Rules, Discretion, and Credibility in a New Keynesian Model

Let us start with a simple version of the new Keynesian model based on periodic nominal wage contracts that we analyzed in chapter 17. The model can be summarized as follows:

where ŷt = yt −  is excess output (i.e., the deviation of (the log of) real output from its natural rate), it is the nominal interest rate, πt is the rate of inflation, 1/θ is the intertemporal elasticity of substitution in consumption, 0 < α < 1 is the exponent of labor in a Cobb-Douglas production with labor as the only factor of production, r N is the natural real interest rate, and εA is a white noise shock to productivity.

is excess output (i.e., the deviation of (the log of) real output from its natural rate), it is the nominal interest rate, πt is the rate of inflation, 1/θ is the intertemporal elasticity of substitution in consumption, 0 < α < 1 is the exponent of labor in a Cobb-Douglas production with labor as the only factor of production, r N is the natural real interest rate, and εA is a white noise shock to productivity.

Equation (20.1) is the new neoclassical synthesis IS curve, determining aggregate demand, and (20.2) is an expectations-augmented Phillips curve.6

To focus on the issue of rules versus discretion and simplify matters, assume that the central bank can use its monetary policy instruments to affect aggregate demand and therefore deviations of output from its natural rate.

Recall that in this model, the natural rate of output is lower than full employment output because of the behavior of labor market insiders. The deviation of full employment output from its natural rate is equal to

where  is the natural rate of unemployment, assumed to be sub-optimally high. If the natural rate of unemployment is positive, then deviations of full employment output from the natural rate of output are also positive.

is the natural rate of unemployment, assumed to be sub-optimally high. If the natural rate of unemployment is positive, then deviations of full employment output from the natural rate of output are also positive.

From (20.2) and (20.3), we can see that deviations of current output from full employment output are determined by

To further simplify the analysis, let us initially assume that there are no exogenous stochastic shocks. Thus the natural real rate of interest is constant at ρ, the pure rate of time preference, and the natural rate of unemployment is constant at  .

.

In the absence of productivity shocks, the model can thus be written as

Thus, (20.5) and (20.6) describe deviations of inflation from previously expected inflation, and deviations of output from full employment output, in terms of deviations of output from its natural rate and the natural rate of unemployment, assumed positive and constant.

20.2.1 The Social Welfare Loss from Inflation and Unemployment

To evaluate the welfare losses from deviations of output from full employment and from inflation, we need a criterion for social welfare. Assume that the present value of the expected social welfare loss from inflation and unemployment is given by

alt=eq20-7.png>

We thus assume that the one-period losses from inflation and unemployment are quadratic. We also assume that β = 1/(1 + ρ) is the discount factor, which depends on the pure rate of time preference ρ; that ζ is the weight of the inflation objective relative to the output objective in the social loss function; and that π* is the optimal inflation rate. This social welfare function can be justified in terms of the suboptimality of deviations of output from full employment output, and the suboptimality of deviations of inflation from the optimal inflation target of the central bank.

Note that we have assumed that the central bank aims to stabilize output around full employment output and not the natural rate of output, which, because of the distortions in the labor market, is suboptimally low.

20.2.2 Monetary Policy under Discretion: The Problem of Credibility

Assume that the central bank chooses interest rates in each period to minimize the loss function (20.7), subject to system of (20.5) and (20.6) and taking the expectations of wage setters as given. Let us call this behavior the discretionary policy. From the first-order conditions for the minimization of (20.7) subject to (20.6), it follows that

In rational expectations equilibrium, and because there are no exogenous stochastic shocks, actual and expected inflation will coincide. Thus, from (20.8), equilibrium inflation will be equal to

Equilibrium inflation under discretion πD will be higher than the optimal inflation rate π*, which is the central bank’s target.

In rational expectations, equilibrium output will also fall short of full employment output, because from (20.6), even when deviations of output from its natural rate are zero, deviations of output from full employment output will be negatively related to the natural rate of unemployment:

Thus, equilibrium inflation will be constant and higher than the optimal central bank inflation target π*. This is because of the incentives of the central bank to reduce unemployment below its natural rate. Inflation will be higher than the optimal inflation target π*, because wage setters anticipate the incentives of the central bank to increase aggregate demand in order to reduce unemployment below its natural rate. Hence, they raise their inflationary expectations to a level where the central bank no longer has an incentive to create surprise increases in aggregate demand and inflation.

Any inflation rate lower than πD creates incentives for the central bank to push inflation up in the short run, in order to reduce unemployment. Thus, an inflation rate below πD lacks credibility.Note that the equilibrium inflation rate depends on the parameter ζ of the social welfare function. The higher is ζ (i.e., the more the social welfare function penalizes inflation relative to output), the lower will be the inflationary bias of discretionary monetary policy. A lower ζ (i.e., a social welfare function that penalizes unemployment more than inflation) will result in a higher inflationary bias.

