Article 3.5 China bond market emerges from the shadows

By Josh Noble

Financial Times October 23, 2013

Since the days of Marco Polo, China has been stuck with the label of the world's largest untapped market.

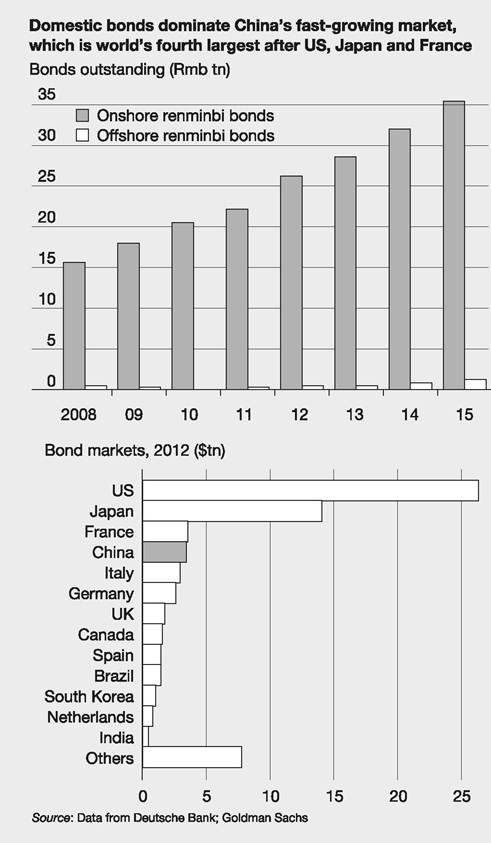

At roughly $4tn, China's domestic bond market is the world's fourth largest, and far larger than the Shanghai equity market's $2.4tn.

It is also growing about 30% a year.Yet for global investors, Chinese credit has been almost entirely off limits, with opportunities limited to relatively small offshore markets - whether in US dollars or renminbi - where a small number of mainland companies have chosen to borrow. But change is afoot as financial reforms crack open the door to domestic Chinese bonds.

‘As the market opens up, it's going to become one of the most important capital markets in the world,' says Geoff Lunt, Asian fixed-income product specialist at HSBC asset management.

Singapore on Tuesday joined London and Hong Kong as financial centres where investors can apply for quotas under China's renminbi qualified foreign institutional investor scheme. Holders of RQFII licences can use renminbi that they hold offshore to invest directly in domestic Chinese assets, from bonds to stocks to money market funds.

The recent expansion of RQFII - totalling Rmb400bn ($65bn) but of which just Rmb130bn has been allocated - is the latest step in Beijing's broad, long-term goal of improving access to China's domestic financial markets. A sister programme denominated in US dollars has also been expanded to attract more foreign investment.

HSBC, which in July became the first big international bank to get an RQFII licence, says it plans to use its licence to launch funds targeting China's domestic bond market. Central banks are also getting in on the act as they look to diversify their holdings away from the US dollar. In April, the Reserve Bank of Australia said it planned to invest about 5% of its reserves in Chinese government debt.

‘Liquidity is better onshore, and the yield pickup is also higher. That's why a lot of central banks have got their own quotas to place funds onshore', says Jack Chang, chief executive of ICBC Asia asset management. His company, whose clients include central banks and sovereign wealth funds, plans to make its first investment in onshore fixed income later this month.

However, few are expecting the swift demise of the offshore - or ‘dim sum' - bond market, which is subject to international legal and regulatory standards and offers much simpler tax and repatriation rules for those seeking to exit investments.

