THE POLLUTER PAYS PRINCIPLE

Internalising costs

Economic instruments such as taxes and charges are supposed to make external costs part of the polluter's decision. Laws can also force the polluter to take notice of these external costs by prescribing limits to what can be discharged or emitted.

Economists argue, however, that the market is better able to find the optimal level of damage: the level that is most economically efficient. The idea that there should be a level of pollution that is above zero but is called 'optimal' is strange, and even repugnant, to many people - but it is a central assumption in the economic theory on which economic instruments are based.If a pollution charge is equivalent to the cost of environmental damage, the theory says that the company will clean up its pollution until any further incremental reduction in pollution would cost more than the remaining charge, that is, until it is cheaper to pay the charge than reduce the pollution. This is said to be economically efficient because if the polluter spends any more, the costs (to the firm) of extra pollution control will outweigh the benefits (to those suffering the adverse affects of the pollution).

This might seem to be a less than optimal solution to the community, but economists argue that the polluter is better off than if it had paid to eliminate the pollution altogether and the community is no worse off because it is being compensated for the damage through pollution charges paid by the firm to the government. In theory, the payments made by firms in the form of charges can be used to correct the environmental damage they cause or to compensate the victims.

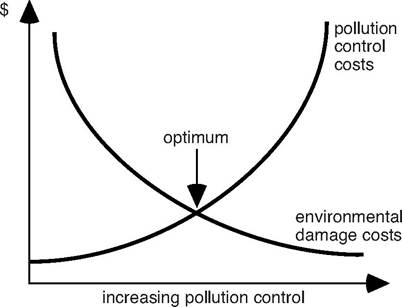

Figure 11.1 Economist's graph showing incremental costs and benefits of pollution control

A further assumption behind the theory - that there is a point of optimal damage - is that progressively more pollution reduction is increasingly expensive (see the upward swing of the pollution control costs curve on figure 11.1) for smaller and smaller environmental gain (see the levelling-off of the other curve).

This premise is based on the idea that pollution reduction is achieved by pollution control equipment being added to production processes. In contrast the aim of ‘clean production' is to change production processes so that the pollution is not generated in the first place. Changes in production processes may end up saving a firm money over the long term.Environmental taxes and charges are supposed to ensure that the price of goods includes the costs to the environment of producing them. In this way, the market is able to work out what quantities of pollutants will be produced. All this supposes that charges and taxes are in some way equivalent to the damage done, that environmental damage can be paid for, and that this is as good as, or even preferable to, avoiding the damage in the first place. This implies that the benefits that arise from the environment can be substituted for other benefits that can be bought on the market. However, environmental quality is not something that can be swapped for other goods without a loss of welfare (see chapter 8). There is also considerable doubt about whether money payments can correct environmental damage in many circumstances; and, more importantly, money collected from pollution charges is seldom used to correct environmental damage or to compensate victims.

Inadequacy of prices

In practice, governments and regulatory agencies do not attempt to relate charges or taxes to the 'external costs' of environmental damage. Additionally, environmental taxes and charges are frequently promoted by economists and others as a way of replacing other charges and taxes that firms would normally have to pay.

The UK research organisation Truscot estimated that if companies had to pay the actual cost of the economic damage caused by carbon emissions - estimated by the UK government to be some pound;20 per tonne - some of them would be paying around half their earnings. Overall it would cost 12 per cent of the earnings of the top 100 UK firms listed on the stockmarket, the FTSE 100 (Robins 2005).

This is not something governments are likely to require because of the economic (and political) ramifications.Pollution charges seldom cover the full cost of pollution as required by the polluter pays principle in the broad sense. In the case of user charges, the difficulties involved in working out the environmental costs of natural resource extraction and use mean that water charges generally cover only the operating costs of the water authority, not the environmental costs; that waste charges generally cover only the physical costs of disposing of the wastes; and that royalties for mining are levied to provide revenue to governments rather than full compensation for resource and environmental loss (Robinson amp; Ryan 2002: 12-3).

Similarly, a performance bond is supposed 'to internalise the risk costs associated' with an activity such as mining or hazardous waste transport. However, the size of the bond is seldom based on a scientific assessment of the damage that might actually occur in the short or the long term (Robinson amp; Ryan 2002: 10).

