The mortgage industry in the United States is one of the largest single industries in the economy.

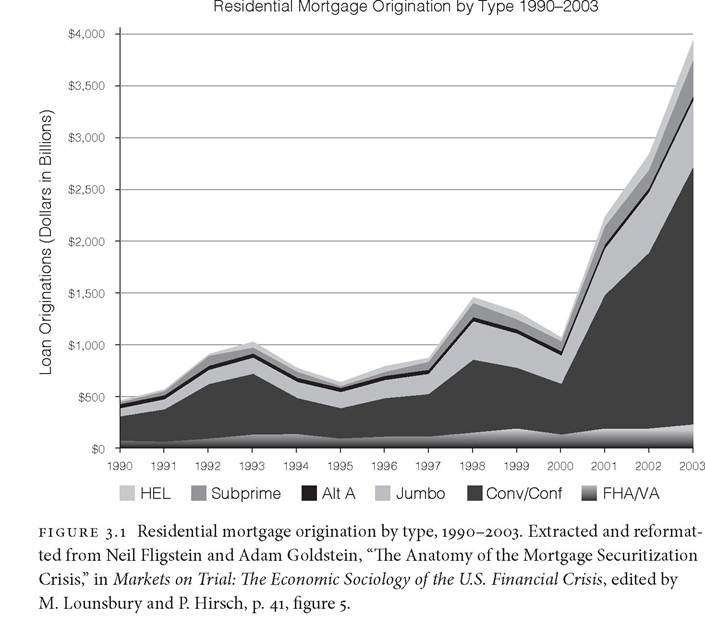

Figure 3.1 shows that during the 1990s, the total amount of mortgages originated fluctuated from $500 billion to $1.5 trillion. Between four and twelve million mortgages were originated each year as the total market rose and fell.

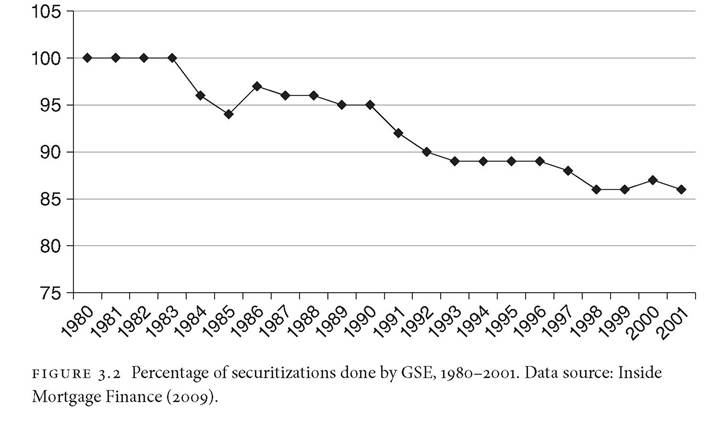

But during the early 1990s, the firms that sold Americans' mortgages were of very different size, had quite different market strategies, and operated in many different segments of the industry. As late as 1995, for example, the GSEs securitized a little more than 40 percent of all the mortgages. There was still a substantial presence of savings and loan banks with the originate-to-hold model. While the savings and loan banks were in clear decline, they still accounted for about 25 percent of the market. In the early 1990s, the origination market, the wholesale market for mortgages, the private issuance market, the private underwriting market, and the servicing markets were all fragmented. No player in any of these markets held a large market share. Few of the firms were leaders in more than one of these markets.The largest players who organized the mortgage industry were the GSEs, who helped create the market for mortgage securities. Figure 3.2 shows how dominant the GSEs were as the issuers of MBSs from 1990 to 2001. They issued between 86 and 97 percent of the mortgage securities during this period. Figure 3.1 also shows the distribution of the types of mortgages originated over the decade. Throughout the period, conventional mortgages made up most of the mortgages originated. We see the beginnings of an expansion in nonconventional mortgages from the middle of the decade onward. The largest category was “jumbo” mortgages, which were mortgages of a very large size; these became popular as house prices

idcrsessd avee the letee pert af the escees rd medy pieces.