FT

Source: Noble, J. (2013) China bond market emerges from the shadows, Financial Times,

23 October.

Emerging markets

Less well-developed economy governments may issue bonds in their domestic currency or in the major hard currencies such as the dollar or the euro. Table 3.5 shows a sample of government bonds from emerging countries for which the coupons and principal will be paid in dollars or euros (there are also a couple of high-yield corporate bonds for Bertin and Kazkommerts). Credit ratings from Standard & Poor's, ‘S', Moody's, ‘M', and Fitch, ‘F', are discussed

Table 3.5 High yield and emerging market bonds

| Jun 16 | Red date | Coupon | Ratings | Bid price | Bid yield | Day's chge yield | Mth's chge yield | Spread vs US | ||

| S* | M* | F* | ||||||||

| High Yield US$ | ||||||||||

| Bertin | 10/16 | 10.25 | BB | Ba3 | 0 | 114.79 | 3.48 | 0.13 | -0.72 | 2.82 |

| High Yield Euro | ||||||||||

| Kazkommerts Int | 02/17 | 6.88 | B | Caa1 | B | 99.88 | 6.91 | 0.03 | -0.47 | 6.86 |

Emerging US$

| Bulgaria | 01/15 | 8.25 | BBB- | Baa2 | BBB- | 104.00 | 1.21 | -0.03 | 0.37 | 1.14 |

| Peru | 02/15 | 9.88 | BBB+ | Baa2 | BBB+ | 105.59 | 0.95 | 0.41 | -0.01 | 0.88 |

| Brazil | 03/15 | 7.88 | BBB- | Baa2 | BBB | 104.76 | 1.18 | 0.03 | 0.05 | 1.07 |

| Mexico | 09/16 | 11.38 | BBB+ | A3 | BBB+ | 123.27 | 0.86 | -0.05 | -0.10 | 0.39 |

| Philippines | 01/19 | 9.88 | BBB | Baa3 | BBB- | 132.51 | 2.34 | 0.00 | -0.02 | 0.65 |

| Brazil | 01/20 | 12.75 | BBB- | Baa2 | BBB | 150.12 | 2.94 | - | -0.35 | 1.23 |

| Colombia | 02/20 | 11.75 | BBB | Baa3 | BBB | 144.23 | 3.18 | -0.01 | 0.02 | 1.48 |

| Russia | 03/30 | 7.50 | BBB- | Baa1 | BBB | 115.25 | 4.32 | 0.16 | -0.21 | 2.63 |

| Mexico | 08/31 | 8.30 | BBB+ | A3 | BBB+ | 143.20 | 4.62 | 0.00 | 0.06 | 2.02 |

| Indonesia | 02/37 | 6.63 | BB+ | Baa3 | BBB- | 113.25 | 5.59 | - | 0.10 | 2.11 |

Emerging Euro

| Brazil | 02/15 | 7.38 | BBB- | Baa2 | BBB | 103.89 | 1.10 | 0.10 | 0.08 | 1.08 |

| Poland | 02/16 | 3.63 | A- | A2 | A- | 105.63 | 0.15 | -0.18 | -0.34 | 0.12 |

| Turkey | 03/16 | 5.00 | NR | Baa3 | BBB- | 105.40 | 1.74 | 0.05 | 0.16 | 1.71 |

| Mexico | 02/20 | 5.50 | BBB+ | A3 | BBB+ | 121.02 | 1.59 | 0.04 | -0.12 | 1.03 |

US$ denominated bonds NY closer; all other London close. * S - Standard & Poor’s, M - Moody's, F - Fitch.

Source: Thomson Reuters

in Chapter 5. Note the additional yield that must be offered on these bonds (‘Spread vs US') compared with what the US government has to pay despite the currency of coupons and principal both being US dollars. This is due to the extra risk of default.

Frequently, these bonds are issued under UK or US law to reassure lenders that should default occur there will be greater protection than under the issuer's law. The benefit of this was shown in the case of Greece's default in 2012 - the majority of its sovereign debt was issued under local law and those holders were forced to accept 74% losses in a ‘bond exchange' (meaning they swapped the original bonds for lower-value ones). The minority holding the few governed under English law were repaid at par. Mind you, it is not always that easy. Take the case of Argentina's bonds, issued under US law. They defaulted in 2001. Following a deal with most of the bond holders (they got about 35 cents on the dollar) the country refused to pay anything to those who did not agree to the reduction (24% of the holders). The ‘holdouts' (mostly hedge funds) fought in US courts for years and won a number of judgments - an Argentine ship was seized in Ghana at one point; the president is reluctant to fly abroad in her plane in case it is seized - which in 2014 resulted in a ruling that they should receive full payment including interest - see Article 3.6.