Article 4.11 Midsized issuers welcome funding scheme

By Andrew Bolger

Financial Times February 16, 2015

An ambitious framework for a European private placement market has been published that aims to widen access to finance by midsized companies.

For many years, lots of midsized European businesses have accessed the US private placement market, which allows insurers to provide long-term finance to companies that wish to avoid the expense and scrutiny of issuing publicly listed bonds.

But a working group led by the International Capital Market Association has launched a voluntary guide for common market standards and best practices which it says are essential for the development of a pan-European market.

‘The guide will be a big help in communicating with and within midsized corporates about an alternative source of finance,' says Colin Tyler, chief executive of the Association of Corporate Treasurers. ‘For potential midsized issuers that have not used private placements before, it will give confidence that there are clear paths to issuing - it is not venturing into Wild West territory.'

Private placements are medium- to long-term senior debt obligations - in bond or loan format - issued privately by companies to a small group of investors. The private placement market typically provides fixed-rate financing of between three and 15 years, most commonly for seven to 10 years.

With private placement deals providing longer maturities than many bank loans, this helps to release companies from the burden of refinancing bank debt every couple of years.

Calum Macphail, head of private placements at M&G Investments, one of the largest European investors in private placements, says the guide provides companies interested in exploring this market an understanding of the process, who was involved and information potential investors would require.

‘As the financing landscape changes as banks de-lever, natural sources of longer- term finance, namely pension funds and institutional investors, are filling this gap,' he says.

‘Pension funds are attracted to the characteristics of private placements - strong, stable cash flows and covenant protections similar to a loan.'In addition to diversification and stronger documentation compared with public bonds, he says investors will also benefit from an illiquidity premium which could provide an enhanced yield as well as regular income over the medium to long term. The popularity of private placements has accelerated since the onset of the financial crisis, with markets in countries such as France and Germany providing borrowers with a local solution.

ICMA, which represents institutions across the international capital markets, says demand for private placements is set to increase as the EU's approximately 200,000 midsized companies look to diversify their sources of funding away from the traditional bank loan market, and view private placements both as an alternative and as an intermediate step towards the listed bond markets.

The guide builds on existing practices and documents used in the European bond and loan markets, especially a charter developed by the Euro PP Working Group, a French financial industry initiative. It is expected costs will be lowered by promoting the use of recently standardised documentation.

Daniel Godfrey, chief executive of the Investment Association, says common market standards for European private placement transactions will remove a significant barrier to the development of the private placement market in the UK and Europe.

‘Our members are major investors in UK businesses and, having worked closely with members and government on the proposed withholding tax exemption for privately placed debt in the UK, in December 2014, we were able to announce that five institutions intend to make investments of around £9bn in private placements and other direct lending to UK companies,' he said.

The French and German domestic private placement markets issued approximately ˆ15bn of debt in 2013 in addition to a further $15.3bn raised by European companies in the $60bn US private placement market.

Standard & Poor's estimates ˆ2.7tn of debt will need to be refinanced by midsized companies between now and 2018, at a time when banks continue to retreat from long term lending markets.

As well as trade bodies, the pan-European private placement initiative has received strong support from government officials in the UK and France, as it is closely aligned with the European Commission's goal of bringing about a capital markets union, on which a green paper is expected this week.

Welcoming the guide, Fabio Panetta, deputy governor of the Bank of Italy, said: ‘It is a useful tool for developing a European private placement market for corporate debt and, consequently, for broadening and diversifying sources of funding to the European economy.'

Source: Bolger, A. (2015) Midsized issuers welcome funding scheme, Financial Times, 16 February.

2015

Timetable for an issue

The timetable for a bond issue can range from a few days to several months; it is longer for more complex issues, those in numerous jurisdictions, when it is the first bond for this issuer, and when the bonds are to be listed on a stock exchange. Here are the basics of the process (except for a bought deal or private placement):

• Pre-launch and launch. The lead manager appoints the trustee or fiscal agent, the principal paying agent, the other members of the syndicate, and prepares the prospectus and other documents. The lead manager or co-lead managers will discuss with the issuer and potential investors the specifications, such as size of issue, coupon and price. As discussion progresses these will be ‘firmed up'. A book-building public promotion period might span two weeks (‘pre-selling the bonds'). Within that, a roadshow and a series of conference calls might take four days with, say, 10 to 100 attendees per meeting in different cities across the country.

• Announcement day.

