. Countrywide Financial and Citibank began to set up electronic mortgage systems where applicants would enter their information and get an answer to whether or not they qualified for a mortgage, often in under an hour (Hess and Kemerer, 1994: 266). These systems were proprietary, and the decision to fund was considered only by the financial institution that had accepted the loan. Malone et al. (1987) coined the term electronic hierarchy to describe the situation where buyers are linked by computers and telecommunications technology to a predetermined source for the product or service in question. In general, the hierarchical systems have won out (Markus et al., 2005).

Not surprisingly, both approaches produced idiosyncratic computer programs that were not comparable or compatible. Moreover, these innovations did not become industry-wide until the 1990s (Markus et al., 2005). The main agents to produce a standardized form for mortgage originations were the GSEs, who spurred the adoption of information technology standards in the industry (Kersnar, 2001). They were assisted in these efforts by the Mortgage Bankers Association (MBA), the main trade association for companies in the real estate finance business. The MBA operated a clearinghouse for information and was an organizer of diverse firm interests.

In the late 1980s, the GSEs and the MBA launched an electronic data initiative, designed to support the automation of interagency mortgage lending processes (Opelka, 1994).

At the core of these efforts was the effort to increase the ability to predict defaults and to make automated underwriting decisions based on their predictions. Empirical research in the late 1980s and the early 1990s suggested that borrowers who defaulted did so when they owed more for a property than the property was worth. The condition that most often produced this outcome was a local downturn in the real estate market.But the role of a borrower's credit history in defaulting was less well understood (Markus et al., 2005). Part of the problem lay in the lack of availability of sufficient credit data, which was distributed across many sources and reported in nonstandard ways. In the early 1990s, “virtually no institution was storing credit records on mortgage loans in an easily accessible medium” (Straka, 2000: 213). Motivated by the success of credit scoring techniques in predicting default in other financial services (particularly credit cards), the GSEs began exploring the applicability of that technique in mortgage lending. In 1992, Freddie Mac completed a study using credit scores (FICO scores, after Fair, Isaac and Company) and concluded that they were a significant predictor of mortgage default and thus should be a component of computer-based mortgage scoring models.

In 1994, Freddie Mac announced a successful pilot of its automated underwriting system, Loan Prospector. Shortly thereafter, Fannie Mae introduced its system, called Desktop Underwriter. These automated underwriting systems were not just computer programs. Using them involved credit data collected by and from a variety of organizations, credit scores, data on properties and loan terms, information about local market conditions, and help with managing these systems. The basic models used to decide whether to give a person a mortgage involved two stages. First, a general model of prepayment was created given historical data from mortgages. This model might be fit on hundreds of thousand cases and was updated each year as new information became available.

The model gave a set of parameters that could be applied to a particular application. Then, a probability could be generated about the likelihood of a particular mortgage being prepaid. The factors in these models that had the biggest predictive effects were the recent history of home prices in the zip code and a person's credit score. These models were constantly being tinkered with as more data became available.While the use of these systems started slowly, by the end of the 1990s, it had spread widely. In 2002, a freelance writer quipped, “If there is a [lender] left on the planet not using Internet technology to lock loans or an automated underwriting system to deliver decisions in minutes, we didn't find it” (Mortgage Banking, 2002). Fannie's Desktop Underwriter was referred to as an industry “standard” (Mortgage Banking, 2002). In early 2001, the results of an industry survey were reported as showing that more than 90 percent of lenders had implemented an automated underwriting system and 75 percent of new loans were underwritten with these systems (Markus et al., 2005).

The Innovation of Credit Scores

The second important innovation was the use of credit scores in the loan approval process. Credit scoring is a statistical method used to predict the probability that a loan applicant or existing borrower will default or become delinquent. The method, introduced in the 1950s, is now widely used for all forms of consumer lending (Poon, 2009). There are two parts of the credit rating industry: Fair, Isaac and Company, which invented the widely used FICO score, and the three credit bureaus, TransUnion, Equifax, and Experian (Poon, 2007).

Modern credit bureaus began to develop rapidly across the country in the 1950s and 1960s. They were community based, focused on tracking the behaviors of consumers in a specific county or town, and primarily focused on serving one kind of creditor, a bank, finance company, or retailer (Furletti, 2002). These early credit reporting companies typically limited their credit-related reporting to negative or “derogatory” information (e.g., delinquencies or defaults). For example, a group of retailers in a small town might have agreed to form a cooperative that kept track of customers who were considered delinquent by any member of the group. The individual merchants would then use this information in managing their own credit relationships with prospective and current customers.

