The Lab-Equipment Model of Growth with Input Varieties

Let us start with a particular version of the endogenous growth model with expanding varieties of inputs and an R&D technology that only uses output for creating new inputs. This is sometimes referred to as the lab-equipment model, since all that is required for research is investment in equipment or in laboratories—rather than the employment of skilled or unskilled workers or scientists.

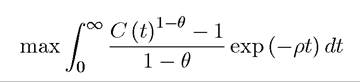

13.1.1. Demographics, Preferences and Technology. Imagine an infinite-horizon economy in continuous time admitting a representative household with preferences

There is no population growth and the total population of workers, L, supplies labor inelasti- cally throughout. Let us assume, as discussed in the previous chapter, that the representative household owns a balanced portfolio of all the firms in the economy. Alternatively, we can think of the economy as consisting of many households with the same preferences as the representative household and each household holding a balanced portfolio of all the firms.

The unique final good of the economy is produced with the following aggregate production function:

where L is the aggregate labor input, N (t) denotes the different number of varieties of inputs (machines) available to be used in the production process at time t, and x (ν, t) is the total amount of input (machine) type ν used at time t. I assume that x’s depreciate fully after use, thus they can be interpreted as generic inputs, as intermediate goods, as machines, or even as capital as long as we are comfortable with the assumption that there is immediate depreciation. The assumption that the inputs or machines are “used up” in production or depreciate immediately after being used makes sure that the amounts of inputs used in the past do not become additional state variables.

This simplifies the exposition of the model (though the results are identical without this assumption, see Exercise 13.22). Nevertheless, I refer to the inputs as “machines,” which makes the economic interpretation of the problem easier.The term (1 — β) in the denominator is included for notational simplicity. Notice that for given N (t), which final good producers take as given, eq. (13.2) exhibits constant returns to scale. Therefore, final good producers are competitive and are subject to constant returns to scale, justifying our use of the aggregate production function to represent their production possibilities set.

One can also write (13.2) in the following form

where with εβ ? 1∕β as the elasticity of substitution between inputs. This form emphasizes both the constant returns to scale properties of the production function and the continuity between the model here and the Dixit-Stiglitz model of the previous chapter.

with εβ ? 1∕β as the elasticity of substitution between inputs. This form emphasizes both the constant returns to scale properties of the production function and the continuity between the model here and the Dixit-Stiglitz model of the previous chapter.

The resource constraint of the economy at time t is  where X (t) is investment or spending on inputs at time t and Z (t) is expenditure on R&D at time t, which comes out of the total supply of the final good.

where X (t) is investment or spending on inputs at time t and Z (t) is expenditure on R&D at time t, which comes out of the total supply of the final good.

We next need to specify how quantities of machines are created and how new machines are invented. Let us first assume that once the blueprint of a particular input is invented, the research firm can create one unit of that machine at marginal cost equal to ψ > 0 units of the final good. The innovation possibilities frontier, which regulates the technology for the creation of new machines, takes the following form:

where η > 0, and the economy starts with some initial technology stock N (0) > 0.

This implies that greater spending on R&D leads to the invention of new machines. Throughout, I assume that there is free entry into research, which means that any individual or firm can spend one unit of the final good at time t in order to generate a flow rate η of the blueprints of new machines. The firm that discovers these blueprints receives a fully-enforced perpetual patent on this machine.There is no aggregate uncertainty in the innovation process. Naturally, there will be uncertainty at the level of the individual firm, but with many different research labs undertaking such expenditure, at the aggregate level, eq. (13.4) holds deterministically.

Given the patent structure specified above, a firm that invents a new machine variety is the sole supplier of that type of machine, say machine of type ν, and sets a price of px(ν,t) at time t to maximize profits. Since machines depreciate after use, px(ν,t) can also be interpreted as a “rental price” or the user cost of this machine.

The demand for machine of type ν is obtained by maximizing net aggregate profits of the final good sector as given by (13.2) minus the cost of inputs. Since machines depreciate after use and labor is hired on the spot market for its flow services, the maximization problem of the final good sector can be considered for each point in time separately and simply requires the maximization of the instantaneous profits of a representative final good producer. These instantaneous profits can be obtained by subtracting the total inputs costs, the user costs of renting machines and labor costs, from the value of our production. Therefore, the maximization problem at time t is:

The first-order condition of this maximization problem with respect to x (ν, t) for any ν ∈ [0,N (t)] yields the demand for machines from the final good sector.