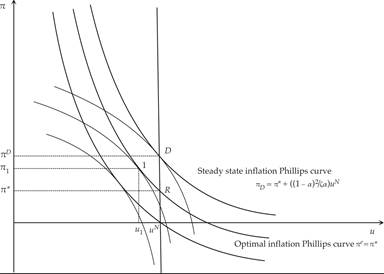

The inflationary bias of discretionary policy is depicted in figure 20.1. The equilibrium inflation rate under discretion is determined at the point where the highest possible indifference curve of the central bank is tangent to the short-run Phillips curve, at the natural rate of unemployment  = u N. Lower inflation rates lack credibility. Assume that the central bank announces that it will stick to an inflation rate equal to π*. If wage setters believe it, the short-run Phillips curve will be the optimal inflation Phillips curve. If the central bank sticks to its announcement, the equilibrium will be at R, with inflation at π* and unemployment at = u N. However, under the discretionary policy, the central bank will maximize social welfare in the short run by raising inflation to π1 so as to reduce unemployment to u1, below the natural rate

= u N. Lower inflation rates lack credibility. Assume that the central bank announces that it will stick to an inflation rate equal to π*. If wage setters believe it, the short-run Phillips curve will be the optimal inflation Phillips curve. If the central bank sticks to its announcement, the equilibrium will be at R, with inflation at π* and unemployment at = u N. However, under the discretionary policy, the central bank will maximize social welfare in the short run by raising inflation to π1 so as to reduce unemployment to u1, below the natural rate  = u N. Thus, the initial announcement lacks credibility. The only inflation rate that does not lack credibility is the rate πD, at which the central bank has no further incentives to increase inflation in order to reduce unemployment.

= u N. Thus, the initial announcement lacks credibility. The only inflation rate that does not lack credibility is the rate πD, at which the central bank has no further incentives to increase inflation in order to reduce unemployment.

Figure 20.1 Inflation and lack of credibility under a discretionary policy.

Under discretion, the central bank does not achieve any of its social objectives. Output and unemployment remain at their natural rates below full employment. Equilibrium inflation turns out to be higher than the optimal inflation rate, because of the rational adjustment of the inflationary expectations of wage setters. As first pointed out by Kydland and Prescott [1977] and Barro and Gordon [1983a] using related models of the expectationally-augmented Phillips curve, if the natural rate of unemployment is inefficiently high, discretionary policy aimed at achieving full employment is characterized by an inflation bias. The discretionary policy results in an equilibrium inflation rate higher than the central bank target, without any effects whatsoever on equilibrium unemployment.7

The social welfare loss under the discretionary policy is given by

where ΛD denotes the discounted social welfare loss from inflation and unemployment under the discretionary policy.

To the extent that the natural rate of unemployment is inefficiently high, there will be a positive inflation bias in a discretionary monetary policy that aims for full employment. Monetary policy cannot permanently reduce unemployment below its natural rate.8

Policies other than monetary policy—such as labor market and tax policies, which can affect the natural rate of unemployment—may be used for that purpose.9

Note that this theory of inflation, which is generally considered to be the theory that explains the moderately high inflation rates in the industrial economies in the late 1960s and the 1970s, is different from the theories of high inflation based on the need for seigniorage revenues that we analyzed in chapter 12.

Seigniorage-revenue theories of high inflation are generally considered to be more appropriate for economies with weak fiscal systems, such as some less-developed economies, or economies that have emerged from a major economic disruption (for example, a war).20.2.3 Monetary Policy under a Fixed Inflation Rule

Let us now assume that, although the discounted social welfare loss is described by the loss function (20.7), the government instructs the central bank to follow a fixed inflation target, π = π* in every period, by following a rule that minimizes

From the first-order conditions for a minimum of (20.12), we have

Inflation is equal to the optimal inflation target rate in every period. Equilibrium output still falls short of full employment output, because it is determined as in (20.10).

The social welfare loss under the constant inflation rule is given by

where ΛR denotes the discounted social welfare loss under the optimal inflation policy rule.

Thus, under a fixed optimal inflation policy rule, social welfare losses are lower than under discretion. There is an improvement in social welfare if the government instructs the central bank to follow the optimal inflation rule irrespective of unemployment. Inflation is at the socially optimal level π*, and unemployment is at its suboptimally high natural rate, which is the case with the discretionary policy as well.

Although this is not a first-best outcome for the government, or society, it is better than the outcome under discretion, where unemployment is at its suboptimal natural rate anyway, and inflation is higher than optimal inflation. In the absence of alternative policies to reduce the natural rate of unemployment, the optimal monetary policy is the policy under the fixed inflation rule. This rule dominates discretion in the absence of shocks.

20.2.4 Central Bank Constitutions

The question of how to constrain the government to have the central bank follow such an optimal inflation rule (and thus not resort to the discretionary policy) can be addressed by appropriate amendements in the constitution of the central bank.

As Rogoff [1985] has shown, the optimal inflation rule can be implemented by creating a politically independent central bank that is constrained by its constitution to be concerned only with inflation and not with full employment. This can be formally modeled by modifying the loss function of the central bank in either of the following two ways.