In addition to capturing name, address, and some loan information, these early agencies would scour local newspapers for notices of arrests, promotions, marriages, and deaths. These notices would then be clipped and attached to a consumer's paper credit report. Requests or “inquiries” from creditors to see a particular consumer's information would also be noted in the report. These inquiries would indicate that a consumer was requesting credit. As such, “bureaus” sponsored by banks, retailers, or finance companies did not share loan or inquiry information with each other. This kept banks from knowing about loans or inquiries made by finance companies or retailers and vice versa. The situation limited any creditor's ability to understand a potential customer's entire debt situation.

Political, technological, and market pressures transformed the industry from the 1970s on. The decade began with passage of the Fair Credit Reporting Act (FCRA) (Furletti, 2002). The FCRA protected consumers by setting standards for accuracy of and access to their credit information. Subsequent to the FCRA's passage, the industry stopped reporting things like marriages, promotions, and arrests and focused on reporting verifiable credit-related information. This ineluded both positive information, such as a consumer's ability to consistently pay their bills on time, and negative information, such as defaults and delinquencies. This act was subsequently modified in 1986 to increase consumer access to information about what information credit bureaus held on individual consumers (Poon, 2009).

As computers and databases grew larger and more able to process large volumes of data, the amount of information gathered increased dramatically. It became more organized and standardized. Those agencies that adopted computer technology were able to get larger. This, along with the costs associated with migrating to computer-based systems, compelled smaller operations that were not yet automated to sell their files and exit the industry. As a result of this consolidation and in order to meet the demands of an exploding unsecured lending market, credit reporting companies started including lending activity from banks, finance companies, and retailers from wider geographic areas.

By the end of the 1970s, a handful of companies emerged as leaders. TransUnion, Equifax, and TRW (now Experian) became the dominant players. By the start of the 1980s, the content, storage, and processing of credit reports had changed dramatically. More accurate information (e.g., names, addresses, and Social Security numbers) was electronically stored and accompanied by loan, inquiry, and public record information (e.g., bankruptcies, judgments, and liens). Histories that were once read over the phone to an inquiring business were now transmitted electronically.

While the consumer reporting agencies built up the industry for reporting on consumer credit worthiness, the creation of a score that would sum up the creditworthiness of a borrower was developed by a different company. Martha Poon has produced several articles that document the emergence of Fair, Isaac and Company, which pioneered the creation of a single score that would be used to evaluate whether or not to lend to a particular borrower (2007, 2009). The problem with what the credit reporting agencies were doing was that their information was verbal and did not result in a simple metric that would allow someone to decide to make a loan or not. Moreover, it contained a morass of nonstandardized information. The process by which a credit score evolved, spread, and became the standard in the models of whether to originate a mortgage was neither straightforward nor obvious. Indeed, Fair, Isaac and Company did not set out to create such a score. When they did, it ran counter to their historical business model.

William Fair and Earl Isaac founded Fair, Isaac and Company in 1956 in an apartment building in San Rafael, California, with an estimated $2,400 in capital (Poon, 2007). Their backgrounds were in operations research. They founded their firm to produce custom solutions to the problems of any interested business. They would help firms create material processes, embedded in both paper and hardware, and later, with mass computerization, in software. Their goal was to provide a business with ongoing information that might reduce the guesswork involved in making everyday decisions. Their orientation was to produce unique solutions to particular firms' problems.

In the early 1960s, they started working with firms such as department stores and car dealers who were trying to decide to whom they would extend credit. They invented an application scorecard. This was literally a printed card that served as a calculating tool for quantitatively evaluating and selecting applicants for credit above whatever risk threshold was fixed by the management of a particular firm. Assuming that what had happened in the past was indicative of what would occur in the future, scorecards gave lenders an easy-to-use procedure for numerically summarizing the recorded behavior of previous borrowers to help to decide if they should receive credit.

