The medium and the message

I am watching. Mostly, I am watching the commercials. There is nothing that can restore the faith of a day trader faster than a series of commercials for online brokerages.

(Anuff and Wolf, 2000: 136)

The increasing significance of electronic and visual media has occurred at the same time as the image of international finance has become more complex and difficult to represent.

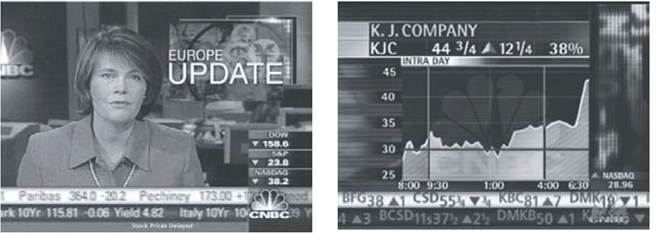

As information technology has taken over many of the functions and relationships of financial practice (like open outcry markets), greater and greater anonymity has accompanied the investment and trading process (Wilhelm and Downing, 2001). Whatever the historical image of international finance was in London and New York, the screen has swamped that image and has replaced it with a cacophony of images, noise and visions. It is also accompanied by a distinctive rhetoric.5The US television channels CNBC and MSNBC, which are rebroadcast globally, provide illustrative examples. On both these channels, the eye is bombarded by an array of constantly changing images and information. While the program anchor remains important, s/he is constantly framed by an electronic ticker tape displaying the latest prices for stocks and bonds and the aggregate price for the three major US stock indices (priced in red or green depending on the day’s trading). Further, programs are presented at breathtaking speed, interviews are interrupted for breaking news, expert analysis deploys yet more data displays, reports from the New York Stock Exchange or the Chicago Mercantile are formulaically fronted by attractive women and backgrounded by the noise, color and hubbub of open outcry trading. These techniques owe more to MTV than to the “serious and sober” financial journalism of the Financial Times or the Wall Street Journal. In doing so, they breathe a new life into finance, turning it into a living organism.

Rather than a rational entity, finance becomes a performative, continuous activity whose appreciation assumes a minimum level of financial literacy

Figure 8.1 Talking about finance

We should not underestimate the importance of these screens which are not only consumed by financial end-consumers, and as such are part of the ecology of everyday life, but are also viewed by more skeptical financial professionals who know that outrageous claims on CNBC or CNNfn can still move markets. While they may be consumed by the new financial audience, they are thus constitutive of the entirety of finance. Furthermore, although they have evidently not replaced canonical entertainment programs in the popular imagination, the sheer ubiquity of money channels in hotel chains around the world, or airport lounges, suggest a presence that is coterminous with the service functions for the global economy. These global money shows have a self-conscious attempt to place reporting according to the 24-hour market trading cycle around the world. Managing time is as important as managing the image of financial reporting (Galison, 2000), a feature emulated in the clocks on the trading screens of financial professionals. Such screens accompany the long periods of “down-time” in finance and at least give the illusion that they are making unproductive time more productive, just as laptops, PDAs and mobile phones have made investment management possible while on the move. Increasingly, the “rhythms of reception produced by the cycles and patterns of [financial] broadcasting overlap with the rhythms of social life” (McCarthy, 2001: 196).

A useful distinction can be made between the passive components of the screen and the active components of the screen. The former include data, updates of data, and so-called news. These are provided rather than discussed, though the implication is always that this is done in real-time as opposed to the delayed material which dominates news magazine programs.

Even so, compared with the Bloomberg channel, the material passively displayed is rarely completely up-to-date. Furthermore, again unlike Bloomberg, data cannot be accessed, displayed and analyzed. While no doubt useful, such passive material is more often than not material for watching and to feed curiosity rather than market trading.By contrast, active components of the screen are presented as if the information and opinion being imparted is urgently needed by the viewing audience. In this sphere of CNBC, “talking heads” dominate with comment, discussion, and the presentation of multi-colored graphics summarizing stock market data. Breathless excitement characterizes such commentary, being associated with “breaking news”, “new information”, and “unexpected events”. Talk is fast and furious. Talk is also often interrupted by some sudden happening, and talk moves on at a breakneck pace covering topic after topic - interrupted, of course, by commercial breaks. Flicking between channels as one might between MTV, VH-1, and CNN might also mean missing a so-called vital piece of information mixed in with all the other material so quickly displayed and so quickly discarded.

Associated with the “talking heads” are regular trading floor commentaries. In these brief moments of report from the action, reporters appear to stand in the middle of Wall Street jostled by exceedingly active - even frantic - traders going about their business. These reporters may be male or female and report to us as if they know something that we don’t know. Over time, they have gained their own following even if they seem to come and go on and off the program without any announcement of departure. As we move on with the program it seems that its producers have made a couple of very basic assumptions about the time we take to watch as well as our capacity for concentration. In the first instance, program producers assume we dip in and dip out of the program with five minutes here and five minutes there.

It appears we don’t follow the program for more than a couple of commercial breaks. Furthermore, it appears that our concentration can only last between 45 seconds and 90 seconds on any one issue. Perhaps they’re right. Perhaps MTV is more challenging and more entertaining!Until recently, much of the active information presented on CNBC has had a positive gloss.6 There were always good stocks, amazing success stories, and hitherto untold opportunities for making a profit. Rarely were investors advised to divest from a particular stock, withdraw from a particular market or given a bleak assessment of market trends (although market bears were treated with respect: the fear that such animals engendered was a perfect emotive counterweight to the relentless good news elsewhere). At the same time, program presenters and pundits took the opportunity to encourage investors to avoid the market herd and take advantage of little-known, out-of-favor opportunities. They know we follow the news, and they know we are self-conscious of our unwillingness to go against market leaders. Like so much of financial market reporting, stocks are hardly ever talked down, while falling share prices are market corrections and even opportunities. Critically, an Orwellian golden rule is that the positive evaluations which turn out to have been wrong are never returned to. He who controls the past truly does control the future, at least on CNBC.

All this activity is executed in a most aggressive manner. In the middle-ground, the presenter is newsworthy in their own right. The banter between the host, commentators and guests is positive but combative. Each personality has their apparent important place in the financial industry - otherwise, why would they be on the show? But it is rare for guests to finish their presentations. Being interrupted, being shunted sideways in favor of breaking news, and having one’s image drowned by a graphic are ever-present risks associated with being on the show However, in contrast, one real advantage of being on the show is that the host never ever questions the veracity of stated opinions.

Commentators and guests never have toPerformingfmance 175 reveal their own interests in the opinions being portrayed and displayed. But we know, of course, that all these pundits have a stake in having their views positively received by the audience (Kurtz, 2000). If they do not directly and immediately benefit from their exposure on the program, can we be sure that their employers do not reach for the calculator to assess likely future bonus payments? While it would be narve to believe that the audience is uncritical in their construction of these opinions (see, for example, Philo, 1990; Dahlgren, 1992, on the construction of information from TV news media) and that what construction of disputability there is is mainly false, the constant drip of infotainment has a subtly opiate effect (for parallels, see Roscoe and Hight, 2001). After all, advertising and commercial interests dominate the channel so why should we expect “independent” advice as if the audience’s best interests are those served by the program? Indeed, seen in this way, perhaps much of the commentary and opinion given out on channels like CNBC is closer to advertising than independent advice and should be understood as such.