Tackling the fallout from COVID-19

Laurence Boone

OECD

The novel coronavirus, COVID-19, hit China at the start of December and outbreaks have since spread more widely. The virus is bringing considerable human suffering.

It is also resulting in significant economic disruption from quarantines, restrictions on travel, factory closures and a sharp decline in many service sector activities. These disruptions are the direct channels through which the virus is affecting economies.There is ample reason to be cautious when assessing the economic consequences of the epidemic, given that the situation is evolving by the day. The main question for the economic outlook is for how long and how widely the virus will spread, and with it the containment measures. At this stage, there is little certainty on this, so we draw a bestcase scenario and a downside scenario (OECD 2020).

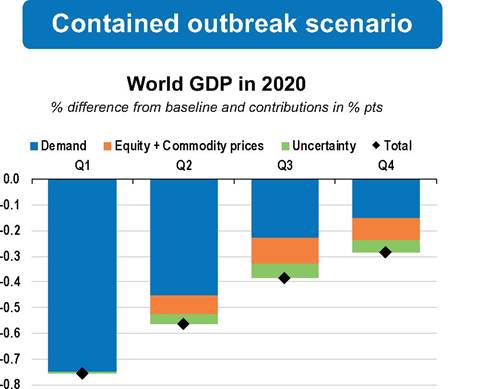

• The base-case scenario (the contained outbreak scenario in Figure 1) is based on the knowledge we have today of the spread of the epidemic, where the extent of the virus is broadly contained in China with some outbreaks in other countries. In this scenario, global economic growth would slow sharply in the first half of 2020, and then it would recover modestly.

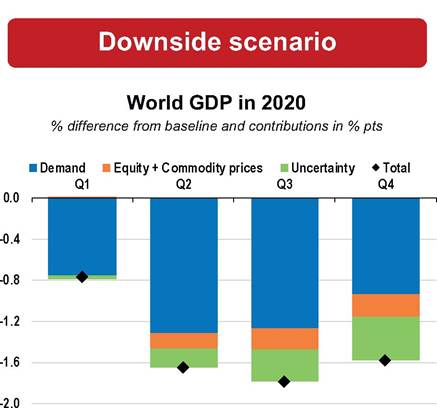

• We also consider an alternative, downside scenario (Figure 1) where there is broader contagion of the virus across the Asia-Pacific region and other advanced economies in Europe and North America. That means more containment measures, a wider decline in confidence, and a much more marked and prolonged slowdown.

Figure 1 Contained outbreak scenario and downside scenario

Note: This simulation shows the impact of a 4% fall in domestic demand in China and Hong Kong-China in 2020Q1 and a 2% decline in 2020Q2, plus declines of 10% in global equity and non-food commodity prices in the first half of 2020, and a 10 bps rise in investment risk premia in all countries in the first half of 2020.

All shocks are assumed to fade away gradually by early 2021.Source: OECD calculations using the NiGEM global macroeconomic model.

Note: This simulation shows the impact of a 4% fall in domestic demand in China and Hong Kong-China in 2020Q1 and a 2% decline in 2020Q2, plus a 2% domestic demand fall in most other Asia-Pacific countries and advanced Northern hemisphere countries in 2020Q2 and 2020Q3,plus declines of 20% in global equity and non-food commodity prices in 2020, and a 50 bps rise in investment risk premia in all countries in 2020. These shocks are assumed to decline gradually through 2021.

Source: OECD calculations using the NiGEM global macroeconomic model.

There are supply, demand, and confidence channels through which the virus affects the economy.

The arrival of the virus triggered containment measures, which are having a large economic impact. These measures include wide-ranging restrictions on passenger transportation and labour mobility, which especially affect the tourism and travel industry and the entertainment and leisure sector, as well as plant closures or reduced activity, spilling into global supply chains.

We can identify three main channels through which these measures spill over globally:

• Supply: significant disruptions in the global supply chain, factory closures, cutbacks in many service sector activities;

• Demand: a decline in business travel and tourism, declines in education services, a decline in entertainment and leisure services;

• Confidence: uncertainty leading to reduced or delayed consumption of goods and services, delayed or foregone investment.