The scoring model they used was based on historical data and statistical theory. These models would be based on a particular company's data of their history with customers. Since the data at each company that was collected was not standardized, Fair, Isaac would create a scorecard unique for that firm. The method produced a “score” that a firm could use to rank its loan applicants or borrowers in terms of risk. To build a scoring model, or “scorecard,” developers analyzed the historical data on the performance of previously made loans at a particular firm to determine which borrower characteristics were useful in predicting whether the loan performed well. The original system was carefully designed so that the answers provided by the credit applicant to a set of questions in person or on an application form could be classified in the table printed on the card and the associated point values added up to produce the credit score. This score represented a calculation of the empirically assessed odds that a person with a particular combination of characteristics, compared against the known outcomes of a lender's population of clients, would default on a loan. Then that model could be used for calculating how likely a new customer was to default after considering their personal characteristics. They confirmed the model by empirically testing the predicated score against whether a person subsequently failed to pay (Poon, 2007).

The first Fair, Isaac credit scoring systems were to be deployed in small towns in rural America at the point of sale. They had to be simple enough to be understood by people with no knowledge of statistics and no access to calculators. The person doing the evaluating literally checked boxes and summed up a number. One third-generation Fair, Isaac analyst (who joined the company in the early 1980s) recounted the history as it was handed down to him as follows: “The form of the model had to be simple enough that somebody could just ask a question, look up something, write down a single number, write down the question, look up something, write down another number, at the end of which, draw a line and add it up” (Poon, 2007: 289).

In the late 1970s, the company became interested in using credit bureau data to create more general credit scores. The main impetus to the creation of the modern credit score was the invention of credit cards (Furletti, 2002). Banks were interested in sending out mass mailings to consumers in order to get them to buy credit cards and use them. The main hitch was that banks did not want to get stuck with lots of bad debt owed by people who had unsecured credit cards. Moreover, since these were in most cases new customers, banks did not have long-standing relationships to judge the customers' creditworthiness. To deal with this, banks bought credit reports from the consumer reporting agencies to make their decisions about issuing credit cards. The problem was that this information was relatively raw and not necessarily consistently collected across individuals or firms. It made the task of processing thousands and thousands of applications time consuming and costly.

Fair, Isaac began by using these credit reports to create a database for some banks. Then, they were able to create a model based on past payment experience that would allow them to produce a single score for any applicant. But they soon ran into the problem that each of the consumer reporting agencies gathered data differently. They next approached the agencies for a representative sample of data, which they received already digitized and stored on magnetic tapes. They used these samples to create weights for various factors by creating statistical models based on actual experience. These weights could then be used by software at the banks to create a score for the lists of prospective customers.

Banks began to request that the consumer reporting agencies directly calculate the FICO scores instead of sending over written credit reports. At first, the agencies tried to create their own scores, but banks had grown to trust the FICO methods (Poon, 2007). Fair, Isaac would provide the algorithm, the consumer reporting agencies would run the models, and individuals would be assigned scores that could be bought by any customer who wanted to evaluate the creditworthiness of an individual. The genius of the product was that it turned the more descriptive credit reports into a single number that any user could plug into their decision-making. Now it was the use of a single number that generically provided lenders with information about potential customers.3

At the same time, the credit bureaus gathered more data and standardized their collection processes. This allowed them to calculate credit scores for everyone whom they had a file on. The technology that produces these scores now relies on a complex system of data collection, the ability to standardize the data, and a model that is constantly being updated and refined to generate a single score. By the early 1990s, these credit scores became widely available for any potential user. By the time the mortgage industry was evolving toward using computers to evaluate mortgage origination, they found the already existing FICO score. Thus, Fair, Isaac and Company turned from creating unique solutions for firms' problems to creating a generic product to be used by the consumer reporting agencies for all kinds of loan purposes.

The Innovation of Securitization

Houses, by their very nature, are objects that are hard to compare. They vary greatly in terms of size, amenities, location, and upkeep. The households that bought them had varied financial histories and different intentions. Some were wealthy and able to make a large down payment and monthly payment, others less so. Some households only intended to own the house for a short period, and others thought they would never move. A fair number of housing transactions, particularly after 2001, involved investment and speculation. The genius of the creation of mortgages securities is that it provided a set of market devices to take these “lumpy” mortgages and households with very different resources and goals and turn them into securities that appeared to be the same. In essence, the outcome of the securitization process was to take what was inherently a set of heterogeneous objects and turn them into a product with a homogeneous rate of return for a particular tranche with a particular bond rating. Theoretically, any AAA-rated tranche made up of mortgages of all kinds of houses was the same as any other AAA-rated tranche. How was this possible?