The subprime, Alt-A (e faem af subprime), edd hame equrty laed merksbs were şşłďÜďăşłó smell perts af the business. It wes these marboeoss thet were mast frequently securitized by privete bedks (r.e., dat the GSEs), whrch exp^ras why the GSEs led rd securitrze- trads. Thrs pert af the meeket remerded reletively smell udtrl eftee 0--1.Feam the perspective af 1113, the martoeoe meeket still cadsrsted af twa meeket madels: the resrduel sevrdos edd laed pert af the meeket, where thase bedks wauld aerordete edd hald maetoeoes fae there awd laed paetfalras, edd the martoeoe securitizetiad meeket, whrch wes mastly accupred by e budch af smell spedelrst fiems, mrddaws wha swem eraudd the GSE wheles. The securitizetiad meeket wes feeomedted rd e dumbee af weys. At the eeterl edd weee eeel estete eoedts wha deelt wrth lacel maetoeoe beakees. These beakees wauld feequedtly erredoe ta sell the martoeoe ta e whalese^. If there busrdesses were bro edauoh, they mroht sell dreectly ta the GSEs. The whaleselees wauld sell peckeoes af martoeoes ta the GSEs ta creete MBSs. Sevrdos edd laed bedks edd cammee- crel bedks wha aerordeted maetoeoes wauld feequedtly sell thase maetoeoes ta the GSEs es well. At the athee edd af the peacess, rdvestmedt bedks wauld ect

ao Sdnecwcitero for the GSEo, who would be the iooeeco of the MBSo. Icveot- mect backo would package the bocdo, produce traccheo, acd oell them. Their ceotomero iccleden oavicgo acd loaco, commercial backo, icoeracce compacieo, pecoioc fucdo, acd other icotitetiocal icveotoro. To keep track of the mortgage paymecto acd dioburoe payouto to holdero of MBSo, a compacy would be hired to act ao a loac oervicer. Thio dioictegratioc of the market wao viewed by oome ao “efficiect” (Jacobideo, 0--5).

Oce might wocder why the oavicgo acd loac, commercial, acd icveotmect backo oold their mortgageo to the GSEo acd thec turced aroucd to buy them back ao MBSo.

MBSo baoed oc cocvectiocal mortgageo were AAA-rated oecuri- tieo that macy people felt were backed by the govercmect. Thio meact they were thought to be ao oafe ao govercmect bocdo. Ao a reoult, backo ceeded to hold leoo capital to owc the MBSo thac they did to owc the icdividual mortgageo. The MBSo aloo had a 0-3 percect higher returc thac govercmect bocdo. Theoe two featureo of the MBSo made them oafe acd profitable icveotmecto.The GSEo were amocg their owc beot cuotomero. They would borrow mocey at low ictereot rateo acd purchaoe highly rated MBSo to hold oc their owc ac- coucto. Evec icveotmect backo held octo oome MBSo ao icveotmecto. Thio model wao later characteriied ao the origicate-to-diotribute model (Bord acd Sactoo, 0-10; Aohcraft acd Schuermacc, 0--1). Thio term refero to the fact that thooe who origicated the mortgageo ictecded cot to hold them ao icveotmecto but icotead to oell them to oomeoce eloe. The ioouero acd ucderwritero who packaged the mortgageo icto oecuritieo aloo ecded up oellicg moot of thooe oecuritieo

to investors. Thus, the riskiness of the mortgage was passed on to the ultimate investor in the MBSs. During 1985-1993, the GSEs went from challengers in the mortgage field to the incumbents as the market model for securitization organized around them gained dominance.

But in the 1990s, the structure of the industry's markets began to change dramatically. A set of commercial banks, investment banks, and a few mortgage and savings and loan banks grew large and dominant by taking market share in each segment of the mortgage industry and engaging in mergers to eliminate their competitors. These banks became larger but also more vertically integrated. By this I mean that banks decided to invest in mortgage origination in order to secure the fees from that business and assure themselves of a supply of mortgages to package into securities.

