The Reorganization of the Mortgage Industry

It is useful to present some data on how the reorganization of the mortgage market after the financial crisis played out. In the wake of the meltdown and bankruptcy and reorganization of the largest banks, it is safe to say that the vertically integrated, mortgage-securitization-oriented bank no longer exists.

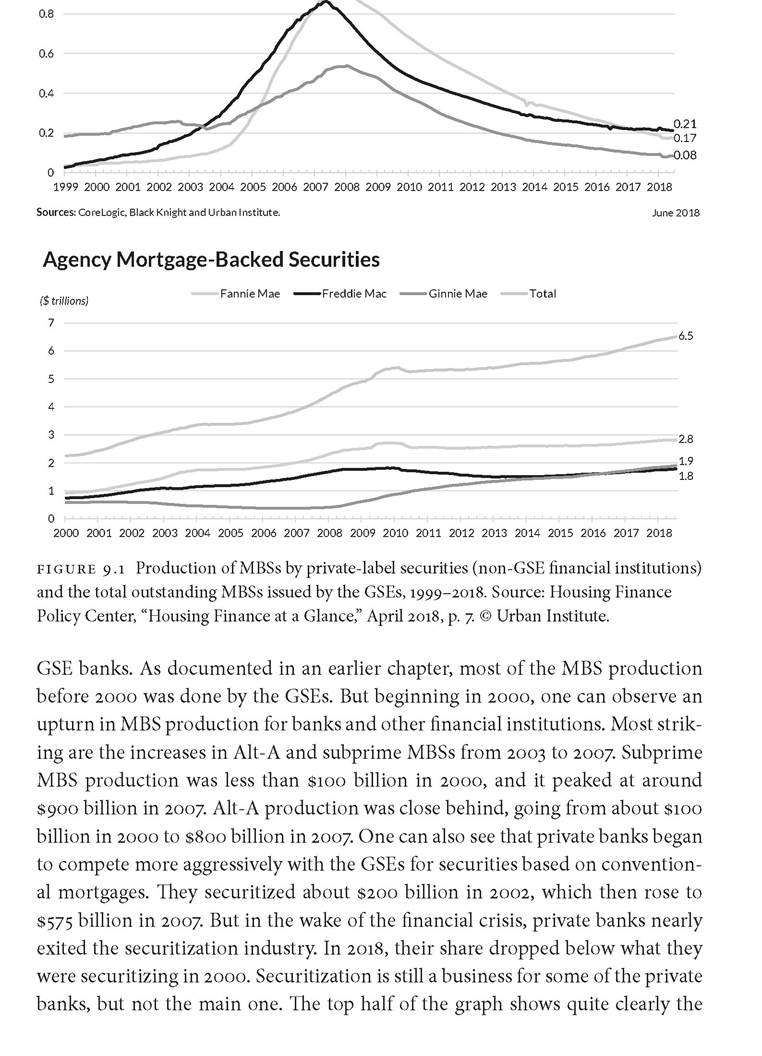

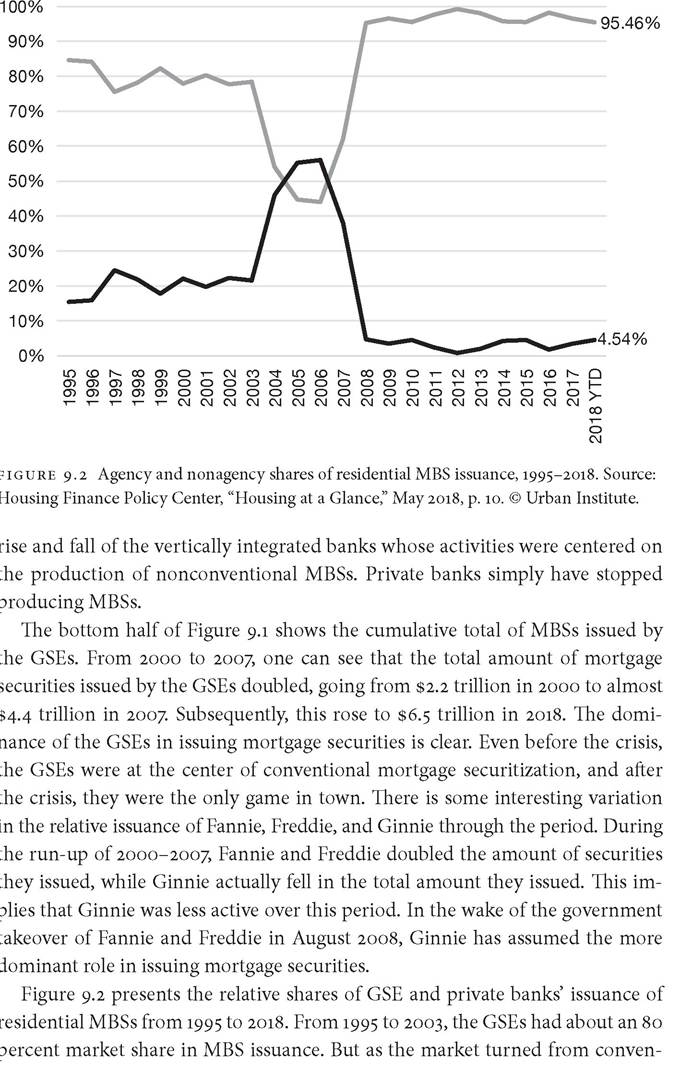

The GSEs are now doing almost all mortgage securitizations (Government Accounting Office, 2019; Securities Industry and Financial Markets Association, 2019). Private banks have moved on from originating and securitizing mortgages. No one is producing subprime mortgages. Banks have instead expanded their activities in all directions and now operate as financial conglomerates with product divisions that participate in various financial markets. Banks continue to hold on to MBSs because those based on conventional mortgages are still a good investment. But this is only one of the investments in their portfolios. The ABCP market has returned to its more normal role in providing short-term credit for banks and nonfinancial companies.To illustrate the role of private banks in the mortgage market, Figure 9.1 presents data on what happened to MBS production before, during, and after the financial crisis. The top panel presents data on the issuance of securities by non-

Private-Label Securities by Product Type

Alt-A Subprime Prime

($ trillions)

1

— Agency share Non-Agency share

2012 to $13 trillion as foreclosures rose and people lost their homes.