It is only on the announcement day that the issue is formally announced (a press notification is usual), including the decision on the maturity and coupon rate or range of coupon rates. The lead manager formally invites the prospective syndicate members to participate, telling them the timetable and their obligations. On the pricing day, the price of the bond relative to par (say £99.85 if the par is £100) is agreed by the borrower and the syndicate group.• Offering day/signing day. The bonds are formally offered the day after the pricing day. The borrower and managing group sign the agreement on the specifications. The size of the allotments to syndicate members is announced by the lead manager. Signing usually occurs between two days and one week before closing and can take place at a meeting or, more frequently these days, by fax or email.

• Closing. The trust deed or fiscal agency agreement are signed, the bond is created and investors pay for the bonds they have purchased.

• Listing. For listed bonds the relevant documentation must be delivered to the listing authority (e.g. in Britain it is the UKLA, part of the FCA) and the stock exchange.

Auction issue

In an auction issue the cost of management fees is bypassed because the issuer goes to investors directly asking for price and quantity bids for prospective bonds with specified maturity and coupon. The disadvantage is that the expertise of the lead manager and others in the syndicate is forgone with regard to market knowledge, contacts, reputation, etc. Thus auction issues are for high-quality, well-known borrowers only.

United States of America

The US has the largest corporate bond market in the world. The Financial Industry Regulatory Authority (FINRA) supervises all aspects of bond trading and its participants. FINRA (www.finra.org) lists over 40,000 corporate bonds, with details of each bond (coupon, maturity, etc.) and, if it has one, its credit rating. To take an example: the Ford Motor Co has about 190 bonds listed, with maturities ranging up to 2097 and coupon rates varying from 0.571% to 12%.

About two-thirds of Ford's bonds have the same credit rating, Baa3 from Moody's and BBB- from Standard & Poor's and Fitch, and recent sales prices vary from $41 to $202.375.Disney has 26 bonds listed, including its famous Sleeping Beauty bond, a 100-year bond issued in 1993 paying a coupon of 7.55% on par (the yield to redemption was 4.071% at the time of writing). This bond is continuously callable and of the initial offering of $300 million, $99 million has been redeemed. It is rated single-A. According to Morningstar, the investment research centre, the Ford Motor Co had $7.7 billion of outstanding bonds and Walt Disney had $13.3 billion in 2014, illustrating how important the bond markets are for funding their operations.

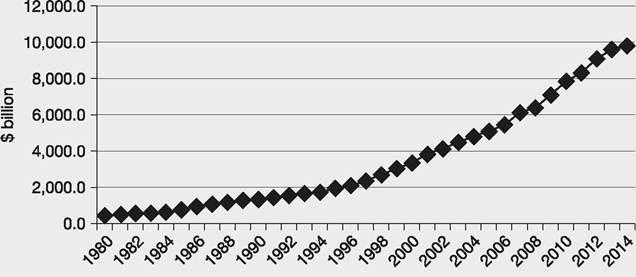

Publicly traded US corporate bonds usually carry a minimum denomination of $1,000. Those paying coupons usually do so every six months. More than 7,000 corporate bonds are listed on the NYSE (more than on any other exchange in the US), but the bulk of trading is in the off-exchange OTC market. Data from the Securities Industry and Financial Markets Association (SIFMA), a trade association for financial enterprises, shows the increase in corporate debt from 1980 to the present, with a total outstanding in 2014 of $9.8 trillion (see Figure 4.8) and daily trading in these bonds averaging over $20 billion.

Figure 4.8 US corporate debt outstanding from 1980

Source: Data from www.sifma.org

Many non-US companies issue US$ bonds in both the public debt market and the private placement market because they are more attractive to investors than bonds issued in a not-so-strong currency. Increasingly, with globalisation corporate bonds are issued all over the world, so a UK company might issue bonds in Japan denominated in yen or dollars because it is transacting business there.

Asia

Bond issuance in China is booming as corporates tap the markets rather than automatically source borrowed funds from banks.

The big issuers are the state- owned enterprises, ranging from the oil company Sinopec to China National Nuclear. But there are many private companies tapping into markets offering good interest rates. Alongside the greater issuance has been the growth in secondary market trading with institutions and retail investors enthusiastic about adding fixed-income securities to their portfolios in what is now a reasonably liquid market. China is beginning to realise the importance of overseas investment in its domestic markets, and has paved the way for renminbi-qualified foreign institutional investors (RQFIIs) to invest their foreign-held renminbi in Chinese corporate (and government) bonds.Domestic pension funds and other institutions in many Asian countries are keen to obtain assets denominated in their own currencies and so welcome further growth of their corporate bond markets - see Article 4.12. Pension funds are particularly interested in bonds of a longer maturity providing a better match to their pension liabilities than short-maturity issues. From the companies' perspective, they benefit from the stability that comes with locking in fixed-rate money for a decade or more.