ORIGIN OF THE TRADERS COLLECTIVE BEHAVIOUR STYLIZED FACTS

... it is important in agent based models not just to replicate features of real markets, but also to show which aspects of the model may have lead to them (LeBaron, p. 226).

In the previous section, we have seen that our model of FX market trading activity is able to generate some of the stylized facts of the FX market traders’ collective behaviour.

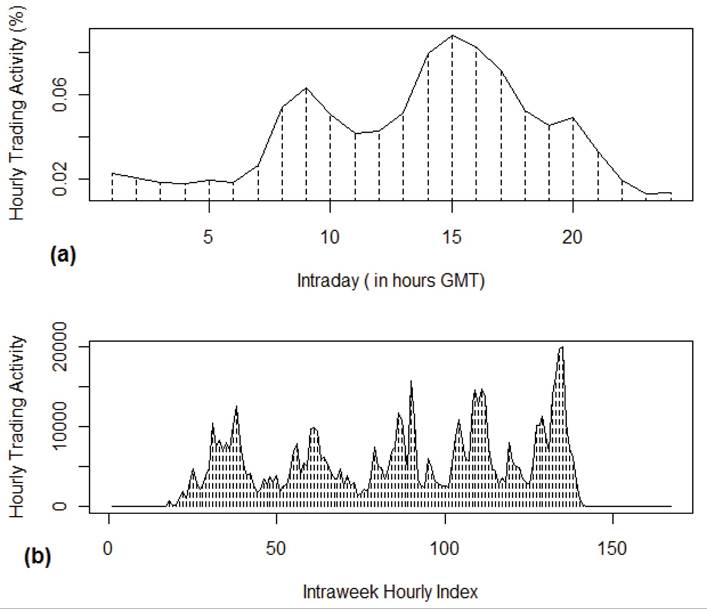

Nevertheless, in our model, the stylized facts were obtained from a combination of specific values of the model’s parameters. In this section, we want to modify some of the model’s parameters in a number of ways in order to understand the nature and origin of FX market traders’ collective behaviour stylized facts. This can be address in a systematic way in order to understand how the stylized facts emerged.Figure 3. The intraday and intraweek seasonality of EUR/USD trading activity on January 2009from the simulation outcome

8.1. The Simplicity of the Model

With a complex model, it is a difficult task to search for conditions under which stylized facts emerge. The complexity of some models of financial markets prevents the developer from identifying the aspects of the model that account for the emergence of stylized facts. Accordingly, we attempt to offer a description of the parameters involved in the model as simply as possible that are capable of replicating the stylized facts of the collective FX market traders’ behaviour. This has an important consequence for investigating the origins of traders’ behaviour stylized facts by means of exploring each of the model’s parameters in isolation of the impact of the other parameters.

The simplicity of our model relies in two main aspects: the use of a simple market mechanism in which we used a currency pair (EUR/USD) of historical prices as a substitute for generating artificial prices from the model, and the simple representation of the trading agents.

The trading agents’ trading strategy is based on a zero-intelligent directional-change event trading strategy (DCT0) in which the trading agents respond by buying or selling to a periodic pattern in the price time series based on their expectations.8.2. Heterogeneity

One of the things that microeconomics teaches you is that individuals are not alike. There is heterogeneity, and probably the most important heterogeneity here is heterogeneity of expectations. Ifwe didn’t have heterogeneity, there would be no trade. But developing an analytic model with heterogeneous agents is difficult - Kenneth Arrow, The Changing Face of Economics, (p. 301).

The role of heterogeneity in modelling the activities of the financial market traders is imperative seeing that, in reality, there are a large number of traders who have different degrees of wealth, demands, aspirations, trading hours, trading strategies, etc. The heterogeneity without doubt affects and characterizes the flow of trading activity in the market. In our model, heterogeneity exists in four forms: (a) the different behavioural groups of zero-intelligence DCT0 traders, (b) within each group the trading agents are endowed with different amounts of cash (wealth), (c) the trading agents have different profit objectives and different risk appetites that lead to the existence of long and short term investors, and (d) the trading agents use different trading time windows that build a source of heterogeneity into the model, leading to the characterization of different trading activities.

8.3. Activation of the Initial Condition

The activation of the initial condition proved to be of vital important in replicating the collective behaviour of FX market traders. Since, if all traders initially start to be active in the market at the same time, this will result in an extremely high level of liquidity in the market at the beginning of the trading period, compared with the middle and the end of the trading period.

