The Rise of the Savings and Loan Model of Mortgages

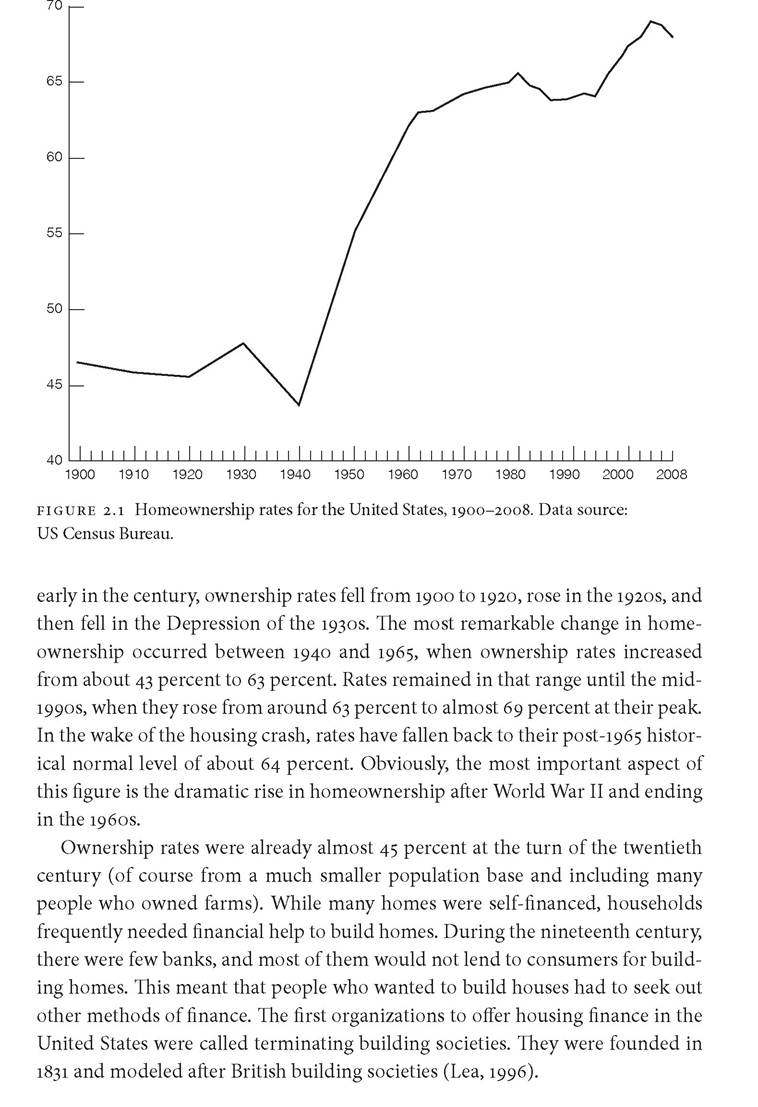

Figure 2.1 presents a graph showing the pattern of homeownership in the United States from 1900 until the eve of the Great Recession in 2008. One can see that

Middle-income households would pool their funds in the terminating building society and agree to loan each member the money to build a house.

The members would contribute to the fund until sufficient funds were built up to lend. The order in which the money to build was lent was based on members offering to pay a higher interest rate in order to build earlier. When the last home was built and paid for, the society would be dissolved. The ability to create such societies required places where people knew each other well, had long time horizons, and trusted that they would get their turn.These building societies were the basis for what would later become the modern savings and loan banks (Haveman and Rao, 1997, 2007). By the mid-1850s, building societies began to accept new members and thus not dissolve when the original members had built their homes. Members were also allowed to remove their funds when they had finished building if they chose to do so. The next important step was for the building societies to begin to accept deposits from individuals who did not want to build a home. These deposits were usually placed in accounts where they could not be removed for some period. These accounts were a forerunner of modern time deposit accounts. This meant that the funds available to build and be repaid would not be removed suddenly. It also had the effect of separating the depositors from being involved in the lending process. As a result, building societies turned to professional management to monitor savings and the loan processes. By the turn of the twentieth century, a version of the modern savings and loan bank was in place (Haveman and Rao, 1997).

Other types of mortgage providers also emerged in the nineteenth century. Mutual savings banks were originally founded to provide outlets for lower-income people to have savings accounts. To protect their accounts, depositors were also the owners of the bank. These banks began to enter the mortgage market in the 1850s and surpassed the building societies as the largest provider of mortgages until the 1920s. Their business model was to take deposits from savers and lend to borrowers who wanted to build homes. Life insurance and mortgage companies also began to offer mortgages on a national basis. Their business model was to use local agents to make and service loans rather than build a national organization. These local agents would find the borrowers and take monthly mortgage payments.

