GLOBAL WARMING MEASURES

The Kyoto Protocol came into force in February 2005, although neither the USA nor Australia has ratified it. The agreed targets (see table 9.2) are meagre compared with the 60-70 per cent reduction in greenhouse gases that the UN Intergovernmental Panel on Climate Change (IPCC) estimates is necessary by 2050 to prevent serious and irreversible climate change.

Table 9.2 Kyoto Protocol targets for greenhouse gas reductions by 2012

| Australia | + 8% | Lithuania | -8% |

| Bulgaria | -8% | Monaco | -8% |

| Canada | -6% | New Zealand | 0% |

| Croatia | -5% | Norway | +1% |

| Czech Rep. | -8% | Poland | -6% |

| Estonia | -8% | Romania | -8% |

| EU | -8% | Russia | 0% |

| Hungary | -6% | Slovakia | -8% |

| Iceland | + 10% | Slovenia | -8% |

| Japan | -6% | Switzerland | -8% |

| Latvia | -8% | Ukraine | 0% |

| Liechtenstein | -8% | United States | -7% |

The signatory nations have agreed to allow nations to pay to exceed their targets using a range of mechanisms.

These are:• Emissions trading, which allows countries to buy the rights to discharge emissions above their agreed target from countries that reduce emissions below their agreed targets.

• Joint implementation (JI), which allows countries to offset their excess emissions by paying for emissions reductions or carbon sinks in other countries which have agreed to the Protocol.

• Clean development mechanism (CDM), which allows countries to offset their excess emissions by paying for emissions reductions or carbon sinks in countries which are not signatories to the Protocol; that is, developing nations.

Carbon sinks are to be created by projects such as tree planting that absorb carbon dioxide. CDM allows for afforestation, reforestation and avoided deforestation to offset greenhouse gas emissions. Offsets could also be generated by providing renewable energy generation projects and energy-efficient technologies to developing countries or by the closing down of old, dirty plants in Eastern Europe. In the case of both JI and CDM, the emissions reductions in other countries are supposed to be additional to what would otherwise have occurred - thus if a polluting facility goes out of business because of financial difficulties, the resulting emissions reductions cannot be claimed as additional because they would have happened anyway.

Each nation, in deciding how to meet its targets, may allocate greenhouse gas allowances to companies and allow them to use the same mechanisms of trading and offsets to meet them. In this way, individual corporations can also invest in projects in other countries to offset their emissions. The need to invest in JI or CDM schemes to offset emissions is supposed to provide an incentive for greenhouse gas generators to lower their own emissions, and income for developing countries to invest in environmentally-friendly technologies.

There is some disagreement between nations about the extent to which they should be allowed to meet their targets using emissions trading and other flexibility mechanisms; but many large corporations are pushing for there to be no limits in this regard, and nations such as Japan, Canada and Norway have acceded to this stance (Bachram et al.

2003: 1; CEO 2000: 9).Emissions trading

The emissions trading system under the Kyoto Protocol is a cap and trade system that will begin in 2008 and cover the 38 nations which are signatories to the Protocol. The cap for each nation is the emissions target it agreed to (shown in table 9.2). If nations are unable to meet their cap by the end of 2012 they will be penalised by having the excess plus a 30 per cent penalty included in their cap for the next 5-year compliance period (Bachram et al. 2003: 18). More effective penalties and fines for non-compliance have been opposed by the same nations that have been pushing for maximum use of market measures such as emissions trading (CEO 2000: 9).

In most countries, corresponding emission allowances will be distributed for free to large polluting companies on the basis of their past emissions (grandfathering). Corporations did not wait for an official international emissions trading scheme to be set up, and by 1999 were already trading $50 billion worth of emissions (CEO 2000: 13). The London International Petroleum Exchange deals in greenhouse gas emission credits and the Sydney Futures Exchange deals in credits from forestry projects (Rising Tide 2005b). Various states in the USA have introduced emissions trading schemes for greenhouse gases from power plants, including Massachusetts, New Hampshire and Oregon (Sonneborne 2002: 2).