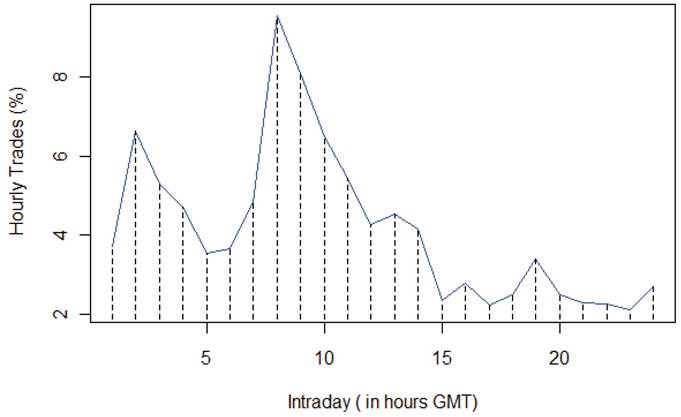

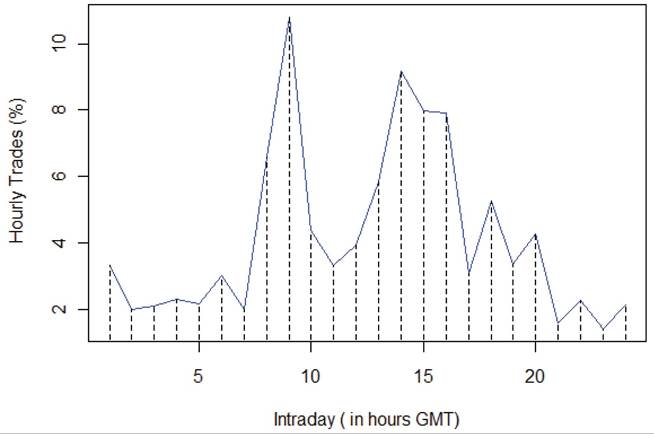

However, this is not the case in reality.To test the impact of the inclusion of the activation initial condition on replicating the intraday seasonality of FX market trading activity, we turn off the initial trading condition with regard to the model. Figure 4 shows the intraday seasonality of EUR/USD trading activity from the simulation outcome without the activation of the initial condition.

A simple inspection proves the lack of realism of the dynamics of intraday seasonality patterns for the following reasons:

Figure 4. Intraday seasonality of EUR/USD trading activity from the simulation outcome without the activation of the initial condition

• There are two trading activity peaks, which occur when the Tokyo and the Sydney trading sessions are open simultaneously. This is not the case for the seasonality of FX market trading activity, given that the first peak of trading activity occurs when the London trading session is operating, while the second peak takes place when the London and New York trading sessions overlap.

• The number of trading activity starts to drops sharply around 07:00 am (GMT time zone). This is when the European market opens. Additionally, the number of trading activity continues to decline through the day, even when the American markets open, and the European and American markets are open simultaneously between 01:00 pm to 04:00 pm GMT. In reality, the FX market witnesses a high number of trading activity when the European market operates, and then a much higher number of trading activity when the European and American markets are open simultaneously due to more traders participating in the market.

• There is no increase in the number of trading activity during the opening hours of the FX market trading sessions in contrast to reality when the number of trading activity increases throughout the opening hours of the FX market trading sessions.

We can conclude that such an initial activation condition represents an important element in replicating the collective behaviour of FX market traders. The initial activation condition is based on a small random probability. After a number of conducted experiments, we found that verifying the initial activation probability does not affect the accuracy of trading agents’ behaviour in terms of reproducing the FX market trading activity. However, we found that verifying the initial activation condition affects the trading number, in that using a high initial activation probability results in a highest number of trading activity, while a low probability results in a low number of trading activity. Cautiousness in choosing the appropriate value of initial activation probability is important.

8.4. Profit Objective

The right setting for the trading agents’ profit objectives is one of the most relevant factors responsible for replicating some of the stylized facts of collective behaviour of FX market traders. The choice of continuous uniform distribution for the traders’ profit objectives rather than other distribution methods was capable of replicating the different seasonalities of trading activity.