These demands take the convenient isoelastic form:

which is intuitive in view of the fact that elasticity of demand for different machine varieties  This equation implies that the demand for machines only depends on the user cost of the machine and on equilibrium labor supply, but not on the interest rate, r (t), the wage rate, w (t), or the total measure of available machines, N (t). This feature makes the model very tractable.

This equation implies that the demand for machines only depends on the user cost of the machine and on equilibrium labor supply, but not on the interest rate, r (t), the wage rate, w (t), or the total measure of available machines, N (t). This feature makes the model very tractable.

Next, consider the maximization problem of a monopolist owning the blueprint of a machine of type ν invented at time t. Since the representative household holds a balanced portfolio of all the firms in the economy and there is a continuum of firms, there will be no aggregate uncertainty, so each monopolist’s objective is to maximize profits. Consequently, this monopolist chooses an investment plan and a sequence of capital stocks so as to maximize the present discounted value of profits starting from time t. Recalling that the interest rate at time t is r (t) and that the marginal cost of producing machines (in terms of the final good) is ψ, the net present discounted value can be written as:

where

denotes profits of the monopolist producing intermediate ν at time t, x(ν,t) and px(ν,t) are the profit-maximizing choices for the monopolist, and r (t) is the market interest rate at time t. Alternatively, assuming that the value function is differentiable in time, this could be written in the form of Hamilton-Jacobi-Bellman equations as in Theorem 7.10 in Chapter 7:

Exercise 13.1 asks you to provide a different derivation of this equation than in Theorem 7.10.

13.1.2. Characterization of Equilibrium. An allocation in this economy is defined by the following objects: time paths of consumption levels, aggregate spending on machines,

involves setting the same price in every period (see Exercise 13.2):

That is, all monopolists charge a constant rental rate, equal to a markup over the marginal cost. Without loss of generality, let us normalize the marginal cost of machine production to

Profit-maximization also implies that each monopolist rents out the same quantity of machines in every period, equal to

(13.10)

x (ν, t) = L for all ν and t.

This gives monopoly profits as:

(13.11) π (ν, t) = βL for all ν and t.

The major implication of this equation is that each monopolist sells exactly the same amount of machines, charges the same price and makes the same amount of profits at all time points. This particular feature simplifies the analysis of endogenous technological change models with expanding variety.

Substituting (13.6) and the machine prices into (13.2) yields a (derived) production function for the final good,

This is one of the main equations of the expanding input or product variety models. It shows that even though the aggregate production function exhibits constant returns to scale from the viewpoint of final good firms (which take N (t) as given), there are increasing returns to scale for the entire economy. Moreover, (13.12) makes it clear that an increase in the variety of machines, N (t), raises the productivity of labor and that when N (t) increases at a constant rate so will output per capita.

The labor demand of the final good sector follows from the first-order condition of maximizing (13.5) with respect to L and implies the equilibrium condition

L and implies the equilibrium condition

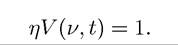

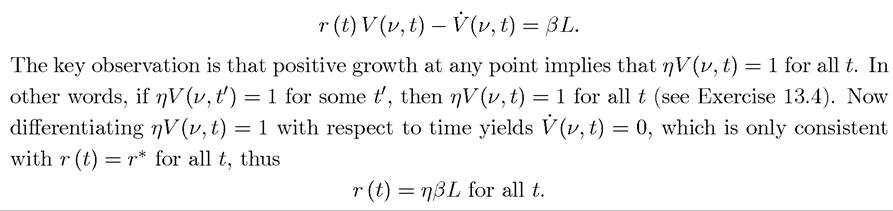

Finally, free entry into research implies that at all points in time  where V(ν, t) is given by (13.7). To understand (13.14), recall that one unit of final good spent on R&D leads to the invention of η units of new inputs, each with a net present discounted value of profits given by (13.7). This free-entry condition is written in the complementary slackness form, since research may be sufficiently unprofitable that there may be zero R&D

where V(ν, t) is given by (13.7). To understand (13.14), recall that one unit of final good spent on R&D leads to the invention of η units of new inputs, each with a net present discounted value of profits given by (13.7). This free-entry condition is written in the complementary slackness form, since research may be sufficiently unprofitable that there may be zero R&D

483

effort, in which case ηV(ν,t) could be strictly less than 1. Nevertheless, for the relevant parameter values there will be positive entry and economic growth (and technological progress), so we often simplify the exposition by writing the free-entry condition as

Note also that since each monopolist ν ∈ [0,N(t)] produces machines given by (13.10), and there are a total of N (t) monopolists, the total expenditure on machines is

Finally, the representative household’s problem is standard and implies the usual Euler equation for consumption,

and the transversality condition

which is written in the “market value” form and requires the value of the total wealth of the representative household, which is equal to the value of corporate assets N (t) V (t), not to grow faster than the discount rate (see Exercise 13.3).