The mortgage companies also pioneered private mortgage bonds. These were based on a model introduced in Germany whereby investors with capital would invest long term in a set of diversified mortgages (Snowden, 1995). The main investors in these bonds were insurance companies in the northeast and investors in Europe. These bonds resembled modern mortgage-backed securities. In the 1890s, there was a financial crisis in the United States, and these bonds failed en masse. Snowden (1995) attributes this collapse to investors having had little information about the underlying mortgages in the bonds. He also suggests that their lack of regulation meant they were riskier than similar bonds in Europe. This event eerily resembles the MBS meltdown of 2008-2009. Many of the national mortgage companies that pioneered these loans disappeared by the early 1900s. The national mutual savings banks met a similar fate. They depended on agents from around the country to monitor the ability of the mortgagor to pay back the loan. In a series of scandals, it was revealed that homes around the country had been appraised at too high a value.

Commercial banks generally stayed out of the market for mortgages in the nineteenth century.

They viewed their main concern as providing loans to small businesses. They also tended to view mortgage lending as risky because capital was committed for long periods of time. But beginning in the twentieth century, they began to enter the market. By 1914, 25 percent of their loans and 15 percent of their assets were in real estate (Snowden, 2010).The mortgage market, until the Great Depression, was not well developed. Mortgages were unevenly available in every part of the country, as capital did not easily flow to the places that needed the funding for housing the most. Different types of firms dominated in different markets (Lea, 1992). Mortgage terms were not standardized. Many loans required mortgagors to put 50 percent down on a home. They also had variable terms, some running as short as two to three years and the longest-term mortgage running ten to twelve years. Building and loan societies tended to have the best offers. Their mortgages would run ten to twelve years and would allow borrowers to take loans out up to two-thirds of the house value. Mutual savings banks tended to have mortgages that ran for five years with a balloon payment due at the end (Morton, 1956). The mortgagor had to either pay the remainder of the mortgage or refinance the mortgage. Commercial banks tended to have the shortest-term mortgages, reflecting their desire to not tie money up for long periods.

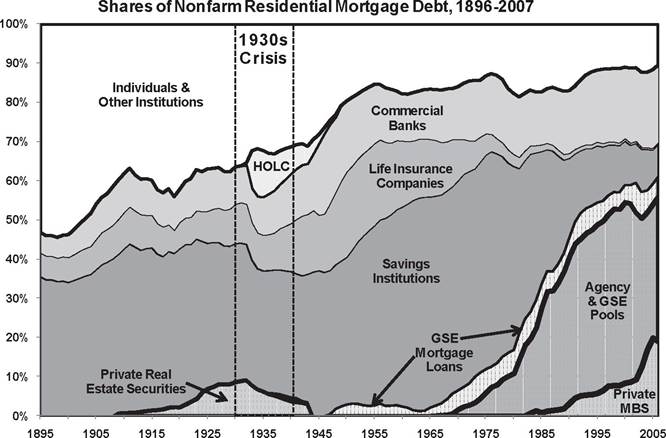

Figure 2.2 documents who held nonfarm residential debt from 1895 to 2005. As a result of the difficulty of finding a mortgage and the need to put down a large down payment, 41 percent of households owned their homes in 1920 but only 40 percent of these were mortgaged (Snowden, 2010: 7). Before 1920, between 40 and 50 percent of these mortgages were provided by individuals or other noninstitutional investors. The 1920s was a period when homeownership increased. The share of the market taken up by savings and loan, mutual savings banks, and commercial banks rose to meet this demand and increased their share of mortgages from 50 to 65 percent.

Private mortgage securities reemerged to help finance homes and took almost 10 percent of the market. On the eve of

figure 2.2 Shares of nonfarm residential debt, 1895-2005. Source: Kenneth A. Snowden, “The Anatomy of a Residential Mortgage Crisis: A Look Back to the 1930s,” NBER Working Paper 16244, figure 2. Used by permission of the author.

the Great Depression, the share of mortgages held by institutions increased to a little over 65 percent (Snowden, 2010: 7).