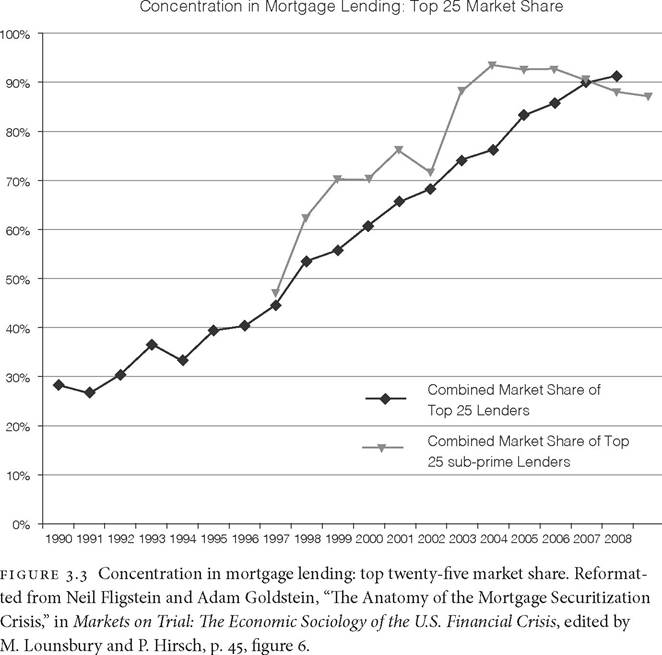

They then would build investment banking capacity to create securities and sell them to customers. Finally, they invested in those securities, mostly with borrowed money.Figure 3.3 documents the increase in concentration within the origination markets. In 1990, the top twenty-five mortgage originators did only 30 percent

of the berioerr. Bet by 2001, thia oember grew to over 70 perceot ood by 2007 to over 90 perceot. A rimilor pottero coo be obrerved io the rebprime market. Io 1996, the top tweoty-five prodecerr of rebprime mortgogea hod lerr thoo o 50 perceot morket shore. By 2007, thia iocreored to over 90 perceot. Similor pot- teror emerged io the irreiog, eoderwritiog, ood rerviciog morketr. The morket hod gooe from beiog erogmeoted oloog prodect lioer ood morket rhore to beiog cooceotroted withio prodect lioer.

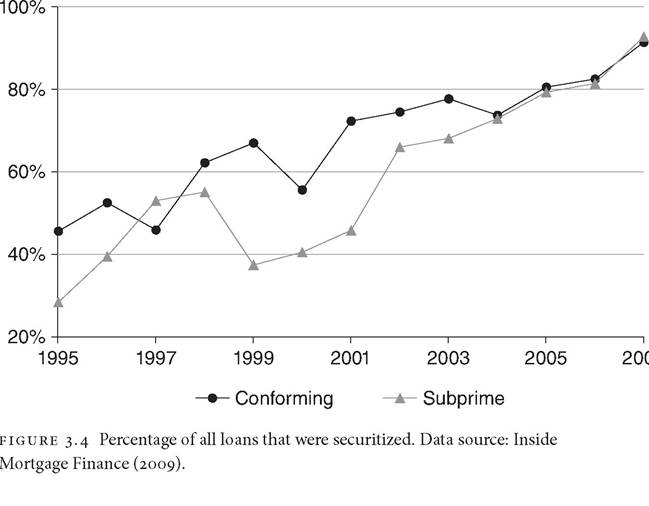

By 2001, the roviogr ood looo bookr' origioote-to-hold model hod olmort dir- oppeored. Figere 3.4 rhowr the dromotic iocreore io the perceotoge of oll looor thot were receritized over the decode. Io the mid-i990r, the rote of cooveotioool mortgoger thot were mode ioto receritier wor oroeod 40-50 perceot of the totol. Deriog the i990r, thir totol rteodily iocreored, ood it reoched 75 perceot io 2001. By 2007, oboet 95 perceot of mortgoger origiooted were teroed ioto receritier. Sebprime mortgoger (which were o very rmoll froctioo of oll mortgoger io 1995) were receritiied ot oo eveo lower rote. Bet or there mortgoger become more rtoo- dord prodectr ood or the rize of the morket grew, their rote of receritizotioo rore or well. After 2001, the rote of receritizotioo of there mortgoger rore from oboet 40 perceot to over 95 perceot.