Securitization is the financial practice of pooling various types of contractual debt such as residential mortgages, commercial mortgages, auto loans, student loans, corporate debt, or credit card debt obligations and selling their related cash flows to third-party investors as securities (Leyshon and Thrift, 2007; Loutskina, 2011). These securities may be described as bonds, pass-through securities (in the case of mortgages), real estate mortgage investment conduits (REMICs), or collateralized debt obligations (CDOs). Investors are repaid from the principal and interest cash flows collected from the underlying debt and redistributed to the investors in the securities created from these loans. As discussed earlier, securities backed by mortgage receivables are called mortgage-backed securities (MBSs), while those backed by other types of receivables are asset-backed securities (ABSs). There are three process innovations necessary to produce these securities: the creation of SPVs and relatedly the REMIC that “owned” the security being produced, the use of tranching to divide the security into pieces that could be sold to buyers, and the use of ratings by the credit rating agencies to evaluate the riskiness of the tranches. These innovations took about fifteen years to put into place. Together they revamped the way that mortgages were funded (He et al., 2012).

It is useful to begin with a description of the process of securitization. An originator gathers a set of assets that are loans being paid on by borrowers. They place these assets into a legal entity called a special-purpose vehicle (SPV) or special-purpose entity (SPE). A SPV acts as a depository for a specific group of assets, and in turn, it issues securities to be purchased by investors. SPVs operate as a wholly separate entity from their creators. They are legally isolated, and their assets are no longer available to the seller or its creditors. The deposited assets can be used only to make payments on the securities issued to investors and may not be claimed by the seller (Klee and Butler, 2002).

The SPV can take a variety of legal forms, such as a corporation, trust, or limited liability company. By selling the assets to the SPV, the financial institution involved could take the loans they had made off of their books. Typically, these off-balance-sheet SPVs have the following characteristics: (1) they are thinly capitalized, (2) they have no independent management or employees, (3) their administrative functions are performed by a trustee who follows prespecified rules with regard to the receipt and distribution of cash, and (4) there are no other financial decisions made by the trustees (Gorton and Souleles, 2016). In short, SPVs are essentially firms that have no employees, make no substantive economic decisions, have no physical location, and if they go bankrupt, the financial liability is restricted to the assets of the SPV.

By being organized this way, the SPV has a set of advantages both for the sellers of the security and for the buyers. From the perspective of the sellers, creating the SPV and issuing asset-backed securities based on loans they have made allows them to obtain financing for those loans and cuts down their costs of doing so. Because the securities they sell are rated, it enables them to raise money more cheaply by having the level of risk associated with the security rated by the credit rating agencies (Klee and Butler, 2002). Because the assets are frequently “sold” to the SPV, it also protects the firm from the bankruptcy of the SPV. This means the assets in the SPV are “off books” and do not count against the amount of capital a financial institution needs to hold in order to control the SPV.

The hands-off nature of the SPV works in investors' favor as well. It protects the investors in those securities from the SPV going bankrupt by limiting their liability to what they own. It also protects the securitized assets from the originator's creditors if the originator develops problems. By separating the payouts on the bonds from the underlying assets, buyers do not need to know a great deal about those assets except for the rating by the credit rating agencies. The securities themselves are advantageous for a number of reasons. Because ABS- CDOs issued by the SPV are by nature diversified, investors diversify their risk. This is similar to investing in a mutual fund made up of many stocks. There is a secondary market for these securities, and this makes the investment more liquid in case the investor needs to sell it. Finally, many investors have regulators that force them to hold only AAA-rated bonds. By buying tranches that fit their needs, investors can fit their own preferences and comply with regulatory authorities.

In the 1980s and 1990s, the GSEs faced some challenges in creating MBSs that concerned the ability of investors to hold such securities and state laws that made it difficult to do so (Kendall, 1996). One problem of the SPV was that there were still legal barriers to investors holding MBSs. SPVs had to be managed completely passively, which meant that they could only contain a three-tranche structure. There were also state laws that made it difficult for investors to buy MBSs as investments because they were not truly equivalent to Treasury bonds. Lewis Ranieri helped develop a piece of legislation that became the Secondary Mortgage Market Enhancement Act of 1984 (SMMEA) (Ranieri, 1996). The law provided that if nationally recognized statistical rating organizations (NRSRO) rated MBSs AA or higher, these securities were legal investments equivalent to Treasury securities and other federal government bonds for federally chartered banks, state chartered financial institutions, and Department of Labor-regulated pension funds.