In light of the previous equations, an equilibrium can be defined more formally as time paths of consumption, expenditures, R&D decisions and total number of varieties,

A balanced growth path (BGP) is again an equilibrium path where C (t),X (t),Z (t) and N (t) grow at a constant rate. Such an equilibrium can alternatively be referred to as a “steady state”, since it is a steady state in transformed variables (even though the original variables grow at a constant rate). This is a feature of all the growth models and I therefore use the terms steady state and BGP interchangeably in the context of models with sustained growth.

13.1.3. Balanced Growth Path. A balanced growth path (BGP) requires that consumption grows at a constant rate, say g'c. This is only possible from (13.16) if the interest rate is constant. Let us therefore look for an equilibrium allocation in which

where “*” refers to BGP values. Since profits at each date are given by (13.11) and since the interest rate is constant, (13.8) implies that Substituting this in either (13.7) or

Substituting this in either (13.7) or

(13.8),

This equation is intuitive: a monopolist makes a flow profit of βL, and along the BGP, this is discounted at the constant interest rate r*.

Let us next suppose that the (free entry) condition (13.14) holds as an equality, in which case we also have

This equation pins down the steady-state interest rate, r*, as:

The consumer Euler equation, (13.16), then implies that the rate of growth of consumption in BGP must be given by

Moreover, it can be verified that the current-value Hamiltonian for the consumer’s maximization problem is concave, thus this condition, together with the transversality condition, are sufficient for characterizing the optimal consumption plans of the consumer (recall Theorem 7.14 in Chapter 7).

In a BGP, consumption cannot grow at a different rate than total output (see Exercise 13.5), thus we must also have the growth rate of output in the economy is

Therefore, given the BGP interest rate, the long-run growth rate of the economy is obtained as:

Let us next assume that

which will ensure that g* > 0 and that the transversality condition is satisfied.

Proposition 13.1. Suppose that condition (13.21) holds. Then, in the above-described lab-equipment expanding input variety model, there exists a unique BGP in which technology, output and consumption all grow at the same rate, g*, given by (13.20).

Proof. The preceding discussion establishes all the claims in the proposition except that the transversality condition holds. You are asked to check this in Exercise 13.7. ?

An important feature of this class of endogenous technological progress models is the presence of the scale effect, which was already discussed in Section 11.4 in Chapter 11 in the context of the Romer (1986a) model: the larger is L, the greater is the growth rate. The scale effect comes from a very strong form of the market size effect discussed in the previous chapter. As illustrated there, the increasing returns to scale nature of the technology (for example, as highlighted in eq. (13.12)) is responsible for this strong form of the market size effect and thus for the scale effect. We will see in Section 15.5 in Chapter 15 that it is possible to have variants of the current model that feature the market size effect, but not the scale effect.

13.1.4. Transitional Dynamics. It is also straightforward to see that there are no transitional dynamics in this model. To derive this result, let us go back to the value function for each monopolist. Substituting for profits, this gives

This establishes:

Proposition 13.2. Suppose that condition (13.21) holds. In the above-described labequipment expanding input-variety model, with initial technology stock N (0) > 0, there is a unique equilibrium path in which technology, output and consumption always grow at the rate g* as in (13.20).

At some level, this result is not too surprising. While the microfoundations and the economics of the expanding varieties model studied here are very different from the neoclassical AK economy, the mathematical structure of the model is very similar to the AK model (as most clearly illustrated by the derived equation for output, (13.12)). Consequently, as in the AK model, the economy always grows at a constant rate.

Even though the mathematical structure of the model is similar to the neoclassical AK economy, it is important to emphasize that the economics here is very different. The equilibrium in Proposition 13.2 exhibits endogenous technological progress. In particular, research firms spend resources in order to invent new inputs. They do so because, given their patents, they can profitably sell these inputs to final good producers. It is therefore profit incentives that drive R&D, and R&D drives economic growth. We have therefore arrived to our first model in which market-shaped incentives determine the rate at which the technology of the economy evolves over time.