The first is to allow the weight ζ on inflation relative to output in the preferences of the central bank to go to infinity. In this case, we end up with the independent central bank instructed to minimize the loss function (20.12), which only depends on inflation and results in the optimal policy rule (20.13).

The second is to modify the output objective in the loss function of the central bank. Instead of the central bank targeting deviations of output from full employment, it can only target deviations of output from its natural rate. The central bank does not seek to keep the economy at full employment, but only at its natural rate. In this case, the loss function minimized by the central bank takes the form

and is minimized subject to (20.5) rather than to (20.6).

From the first-order conditions for a minimum, we have

where

In rational expectations equilibrium, the inflation rate will be equal to

Thus, an independent central bank that does not systematically try to reduce unemployment below its natural rate will implement the optimal monetary policy as well. This solution can also be implemented by appropriately modifying the constitution of an independent central bank, so that it will then be constrained to follow the optimal policy by minimizing the objective (20.15). This objective states that the central bank should aim for the optimal inflation rate π*, unless unemployment deviates from its natural rate.

What is the difference between the objectives (20.12) and (20.15)? In the absence of stochastic shocks to inflation and unemployment, the two objectives lead to the same outcome: the stabilization of inflation at its optimal rate π*. However, as we shall see below, in the presence of shocks that affect unemployment independently of inflation, the objective (20.15) allows for more flexibility. The central bank can react to shocks that cause deviations of unemployment from its natural rate, something that it would not be able to do if its constitution constrained it to maintain inflation at π* under all circumstances.

20.2.5 Reputation as a Solution to the Problem of Inflationary Bias

Restrictive constitutions for central banks are not the only solution to the problem of the inflationary bias of discretionary monetary policy. An alternative is for the central bank to commit in advance to the optimal inflation policy π* and to not succumb to the short-run incentives of following the discretionary policy. This way, the central bank will acquire an anti-inflationary reputation, although wage setters know that it has a short-run incentive to follow the discretionary policy. The solution based on the acquisition of an anti-inflationary reputation was first analyzed by Barro and Gordon [1983b]; Backus and Driffill [1985a, b], Tabellini [1985], and Barro [1986].

To analyze this reputational mechanism, we need to explicitly analyze monetary policy as a repeated infinite-horizon game between the central bank and wage setters in the labor market. In this game, the central bank chooses inflation, and wage setters choose their inflation expectations. Such repeated games have multiple equilibria. There are at least two possible equilibria in this case.10

The first is the time-consistent equilibrium, in which the central bank always follows the discretionary policy. The properties of this equilibrium are that unemployment is equal to its natural rate and inflation is higher than the optimal inflation rate, as in (20.9).

The second is a time-inconsistent reputational equilibrium, in which the central bank chooses to continuously follow the optimal inflation strategy (20.13), not succumbing to the short-run incentive to create surprise inflation in order to reduce unemployment below its natural rate. This equilibrium results in the optimal inflation policy, but it is time inconsistent, in the sense that the central bank always has a short-run incentive to depart from the equilibrium policy.

The question that naturally arises is: What is the mechanism that stops the central bank from departing from the reputational policy and reverting to the time-consistent policy, in the absence of a restrictive constitution? The short answer is the risk of the loss of its anti-inflationary reputation.

By sticking to the reputational policy, the gain for the central bank is the difference between the discounted future losses of the time-consistent policy and the reputational policy. From (20.11) and (20.14), this difference is equal to

Expression (20.19) is a measure of the welfare benefits from sticking to the time-inconsistent reputational policy rule. Thus, it measures the cost to the central bank of losing its antiinflationary reputation.

Suppose that to reduce unemployment, the central bank succumbs to the short-run incentive to follow the time-consistent discretionary policy and thus creates surprise inflation. With inflationary expectations predetermined at π*, the central bank would reduce unemployment below its natural rate and would gain a one-period welfare benefit equal to

Thus, if by departing from the optimal policy once, the central bank risked losing its antiinflationary reputation forever, the net gain would be the difference between the one-period gain (20.20) and the discounted loss (20.19). This difference is equal to

id=eq20-21.png class="lazyload" data-src="/files/uch_group77/uch_pgroup317/uch_uch7367/image/image1405.jpg" alt=eq20-21.png>

which is always negative for a nonnegative pure rate of time preference, so the central bank would never depart from the reputational equilibrium in this model. The condition for (20.21) to be positive is (1 − α)2 < −βζα2, which cannot be satisfied. The threat of the loss of its anti-inflationary reputation forever is sufficient to sustain the reputational equilibrium in this case.

The reputational equilibrium can also be sustained by less extreme threats to the anti-inflationary reputation of the central bank. Thus, if the behavior of wage setters was such that the central bank lost its anti-inflationary reputation only for one period and not forever, then net the gain for the central bank would be equal to

This would be positive if and only if

The smaller the discount factor β and the higher the relative weight of inflation ζ in the social welfare function, the more likely it is that even the threat of a temporary loss of anti-inflationary reputation can sustain the reputational equilibrium. Thus, reputational mechanisms can also be a solution to the problem of the inflationary bias of monetary policy.

20.3