Article 8.1 Daily fix that spiralled out of control

By Brooke Masters, Caroline Binham and Kara Scannell

Financial Times December 19, 2012

UBS traders and managers on three continents used phone calls, electronic chat rooms and emails to manipulate benchmark interest rates in five currencies on an almost daily basis, according to documents filed by US, UK and Swiss authorities.

The web of activity spanned the globe, taking in traders in Japan and the US, brokers in London and elsewhere and rate submitters based in London and Switzerland.

About 40 UBS employees, traders at five other banks and 11 employees at six interdealer brokers were directly involved or aware of efforts to manipulate Interbank lending rates in various currencies, according to the UK Financial Services Authority final notice.

US authorities have charged two former UBS traders, Tom Hayes and Roger Darin, with criminal conspiracy, and Mr Hayes also faces a criminal price-fixing charge in connection with allegations he ‘colluded’ with another bank to manipulate the yen Libor rate.

The charging and settlement documents include excerpts from myriad emails and chat room messages focused on the daily fixing process for Libor, the collective name for benchmark lending rates set in London for 10 currencies, and Euribor and Tibor, similar rates set in Brussels and Tokyo.

All of the benchmarks rely on averaging daily estimates from panels of banks, so they can in theory be moved if one or more banks deliberately aim high or low.

That was not a problem in Libor’s infancy in the mid-1980s when it was used primarily to price corporate and other lending. But the Interbank lending rates became a crucial benchmark for derivatives in the late 1990s, transforming the importance of the daily fixings. A swing of only a few basis points changed from being a rounding error on a loan rate to making the difference between a bonanza trading day and devastating losses.

According to the regulators, that shift also drew the attention of UBS traders, who, according to the Swiss regulator Finma, could triple or even sextuple their annual salaries with bonuses for good results.

The FSA documented more than 2,000 requests to move rates, including more than 800 internal conversations at UBS between traders and rate submitters - nicknamed the ‘cash boys’ - and more than 1,100 external contacts.

The US Commodity Futures Trading Commission said that it found rate requests focused on yen Libor on 570 of the trading days between 2006 and 2009, or roughly three-quarters of the time.

A US criminal complaint alleges that Mr Hayes, based in Tokyo, used an electronic chat room to tell Mr Darin, who helped submit UBS's Libor estimates, that he had a big derivative riding on the six-month US dollar Libor rate. ‘Can we try to keep it on the low side pls?' he wrote in April 2008.

Mr Darin allegedly responded ‘I'll submit something low... but if u can u should square it up', adding ‘the correct 6m is 1.08'. UBS then submitted a rate of 0.98, the criminal complaint said.

The internal contacts were so pervasive that one submitter responded to a January 2007 rate request with ‘standing order, sir', the FSA said.

UBS traders also reached out directly to their counterparts at other banks and they sometimes worked in concert.

But the vast majority of external requests, particularly for yen Libor, went through the interdealer brokers. The FSA said four UBS traders based in Tokyo used 11 employees at six brokerages as conduits, asking them to pass on requests for specific rates to traders and more broadly influence the market.

Although brokers do not participate in the rate setting process directly, they were frequently contacted for market information by submitters at some panel banks. So UBS traders also asked the brokers to report false bids and offers - known as ‘spoofs' - and asked them to manipulate the rates shown on their trading screens to skew market perceptions, according to the FSA.

The brokers were repaid for their assistance in two ways. In one broker's case, UBS traders would place ‘wash trades' - transactions that have no purpose other than to generate fees - with the helpful party. In addition, UBS made corrupt payments of £15,000 per quarter to brokers to reward them for their assistance over a period of at least 18 months.

Source: Masters, B., Binham, C. and Scannell, K. (2012) Daily fix that spiralled out of control, Financial Times, 19 December.

2012

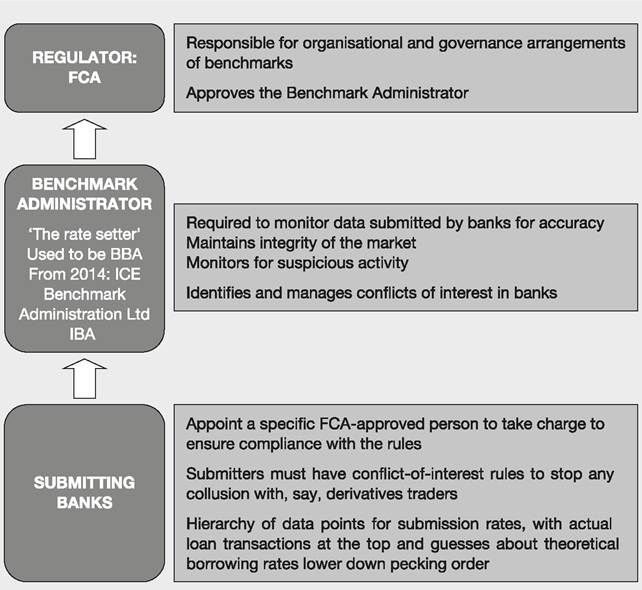

The new regime

In 2013 the BBA was stripped of its ‘sponsor' role and a new administrator created, ICE Benchmark Administration Limited (IBA), part of the US-based Intercontinental Exchange Group. The benchmark administrator is overseen by the Financial Conduct Authority, the financial regulator (formerly the Financial Services Authority) - see Figure 8.1.

ICE began its role on 1 February 2014 and issued its first ICE Libor rates on 3 February - see Article 8.2. Note the determination to move away from rates based on theoretical loans to actual lending agreements.

Figure 8.1 The new Libor structure