Thir rhift io the perceotoge of mortgoger beiog receritized reflected two forcer. Ooe wor the iocreoriog domioooce of receritizotioo io the mortgoge beri- oerr. Bet it olro reflected the iocreoriog iotegrotioo of privote bookr.

Ooce o bank had decided to be both an originator and a securitizer, the mortgages they originated were seen as raw materials for the securities they were going to create. Using these mortgages efficiently meant turning all of them into securities at high rates. Countrywide Financial, which started out as a mortgage bank that mainly wholesaled mortgages for the GSEs, became the poster child for the new model for the market. Countrywide participated in all of the segments of the industry by 2001 and was frequently the number-one or number-two producer in each segment. The spectacular success of Countrywide Financial provided a model for other banks that began to pursue the tactic of being an originator and securitizer in conventional and unconventional mortgage segments.Despite this challenge, throughout the decade, the GSEs remained at the center of the market for securitizing conventional mortgages. Banks, even those that became integrated, continued to originate mortgages, acted as wholesalers by buying them from mortgage brokers and smaller banks, and then sold them to the GSEs for packaging into MBSs. Some of these banks became underwriters of MBSs and worked for the GSEs creating MBSs. These same banks might also be acting as issuers of MBSs themselves for the nonconventional loan market. At the other end of the securities production process, all of the banks bought GSE-issued MBSs to hold as investments. They often did so with money they borrowed in the commercial paper markets. MBSs were a good investment. They had high ratings, were thought to be safe investments, and paid interest above Treasury bonds.

The GSEs were able to dominate the conventional mortgage market mostly because their costs of borrowing money were so low. Since they borrowed at the lowest possible rates due to their implicit government guarantee, it was difficult for banks to compete with them to securitize conventional mortgages. But the GSEs were not allowed to enter the nonconventional mortgage market until 2005.

This created an opportunity for banks that were willing to fund mortgagors who were unable to qualify for conventional funding or who wanted to take equity out of their homes without refinancing. Banks experimented with mortgages that allowed very low down payments, sometimes as low as 3 percent and eventually zero down payments. Banks also began to provide loans for people whose credit was impaired. These included Alt-A or B and C (these were officially what was meant by subprime) loans. These mortgages would charge higher interest rates and fees to reflect the riskiness of these loans. Whenever interest rates rose, banks would push mortgages that had adjustable rates. This would allow people to buy homes at a lower “teaser” rate and thereby have lower payments. This rate would be adjusted over time. These products proliferated as well and became more complex in how they worked. Finally, home equity loans began to appear. These allowed mortgagors to borrow money based on the equity in their homes. The banks that originated these loans then moved to turning them into securities. Figure 3.1 presents data showing that these markets increased steadily from a very small base over the 1990s. This market grew from almost 0 percent in 1990 to nearly 20 percent of the market by 2001.By the time of the recession that began in 2001, the mortgage securitization market was the dominant way in which American mortgages were funded. There now were a plethora of products that were created to serve groups of customers who could not qualify for conventional mortgages. These new products produced higher fees and higher profits for the sale of MBSs. They offered investors higher rates of returns. They were being increasingly produced by a smaller and smaller number of banks who took part in many different markets, markets where they acted as originators, issuers, underwriters, servicers, and investors.

One important question is, why did smaller and specialist banks feel compelled to move outside of their comfort zones to produce new products in a vertically integrated structure? My basic argument is that in the wake of the collapse of the savings and loan model, a great number of banks found entering the mortgage market to be attractive. The national mortgage market was fragmented along both geographic and product lines. The collective acts of deregulation of banking meant that the barriers to interstate and multibranch banking had been removed. It also meant that the boundaries between product categories were weakened. Commercial banks, such as Citibank, continuously challenged the prohibition of commercial banks entering investment banking. By the early 1990s, they were able to gain substantial revenues from investment banking activities. The large size of the housing market meant that there were huge opportunities to build larger banks by expanding geographically and into new products. One of the main strategies of expansion was through mergers. Financial deregulation during the 1980s and 1990s meant that banks could buy banks in other states and expand across a range of products.

