Prospect Theory

Prospect theory was developed by Daniel Kahne- man and Amos Tversky in 1979. Starting from empirical evidence, it describes how individuals evaluate losses and gains. In the original formulation, the term prospect referred to a lottery.

Kahneman and Tversky developed this theory to remedy the descriptive failures of expected utility (EU) theories of decision making. Prospect theory attempts to describe decisions under uncertainty, and has also been applied to the field of social psychology.

Shiller refers to prospect theory as a mathematically-formulated alternative to the theory of expected utility maximization -- an alternative that is supposed to capture the results of such experimental research (Shiller, 1999, pp. 1308-1310).

Prospect theory is probably the most widely accepted behavioral theory and has the most impact on economic research. It is very influential despite the fact that it is viewed by many economists as less important than expected utility theory. Expected utility theory offers a restrained representation of rational behavior under uncertainty. It works well as a foundation for an economic theory based on the assumption of strictly rational behavior. However, it is known that in certain circumstances EU incorrectly predicts human behavior as it is shown in experimental evidence. Many theories are created to match this evidence, prospect theory being foremost among them. As mentioned at the beginning of this section, prospect theory was first developed by Daniel Kahneman and Amos Tver- sky in their milestone paper, “Prospect Theory: An Analysis of Decision under Risk” (1979). In prospect theory, Kahneman and Tversky formalized loss-averse behavior and other seeming anomalies as behavioral elements. They replaced the utility function with a valuation function that evaluates changes in expected income from the current level based on a current reference frame that conditions expectations.

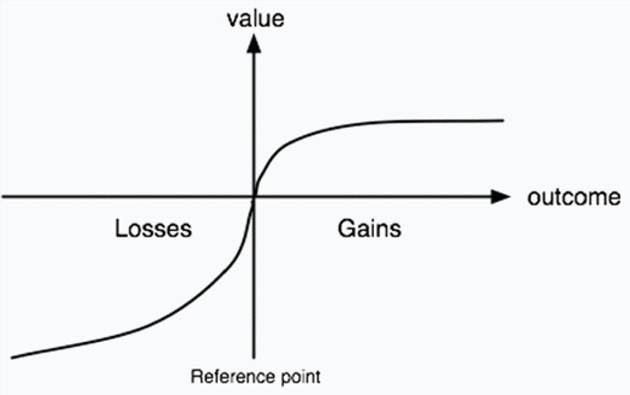

While increases in income are weighted by a small marginal utility, decreases in income are weighted by a larger marginal utility (Figure 1).Prospect theory is basically divided into two stages: editing and evaluation. In the editing stage, the different choices are ordered following some heuristic so as to simplify the evaluation stage. The evaluations around losses and gains are developed starting from a reference point. The value function (sketched in Graph1) which passes through this point is s-shaped, and as its asymmetry implies, given the same variation in absolute value, there is a bigger impact of losses than of gains (loss aversion). Some behaviors observed in economics, like the disposition effect or the reversing of risk aversion/risk seeking in case of gains or losses (termed the reflection effect), can be explained referring to prospect theory.

The three main characteristics of Tversky and Kahneman’s value function, which replaces the expected utility value function in the investor’s decision, are as follows (Mullainathan & Thaler, 2000, p. 6):

• The value function is defined over changes to wealth rather than levels of wealth (as in Expected Utility) to incorporate the concept of adaptation.

• The loss function is steeper than the gain function to incorporate “loss aversion,” which is the concept that people are more sensitive to decreases in their well-being than to increases in their well-being.

• Both the gain function and loss function display diminishing sensitivity (the gain function is concave, the loss function is convex) to reflect experimental findings.

Figure 1. Hypotetical value function

Source: Kahneman and Tvesrky 1979, p286

To fully describe choices, prospect theory often needs to be combined with an understanding of “mental accounting.”

In conclusion, the discontinuity on the slope at the reference point is probably the most significant element evidenced by prospect theory. But at the same time, it doesn’t accurately define what determines the location of the reference point, nor how to distinguish the difference between very high probabilities and extremely high probabilities.

The experimental evidence shown by Kahneman and Tversky does not point out systematic patterns which could be codified in a generalized theory; therefore these elements could not be specified (Cornicello, 2004, p. 26).Shiller reviewed prospect theory in finance, positing that expected utility theory, with its rational expectations derivative, is still the dominant paradigm for investor decisions in finance and for economic decisions in general (1999, pp.1308-1309). Here it will be useful to note that the importance of behavioral finance theory has been growing rapidly in the last decades. The full range of asset pricing models are surveyed and assessed by Campbell in 2000. He focused on the interplay between theory and empirical work and on the trade-off between risk and return. Facts about interest rates, aggregate stock prices, and cross-sectional patterns in stock returns have stimulated new research on optimal portfolio choice, intertemporal equilibrium models, and behavioral finance (p.1515).

Many of these models have been used to identify anomalies in investor behavior. Cochrane also discusses the broad category of alternative APMs, called multifactor models (Gorener, 2003, p. 20).

A paper by Barberis, Huang and Santos from 2001 discusses prospect theory in the context of national income accounts, incorporating consumption and changes in wealth as part of the reference frame. They also surveyed recent finance literature that focuses on prospect theory and loss aversion (Barberis et al., 2001, p.48).

Another research direction in the literature follows the practice of the first Kahneman and Tversky paper, and obtains responses by surveying. This approach seems less satisfactory than working with a large panel of historical data: as Kahneman and Tversky point out, survey responses may be influenced by the phrasing of the questions.

Recently, prospect theory has been entering the literature about investor behavior. In many cases, however, it keeps its links with psychology.

Many sensible and plausible ideas from psychology do not come into finance in forms that are readily testable, particularly with high frequency data. This matter is well illustrated by Shefrin in the year 2000. He identifies and discusses several practices associated with reference dependence, including mental accounting, hedonic editing, regret minimization, and what is commonly called isolation (Gorener, 2003, p. 21).The original Kahneman and Tversky (1979) paper contains these concepts. However, the scope for analyzing them in the historical financial market data only does not seem very promising, as the findings should be supported with empirical findings using real market financial data.

In brief, prospect theory differs from many other psychological theories in that it has a solid mathematical basis, which gives economists the opportunity to play with it. Prospect theory has some elements similar to expected utility theory. In both theories, individuals maximize a weighted sum of “utilities,” but the difference with prospect theory is that the weights are not the same as the true probabilities, and the utilities are determined by a “value function” rather than a utility function.

It can be argued that behavioral finance literature has two important aspects: cognitive biases and limits to arbitrage. These two subjects will be discussed in the following subsections.