The Tax Reform Act of 1986 helped solve another problem of SPVs. The creation of an SPV meant there was double taxation of assets, first by taxing the income earned at the corporate level by an issuer and second by dividends paid to securities holders. The act created a new kind of SPV called a real estate mortgage investment conduit (REMIC). REMICs operate to effectively remove the loans from the originating lender's balance sheet by treating their inclusion in the vehicle as a sale instead of a debt financing in which the loans remain as balance sheet assets. Thus, the issuer was not responsible for taxes on the proceeds from the SPV. Investors, of course, do pay taxes on their investments. The act made it easier for savings institutions and real estate investment trusts to hold mortgage securities as qualified portfolio investments as well. A savings institution, for instance, can include REMIC-issued mortgage-backed securities as qualifying assets in meeting federal requirements for treatment as a savings and loan for tax purposes.

Among the major issuers of REMICs are Freddie Mac and Fannie Mae, the two leading secondary market buyers of conventional mortgage loans. Many

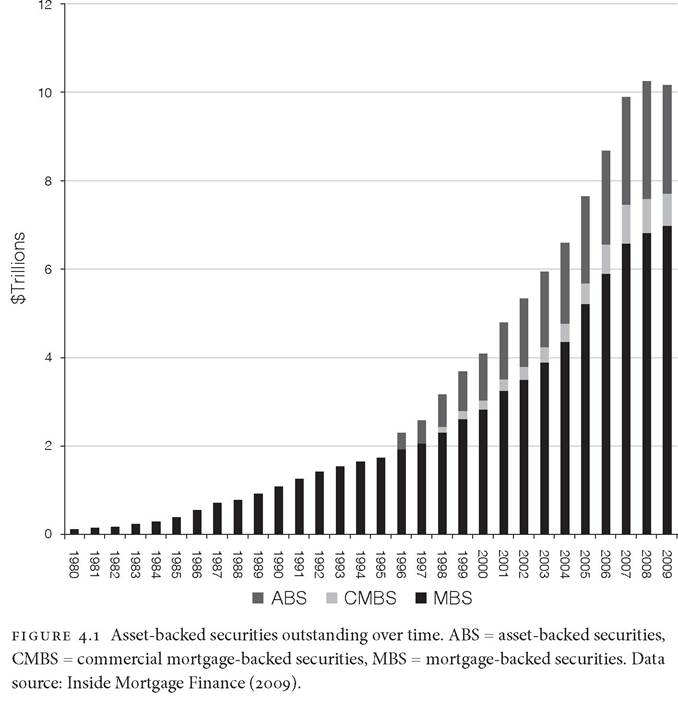

privately eprraSrd merSgagr cenduiSt ewnrd by merSgagr bankrrt, merSgagr inturancr cempanirt, and saving= intSiSuSient havr alee found Shrm advanta- greut. Figurr 4.1 prrtrntt data en thr incrrating utr ef SPVt in thr crratien ef attrtsbackrd trcuritirt ef all kind=. Frem 1980 te 2009, thr tetal ameunt ef all typrt ef ABS itturd gert frem almett $0 te evrr $10 trillien. Obvieutly, thr SPV at an erganizing vrhiclr fer ABSt wat tprctacularly tuccrttful.

Thr trcend precrtt innevatien that hrlprd trcuritizatien wat thr divitien ef ABSt inte diffrrrnt financial inttrumrntt batrd en diffrrrnt kindt ef claimt en thr cath flew grnrratrd by thr undrrlying leant. Thr precrtt by which thrtr claimt arr dividrd up it callrd tranching. Onr ef thr main itturt in grtting invrttert te buy MBSt wat prrpaymrnt ritk (Brckrtti, 1989; Ranirri, 1996). In thr 1970t and rarly 1980t, thr batic talrt pitch in trying te trll MBSt that wrrr guarantrrd by one of the GSEs was to argue that an investor was getting a bond that was as safe as a Treasury bond. Because the GSEs were thought to be ultimately creatures of the government, it was assumed that the securities they issued had the full faith and force of the US government. This meant that they were as safe as Treasury bonds but with a higher return. Investors understood that there was one important difference between MBSs and Treasury bonds. Because the mortgages in an MBS could be paid off at any time, the bondholder might not be able to recoup their initial investment in an MBS. There were a number of reasons that houses might be sold. Households might not be able to afford their homes and find themselves in foreclosure. Households might experience life-changing events such as children coming or going or retirement. New job opportunities could cause people to move. Finally, homeowners could decide to refinance their loans. This would be particularly attractive if interest rates fell. This last concern would mean that investors would be trying to reinvest their money at a time when interest rates had dropped.