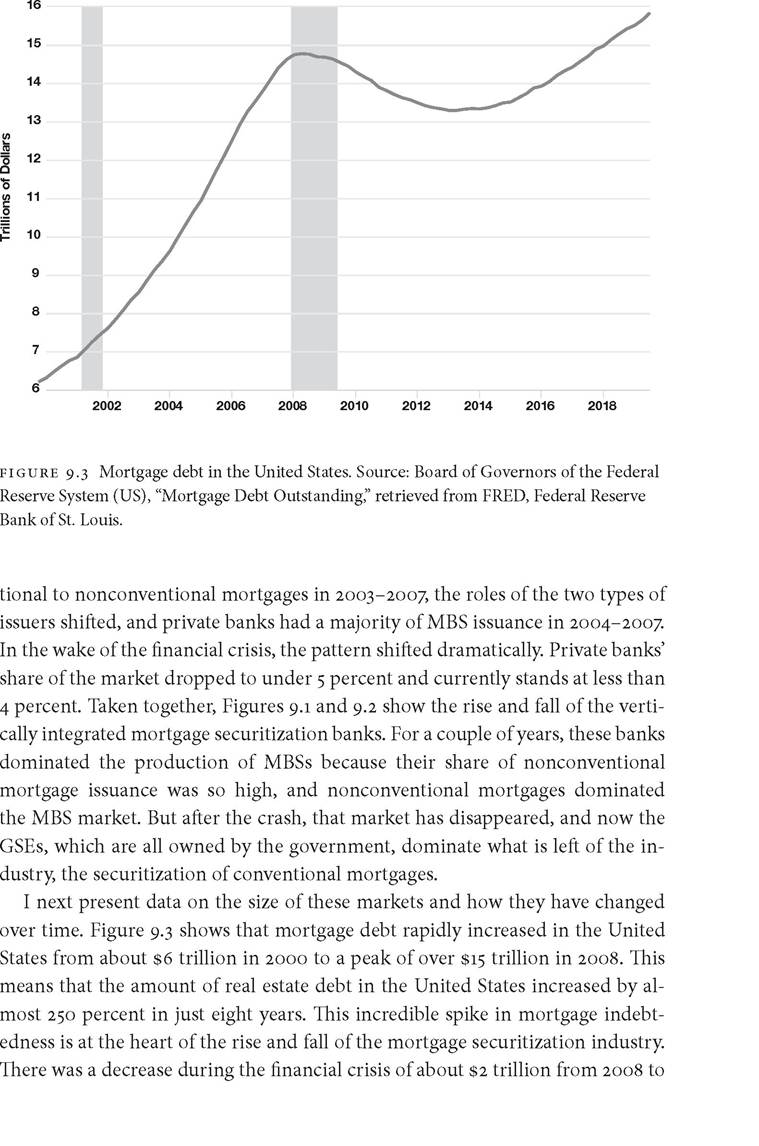

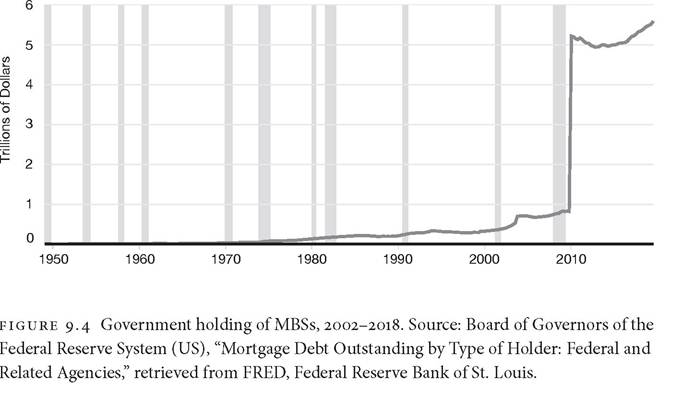

This is about a 13 percent decrease. But since 2012, mortgage debt has been on the rise again and is about $15.8 trillion in 2018. This is an increase of $2.8 trillion in six years, about 20 percent. While the increase is not as dramatic as the increase earlier in the 2000s, it is still quite large.One of the most interesting questions is, who now owns the huge amount of MBSs that exist? Figure 9.4 shows the amount held by the federal government. In 2000-2008, the federal government held about $1 trillion of mortgage debt. Most of this was in the form of conventional MBSs that were produced by the GSEs. In the summer of 2008, the federal government took over Fannie Mae and Freddie Mac and thereby got their MBS and loan portfolios. These totaled about $1.2 trillion. The Federal Reserve also began its asset-purchasing program in 2008 by buying agency securities from banks in order to provide them with liquidity and became a large holder of MBSs. Figure 9.4 provides graphic information about how this huge run-up in securities affected the federal government's ownership of mortgages. The total held by the government before the financial crisis was around $1 trillion. But beginning in 2008-2010, this increased to over $5 trillion dollars. In 2018, it stood at about $5.7 trillion. Given that all mortgage debt in the United States was about $15.8 trillion, the federal government owned about 36 percent of all mortgage debt in the country. One of the great ironies of what has happened is that the federal government created the GSEs in the 1960s as a way for them to not be directly involved in owning mortgages. But as a result of the financial crisis, the federal government is the owner of over a third of all mortgage debt in the United States. Most Americans are unaware that every month when they pay their mortgages, that money is going to the government.