There are now several active emissions trading markets:

• The UK system was the first to be established, in 2002. It is an emission reduction scheme rather than a cap and trade scheme. Reduction credits are earned by reducing emissions below a baseline based on past emissions. Companies which agreed to participate received an 80 per cent discount on the Climate Change Levy - a carbon tax on industrial and commercial energy use (IETA 2005: 34; Royal Society 2002: 37).

• The NSW Greenhouse Gas (GHG) Abatement Scheme began in 2003. All electricity retailers have to take part and are required to reach set reduction targets or buy credits to cover any excess (IETA 2005: 35).

• The Chicago Climate Exchange (CCX 2005) was set up in 2003. It claims to be the world's first 'voluntary, legally-binding rules-based greenhouse gas emissions allowance trading system'. Its purpose is to demonstrate how an emissions trading system could work. There is also a Chicago Climate Futures Exchange where investors can gamble on what the price of allowances will be in the future. The CCX deals in all six greenhouse gases and includes carbon offsets projects.

• The EU emissions trading system began in 2005 and covers some 13 000 companies including electricity and heat generators, and producers of cement, ceramics, ferrous metal, glass and paper (Chatterjee 2005).

• Individual European countries have also set up trading programmes. Denmark, for example, has set up a cap and trade programme to cover its electricity sector. The Netherlands has also set up a domestic greenhouse gas emissions trading system (Rising Tide 2005a; Bachram 2004: 5).

Carbon offsets

Both joint implementation and the clean development mechanism include a wide variety of projects providing carbon offsets. For example, the World Bank's Prototype Carbon Fund (PCF) 'counts energy efficiency in the Czech Republic, waste management in Latvia, afforestation in Romania, waste incineration in Mauritius, landfill gas extraction in South Africa and soil conservation in Moldou as eligible for carbon offset credits' (Bachram et al. 2003: 26).

One of the earliest carbon offset projects was created in 1988 when a proposal to build a coal-fired power plant in Virginia, USA, was justified by a $2 million project to pay farmers in Guatemala to plant pine and eucalypt trees and manage them to offset the power plant's CO2 emissions. Similarly, in 1998 American Electric Power, which uses coal to generate electricity, pledged it would preserve 2.7 million acres of a tropical rainforest in Bolivia in the hope that this would exempt it from having to reduce its greenhouse gas emissions, which would be far more expensive.

By that time there were around 100 such projects worldwide, including projects in Costa Rica, Uganda, Mexico and Australia (Lohmann 1999; Lynch 1998).Australia

In New South Wales a Carbon Rights Legislation Amendment Act, passed in 1998, 'enabled State Forests to acquire and trade in such rights as well as to procure land and manage it for investors of such rights'. Under this legislation Tokyo Electric Power Company (TEPCO) paid NSW State Forests to plant 40 000 hectares of trees. In return TEPCO will get both the revenue from the timber when it is logged and from the carbon offsets from the growing trees. Queensland has similarly amended its legislation to separate 'ownership of timber harvesting rights and carbon rights in a stand of trees from ownership of land' (Robinson amp; Ryan 2002: 27). A National Carbon Accounting Standard has also been developed to enable other organisations and individual landholders to get credit for their carbon sequestration activities (Salvin 2000).

Australia is one of the first countries to introduce legislation that enables carbon rights to be separated from land and resource ownership and to be owned and traded separately. This has enabled the Australian Sustainable Investments Fund to be established as a carbon fund which buys the carbon rights to Australian forests and plantations (Dickie 2005).

Global market in carbon offsets

The global market in carbon credits is expected by 2010 to be worth some $27.5 billion, according to the International Energy Agency (IEA) (cited in Marriott 2005). In 2004, some 107 million metric tonnes of greenhouse emission reductions, generated mainly by JI and CDM projects, were being traded. This was an increase of 38 per cent on 2003. Sixty per cent of these were bought by European buyers and just over 20 per cent by Japanese buyers. Almost 70 per cent were bought by private buyers as opposed to governments. They sell for between $3 and $7 per tonne of CO2 equivalent, much less than the price in emissions trading systems.

