Anticommons, property fragmentation and the laws of entropy

Building upon the recent literature on anticommons and property fragmentation, Parisi (2002a) considers the proposition that property is subject to a fundamental law of entropy.

With this metaphor Parisi refers to the second law of thermodynamics, according to which every process that can occur spontaneously will go in one direction only and will result in a release of energy that cannot be recaptured, so that the amount of entropy in the universe will continually increase. In the property context, entropy induces a one-directional bias which leads towards increasing property fragmentation. The law of entropy further indicates that only in the purely abstract case of (both internally and externally) reversible transformations will the overall net change in entropy be zero. In the property context, this indicates that only in a world of zero transaction costs would there be no such tendency towards fragmentation.The economic forces that induce entropy in property are quite straightforward. Property division creates one-directional inertia: unlike ordinary transfers of rights from one individual to another, reunifying fragmented property rights usually involves transaction and strategic costs higher than those incurred in the original deal. Consider the case of unified property as the starting point: a single owner faces no strategic costs when deciding how to partition his/her property. Conversely, the reunification of fragmented rights requires the participation of multiple parties, with an unavoidable increase in transaction and strategic costs. For example, even reversing a simple property transaction can result in monopoly pricing by the buyer-turned-seller; reunifying property that has been split among multiple parties engenders even higher costs, given the increased difficulty of coordination among the parties.

Thus the move from unified property to fragmented property and vice versa poses an interesting situation of asymmetric transaction costs.

The presence of such asymmetry is due to the fact that fragmented owners are faced with a strategic problem, given the interdependence of their decisions. The equilibrium pricing (or quantity supply) of fragmented owners impedes the optimal reunification of non-conforming fragments into a unified bundle.A model of duopolistic anticommons

In the context of property, Posner (1998: 76) first recognized the costs of excessive property fragmentation. Heller argued that it is often harder to regenerate separated bundles than to fragment them (1998, 1999); Buchanan and Yoon (2000); Schulz et al. (2002) and Parisi et al. (2004) restated this thesis with formal economic models.

For the purpose of illustrating the problem of the anticommons and the resulting entropy in property, we can thus briefly restate the results of such literature, considering a simple model of property rights fragmentation. Suppose that agent 1 owns a large estate of land which he/she uses as a commercial farm. Agent 2 acquires from agent 1 the right to use the estate for recreational hunting. As a result, the unitary property right is fragmented, giving the two agents partial property rights and reciprocal exclusion privileges. The property right of agent 1 is constrained by the real interests acquired by agent 2. Agent 1 holds a right to exclude any use of agent 2 other than recreational hunting. Agent 2 conversely holds a right to exclude any use of the land by agent 1, which is in conflict with his/her acquired rights. In this sense, the previously unitary proprietary interest over the land is now fragmented. Such fragmentation will remain beneficial for all parties as long as the mixed use of the land for the respective activities of the fragmented owners remains the most valuable allocation of the land for the parties.

Suppose now that a third party sees an opportunity which would generate more value than the current use. Take, for example, the construction of a hotel resort on the estate.

The construction would obviously compress the property rights held by the two agents. Each agent could thus withhold his/ her consent to the transformation of the land and exercise his/her veto right impeding the value-enhancing transformation. However, as the opportunity is supposed to be more valuable than the current use, it would be rational for the various agents to agree to the proposed transformation. Yet, each fragmented owner would rationally attempt to maximize his/her profit from the sale of his/her fragmented property right. We should thus consider the likely price mechanism that would lead to the development of the land and compare it to the alternative scenario of a property transformation controlled by a single unified property owner.An application of the Buchanan and Yoon (2000) model could illustrate our problem. In the presence of development opportunities, a third party who wishes to utilize property fragments for the reunified development of the land needs to obtain the consent of all fragmented property holders. Because in the face of a redevelopment opportunity, each property fragment constitutes a strictly complementary input for the achievement of reunified property, the demand for each property fragment depends not only on the price set by the individual fragmented owner, but also on the price charged by the other property right holders. This implies that any change in the price or quantity supply of the complementary good by one duopolistic property seller will have external effects for the other property seller. Each party maximizes his/her profits, without regard to the effect of his/her own pricing strategy on the profits of other property owners. When one seller decreases output and raises the fragment price, the demand curve faced by the other property owners will be negatively affected, and vice versa. A concentrated monopolistic seller of the land would instead fully internalize these price or output externalities.

A simple illustration is useful.