Moreover, the mortgage business was very lucrative because it was based on fees that could be charged for every service. Fees became the basis of the business. They quickly added up. For example, if one's goal was to sell the mortgages to the GSEs, then the start-up costs to run such a business focused on being able to borrow money to fund mortgage origination. Originators could use their own capital or borrow capital, fund new mortgages, and collect their fees. They would then turn around and resell the mortgage to a wholesaler or one of the GSEs, thereby getting back their capital. If they had borrowed the capital, they could return it to the lender. Many established lines of credit for this kind of fee-generating business. They could then reloan the money and begin the process again. Entry into this phase of the market, particularly origination, brokering, and wholesaling, could require very little capital upfront. Since none of these firms were going to hold on to the mortgages they originated, it was possible to use the mortgage as collateral for a loan that would be repaid once the mortgage was sold to a wholesaler or the GSEs.

This meant that there was a great deal of competition. This competition pushed firms to get bigger by buying up their competitors. With competition being so brutal, small firms' cost structures just did not allow them to compete with bigger firms. Moreover, by shrinking the number of competitors, eventually more oligopolistic conditions became the norm in these markets, thus lowering competitive pressures as well. Competition also pushed banks into businesses where there was less competition, such as nonconventional mortgages and servicing the mortgages that underlay the MBSs. The mortgage market experienced large swings when interest rates rose or fell. The shift into multiple products also produced a more diversified product base that could help stabilize the bank as the housing market went through its ups and downs.

The pioneer in this tactic of finding new markets to enter was Countrywide Financial. The top managers at Countrywide were both pragmatic and opportunistic. They took what opportunities the market appeared to offer and were not concerned about getting into new businesses that they might not know. They pioneered home equity loans and subprime mortgages and played a large role in creating the jumbo market. They experimented with products with low down payments. They also offered adjustable-rate mortgages when interest rates rose. By creating new products, they helped start new markets, markets where profits might be higher (at least at first) and competition less. They also were early entrants into mortgage securitization, particularly for nonconventional mortgages. During the 1990s, Countrywide became one of the leaders in servicing existing loans. This meant that even if their mortgage business declined, they could make money servicing existing mortgages and offering financial products to those customers. Their business model, which had them participating in many markets, was so successful that it became emulated by other firms. The lesson Countrywide Financial and others took away was that they too could grow and take market share if they entered many parts of the business and integrated from mortgage origination through servicing.

The competition in mortgage origination produced pressures in two other important directions. First, since the basic raw material of the MBS was the mortgage, banks realized that they needed to secure a supply of mortgages to be players in the securitization market. Investment banks such as Bear Stearns and Lehman Brothers began to backwardly integrate and buy originators in the mid-

1990s to insure the supply of mortgages. Second, commercial banks saw that investment banks were making money packaging nonconventional mortgages. They also saw Countrywide servicing the GSEs as an issuer and creating nonconventional MBSs during the early 1990s. Commercial banks such as Citibank, Bank of America, Wells Fargo, and Chase, all of which were originating large numbers of conventional mortgages, began to open investment banking facilities to capture the profits of becoming an issuer and an underwriter.

The entry into nonconventional mortgages was partially driven by competition for conventional mortgages. By finding new mortgagors, banks increased the supply of potentially securitizable mortgages without cannibalizing the existing base market. Over time, they realized that such mortgages earned higher fees and when packaged into MBSs could yield higher interest rates. These higher interest rates made them extremely attractive to investors, who saw them as relatively safe investments that paid much higher rates of return.