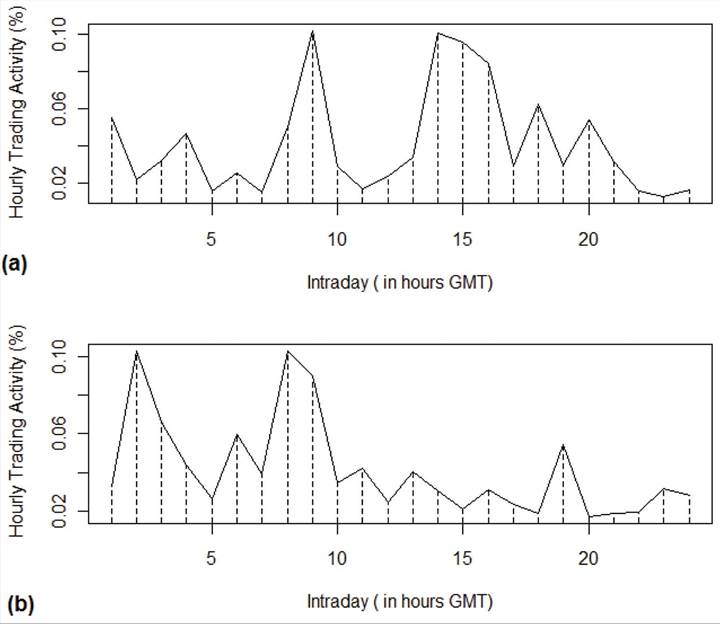

In order to test the impact of different distribution methods for the trading agents’ profit objectives on the intraday seasonality of FX market trading activity, we performed some experiments in which we used a power-law distribution or normal distribution instead of a continuous uniform distribution. Figure 5 shows the intraday seasonality of EUR/USD trading activity from the simulation outcome using normal distribution (a) and power-law distribution (b).

We can observe by a simple inspection that the dynamics of intraday seasonality are not realistic. In the case of a normal distribution (Figure 5a), we can spot that there is a sort of continuous fluctuation in the intraday seasonality of trading activity which is not the case in reality. In the case of the power-law distribution (Figure 5b), it is not possible to recognize the well-known double U- shape of FX market intraday seasonality of trading activity within the various patterns in the graph.

Verifying the scaling exponent for the power law distribution does not change the unrealistic results. However, due to space limitations, we will not report all these results.The power-law distribution and the normal distribution characterize unfairly distributed profit objective values that imply more values in terms of traders’ profit objectives than others. For in-

Figure 5. The intraday seasonality of EUR/USD trading activity from the simulation outcome using normal distribution (a) and power-law distribution (b)

stance, a power law distribution would assign high profit objectives to only a few traders, whereas low profit objectives apply to the majority. This results in a large group of traders having similar behaviour patterns and preferences, whereas in reality, traders have a variety of preferences and demands. For that reason, choosing a continuous uniform distribution is a good option seeing that it gives an equal distribution with a variety of profit objective values for the trading agents.

8.5. Risk Appetites

We observed from the microscopic analysis of OANDA individual traders’ historical transactions, the existence of high risk trading in the market in which traders’ risk appetite is higher than their profit objectives (as described in Section 6.1.3). Based on this observation, we defined the trading agents’ risk appetites to be four times their profit objectives.

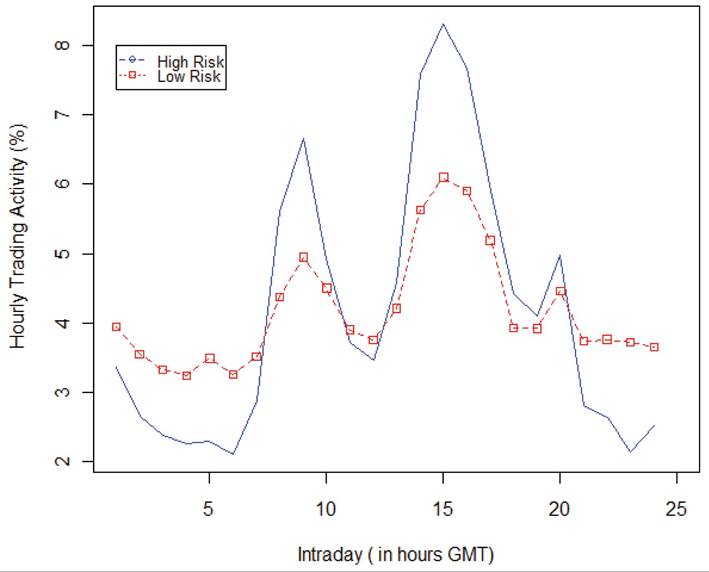

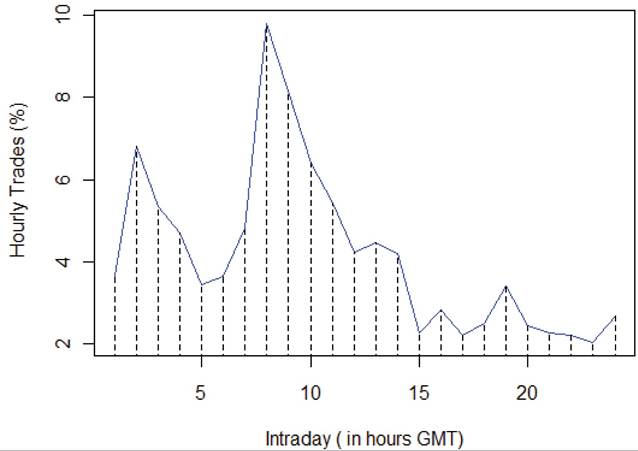

In order to test the impact of such a parameter on the seasonality dynamic of trading activity, we performed several experiments in which the trading agents’ trading strategy involved high risk or low risk. In Figure 6, we can see the intraday seasonality of EUR/USD trading activity from the simulation outcome with risk appetites equal to the traders’ profit objectives (low risk) and risk appetites four times the traders’ profit objectives (high risk). Due to space limitations, we will not report the results with all the other possible values oftraders’ risk appetites.

