Article 10.4 Repo ‘fire sale' risk worries regulators

By Michael Mackenzie and Tracy Alloway

Financial Times October 2, 2013

The prospect of financial assets being dumped in a ‘fire sale’ has re-emerged as a substantial risk in a crucial $2tn funding market used by US banks, despite changes since the financial crisis to reduce risk.

The tri-party repo market, where banks loan out their securities in exchange for short-term loans from investors, has been one of the key areas of financial reform after playing a major role in the 2008 collapse of Lehman Brothers.

Banks use the market to pledge their assets as security, or collateral, in exchange for short-term loans from lenders that include money market funds, insurers and mutual funds. In 2008, much of that financing was suddenly pulled away after the value of mortgage-related collateral underpinning the loans was called into doubt. Fire sales, where assets are sold in a manner that can sharply depress prices and thereby pressure other investors into selling their assets, were a hallmark of the financial crisis.

While much of the market has been strengthened, regulators including Bill Dudley, president of the Federal Reserve Bank of New York, say that a run on repo collateral remains a risk. The issue is likely to dominate a New York Fed conference on Friday.

‘This is a process that's providing credit from one part of the market to another,' said Martin Hansen, senior director at Fitch Ratings. ‘But the issue is that at one end of this chain of credit you have risk averse, short-term lenders. If they have concerns, then that can create ripple effects along the rest of the chain and beyond.'

Fitch estimates that the use of interest rate-sensitive securities such as US Treasuries and other US government-backed securities as collateral in the tri-party repo market fell $187bn between May and July, after the Fed began talking about winding down its emergency economic support.

That suggests sell-offs in the repo market remain an issue more than five years after the crisis.‘The risk is that once a dealer [bank] goes under, money funds have to liquidate the securities they hold and a money fund may not have the expertise to liquidate large amounts of securities,' said Scott Skyrm, a former repo broker.

The New York Fed has overseen reform of the tri-party repo market in recent years, with a heavy focus on the role played by the two custodian banks that incur daily counterparty risk, JPMorgan Chase and Bank of New York Mellon.

While dependence on so-called ‘intraday credit' from the two banks, along with poor liquidity and credit risk management practices by the banks, has largely been addressed, the spectre of fire sales remains an issue for regulators.

Regulators also point to a lack of data concerning the bilateral repo market, which operates in a similar way but without custodians. Estimates of the market's size vary from about $3tn to $5tn, and a report from the Office of Financial Research this week warned of ‘data gaps' in securities lending and repo markets.

Friday's meeting organised by the New York Fed will bring together academics, market participants and other regulators. Speakers are expected to discuss ways of setting up ‘a process for orderly liquidation' of repo collateral.

FT

Source: Mackenzie, M. and Alloway, T. (2013) Repo ‘fire sale' risk worries regulators, Financial Times, 2 October.

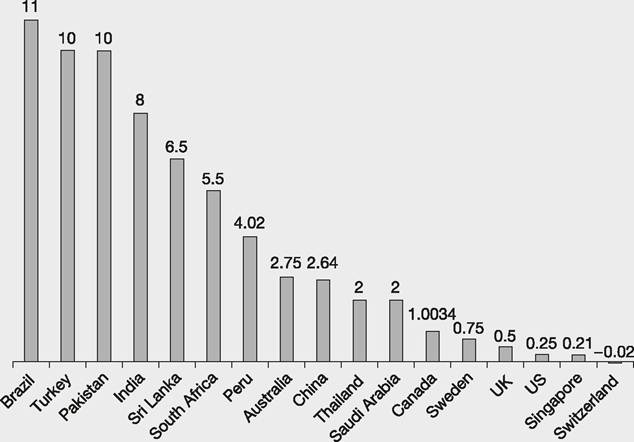

Whereas in the UK, US and many other developed countries repo rates are currently low, typically between 0% and 1%, in other parts of the world the rate can be considerably higher. The rates reflect the risk element, anticipated current and future degree of inflation, and the credit rating in each country - see Figure 10.3.

The sell/buy-back

Some countries, such as Italy, never developed, or were slow to develop, the legal frameworks, IT systems and settlement systems for repo transactions. The

Figure 10.3 Overnight repo rates, per cent (annualised), 2013/2014

Source: Data from national banks and other sources

sell/buy-back was created instead, which is very similar to a repo but involves an outright cash sale of bonds, and a separate agreement to buy back the bonds at a forward date.