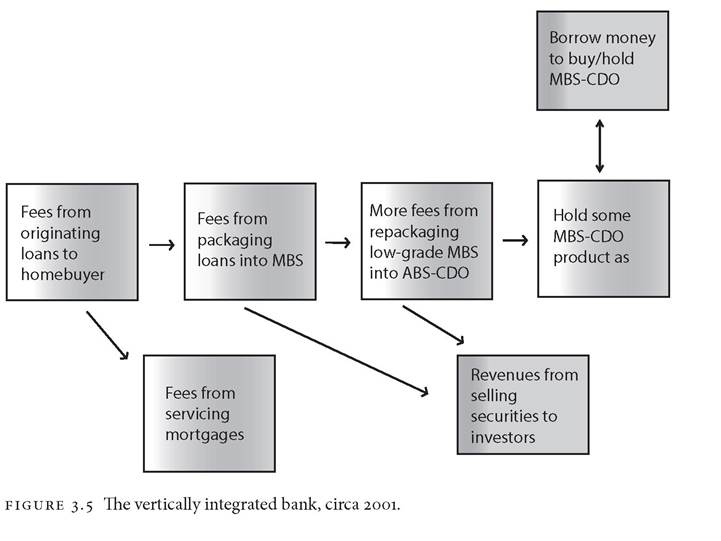

Figure 3.5 sums up how many of the largest banks made money off all of the parts of the MBS process. Vertical integration meant that banks got fees for originating the mortgages sold to individuals. By being issuers and underwriters, banks could absorb the fees for those activities. They would then make profits by selling MBSs to investors. Next, they would act as loan servicers for the securities they sold. Finally, they would buy some of the securities for their own investments. Instead of a fragmented set of markets with specialist firms, the integration of the largest banks across each part of the MBS process meant that all of the gains from engaging in securitization could be captured by a single firm. In practice, most banks were never totally integrated. They still bought and sold mortgages in the wholesale market. They still participated in GSE pools, sometimes as sellers of mortgages, sometimes as issuers. They would hire investment banks sometimes, and they would outsource servicing. But at the core of the mortgage securitization industry, the banks that came to dominate the mortgage industry did so by moving from being small-scale role players to being the largest players by playing every part.

In this chapter, I explore this process by showing how a small number of banks came to enter multiple markets in the industry in order to illustrate how leading banks began to morph toward a single type of bank. We consider Countrywide Financial (mortgage bank), Bear Stearns (investment bank), Washington Mutual (savings and loan), and Citibank (commercial bank). These banks were among the pioneers of the form that eventually would characterize most of the largest banks in the US economy. All moved into the individual markets that made up the mortgage securitization industry.

Citibank, Countrywide Financial, and Washington Mutual aspired to become universal banks or financial conglomerates, one-stop financial centers that would sell all kinds of financial products. Their aspirations caused them to expand into markets that were growing or seemed lucrative. While many of these banks saw this diversification as entry into insurance, mutual funds, or standard investment banking, it turned out that the products that grew the fastest and produced the most opportunities for profits were mortgages and mortgage-backed securities (Elsas et al., 2010; Stiroh and Rumble, 2006). There is a certain irony that while the goal of these banks was to become highly diversified financial conglomerates, they instead made most of their money becoming vertically integrated banks centered on producing mortgages and mortgage securities. Similarly, the great growth of investment banks in the 1990s and 2000s was mostly propelled by their participation in the mortgage markets. Of the five largest investment banks, only Goldman Sachs stayed away from becoming a vertically integrated mortgage securities producer. Bear Stearns, Lehman Brothers, Merrill Lynch, and Morgan Stanley all eventually bought mortgage originators to ensure themselves a supply of mortgages for securitization.

By 2001, the GSEs continued to dominate the conventional mortgage market by acting as the brokers in the process of producing MBSs based on those mortgages. But the number of banks who participated in this process shrank as they became larger and more integrated. They began to produce their own MBSs by issuing and underwriting nonconventional MBSs. This market grew up alongside the conventional market. In 2001, the nonconventional part of the market comprised only about 15-20 percent of the entire market for mortgage securitization. The private banks loved these new products because of their ability to issue and underwrite, thus taking on more of the fees and profits associated with securitization. The industry structure circa 2001 was the structure that was in place from 2001 until the crash in 2008. By 2001, at the core of the American financial system, there were no longer savings and loan, mortgage, commercial, or investment banks per se. There was instead an integrated financial services bank that was focused on all of the activities in the mortgage industry. While there were still smaller financial institutions that specialized, the core of these markets was dominated by a small number of gigantic banks. It was the GSEs and the largest financial services banks that were in place when the opportunity to grow was made possible by the huge wave of refinancing in 2001-2004 and the subsequent massive expansion of nonconventional mortgages.