OXFORD'S PLANS GO ASTRAY

In contrast to the carefully controlled scheme by which employees of Wickes PLC artificially reduced the company’s expenses, an utter lack of controls was the source of a massive understatement of costs at Oxford Health Plans.

That difference mattered little to users of the companies’ financial reports, who were misled in both instances. In both cases, moreover, an astute reader of the income statements determined through simple ratio analysis that something was amiss.Stephen F. Wiggins started Oxford, a Connecticut-based health maintenance organization (HMO), in 1984 in a spare bedroom. By 1997, the company grew to 2.1 million members generating $4.1 billion of revenue. Investors benefited richly from the Oxford’s success. A $100 investment in the company’s 1991 initial public offering rose to $4,000 at the stock’s peak in July 1997.

Oxford’s data handling systems failed to keep up with the company’s explosive growth. The HMO had to track billing codes for hundreds of diagnoses, accounts for thousands of doctors, and personal data on members that numbered over one million by 1996. With claims beginning to back up, Oxford switched over to a new computer system created by its own people. Immediately, billing procedures began to misfire, data became corrupted through links between the old and new systems, and the claims-paying process broke down. The company temporarily ceased sending out monthly bills to many of its accounts, fearing that it might annoy them with incorrect statements. By the spring of 1997, uncollected premiums owed to Oxford had swollen to approximately 40 % of revenue, double the percentage of six months earlier.

These revenue problems and the resulting cash flow strains were compounded by a loss of control over costs.

As many as 30,000 customers had their medical care paid by Oxford despite having withdrawn from its plans or having refused to pay their premiums after months of receiving no bills. In 1997, Oxford’s health care cost per Medicare patient rose by 21%, about three times as much as the company had projected, while revenue per patient grew by only 4.3%. To make matters worse, the computer system breakdown prevented management from even becoming aware of the problem.17Complaints by physicians, who were irate over Oxford’s failure to pay its bills even as it was reporting robust profits, finally brought matters to a head. New York insurance regulators investigated the company’s finances and determined that its reserves for future medical claims were inadequate. On October 28, 1997, the state’s insurance commissioner told Oxford’s board of directors that the company would either have to adopt the corrective measures that he prescribed or stop enrolling new members and possibly even put itself up for sale. Seeing that the regulators were about to lower the boom, the company announced on October 27 that it would post its first loss ever in its third-quarter report. That day, the HMO’s stock plunged from $68¾ to $24¾. In the fourth quarter, Oxford reported a loss so large that it erased all profits reported since the company went public. On February 24, 1998, founder Stephen Wiggins resigned as chairman.

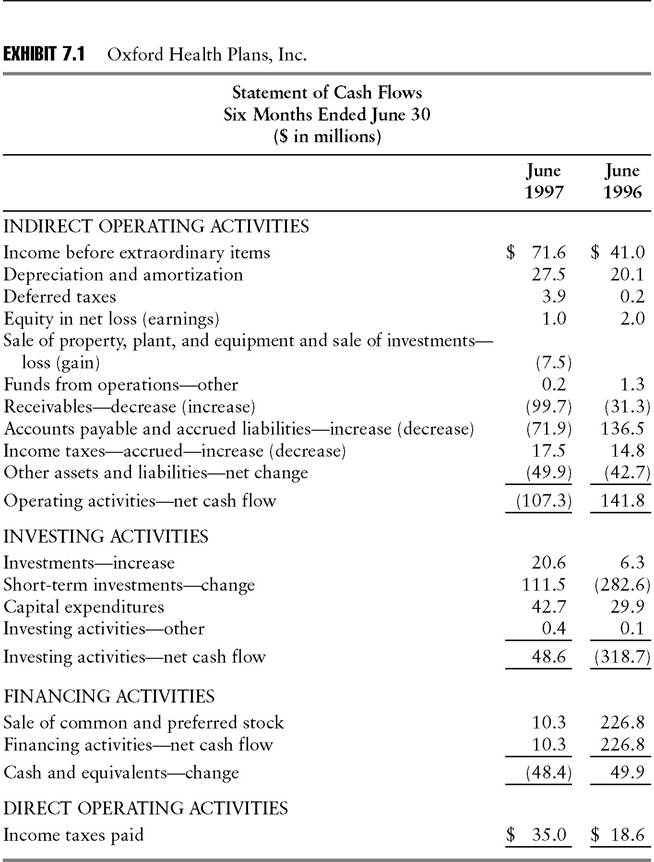

As in many other debacles involving expense recognition, rudimentary analysis of Oxford’s financial statements provided more than a hint of the trouble that lay ahead. Consider the Form 10-Q report for the quarter ended June 30, 1997, the last filed by the company before the October bloodbath. The statement of cash flows (Exhibit 7.1) displayed the classic problem that first gave rise to cash flow analysis (see Chapter 4). Even

Source: Compustat.

though net earnings for 1997,s first half rose by 74.6% over the comparable 1996 period, cash from operating activities deteriorated to -$107.3 million from $141.8 million.

The bulk of that adverse swing resulted from medical costs payable turning from a large cash source to a major cash use. As the notes to financial statements disclosed, Oxford advanced cash to the disgruntled physicians and hospitals while it tried to get its billing procedures back on track, deducting the amounts from the medical costs payable.Readers should not imagine that analysts identified these signs of trouble only in hindsight. Christopher Teeters, an analyst at the Center for Financial Research & Analysis, highlighted the divergence between earnings and cash flow in a report that he published ten days before Oxford’s October 1997 bombshell. “We had no idea it was as bad as it was,” Teeters acknowledged. “We just saw some indicators that looked kind of strange.”18 As far back as 1994, Anne Anderson of Atlantis Investment Company noted the haphazardness of Oxford’s membership reports. They were prone to restatement and in some cases contained handwritten changes.