13.1.5. Pareto Optimal Allocations. The presence of monopolistic competition implies that the competitive equilibrium is not necessarily Pareto optimal (and Theorems 5.5 and 5.6 in Chapter 5 no longer apply). In particular, the current model exhibits a version of the aggregate demand externalities discussed in the previous chapter and features two sources of potential inefficiencies. First, there is a markup over the marginal cost of production of inputs. Second, the number of inputs produced at any point in time may not be optimal. The first source of inefficiency is familiar from models of static monopoly, while the second emerges from the fact that in this economy the set of traded (Arrow-Debreu) commodities is endogenously determined. This latter source of potential inefficiency relates to the issue of endogenously incomplete markets (there is no way to purchase an input that is not supplied in equilibrium) and will be discussed in greater detail in Section 17.6 in Chapter 17.

To contrast the equilibrium allocations with the Pareto optimal allocations, let us set up the problem of the social planner and derive the optimal growth rate. Notice that the social planner will also use the same quantity of all types of machines in production, but because of the absence of a markup, this quantity will be different than in the equilibrium allocation. The social planner will also take into account the effect of an increase in the variety of inputs on the overall productivity in the economy, which monopolists did not, because they did not appropriate the full surplus from inventions.

More explicitly, given N (t), the social planner will choose

which only differs from the equilibrium profit maximization problem, (13.5), because the marginal cost of machine creation, ψ, is used as the cost of machines rather than the monopoly price, and the cost of labor is not subtracted. Recalling that ψ ? 1 — β, the solution to this program involves

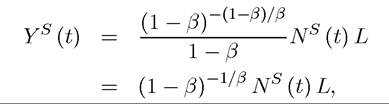

so that the social planner’s output level will be

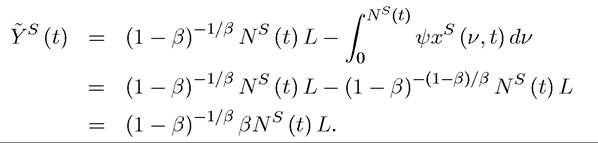

where superscripts “S” are used to emphasize that the level of technology and thus the level of output will differ between the social planner’s allocation and the equilibrium allocation. The aggregate resource constraint is still given by (13.3). Let us define net output, which subtracts the cost of machines from total output, as

This is relevant, since it is net output that will be distributed between R&D expenditure and consumption. Net output can be written as

Given this expression and (13.4), the maximization problem of the social planner can be written as

subject to

In this problem, N (t) is the state variable, and C (t) is the control variable. Let us set up the current-value Hamiltonian,

The necessary conditions for the social planner’ as problem are

It can be verified easily that the current-value Hamiltonian of the social planner is concave and satisfy the conditions of Theorem 7.14, thus the above conditions are both necessary and sufficient for an optimal solution (see Exercise 13.9).

Combining these conditions, we obtain the following growth rate for consumption in the social planner’s allocation (see again Exercise 13.9):

Like the equilibrium, the social planner also chooses and allocation with a constant rate of consumption growth (thus no transitional dynamics). The growth rate of consumption chosen by the social planner, (13.22), can be directly compared to the growth rate in the decentralized equilibrium, (13.20). The comparison boils down to that of

and it is straightforward to see that the former is always greater since by

by

virtue of the fact that β ∈ (0,1). This implies that the socially-planned economy will always grow faster than the decentralized economy

PROPOSITION 13.3. In the above-described expanding input variety model, the decentralized equilibrium is always Pareto suboptimal. Starting with any N (0) > 0, the Pareto optimal allocation involves a constant growth rate

which is strictly greater than the equilibrium growth rate g* given in (13.20).

Proof. Most of the proof is provided in the preceding discussion. Exercise 13.11 asks you to show that the Pareto optimal allocation always involves a constant growth rate and no transitional dynamics. ?

Intuitively, the Pareto optimal growth rate is greater than the equilibrium growth rate because the social planner values innovation more. The greater social value of innovations stems from the fact that the social planner is able to use the machines more intensively after innovation, since the monopoly markup reducing the demand for machines is absent in the social planner’s allocation. This is related to the pecuniary externality resulting from the 488

monopoly markups (and is thus related to the aggregate demand externalities discussed in the previous chapter). Moreover, this pecuniary externality also affects the set of traded commodities (thus the rate of growth of inputs and technology). Other models of endogenous technological progress we will study in this chapter incorporate technological spillovers and thus generate inefficiencies both because of the pecuniary externality isolated here and because of the standard technological spillovers.