The epidemic, via containment measures and the transmission channels, has sharply slowed manufacturing and domestic consumption in China and in its economic partners. In other countries, outbreaks that are more recent are also prompting containment measures. All this is severely affecting consumer and financial market confidence.

Two scenarios provide a range of possible outcomes

As the epidemic situation is evolving by the day, it is even more difficult than usual to project the economic outlook. This is why we focus on best-case and downside-risk scenarios in order to offer an interval of possible outcomes and policy proposals to soften the economic implications of the virus.

Best-case scenario

In a first best-case scenario, the epidemic stays contained mostly in China with limited clusters elsewhere.

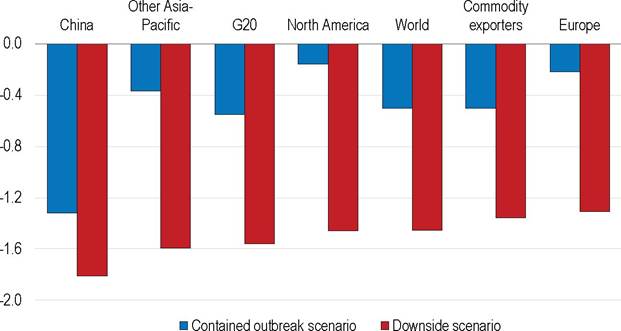

This would still affect global growth, which has been cooling for the past two years, bringing it to a subdued level. High-frequency indicators such as coal demand, air pollution, car sales and business surveys suggest the Chinese economy slowed sharply in the first quarter of 2020. As China accounts for 17% of global GDP, 11% of world trade, 9% of global tourism and over 40% of global demand for some commodities, negative spillovers to the rest of the world are sizeable. This affects primarily China, but also other countries’ supply and demand as well.

In our best-case scenario, most of the slowdown in activity comes from the contraction of demand in China. We have modelled the global impact of this contraction, including uncertainty effects and the impact on equity prices and commodity prices, and used it as a guide for the updated growth projections in the March OECD Interim Economic Outlook. The impact of the coronavirus outbreak, and the measures used to contain its spread, is akin to an adverse supply-side shock, with an enforced decline in the number of hours worked. However, the effects are mirrored in weaker demand. A decline in confidence, foregone income for laid-off workers, and lower demand for travel and tourism services all hit consumer spending; a reduction in cash-flow and higher uncertainty delay corporate investment; and existing inventory levels are run down due to the disruption of supply chains.

In this best-case scenario, overall, the level of world GDP is reduced by up to 0.75% at the peak of the shock, with the full year impact on global GDP growth in 2020 being around half a percentage point.

Most of this decline stems from the effects of the initial reduction in demand in China. Global trade is significantly affected, declining by 1.4% in the first half of 2020 and by 0.9% in the year as a whole.The impact on the rest of the world depends on the strength of cross-border linkages with China. In the near term, the adverse effects on GDP are relatively strong in Japan, Korea, other smaller economies in East and South-East Asia, and commodity exporters. All of these economies are significantly exposed to China via strong supply-chain linkages and tourism and other travel-related services.

The net effects of the combined shocks are deflationary, with consumer price inflation pushed down by around a quarter of a percentage point in 2020 in the OECD economies and by a little more in non-OECD economies.

We are obviously cautious in that this analysis cannot pick up the full extent of possible sharp discontinuities that might arise from the impact of the virus in China. These include possible supply-chain disruptions (particularly if alternative sources of supply are scarce) or the complete stop of cross-border travel into some locations. Such factors may change the impact of the virus outbreak over time and across regions.

Figure 2 Adverse impact on growth across regions

Change in GDP growth in 2020 relative to baseline (percentage points)

Note: Simulated impact of weaker domestic demand, lower commodity and equity prices and higher uncertainty. Contained outbreak scenario with the virus outbreak centred in China; downside scenario with the outbreak spreading significantly in other parts of the Asia-Pacific region, Europe and North America. Commodity exporters include Argentina, Brazil, Chile, Russia, South Africa and other non-OECD oil-producing economies.

Source: OECD calculations using the NiGEM global macroeconomic model.

How far the epidemic spreads will determine economic prospects, hence the downside scenario of broader contagion.

Downside scenario

In the downside scenario, the outbreak of the virus in China is assumed to spread much more intensively than at present through the wider Asia-Pacific region and the major advanced economies in the northern hemisphere in 2020. The scenario considers the additional impact if there were to be a sharp fall in private-sector demand in these regions as well.