From the figure, we can see that when the trading agents’Figure 6. The intraday seasonality of EUR/USD trading activity from the simulation outcome with low and high trading risk

trading strategy involves high risk, the patterns of intraday seasonality of the FX market trading activity is precisely exhibited. Meanwhile, when the trading agents’ trading strategy involves low risk, the patterns of intraday seasonality moves within a narrow level of the resistance, whereas in reality it is wider.

8.6. Limit Orders

The generation of limit orders, profit-taking limit orders, and stop-loss limit orders during trading has an important effect on replicating some of the stylized facts of FX market traders’ collective behaviour. To test the impact of the inclusion of limit orders on the intraday seasonality of trading activity experimentally, we performed several experiments in which we had either profit-taking limit orders, or stop-loss limit orders, or none of them.

Figure 7 shows the intraday seasonality of EUR/USD trading activity from the simulation outcome without the two types of limit orders being generated. We can observe that the dynamic of intraday seasonality is not realistic for the following reasons:

• The intraday seasonality of trading activity has two peaks in which the first peak is higher than the second peak. The first peak of trading activity occurs when the European FX market trading sessions are open, while the second peak occurs when the European and American FX market sessions overlap. This is in extreme contrast to the dynamics of the intraday seasonality of trading activity in the FX market in which the second peak of the trading activity is higher than the first peak.

Figure 7. The intraday seasonality of EUR/USD trading activity from the simulation outcome without the two types of limit orders being generated

• There is some degree of continuous fluctuation at the end of the dynamic intraday seasonality of trading activity, which is not the case in terms of the FX market intraday seasonality of trading activity.

These unlikely results might be caused by the lack of a comprehensive trading strategy in which the trading agents must lock a certain profit realization, or seek to limit the potential loss for their open positions. What we can conclude from these results is that the two types of limit orders represent an important element in the generation of realistic FX market traders’ behaviour.

8.7. FX Market Trading Sessions and Market Holidays

Although the FX market operates 24 hours a day and does not imply a fixed trading time window, the number of trading activity increases during the opening time of the FX market trading sessions in the morning, while during the closing time of the FX market trading sessions, the number of trading activity falls. The overlapping business hours of two or more market sessions always witnesses a high number of trading activity compared to other trading hours. Additionally, the weekends in the FX market exhibit a low number of trading activity. These in turn shows the effectiveness of the FX market trading sessions and weekends with regard to trading behaviour.

At the beginning, we modelled the trading agents without incorporating the role of FX market trading sessions and holidays. The reason behind our decision is that algorithmic trading, also referred as automated trading, which uses computer programs to place orders automatically, has attracted many FX traders, and, most importantly, has a significant impact on the growth of the FX market. Evidently, our decision was not absolutely precise, seeing that some of the stylized facts of the FX market traders’ behaviour did not emerge in the stylized facts of the collective behaviour of our agent-based models of traders. Figure 8 represents the intraday seasonality of EUR/USD trading activity from the simulation outcome, without incorporating the role of FX market trading sessions.

Figure 8. The intraday seasonality of EUR/USD trading activity from the simulation outcome, without incorporating the role of FX market trading sessions

We can obviously spot that the intraday seasonality of FX market trading activity is not exhibited, in that it is impossible to spot the “double U-shape” that is reported in the literature. This is case for the following reasons:

• The highest number of trading activity takes place in the first hour of the day, as well as around 07:00 am GMT. Following this, the trading activity declines throughout the day, which is in contrast with the case in the FX market. The highest number of trading activity in the FX market takes place when the London and New York trading sessions overlap.

• During the business hours of the London and the New York trading sessions between 08:00 am - 09:00 pm GMT, there is a sharp drop in the number of trading activity, whereas in reality the FX market witnesses an increase in the number of trading activity during the opening hours of the London trading session, and a much greater rise in the number of trading activity within the opening hours of the New York sessions, in view of the fact that the London and the New York trading sessions overlap between 01:00 pm - 04:00 pm GMT.

8.8. Evaluation

One of the main constraints in modelling the market traders’ behaviour is the ability to verify if the stylized facts of real traders’ behaviour are exhibited. Fortunately, this study makes use of a unique high-frequency set of data of individual trader’s historical transactions at an account level. This has allowed us to define some stylized facts with regard to the collective behaviour of FX market traders. Using the identified stylized facts, we can evaluate precisely the accuracy of the agent-based models of traders in resembling the collective FX market traders’ behaviour. Most importantly, this allows us to experimentally trace under which conditions the stylized facts of the FX market collective traders’ behaviour are exhibited in our model.

9.