Coupon payments during the term are paid first to the buyer and only given to the original owner on termination.Certificates of deposit (CDs)

Certificates of deposit are issued by banks when funds are deposited with them by other banks, corporations, individuals or investment companies. The certificates state that a deposit has been made (a time deposit) and that at the maturity date the bank will pay a sum higher than that originally deposited, i.e. they are issued at face value and at maturity the holder receives the face amount plus interest. The maturities can be any length of time, with a minimum of one week, and are typically between one to four months. But they can be issued with a maturity date of five years or longer. For those lasting less than one year the interest is generally payable on maturity. However, some short-term CDs also occasionally pay variable interest rates, e.g. the interest on a 6-month CD changes every 30 days depending on interbank interest rates. Those dated for over one year have interest paid annually, or sometimes semiannually; they may also pay a variable rate of interest, with the rate altered, say, each year, based on the rates on a benchmark rate, e.g. Libor.

Negotiable and non-negotiable

CDs can be negotiable, that is, permitted to be traded in a secondary market to another investor before the maturity date, although many negotiable CDs are not all that liquid, with few potential buyers interested in trading. CDs can also be designated non-negotiable, meaning they have to be held to maturity by the original investor - there is a penalty on withdrawal of cash from the bank before the maturity date. The advantage of negotiable CDs is that although they cannot be redeemed before maturity at the issuing bank without a penalty, the original depositor can achieve liquidity while the bank issuing the certificate has a deposit held with it until the maturity date. The rate of interest paid on negotiable CDs is lower than a fixed deposit because of the attraction of liquidity.

A company with surplus funds can put it into a CD knowing that if its situation changes and it needs extra cash, it can sell the negotiable CD. The tradable value of the CD rises as the remaining length of its maturity reduces.United Kingdom and United States of America

At the centre of the secondary market is a network of brokers and dealers in CDs, striking deals over the telephone or on the internet. CDs are normally issued in lots ranging from £100,000 to £500,000 in the UK. Most sterling CDs are held by other banks operating in the UK, building societies and other money market players. Individual/personal holdings are negligible. For sterling CDs the interest is calculated on an actual/365 days basis.

Lot sizes are generally $100,000 to $1,000,000 in the US for the main wholesale market, with similar sized lots in the eurozone, Japan and other countries. In the US, however, CDs are frequently bought by retail investors in denominations that can go as low as $100. Individuals generally buy non-negotiable CDs because the minimum denomination for a negotiable CD is $100,000 (also termed a jumbo CD). Most retail-focused CDs are guaranteed by the Federal Deposit Insurance Corporation (FDIC) for up to $250,000 per depositor, meaning that if the issuing bank does not redeem them this government- sponsored agency will. For US CDs the interest is calculated on an actual/360 basis, with the interest generally paid at maturity.

Quotations

CDs are quoted in the trading markets on a yield to maturity basis. So, if a deposit of £100,000 is made and a CD is handed over which states that after one-quarter of the year the holder will receive £100,500, the yield to maturity is £500 divided by £100,000 multiplied by 4 to annualise it. Thus the annual rate of interest is 2%. (See Chapter 14 for more on CD calculations.)

Many CDs issued today lack a paper certificate, which, given that ‘certificate' is in the title, seems a little oxymoronic.

These ‘dematerialised' CDs are held as electronic book entries only. Euroclear operates a book entry system in London. Here CDs are issued and transferred using Delivery Versus Payment (DVP), meaning that the electronic transfer of ownership in the secondary market is at the same time as payment.Eurocurrency CDs

As well as domestic currency CDs there are Eurocurrency certificates of deposit, Euro-CDs, outside the jurisdiction of the authorities of the currency of denomination. Standard Eurocurrency deposits (not CDs) have fixed maturities - say seven days - and you cannot get at that money until the seven days have passed. By issuing Eurodollar CDs banks are able to offer an advantage if those CDs are negotiable, by allowing depositors to sell the CDs to other investors before maturity. Those issued by a bank with a high credit standing are likely to have greater liquidity. Eurodollar CDs tend to offer higher yields than CDs issued in dollars in the US because the American-based CDs have the backing of the Federal Reserve regulatory environment for banks, making them safer for investors.