Together, the countries affected in this scenario represent over 70% of global GDP (in purchasing power parity terms). While the extent of the restrictions on movement currently seen in China may not be fully replicated everywhere, many of the economic impacts are likely to be similar, with a significant hit to confidence, heighted uncertainty and (voluntary) restraints on travel and commercial and sporting events all likely to depress spending.

Overall, the level of world GDP is reduced by up to 1.75% (relative to baseline) at the peak of the shock in the latter half of 2020, with the full year impact on global GDP growth in 2020 being close to 1.5%. Initially, the adverse impact is concentrated in China, but the effects in the rest of Asia, Europe and North America gradually build up through 2020. The major part of the decline in GDP again stems from the direct effects of the reduction in demand, but the impact of heightened uncertainty accumulates gradually. World trade is substantially weaker, declining by around 3.75% in 2020, hitting exports in all economies.

The deflationary effects of the combined shocks are considerably larger than in the bestcase scenario, with consumer price inflation pushed down by around 0.6 percentage points in 2020 in the OECD economies.

Policy recommendations

Economic policy choices have an important bearing on cushioning the implications of containment measures and the speed at which the economy can adjust towards more normal conditions after the virus outbreak.

Increased government spending should be first directed at the health sector, supporting all necessary spending on prevention, containment and mitigation of the virus, including higher overtime pay and better working environment conditions, as well as research.

Supporting vulnerable households and firms is essential.

Containment measures and the fear of infection can cause sudden stops in economic activity. Beyond health, the priority should be on people. Options include using short-time working schemes and providing vulnerable households with temporary direct transfers to tide them over the loss of income from work shutdowns and layoffs. Increasing liquidity buffers to firms in affected sectors is also necessary to avoid debt default by otherwise sound enterprises. Reducing fixed charges and taxes and credit forbearance would also help to ease the pressure on firms facing an abrupt falloff in demand.

If the epidemic spreads outside China, the G20 should lead a coordinated policy response.

Countries should cooperate on support to healthcare in countries where it is needed, as well as on containment measures. In addition, if countries announced coordinated fiscal and monetary support, confidence effects would compound the effect of policies (OECD 2019, Boone and Buti 2019). This would help reverse the sharp decline in confidence that a more widespread outbreak would provoke. It would also be more effective than working alone. Our work presented in the November 2019 OECD Economic Outlook (OECD 2019) shows that if G20 economies implement stimulus measures collectively, rather than alone, the growth effects in the median G20 economy would be one-third higher after just two years.

Some would say it is trite to call for international cooperation. However, in this globally connected economy and society, the coronavirus and its economic and social fallout is everyone’s problem, even if firms decide in the wake of this virus shock to repatriate production and make it less inter-dependent.

Authors ’ note: For more information visit the latest Interim Economic Outlook, released 2 March 2020.

References

Boone, L and M Buti (2019), “Right here, right now: The quest for a more balanced policy mix”, VoxEU.org, 18 October.

OECD (2019), OECD Economic Outlook, Volume 2019 Issue 2, OECD Publishing.

OECD (2020), OECD Economic Outlook, Interim Report March 2020, OECD Publishing.

About the author

Laurence Boone is Chief Economist at the OECD, leading the Economics Department and supervising the contributions of the Economics Department to the New Approaches to Economic Challenges (NAEC) and Inclusive Growth (IG) initiatives. She represents the OECD on economic issues and participates with the Secretary-General in the International Monetary and Financial Committee, and with the OECD Sherpa in the G7 and G20 meetings. From 2016-2018 she was Chief Economist at AXA Group, and Head of Research and Member of the Management Board of AXA Investment Managers. From 2014 to 2016, Laurence was special advisor to the French president on multilateral and European economic and financial affairs. Prior to this, she was Chief Economist Europe & Managing Director at Bank of America Merrill Lynch Global Research, and Chief Economist France at Barclays Capital. Laurence holds a PhD in Applied Econometrics from London Business School, a postgraduate diploma in Quantitative Analysis and Modelling, and a Master’s degree in Economics from Paris X Nanterre University, as well as an MSc in Econometrics from the University of Reading.

3