Monetary Policy, Financial Frictions, and the Zero Lower Bound on Interest Rates

The interest rate rules we have been examining up to now assume that there are no financial frictions and that the central bank can freely adjust the nominal interest rate.

In chapter 19, we discussed the nature of financial frictions and how they can result in financial crises, such as that of 2008–2009 or the Great Depression of the 1930s.

We also analyzed the macroeconomic implications of financial frictions, using two alternative new Keynesian models, one with staggered pricing and one with periodic nominal wage contracts. We showed that if the central bank follows a Taylor [1993] rule for interest rates, financial frictions that raise the external finance premium result in recessions and deflations, in the sense that inflation falls below the optimal inflation rate.We also argued that the normal Taylor rule is not the optimal macroeconomic response to a financial markets shock. The optimal macroeconomic response would be for the central bank interest rate to completely neutralize the rise in the external finance premium, by falling sufficiently so as to completely avert a recession. This can be achieved if the response of the central bank interest rate to inflation became infinitely large, completely stabilizing the inflation rate at its optimal level. However, this may not be possible if there is a zero lower bound on interest rates.

Prior to the Great Recession of 2008–2009, inflation was low and close to official target rates in the advanced economies, so that short-term nominal interest rates tended to deviate relatively little from their long-run average. The only exception was Japan, where short-term nominal interest rates had been close to zero since the 1990s. Central banks in the other industrialized economies responded to the Great Recession by lowering key policy interest rates to, or very close to, zero.

Because the nominal return from holding money in the form of cash is equal to zero, it is generally accepted that central banks cannot sustain their policy interest rates below zero, as cash can always be held as an alternative to negative interest rate bearing assets, such as deposits or bonds.

The implication is that nominal interest rates have a zero lower bound even if the state of the economy requires negative nominal and real interest rates to minimize deviations of inflation from target and output and employment from their natural rates. Hence, conventional monetary policy cannot respond effectively to financial or other shocks that tip the economy toward the zero lower bound.20.7.1 The Liquidity Trap

Such a situation was referred to as a theoretical possibility by Keynes in the General Theory and has since been known as a liquidity trap. Keynes [1936, p. 187] argued

There is the possibility … that, after the rate of interest has fallen to a certain level, liquidity-preference may become virtually absolute in the sense that almost everyone prefers cash to holding a debt which yields so low a rate of interest. In this event the monetary authority would have lost effective control over the rate of interest. But whilst this limiting case might become practically important in future, I know of no example of it hitherto.

The liquidity trap was analyzed by Modigliani [1944] as a special case of the Keynesian model in which the LM curve becomes flat, and monetary policy is thus ineffective. In such a case, a monetary expansion would fail to further reduce nominal and real interest rates, increase aggregate demand, and counteract deflation and recession.

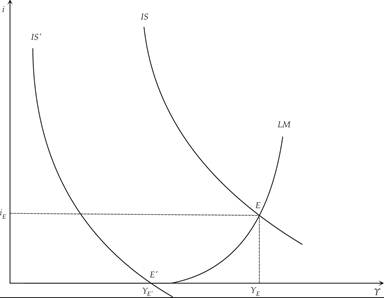

The liquidity trap can be analyzed with the help of figure 20.2. Assume that the economy is at an initial equilibrium E, and that a negative shock to aggregate demand shifts the IS curve to the left. Short-run equilibrium output moves from YE to YE′, and the nominal interest rate shifts from iE to zero.

Figure 20.2 The liquidity trap.

The central bank cannot counteract the contraction in aggregate demand by increasing liquidity.

Increases in liquidity cannot result in further reductions in nominal interest rates, because households and firms prefer to hold money (which has a zero nominal yield) to bonds (which would have a negative nominal yield). Hence, conventional open market operations, in which the central bank increases liquidity by exchanging money for short-term bonds, would have no effect on nominal interest rates. Commercial banks and the nonbank public would be quite happy to exchange zero-yield bonds or deposits for cash, without any effect on the price or yield of these bonds.20.7.2 Monetary Policy at the Zero Lower Bound

As already mentioned, the theoretical possibility of a liquidity trap became a reality in Japan during the 1990s, and in the other industrial economies in the aftermath of the recession of 2008–2009, when short-term interest rates touched the zero lower bound and in some cases became slightly negative for a brief period.

The analysis of monetary policy at the zero lower bound became an active area of research since Krugman [1998] studied it, prompted by the Japanese experience. Krugman used an intertemporal model of savings and investment with and without price flexibility. Eggerstsson and Woodford [2003], Jung et al. [2005], and others have since extended the analysis to new Keynesian models.

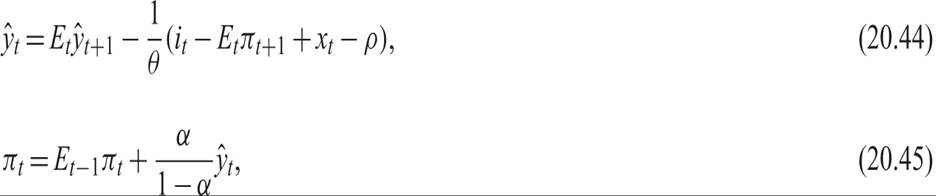

To analyze the conduct of monetary policy at the zero lower bound, consider the model consisting of (20.1) and (20.2), augmented for an external finance premium, as in chapter 19. We abstract from productivity shocks to focus on financial shocks. The modified model thus takes the form

where xt is, as in chapter 19, an exogenous external finance premium. This is our financial shock.