There was a proliferation of business models for the various parts of the industry during the 1920s in what would now be called financial innovation. Each of the participants in the booming real estate market had a different way to fund mortgages and mortgage products with very different characteristics. For example, during the 1920s, a bond market that funded a pool of mortgages reemerged. This time, the market that evolved created bonds that would own businesses that would develop particular tracts of land. Private mortgage insurance, which had sprung up earlier, now grew rapidly to support the growing private market for mortgages. Mortgage issuers of all varieties used the insurance to protect their mortgages.

Unfortunately, when the Great Depression hit, the mortgage industry was particularly vulnerable to the economic downturn. The 1930s witnessed the collapse of the entire banking system (Bernanke, 1983). As businesses went bankrupt, people were laid off, and unemployment rose to almost 25 percent. The drop in economic activity meant that banks had loans that stopped performing, many of which were based on assets that were rapidly losing value. The housing market was particularly hard hit. As people lost their jobs, they could not pay their mortgages, and many just abandoned their homes. This left banks with outstanding loans based on homes whose value had dropped dramatically. Not surprisingly, banks failed at a high rate.

Commercial banks were hit by losses in both their loans to business and their loans for homes. Savings and loan banks found themselves with defaulted loans. Grebler et al. (1956: 477) estimates that they lost $5 billion between 1930 and 1933. As a result, it is thought that nearly a thousand homes a day were foreclosed on from 1930 to 1937. Half of the twelve thousand building and loan associations disappeared between 1929 and 1941 (Kendall, 1962: 76-77).The buildings and loan model, the private mortgage insurance industry, and the private bonds markets all collapsed. Many of the buildings and loans associations were privately held and owned by their customers. This meant that they were not subject to the same laws as the commercial banks. Moreover, many of these associations had put their capital in accounts in commercial banks (Green and Wachter, 2005). When those banks went bankrupt, those funds were nearly impossible to recover. In spite of their apparent insolvency, it was not easy for such organizations to go bankrupt. Given that they also held mortgages that were ten to twelve years in length, the wind-down of these organizations took years. These problems also discredited the building and loan model of creating mortgage pools to fund housing. People who had entered these pools were likely to have lost all of the money they put into the organization and, for those whose houses were foreclosed, their houses as well. This meant the end of this model for providing mortgages.

Private mortgage insurers had sprung up in some states. These firms offered insurance policies against defaults on mortgages. They were regulated by state insurance boards. Herzog (2009) provides evidence that there were fifty of these companies in New York alone. He also shows that between 1930 and 1934, the entire industry went bankrupt. Part of the problem was that investigation of these failures showed that private insurers did not do their due diligence as the housing market heated up through the late 1920s.

They sold policies to anyone, as they were more interested in collecting premiums than they were in making sure the borrower was able to pay the mortgage. The scandal created a huge distrust in this kind of insurance, and the New York State Legislature held hearings on the matter and recommended that the industry be made illegal (Snowden, 2010: 18). As a result, private mortgage insurers did not return to the market until 1957 (Herzog, 2009: 3).As mentioned above, the mortgage bond reemerged during the 1920s. Most of these bonds were created to build particular projects. Bonds would fund the projects, and once they were built and sold, the bondholders would be returned their money. The amount of these bonds grew dramatically during the 1920s (see Figure 2.2). Snowden documents how these projects massively failed during the Depression (2010: 14). It is estimated that 80 percent of the bonds in Chicago, Cleveland, and Detroit failed. Half of all the bonds issued during the 1920s defaulted (Snowden, 2010). These bonds were also the subject of hearings. The US Congress passed legislation allowing closer regulation of the industry by the Securities and Exchange Commission (Halliburton, 1939: 46-93). The single-project bond industry was never able to overcome this downturn, and it disappeared as a form of real estate financing (Koester, 1939).

In response to the Depression, the entire banking system became the subject of regulation. In a series of pieces of legislation, each of the parts of the now-al- most-bankrupt system came under some new form of regulation. At the state level, governments worked to maintain protection for banks that were located within their borders (Kroszner and Strahan, 2005). At the national level, this regulation pushed banks to define themselves as commercial or investment banks. It also set rules for loans and solvency and provided deposit insurance (Sellon, 1990).