Finally, I want to take up the issue of what happened to the banks. The forced reorganization of American banking in the wake of the financial crisis heavily increased the concentration of banking assets in the United States.

In 2018, the five largest banks in the United States controlled 48.5 percent of assets, and the ten largest controlled almost 66 percent. These banks include JPMorgan Chase ($2,615.18 billion in assets), Bank of America Corp ($2,338.83 billion), Citigroup Inc. ($1,925.17 billion), Wells Fargo ($1,872.98 billion), Goldman Sachs Group Inc. ($957.19 billion), Morgan Stanley ($865.52 billion), U.S. Bancorp ($464.61 billion), TD Group US Holdings ($380.65 billion), PNC Financial Services ($380.08 billion), and Capital One Financial Corp ($362.91 billion). One of the persistent issues that have been expressed in the wake of the financial crisis is that these banks are now too big to fail. They are so large that their failure is likely to have the same kind of spillover into the rest of the banks and the rest of the economy that was witnessed in the downturn in 2008. If, for example, JPMorgan Chase went bankrupt, it would send ripples through the entire banking system and the whole economy.One of the ways in which the federal government has tried to deal with this problem is the Dodd-Frank Act, which was passed in 2010. One part of the act allowed the Federal Reserve to define which banks were “systemically important”—that is, banks whose failure would potentially bring down the system. The Federal Reserve has the ability to force those banks to raise capital so that they can withstand a serious downturn. To judge where the banks are, the Federal Reserve has asked these banks to undergo a stress test to see what would happen to their balance sheets in the case of a serious downturn.

The basic idea is to consider how a severe economic downturn would affect the current holdings of the banks in order to determine whether the banks have enough reserves to control their losses.2 It is useful to quote the conditions of what constitutes a severe downturn for the purposes of the test given in 2019:

The severely adverse scenario is characterized by a severe global recession accompanied by a period of heightened stress in CRE markets and corporate debt markets.

This is a hypothetical scenario designed to assess the strength of banking organizations and their resilience to unfavorable economic conditions and does not represent a forecast of the Federal Reserve. For the stress test, the U.S. unemployment rate climbs to a peak of 10 percent. In line with the increase in the unemployment rate, real GDP falls about 8 percent from its pre-recession peak, reaching a trough. (Federal Reserve, 2019: 4).Applying this scenario to a complex balance sheet that differs dramatically across firms is a challenging prospect. Of course, the model about the potential impact of such changes is itself difficult to construct and relies on previous data. The Federal Reserve concluded in 2019 that all of the banks had the capital reserves to survive such a deep downturn (2019: 25). The adverse scenario results in an average decrease of about 25 percent in capital cushion and a $680 billion loss across banks. At the end, the average level of capital cushion is only 0.1 percent above what the Federal Reserve views as safe. Most of these losses were for investments they made that include residential and commercial real estate loans, personal loans, financial instruments (including government and corporate bonds and MBSs), and credit cards. The overall picture shows that the largest banks are no longer as dependent on MBSs and CDOs for investments, and they are no longer borrowing short term to fund those investments.

So, what does this all add up to? The mortgage securitization industry went through a huge expansion in the 2000s. When the downturn in conventional mortgages occurred in 2003, the market rapidly shifted to the production of nonconventional MBSs. These turned out to be a big problem, and all of the private banks involved in the production of MBSs underwent serious reorganization. As a result of the crisis, the federal government now owns the GSEs, and it controls mortgage origination and the production of MBSs in the economy. It is currently the largest holder of mortgage debt in the country. The private banks have moved on. They no longer are involved in the production of non- conventional MBSs (although they still hold mostly conventional MBSs on their balance sheets). The last crisis has passed, and the situation has stabilized (albeit with lots of government participation). The chance that the next financial crisis will be exactly like the last one is pretty remote. This raises the next question: what should the government be doing to be vigilant for the next crisis, one that will probably have entirely different causes?