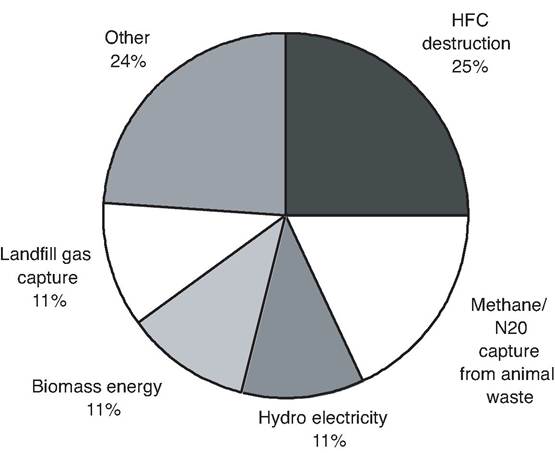

The emissions reductions were mainly generated in India, Brazil and Chile (IETA 2005: 3-4, 21). Most emission reductions are earned by reducing greenhouse gases other than CO2 (see figure 9.1).Figure 9.1 Source of emission reduction credits, 2004-5

Note: HFC is a refrigerant and a greenhouse gas

Source: (IETA 2005: 3)

Carbon neutral

A number of companies, such as the Carbon Neutral Company and Carbonfund.org, now sell the opportunity to be carbon neutral to people taking aeroplane trips, driving cars and engaging in other greenhouse gas generating activities. The 2005 G8 meeting was advertised as carbon neutral. Various bands, like the Rolling Stones, and celebrities have also made international tours that are supposed to be carbon neutral (McCallin 2005). Organisers of the 2006 Commonwealth Games in Melbourne proposed to make it carbon neutral through the mass planting of trees. The UK-based Carbon Neutral Company (previously Future Forests) had a turnover of pound;1.4 million in 2004 and expects that to increase to pound;2.5 million in 2005 (Hopkins 2005c).

Carbon taxes

A carbon tax is a tax on the carbon content of fossil fuels such as coal, natural gas and oil. The tax is imposed in order to raise revenue and to encourage people to use less of these fuels, which contribute to greenhouse gases in the atmosphere. Because so much carbon is used in affluent countries, even a fairly small tax could raise large amounts of money.

Carbon taxes are most prevalent in Europe, being levied in Belgium, Denmark, Finland, France, Italy, Luxembourg, the Netherlands, Norway and Sweden (NCEE 2004: 21). However, they 'are not applied to all fossil fuels or based on the quantity of CO2 emitted'. For example, the UK's Climate Change Levy is a tax on energy rather than a carbon tax, and excludes household energy use. Only in New Zealand was a genuine carbon tax proposed, but it was subsequently abandoned because of concerns that its cost (estimated at NZ$4 per week per household) would not be justified by sufficient reduction in emissions (New Zealand Scraps Kyoto Carbon-Tax Plan 2005).

Are economic instruments, whether based on prices or property rights, appropriate policies for environmental protection? Chapter 10 considers whether the economic instruments used for pollution control comply with the sustainability principle. Chapter 11 considers whether they comply with the polluter pays principle and the precautionary principle, and chapter 12 evaluates these economic instruments in terms of human rights principles, the equity principle and the participation principle.

Further Reading

Clean Air Markets (2006) US EPA, lt;http://www.epa.gov/airmarkets/gt; International experiences with economic incentives for protecting the environment

(2004) National Center for Environmental Economics, US EPA, Washington DC, November, lt;http://yosemite.epa.gov/ee/epa/eermfile.nsf/vwAN/EE-0487- 01.pdf/$File/EE-0487-01.pdfgt;

OECD (2003) OECD/EEA launch new database on economic instruments used in environmental policy, 2003, lt;http://www.oecd.org/document/15/ 0,2340,en_2649_34487_2505231_1_1_1_1,00.htmlgt;

Robinson, Jackie amp; Sean Ryan (2002) A review of economic instruments for environmental management in Queensland, CRC for Coastal Zone, Estuary and Waterway Management, lt;http://www.coastal.crc.org.au/pdf/economic_ instruments.pdfgt;

Water Quality Trading (2006) US EPA, lt;http://www.epa.gov/owow/watershed/ trading.htmgt;