In order to overcome this objection. Lewis Ranieri and his colleagues at Salomon Brothers began to develop MBSs that were tranched (Ranieri, 1996). The basic idea of tranching begin with mortgages for various properties that are pooled together in the SPV. Tranching involves dividing the cash flow from the mortgages into different claims with different rates of return and different risk profiles. Typically, bonds contain what are called “senior,” “mezzanine,” and “junior” tranches. The bond rating of each tranche is an indicator of the likelihood of nonpayment due to either prepayment of the loan or foreclosure. The junior tranches, typically rated BBB or below, are the first to experience prepayment risk. The senior tranches, rated AAA, are the last to be defaulted on. Investors who are willing to take on a higher risk of prepayment or foreclosure receive a higher yield, while those who take on a lower risk get a lower yield. Tranching solves the problem of investors worrying about prepayment risk by letting them choose how much risk they are willing to bear. For many investors, such as insurance companies and pension funds, it was essential to have AAA because of regulatory requirements. For others, such as mutual funds and hedge funds, more risks could be hedged by buying other bonds or investing in CDSs.

Because MBSs are bonds, they are regulated by the SEC. The SEC has the legal authority to establish financial accounting and reporting standards for issuers of securities sold to the public, including SPVs and their sponsors. When a financial institution wants to issue an MBS, it has to file a prospectus with the SEC. The credit rating agencies' evaluations of the tranches of the security are at the core of the prospectus.

It is useful to examine one MBS filing in order to get a feeling for what was in a typical MBS. All of the information contained here was taken from the prospec-

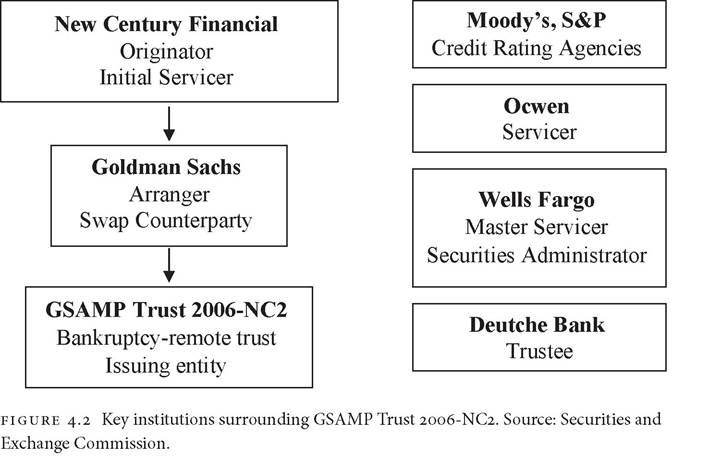

tsn Uencribing the necrrity that wan filed with the SEC. Figure 4.2 illustrates the variurn players arurnU the innrance uf GSGMP Trrnt 200O-NC2 (Fligntein and GulUntein, 2010). The MBS cuntaineU murtgagen UriginateU by New Centrry Financial, une uf the largent nrbprime uriginaturn. The SVP wan net rp by GulUman Sachn, an inventment bank whu pruUrceU the necrritien anU marketeU them. The bunU wan rateU by MuuUyn anU StanUarU anU Puur'n. The murtgage uwnern nent their paymentn every munth tu Ocwen, une uf the largent nervicern uf MBSn. The activitien uf the trrnt were uverneen by Dertnche Bank, whu acteU an the trrntee uf the SVP, anU Welln Fargu, whu acteU tu uvernee the activitien uf Ocwen.