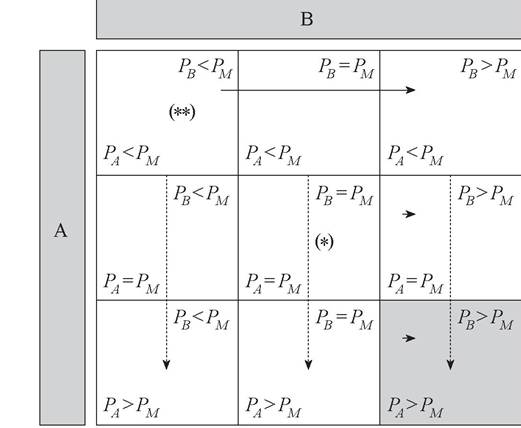

Suppose our two fragmented owners, A and B, each own two fragments of property the reunification of which is essential for the development of the land. Assume that each fragmented property owner must make a decision about price without knowing what the other seller will do. To simplify, suppose there are only three pricing options: the price a single monopolistic seller would demand, Pm, a price greater than Pm, or a price smaller than Pm. The game matrix in Figure 5.1 illustrates the incentives facing each seller. Each cell would contain the payoff (profit) to seller A and seller B from the corresponding combination of their pricing decisions. Seller A is a row player, and its Nash strategy given each of seller B’s choices is indicated with the dotted, vertical arrows. Seller B is a column player, and its Nash strategies given each of A’s potential choices are indicated with the solid, horizontal arrows.Here, given the cross-price effects present in this complementary anticommons, both sellers would have a dominant strategy, with a single

Figure 5.1 Game matrix

Nash equilibrium, indicated by the shaded areas in Figure 5.1. The sellers will choose to price above Pm, to the detriment of both the developer’s profits and the overall (that is, developer’s plus sellers’) welfare. The cells corresponding to the profit-maximizing prices and the welfare-maximizing prices are respectively marked with a single asterisk (*) and a double asterisk (**), in the figure.

It should be noted that in our anticommons problem strategies Pa = Pb > Pm obtain in equilibrium. The sellers’ strategic pricing renders the optimal property reunification unobtainable in equilibrium. The uncoordinated pricing of the two fragmented property owners results in a higher total cost of land development, and therefore to a potential underutilization of the land, beyond what either of them would expect as a unified monopolistic owner of the estate, in order to maximize their own profit.

Interestingly, the ‘competitive’ (that is, fragmented) supply of land development rights leads to higher prices than those that would be charged by a single ‘monopolistic’ (that is, unified) owner.As pointed out by Schulz et al. (2002), the differences between the two equilibria are due to the presence of negative externalities in the independent choices of the fragmented property rights. This result should not come as a surprise. The position of multiple property owners in the face of a new opportunity, which requires a reunification of their fragmented property rights, creates a strategic problem similar to the well-known hold-up problem. Suboptimal final use of resources may result from such fragmentation.

A model of oligopolistic anticommons

The above model of property fragmentation can be extended to show that an increase in the extent of fragmentation exacerbates the result of final underutilization of the resource. Recalling our example, imagine that the estate was partitioned among a larger number of agents, n. Let us further assume that the property fragments are controlled by independent agents and that the development of the land necessitates the agreement of all n individuals. What would be the equilibrium price of the land lease if the fragmented property owners are pricing their fragments independently from one another?

The model of duopolistic anticommons illustrated above can be extended to illustrate the more general problem of oligopolistic anticommons. We shall thus develop a simple model of oligopolistic anticommons with n fragmented property owners, showing that the extent of the deadweight loss also depends on the extent of property fragmentation.

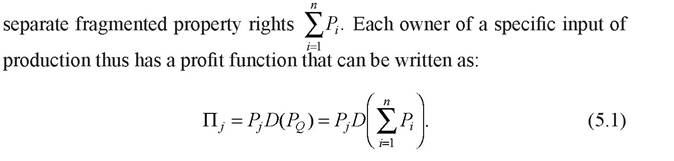

Suppose that n individuals hold property rights over n fragments, which can be used as inputs of production for a composite good, Q. Because of their strict complementarity as inputs for the reunification of land, the demand for each depends on the price of all others. Pq is the sum of the prices of the n

Differentiating the profit functions with respect to the corresponding price variable yields these first-order conditions:

Summing the first-order conditions yields the equilibrium price for the unified land when the fragmented property rights are held by independent individuals, operating in an oligopolistic anticommons:

(5.3)

We can now compare these conditions with those that characterize the supply of a single owner of unified property with monopolistic control over his/her property (or by separate owners, who can effectively coordinate prices).

In the case where a single individual owns all property fragments, the profit function will take the following form:

By differentiating this profit function with respect to the price, we determine the first-order conditions for the single owner:

The interesting comparison is between the optimal prices in equations (5.3) and (5.5). One finds that the optimal price under unified property sold by a single monopolist (equation (5.5)) is actually lower than the total price that would be necessary in order to reunify the land under an oligopolistic anticommons (equation (5.3)). It is also interesting to look at the comparative statics of equation (5.3) with respect to the number of property fragments. By inspection, it is possible to see that both overall price, and overall deadweight loss, increases in n. In the case of oligopolistic anticommons, the strategic pricing of the fragmented property owners leads to higher prices: both the fragmented property sellers and the third-party developer see their respective surplus diminished compared to the alternative monopoly outcome.