Subsidies, bounties and tax concessions do not conform to the polluter pays principle at all, because the polluter is being subsidised rather than bearing the full cost of pollution control measures. The OECD (1989) has found that environmental subsidies tend to serve economic rather than environmental goals - most notably the provision of financial support to firms that find it expensive to meet environmental standards.

Similarly, the cost of tradeable pollution rights is determined by the market; it has no direct relationship with the cost of environmental damage. This means that polluters are not paying the actual costs of the damage they cause and that these economic instruments do not conform to the polluter pays principle. This is particularly the case when emissions credits or allowances are allocated to companies at no cost, which usually happens with emissions trading schemes. In such cases, polluters are paying only for the extra credits they need beyond those allocated, and polluters that reduce emissions below their allocations can even make money from them.

Incentives for innovation

Economists argue that the imposed costs, even if they don't internalise the real environmental costs of polluting activity, nevertheless provide an incentive for companies to reduce their pollution and thereby save money. The contention is that legal standards might ensure firms meet particular targets, but once having met them there is no incentive to go beyond them, whereas under the financial incentives provided by economic instruments, 'businesses are constantly motivated to improve their financial performance by developing technologies that allow them to reduce their output of pollutants' (Stavins amp; Whitehead 1992: 30).

Adding costs to a firm's operations may impose pressure on it to reduce its costs but there is no guarantee that it will do so in the area where the cost is imposed. A firm might find it easier, cheaper, or even more profitable, to apply new technology and methods in other parts of its operation or simply to pass the increased cost on to the consumer - especially in sectors where there is little price competition between firms.

A number of studies have shown that 25-30 per cent of dischargers who are subject to effluent charges do not understand the pricing system and that 'significantly different levels of payment could arise if they altered the strength/volume composition of the effluent' (Rees 1988: 184). Many of them do not have sufficient knowledge of alternative methods and costs to make optimal decisions in their own interest. Jacobs (1993: 7) gives the following example:

In Britain a rise of 400% in sewerage charges failed to change firms' behaviour, even though it was shown that small investments in pollution control would pay back in under a year. The charging system was not understood by the firms affected; it was dealt with by the finance department, not the engineers; and the firms did not know the technological options available. A regulation requiring them to install the better technology would almost certainly have been more efficient - that is, cost less overall - than the huge price hike which would have been required to get the same changes made.

Joseph Rees (1988: 172) says that advocates of economic instruments tend to assume that 'the pollution control system is populated by economically rational entrepreneurs and regulators, operating without technical, perceptual, organisational and capital availability constraints'. This is not the situation in the real world. For example, a firm may not be able to afford the initial capital cost of changing production processes or putting in pre-treatment equipment, even if this would be cheaper in the long term than paying the charges. As Amory Lovins has pointed out, 'Although price matters, the ability to respond to price matters more' (quoted in Jacobs 1993: 7).

The degree of incentive provided will obviously depend on how large the charge or tax or subsidy is: 'If it is low, and environmental improvement is primarily achieved through major investments in plant and equipment which occur rarely, there may be little effect' (Jacobs 1993: 7). In theory, the fee or charge or price of allowances should be more than the profits made by not reducing pollution; but in practice the amounts charged are often very low. Similarly, pollution charges and user charges are usually not high enough to provide an incentive to minimise pollution or resource use (NCEE 2004: 3). This is the result of political pressure from industries not wanting to pay higher charges, and of concerns that higher charges might encourage illegal dumping and evasion of the charges.

Disincentives for innovation

Although economic instruments are supposed to encourage technological innovation, they often stifle it by allowing firms to pay for pollution rather than reduce their emissions. It is often much easier to pay a charge or buy pollution allowances than to invest in research and development that may or may not result in pollution reduction technologies that will be cheaper than the cost of the charge or allowance.

A 'trading program effectively lessens or eliminates the pollution control obligations of the sources having the greatest need for innovation, those facing high control costs', while those who can reduce their emissions for low cost don't need to innovate to gain credits to sell.

Similarly, international emissions trading and offsets create 'an economic incentive to deploy existing technology abroad in lieu of innovation at home'. For example, an electricity supplier is able to install standard technology on a coal-fired power station it operates in another country rather than find renewable energy sources at home (Driesen 1998). The pressure to change production methods and energy sources to be more sustainable is reduced, thus increasing 'the risk that countries and industries that have the capacity to develop new technologies will fail to do so' (Ott amp; Sachs 2000:17; Richman 2003: 170-1).Quick and easy

The market often favours the technologies that are cheapest in the short term, even though more expensive options have broader benefits and are more economical in the long term: 'Energy efficiency investments that save money for the society as a whole over a long period of time do not necessarily appear economic' to investors. Renewable energy projects, for example, 'tend to be greenfield developments [new developments] which are capital-intensive, provide low rates of return and generate relatively small volumes of credits' over a long time period. Yet these projects have 'greater environmental and social value than a project that merely captures end-of-pipe emissions' from an existing facility (Lohmann 2004: 34-5).