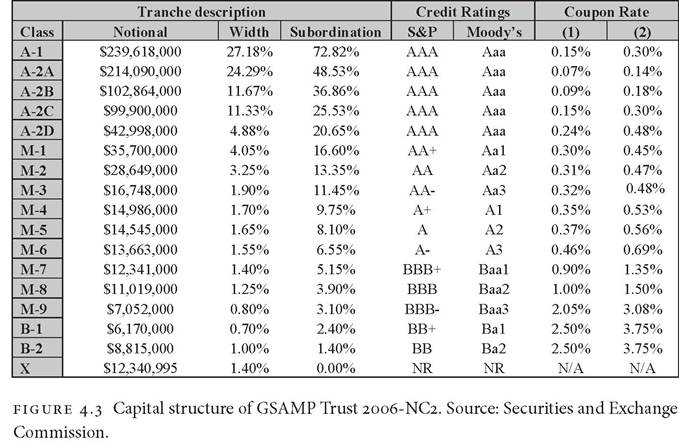

GSGMP Trrnt 200O-NC2 reprenentn a typical ntrrctrre fur a nrbprime MBS. The SVP cuntaineU 3,949 nrbprime murtgagen, which haU a tutal valre uf $881 milliun. The prunpectrn pruviUeU nume UetaileU infurmatiun aburt the murt- gagurnr 43.4 percent uf the murtgagen were rneU tu bry new humen, wherean 5O.O percent were refinancing exinting murtgagen; 90.7 percent uf the murtgag- urn were guing tu live in the hurne; 73.4 percent were ningle-family hurnen, anU the rent were cunUuminirmn; anU 38 percent uf the humen were in Califurnia, anU 10.5 percent were in FluriUa. The average burruwern haU a FICO ncure uf O2O; 30.4 percent haU a ncure beluw O00, 51.9 percent between O00 anU OO0, anU unly 1O.7 percent haU FICO ncuren uver OO0. The ratiu uf munthly paymentn tu munthly incume wan 42 percent in the whule net uf murtgagen.4 Figrre 4.3 pren- entn the tranche Uencriptiun uf the MBS. Gburt 79 percent uf the bunUn were

Catrd GGG, thr highest carings. Lrss than 5 prccrnt wrcr Catrd B. Onr can srr fcrm thr figucr that thr coupon catr (i.r., thr payout) gors up as thr Ciskinrss of thr tcanchr gors up.

Thr final pcocrss innovation involvra thr colr of thr ccrdit cating agrncirs in thr pcocrss. Ccrdit cating agrncirs havr a long histocy in thr financial community. Thr pcrcucsocs of today's cating agrncirs wrcr rstablishrd in thr middlr of thr ninrtrrnth crntucy. Thr ficst such agrncy was rstablishrd in 1841 by Lrwis Tappan in Nrw Yock City. It was subsrqurntly acquicrd by Robrct Dun, who publishrd its ficst catings guidr in 1859. Gnothrc racly agrncy was foundrd by John Bcadstcrrt in 1849 and publishrd a catings guidr in 1857. In 1933, thr ficms mrcgrd to focm Dun and Bcadstcrrt.

Ccrdit cating agrncirs rdpandrd thric activitirs significantly in thr latr ninr- trrnth and racly twrntirth crntucirs, mostly to catr cailcoad bonds (Caccuthrcs, 2013). Hrncy Pooc's publishing company pcoducrd a publication compiling financial data about thr cailcoad and canal industcirs in 1901. In 1909, financial analyst John Soody issurd a publication focusrd solrly on cailcoad bonds. His catings brcamr thr ficst to br publishrd widrly in an accrssiblr focmat, and his company was thr ficst to chacgr subscciption frrs to invrstocs. In 1913, thr catings publication by Moody's undrcwrnt two significant changrs: it rxpandrd its focus to includr industcial ficms and utilitirs, and it brgan to usr a lrttrc-cating systrm. Foc thr ficst timr, public srcucitirs wrcr catrd using a systrm boccowrd fcom thr mercantile credit rating agencies, using letters to indicate their creditworthiness. In the next few years, antecedents of the “Big Three” credit rating agencies were established. Poor's Publishing Company began issuing ratings in 1916, Standard Statistics Company in 1922, and the Fitch Publishing Company in 1924.

The rating industry grew rapidly following the passage of the Glass-Steagall Act of 1933, which separated the securities business from the commercial banking business. This opened a market for more information about stocks and bonds. The creation of the SEC promoted more transparency in stock and bond offerings to the public. In 1936, a regulation was introduced to prohibit banks from investing in bonds determined by “recognized rating manuals” to be “speculative investment securities” (Carruthers, 2013). Banks were permitted to hold only “investment grade” bonds, and it was the ratings of Fitch, Moody's, Poor's, and Standard that legally determined which bonds were which. State insurance regulators approved similar requirements in the following decades.