13.1.6. Policy in Models of Endogenous Technological Progress. The divergence between the decentralized equilibrium and the socially planned allocation introduces the possibility of Pareto-improving policy interventions. There are two natural alternatives to consider:

(1) Subsidies to Research: by subsidizing research, the government can increase the growth rate of the economy, and this can be turned into a Pareto improvement if taxation is not distortionary and there can be appropriate redistribution of resources so that all parties benefit.

(2) Subsidies to Capital Inputs: inefficiencies also arise from the fact that the decentralized economy is not using as many units of the machines/capital inputs (because of the monopoly markup); so subsidies to capital inputs given to final good producers would also be useful in increasing the growth rate.

Moreover, it is noteworthy that as in the first-generation endogenous growth models, a variety of different policy interventions, including taxes on investment income and subsidies of various forms, will have growth effects not just level effects in this framework (see, for example, Exercise 13.13).

Naturally, once we start thinking of policy in order to close the gap between the decentralized equilibrium and the Pareto optimal allocation, we also have to think of the ob jectives of policymakers and this brings us to political economy issues, which are the sub ject matter of Part 8. For that reason, I will not go into a detailed discussion of optimal policy (leaving some of this to you in Exercises 13.12-13.14). Nevertheless, it is useful to briefly discuss the role of competition policy in models of endogenous technological progress.

Recall that the optimal price that the monopolist charges for machines is

Imagine, instead, that a fringe of competitive firms can copy the innovation of any monopolist, but they will not be able to produce at the same level of costs (because the inventor has more know-how). In particular, as in the previous chapter, suppose that instead of a marginal cost ψ, they will have marginal cost of then this fringe is not a

then this fringe is not a

threat to the monopolist, since the monopolist could set its ideal, profit maximizing, markup and the fringe would not be able to enter without making losses. However, then the fringe would prevent the monopolist from setting its ideal monopoly price. In 489

then the fringe would prevent the monopolist from setting its ideal monopoly price. In 489

particular, in this case the monopolist would be forced to set a “limit price”,

which has an explanation identical to the limit price in the previous chapter.[XVIII] When the monopolist charges this limit price, its profits per unit would be

which is less than β, the profits per unit that the monopolist made in the absence of the competitive fringe.

What is the implication of this on the rate of economic growth? It is straightforward to work out that in this case the economy would grow at a slower rate. For example, in the baseline model with the lab-equipment technology, this growth rate would be (see Exercise 13.15):

which is less than g* given in (13.20). Therefore, in this model, greater competition, which reduces markups (and thus static distortions), also reduces long-run growth. This might at first appear counter-intuitive, since the monopoly markup may be thought to be the key source of inefficiency and greater competition (lower 7) reduces this markup. Nevertheless, as mentioned above, inefficiency results both because of monopoly markups and because the set of available inputs may not be appropriately chosen. As 7 declines, monopoly markups decline, but the problem of underprovision of inputs becomes more severe. This is because profits are important in this model to encourage innovation by new research firms. If these profits are reduced, then incentives for research are also reduced. Since 7 can also be interpreted as a parameter of anti-trust (competition) policy, this result implies that in the baseline endogenous technological change models more strict anti-trust policy reduces economic growth.

Welfare is not the same as growth, however, and some degree of competition reducing prices below the unconstrained monopolistic level might be useful for welfare depending on the discount rate of the representative household. Essentially, with a lower markup, households are happier in the present, but suffer slower consumption growth. The tradeoff between these two opposing effects depends on the discount rate of the representative household (see Exercise 13.15 for the details).

Similar results apply when we consider patent policy. In practice, patents are for limited durations. In the baseline model, we assumed that patents are perpetual; once a firm invents a new good, it has a fully-enforced patent forever and it becomes the monopolist for that good forever. If patents are enforced strictly, then this might rule out the competitive fringe from competing, restoring the growth rate of the economy to (13.20). Also, even in the absence of the competitive fringe, we can imagine that once the patent runs out, the firm will cease making profits on its innovation. In this case, it can easily be shown that growth is maximized by having as long patents as possible. Again there is a tradeoff here between the equilibrium growth rate of the economy and the static level of welfare.

Perhaps, more important than these tradeoffs between growth and level is the fact that the models discussed in this chapter do not feature an interesting type of competition among firms. The quality competition (Schumpeterian) models introduced in the next chapter will allow a richer analysis of the effect of competition on innovation and economic growth.

13.2.