After the Great Depression, banks were restricted in the rate of interest they could charge on all types of deposit accounts. Under Regulation Q of the Banking Act of 1933, savings accounts were capped at 5.25 percent, and time deposits were limited to between 5.75 and 7.75 percent, depending on maturity. Paying interest on checking accounts was outlawed. These regulations were intended to prevent interest rate wars whereby banks would offer higher and higher rates to obtain deposits. In order to encourage mortgage lending within local communities, however, thrift institutions were allowed to offer deposit accounts interest rates 0.25 percent higher than other banks (Sherman, 2009; Sellon, 1990; Gilber, 1986). It should be noted that from 1934 until 1965, Regulation Q interest rate ceilings were above the average interest rates in general and thereby had little effect on what was actually being paid (Gilber, 1986: 17).

The federal government implemented several other emergency measures to respond to the mortgage crisis. Congress passed the Federal Home Loan Bank Act in 1932 (Ewalt, 1962: 87). Ewalt (1962) presents evidence that the United States Building and Loan League (USBLL), a trade association for the savings and loan banks, played a significant role in this creation by lobbying for the legislation for over a decade. The structure they lobbied for worked to the benefit of those banks and against the more traditionally organized buildings and loans. The act created the Federal Home Loan Bank Board (FHLBB), which was organized on a regional basis with twelve banks. These facilities began to help member institutions in early 1933 to help refinance the loans of distressed homeowners (Ewalt, 1962: 66). Of the eleven thousand building and loan associations, only thirty-nine hundred joined. These associations became the core of the modern savings and loan industry and ended up holding 92 percent of all savings and loan assets by 1950 (Ewalt, 1962: 97).

The Home Owners' Loan Act of June 1933 represented a second federal emergency response to the mortgage crisis. The act authorized the Home Owners' Loan Corporation (HOLC) to offer new loans to homeowners who were delinquent on existing mortgages (Harriss, 1951). The HOLC opened four hundred offices throughout the country and employed twenty thousand people to process loans and appraise properties. It ended up writing new loans on 10 percent of the owner-occupied homes in the United States. These loans reappraised the value of the homes to reflect the depressed prices around the country. Lenders could hold on to the refinanced mortgages, or they could sell them to the HOLC. Either way, the HOLC allowed many households to stay in their homes with more affordable mortgages (Harriss, 1951).

The FHLBB was given authority in the Home Owners' Loan Act of June 1933 to establish a system of federally chartered savings and loan associations. Two elements of the model ensured that members of the federal savings and loan industry would be structured and behave differently than traditional building and loans. First, federal savings and loans offered new kinds of contracts: share savings accounts instead of membership dues and direct reduction loans to replace the fragile share accumulation loan plan. Second, federal charters erected new barriers to entry so that small, part-time associations would never again represent a competitive fringe. About six hundred federally chartered savings and loan banks emerged and joined the FHLBB (Ewalt, 1962).

The final element of the industry's transformation was the creation of the Federal Savings and Loan Insurance Corporation (FSLIC) enacted in the 1934 National Housing Act. The government had earlier passed legislation creating the Federal Deposit Insurance Corporation (FDIC). That organization helped provide insurance for the savings and checking accounts of people who put money in commercial banks. The savings and loan industry realized that if they wanted to get deposits from local citizens, they would need to offer similar protection. The FSLIC made it safe for depositors to put their money into savings and loan banks.

The National Housing Act of 1934 created the Federal Housing Administration (FHA), which took a different approach to federal residential mortgage policy (Ewalt, 1962: 138-144). The FHA had two main activities. First, it created the FHA mortgage insurance program, which was designed to encourage commercial banks and insurance companies (competitors of savings and loans) to increase their presence in the mortgage market by providing mortgage insurance for lenders. Second, the FHA created a loan program that created the modern conventional mortgage. They specified down payments and loan limits as well as fixed terms and interest rates for mortgages. The idea behind giving the FHA these powers was to make sure that credit would flow to parts of the country where savings and loan banks were not able to raise enough capital to keep up with demand for mortgages. These features soon attracted commercial banks, life insurance companies, and mortgage companies to the program.

In practice, the FHA played two important roles in the postcrisis residential market (Jones and Grebler, 1961: 40-44; Klaman, 1959). First, federally insured mortgages became the dominant instrument that was used to aid the interregional transfer of mortgage credit. Second, these loan programs were used to finance the activities of large merchant builders because they provided advanced commitments for permanent financing during construction. This meant that FHA financing was used extensively to finance the expansion of the multifamily housing stock.