The narrow focus on a tradable commodity means that a carbon market will actually frustrate environmentally superior outcomes by directing investment away from projects with the most overall benefits. By going after the cheapest reductions, the market all but ensures that investment will flow to the 'lowest quality' reductions, those that involve the least investment, least genuine technology transfer, and least sustainable development co-benefits, as all this would raise prices. (Lohmann 2004: 34)

Substantial changes to technological paradigms require institutional changes that decision-makers prefer to avoid.

In addition, decisions to retrofit old plants or build new coal-fired power plants abroad may actually make it harder to switch to cleaner technologies once they become available. Once investors make fresh investments in older plants, they may want to keep these plants running for a long time in order to maximize the return from these sunk costs. (Driesen 1998)

In this way any technological improvements are marginal rather than wholesale, and more radical innovations are avoided.

US experience

Under the US acid rain emissions trading programme, state electricity companies have developed a pattern of buying low-sulphur coal from another state or emissions credits from another company rather than investing in new technologies such as integrated gasification-combined cycle or investing in renewable energy sources:

The market places no value on integrated gasification-combined cycle's ability to reduce not only sulfur dioxide by an order of magnitude, but also reduce oxides of nitrogen, carbon monoxide, volatile organic compounds and heavy metals such as mercury. The polluter is interested in one - and only one - outcome: reducing emissions of sulfur dioxide to its allocated level of pollution, no more, and at the lowest possible price. (Moore 2004a: 7-8)

Under the Los Angeles Regional Clean Air Incentives Market (RECLAIM) programme, the cheap initial price of emissions credits made them more desirable than installing pollution controls. In 1997, for example, the cost of NOx credits was less than 50 times the cost of the best available control technology to reduce nitrous oxides. Power plants, which had been responsible for 14 per cent of NOx emissions, bought up 67 per cent of the NOx emission credits expiring in 2000 rather than install available technologies for reducing NOx emissions (Moore 2004b).

Under the previous legislative regime, southern California had been the leader in development of environmental technologies. The Technology Advancement Office had spent around $10 million, raised from a small portion of car registration fees, to develop new technologies such as fuel cells, low-emitting burners and turbines, ultra clean fuels and zero-emission paints. Under the RECLAIM programme, these technologies were not implemented and lost their markets (Moore 2004b).

Annual NOx emissions were reduced by only 1305 tons between 1994 and 1998 through the implementation of pollution control equipment by companies seeking to comply with RECLAIM, compared with reductions of 9000 tons per year 'in the same time frame as a result of discretionary implementation of control equipment initiated under the rules prior to RECLAIM. This illustrates how emissions trading has muted the incentive to innovate' (Drury et al. 1999: 277-8). For example, the AES Alamitos electricity generating plant near Long Beach, California, had been required to install selective catalytic reduction for NOx emissions in the early 1990s under Rule 1135, which set NOx emission limits for power plants. When RECLAIM was introduced in 1993 the installation of this technology was abandoned, leaving two boilers with it and two without. When electricity generation increased at the plant so did NOx emissions (Moore 2004b).

When the price of emissions credits jumped by more than 100 times in the space of a few months in 2000, polluters were caught short, with no time to install control equipment, and had to pay large amounts for credits. Companies spent some $177 million buying credits, which was far more expensive than installing the pollution control equipment that would have made buying credits unnecessary. This money went to credit brokers speculating on the market rather than to cleaning up the environment (Moore 2004b).

In the acid rain program, for example, there is no evidence that so much as one advanced coal combustion technology has been deployed because of trading, though there is ample proof that command and control programs have induced such efforts. Similarly, the trading of leaded gasoline does not appear to have stimulated any advances in superior refining technologies. Indeed, the greatest single advance in fuel in the past 15 years, the development of environmentally engineered, or reformulated, gasoline was largely prompted by the command and control requirements of California that preceded RECLAIM. (Moore 2004b)