Consider the impact of a large xt. To avert a recession would then require a reduction in the central bank nominal interest rate it that would make the real interest rate plus the external finance premium equal to the natural interest rate ρ.

Thus, the central bank nominal interest rate would have to be

If the shock to the external finance premium is large enough (i.e., if xt > ρ + Etπt+1), then the central bank nominal interest rate ought to become negative. If it cannot become negative because of the zero lower bound, then from (20.44), a recession cannot be avoided.

Hence, the zero lower bound constraint (that the central bank cannot reduce nominal interest rates below zero) results in financial shocks and also other aggregate demand shocks, which could in principle be neutralized by monetary policy, having real effects on output and employment. If the central bank could fully adjust nominal interest rates below the zero lower bound, negative aggregate demand shocks would not affect output and employment in this model. It is only because nominal interest rates may hit the zero lower bound that we end up with real effects for financial and other aggregate demand shocks, even under the optimal policy.

20.7.3 The Zero Lower Bound and Unconventional Monetary Policy

Is there scope for additional action from monetary policy in such a case? Krugman [1998] and Eggerstsson and Woodford [2003] have suggested a potential solution that rests on the central bank announcing that it will not return to its inflation target π* (at least in the immediate future) and that future inflation will be above target. For example, assume that the central bank announced that its inflation target for t + 1 would be high enough that the nominal interest rate in (20.46) is positive, despite the shock to the external finance premium. If that was credible, then from (20.46), the recession would be avoided, as the current real interest rate, including the external finance premium, would become equal to the natural rate.19

Obviously, if π* is the optimal inflation rate, then implementing a policy such as that implied by the above discussion would not result in optimal future inflation.

The upshot of this analysis is that managing expectations about future inflation is potentially an important form of unconventional monetary policy at the zero lower bound. The announcement of higher future inflation targets, even temporarily, is a form of unconventional monetary policy called forward guidance. As central banks cannot use conventional monetary policy to further reduce short-term nominal interest rates below the zero lower bound, they are using announcements about future monetary policy to affect current expectations about future inflation and thus affect real interest rates; aggregate demand; and through aggregate demand, aggregate income and employment.

To be more credible, forward guidance must be accompanied by action. At the zero lower bound, open market operations (such as further purchases of short-term securities by the central bank) would have no further effect on short-term nominal interest rates. Thus, even if the central bank expands the money supply, the additional money is willingly held by the public, because it is considered a perfect substitute for short-term bonds, which pay an interest rate of zero.

An additional unconventional way in which policy can attempt to stimulate the economy is by direct intervention in credit markets that would affect the external finance premium. In 2008 and 2009, the Federal Reserve and other central banks took actions aimed at the markets for specific types of credit, supporting commercial-paper issuance, mortgage lending, and so on. Such actions are clearly most likely to be effective when the particular markets they are aimed at have been disrupted, as in the case of a financial crisis.

The appropriate response of monetary policy is to increase liquidity in order to increase bank lending and reduce interest rates, thereby reversing the effects of the financial crisis and the rise in the external finance premium on aggregate demand. In addition, central banks may be required to act as lenders of last resort to the banking system and to bail out banks, in order to prevent deleveraging, bankruptcies, and further reduction in aggregate demand, output, and employment.

The policy of continuing to expand the money supply at the zero lower bound is usually called quantitative easing and is a policy that was widely adopted in the aftermath of the financial crisis of 2008–2009, when interest rates reached the zero lower bound. By increasing the money supply, quantitative easing makes the commitment to higher future inflation, through forward guidance, more credible.

Another possible way for the central bank to provide stimulus in the face of the zero lower bound is to purchase assets other than short-term government debt in its open market operations. This is another form of unconventional monetary policy, called asset purchases. For example, the central bank can purchase long-term government debt or corporate debt, both of which are likely to offer positive nominal returns even when the interest rate on short-term government debt is zero. One can envisage such transactions as conventional open market operations, followed by exchanges of short-term zero-interest government debt for the alternative asset. Such open market operations can reduce long-term rates and the external finance premium directly. These operations thus affect aggregate demand, even when short-term interest rates are at the zero lower bound. Open market operations that involve buying assets other than short-term government debt are an additional form of quantitative easing.20

Another type of unconventional open market operation that has attracted considerable attention is exchange market intervention (Svensson [2001]). By purchasing foreign currency or other foreign assets, the central bank can presumably cause the domestic currency to depreciate. An exchange rate depreciation will also stimulate aggregate demand and increase output and employment.

In conclusion, the zero lower bound and financial frictions are serious issues that are likely to constrain monetary policy under particular circumstances, such as a financial crisis. The recent experience of the 2008–2009 financial crisis, and its theoretical analysis, have provided important lessons about unconventional forms of monetary policy and its effects and also revived interest in the use of fiscal policy as a tool for stabilizing the economy.21

We shall return to how the financial crisis of 2008–2009 has affected not only the analysis of monetary policy but also macroeconomic modeling in general in chapter 23.

20.8