By 1940, the shape of the modern savings and loan industry was in place (Prasad, 2012). Government regulators had created a world where local households would put their money into savings and loan banks that guaranteed the safety of their deposits. These banks would use those funds to loan local households' money to buy homes with fixed-rate mortgages that required a 20 percent down payment and a fifteen- to thirty-year term. The banks would hold on to the mortgages until they were paid off. Banks had Regulation Q, which provided a ceiling for the rate at which they had to pay for funds. This meant that there was little competition between banks for the deposits of savers. In sum, households with relatively small down payments could buy houses with reasonable payments and know how much they would be paying over the course of the mortgage. This became the major source of house financing in the United States until the 1980s. Their share of mortgages was around 60 percent at the peak of the industry.

But the government also created its own direct model of intervening into the housing markets. By providing deposit insurance for commercial banks and creating the FHA, the government made sure that incentives were in place for these banks to lend to homeowners as well. The FHA defined the conventional mortgage in the late 1930s, and it quickly became the standard for both the savings and loan and commercial banks. The FHA helped low-income households buy homes directly by loaning money. FHA loans could be marketed through commercial and mortgage banks. The FHA also provided mortgage insurance to commercial and mortgage banks to facilitate buying.

The last piece of the New Deal legislation to consider was the creation of the Federal Home Mortgage Association, eventually known as Fannie Mae, in 1938. The organization's explicit purpose was to provide local banks with federal money to finance home mortgages in an attempt to raise levels of homeownership and the availability of affordable housing. Fannie Mae was supposed to create a liquid secondary mortgage market and thereby made it possible for banks and other loan originators to issue more housing loans, primarily by buying FHA-in- sured mortgages. Until the 1970s, Fannie remained quite small. There was not much market to buy mortgages, and Fannie was the main buyer in that market.

With the end of World War II in sight, Congress passed the Servicemen's Readjustment Act of 1944, informally known as the GI Bill. Included in the GI Bill was the invention of the Veterans Administration mortgage insurance program. This program allowed veterans returning home to obtain mortgages with very low down payments. The program was intended both to reward veterans and to stimulate housing market construction. The FHA also sought to stimulate housing construction by substantially liberalizing its terms. In 1948, the maximum term of a mortgage rose to thirty years (from an initial maximum of twenty years). In 1956, the FHA raised the maximum loan-to-value ratio to 95 percent (from an initial maximum of 80 percent) for new construction and to 90 percent for existing homes.

One interesting question is the degree to which the creation of this stable structure can account for the huge growth in homeownership in the postwar era. It is obviously difficult to untangle the large set of factors that explain the rise of homeownership. For example, once the basic institutional infrastructure to fund homeownership was in place by 1940, it did not change much. Thus, one can compare homeownership rates before and after the 1930s and conclude that the government interventions made a great deal of difference. But it is useful to try to separate the contributions of each of these innovations to explain the nearly 60 percent increase in homeownership over two decades.

The academic literature shows there is a good empirical case to be made that each of these reforms had a significant effect on homeownership rates. Chambers et al. (2013) show that about 21 percent of the increase was due to changes in mortgage terms. Fetter (2011) makes a plausible case that around 20 percent of the increase was due to shifts in policy by the FHA and the VA after the Second World War to encourage homeownership. Grebler et al. (1956: 243) present data showing that the share of mortgages in the United States provided by the FHA and the VA rose from 0 percent in 1935 to 44.1 percent in 1952. Rosen and Rosen (1980) show that about 20 percent of the increase was due to the tax deductibility of interest paid on mortgages. Taken together, this implies that the aspects of government policy that can most easily be measured account for up to 60 percent of the increase in homeownership from 1940 to 1965. The models used in this work correct for increases in education, income, economic growth in the postwar era, all of which had an impact on people's ability to borrow money.

I note that there are several features of what happened that are not easy to measure. The government created the legal and regulatory conditions for a stable mortgage market to emerge. The expectations of everyone in the system were built on the knowledge that at the end of the day, the government was committed to mortgages being available. Because of depository insurance, savers knew their deposits were now safe in banks. This stability had a cognitive aspect as well. Mortgage providers had a standardized product they could easily price because of Regulation Q. The savings and loan industry had a well-known business model by which they could borrow from individual households at a relatively fixed rate and make a profit loaning money. Figure 2.2 shows that between 1945 and 1975 the savings and loans increased their share of mortgage debt from about 35 percent to 50 percent. The FHA and the VA played their part by stimulating property developers and providing money to individuals to buy houses. The tax incentives for mortgage interest deduction meant that renting was not much cheaper than owning. As the economy grew in the postwar era and people had more disposable income, the structure was in place for them to buy houses with affordable mortgages (Prasad, 2012).