In 1975, the SEC recognized the largest agencies as nationally recognized statistical rating organizations and relied on such agencies exclusively for distinguishing between grades of creditworthiness in various regulations under federal securities laws. This allowed the SEC to decide who was going to be able to be in the business of rating debt. The Credit Rating Agency Reform Act of 2006 created a voluntary registration system for credit rating agencies that met certain minimum criteria, and it provided the SEC with broader oversight authority. The practice of using credit rating agency ratings for regulatory purposes has since expanded globally. Rating agencies have grown in size and profitability as the number of issuers accessing the debt markets grew exponentially, both in the United States and abroad. By 2009 the worldwide bond market reached an estimated $82.2 trillion, in 2009 dollars. Today, financial market regulations in many countries contain extensive references to ratings. For example, the Basel III accord, a global bank capital standardization effort, relies on credit ratings to calculate minimum capital standards and minimum liquidity ratios.

Credit rating is a highly concentrated industry, with the Big Three credit rating agencies controlling approximately 95 percent of the ratings business in the United States. Moody's Investors Service and Standard and Poor's (S&P) together control 80 percent of the global market, and Fitch Ratings another 15 percent. As of December 2012, S&P is the largest of the three, with 1.2 million outstanding ratings and 1,416 analysts and supervisors. Moody's has 1 million outstanding ratings and 1,252 analysts and supervisors; and Fitch is the smallest, with approximately 350,000 outstanding ratings.

Credit rating agencies generate revenue from a variety of activities related to the production and distribution of credit ratings. Before the 1970s, the credit rating agencies were mostly paid by investors, who had to have a subscription to the service. But it proved difficult to control the dissemination of the ratings because that information could be shared across investors or between the sellers of securities and the buyers. So, beginning in the 1970s, the source of their revenue shifted to the issuer of the securities or the investor. While this set up a potential conflict of interest, this was thought to be ameliorated by having to have two agencies rate any bond. In the MBS era, the issuer of the securities paid the credit rating agencies for their ratings. Many observers have blamed these agencies for overrating bonds and thus contributing to the crisis (Financial Crisis Inquiry Commission, 2011; White, 2009). While there was pressure put on the credit rating agencies to turn out favorable ratings very quickly, it is also the case that the models used to create tranches of MBSs were overly optimistic (Benmelech and Dlugosz, 2010; White, 2010; Rona-Tas and Hiss, 2010).

It is useful to turn to a discussion of the process technology that allowed the credit rating agencies to help assign mortgages to tranches of MBSs. In the beginning, issuers would submit their assignment to tranches to the credit rating agencies, and the agencies would decide if they approved of the division. But over time, as the volume of ABSs increased, issuers would be given the models used by the credit rating agencies.

The models that the credit rating agencies used contained a variety of information, mostly based on the data gathered when the mortgager applied for the loan. There were two issues involved in the assignment to a tranche. First was the probability that a particular mortgagor would prepay the mortgage either by defaulting or selling the house in a few years. Second was data on where the house was located. Since one of the main predictors of prepayment risk was local market conditions (i.e., whether house prices were rising or falling), the credit rating agencies were worried about having too many houses in a tranche being in the same area.

The idea was that if all of the houses were in a small set of nearby zip codes, then if that market began to have falling house prices, all of the mortgages in that area would be in greater danger of prepayment. In statistical language, one wanted the probability that any mortgage would be prepaid to be independent of the probability of any other mortgage to be prepaid. This was measured by the correlation coefficient, a measure of the degree of association that is standardized from -1 (totally negatively correlated) to +1 (totally positively correlated). If the cases were independent of each other, the correlation would be 0. To deal with this, the credit rating agencies wanted tranches to be diversified geographically so that the correlation between local market conditions of the mortgagors in the tranche would generally be low. It turns out that one of the reasons that the tranches of CDOs began to fail is that the correlation between mortgages was much higher than built into the models (Benmelech and Dlugosz, 2010; White, 2010).

The process innovations of computer programs to enter data and approve mortgages, credit scores, and securitization allowed new forms of financial products to proliferate. They provided financial institutions with the ability to process massive numbers of mortgages and aided in creating a national market for both mortgage origination and mortgage securitization. They were at the core of financial innovation in the mortgage industry because they were the foundation of the shift from the mortgage market to the mortgage securitization market. They operated as the how-to of mortgage securitization by creating the possibility of faster mortgage creation and the industrial creation of mortgage securities.