A Dynamic Simulation of the Effects of Monetary and Real Shocks

To visualize the impulse response functions of the model to nominal and real shocks, we review the results of dynamic simulations of the model. The first simulation follows an unanticipated temporary 1% shock to the nominal interest rate, and the second follows an unanticipated 1% shock to productivity.

We use the version of the model without staggered pricing.The simulations are based on the following values of the parameters: α = 0.333, ρ = 2%, θ = 1, δ = 0.5, ϕπ = 1.5, ϕu = 0.5, ηA = 0.75, and γ = 0. The natural rate of unemployment is assumed equal to 5%, and the target inflation rate is 2%.

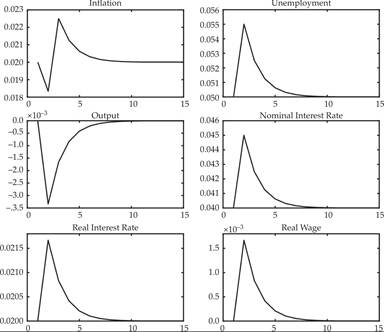

Figure 17.1 presents the impulse response functions of the model following an unanticipated temporary 1% shock to the nominal interest rate. Note that such a nominal shock does not affect the natural rate of real variables, which only depend on real shocks.

Figure 17.1 Impulse response functions following a 1% unanticipated temporary positive shock to the nominal interest rate.

Inflation initially falls below the target of 2%, unemployment rises above its natural rate of 5%, and output falls below its own natural rate. The real interest rate and the real wage rise above their natural rates. Because of the fall in inflation and the rise in unemployment, after the initial shock, the nominal interest rate follows a downward path toward its natural rate of 4%, inflation rises, unemployment gradually declines toward its natural rate, and all other real variables adjust toward their natural rates too. Thus, a temporary nominal shock has persistent real effects, because of the persistence of deviations of employment from its natural rate.

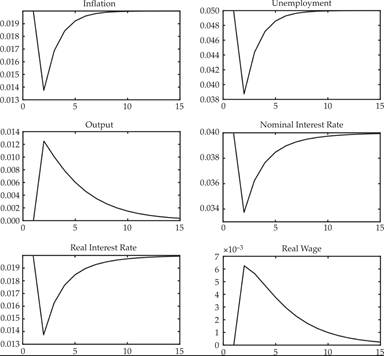

Figure 17.2 presents the impulse response functions of the model following an unanticipated 1% shock to productivity a. Inflation initially falls, and so does unemployment and nominal and real interest rates relative to their steady state natural rates. Output rises above its natural rate, and so do real wages. Following the initial shock, all variables gradually return to their steady state natural rates.

Figure 17.2 Impulse response functions following a 1% unanticipated persistent positive shock to productivity.

Thus, both nominal and real shocks cause persistent deviations of all variables from their steady state values.

Also note that the correlation of inflation and unemployment (or output) depends on the nature of the shocks. The short-run correlation of inflation and unemployment following a nominal shock is negative, because unanticipated inflation reduces unemployment. But the short-run correlation of inflation and unemployment is positive following a real shock, because higher productivity reduces both inflation and unemployment. Thus, this model could explain stagflation as the outcome of negative real shocks.

17.10