Article 6.7 Rate rise fears spark boom in convertible bonds

By Michael Stothard and Arash Massoudi

Financial Times July 19, 2013

Demand for convertible bonds is expanding sharply as fears of rising rates have hit prices in traditional debt markets, while at the same time equity markets are bouncing to record highs.

The convertible bond acts as a powerful weapon for investors looking to get the potential upside of the equity markets while staying within the more cautious realm of fixed income.

A convertible bond is essentially a low yielding corporate debt issue with an attached equity option. If the share price of the company rises past a fixed point, the investor benefits. If it falls, the investor still has the yield from the debt.

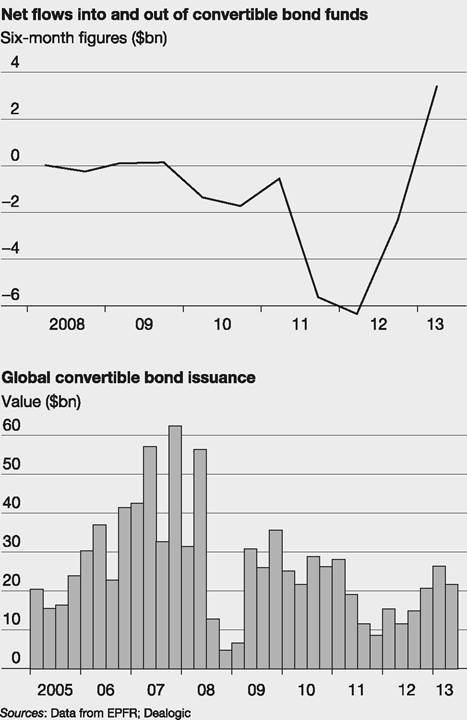

These features - in a market where shares have been rising but bonds falling in recent months - have bolstered demand, with a record-breaking net inflow into convertible bond funds of $4.8bn in the past six months, according to EPFR.

This follows three-and-a-half years of outflows from the asset class, and the net figure is 36 times larger than the previous record half-year inflow back in 2009. The boom reflects investors’ bets that improving economic conditions will be good for equities, while pushing interest rates up from near-zero levels and putting pressure on the price of regular bonds.

Traditional hedge funds, which dominated the market with very leveraged bets before the financial crisis, have been edging back into the game. BlueMountain Capital Management, a $13bn hedge fund, launched a convertibles desk last year.

The big managers have been buying as well. ‘It has been a great year for the asset class,’ says Leonard Vinville, manager of the M&G Global Convertibles Fund, whose assets under management have grown 50% this year.

‘People want to have exposure to equities, but they also want a degree of protection on the downside if equities fall or if the wider markets start to see a lot more volatility.’

Those bets have paid off, at least compared with pure fixed-income investments.

Convertible bonds have returned 12.8% this year, compared with 3.2% for high yield and a loss of 3% for investment grade debt.The strong demand has prompted companies to take advantage of the instruments as a source of cheap and flexible financing. Companies around the world raised $48bn in the first half of the year.

And it is not just the traditional unrated companies in the technology or biotechnology sector - which struggle to get normal bond market funding - that are

borrowing. ArcelorMittal, the world's largest steelmaker, raised $2.2bn through a convertible bond while Volkswagen raised $1.6bn.

Terms for many of these deals have been attractive for issuers. Online travel company Priceline.com was able to raise nearly $1bn in seven-year debt in May with a coupon of just 35 basis points, alongside an option premium of 66%.

‘Given the ultra-low pricing issuers can get on convertible bonds right now, lots of blue-chip companies are looking to tap the market as well as smaller ones,' says Klaus Hessberger of JPMorgan.

The greatest danger looming for investors in convertible bonds is really share prices going down substantially. Many convertible bonds trade in close alignment to equity, and so can be hit in a downturn more than regular fixed income.

‘The option element does mitigate the risk, but convertible bonds will typically fall when equity markets fall,' says Mark Wright, a fund manager at Miton Group. ‘That is our biggest worry.'

FT

Source: Stothard, M. and Massoudi, A. (2013) Rate rise fears spark boom in convertible bonds, Financial Times, 19 July.

The conversion price can vary from as little as 10% to over 65% greater than the share price at the date of the bond issuance. So, if a £100 bond offered the right to convert to 40 ordinary shares, the conversion price would be £2.50 (that is £100 ÷ 40), which, if the market price of the shares is £2.20, would be a conversion premium of 30p divided by £2.20, which equals 13.6%.

The right to convert may be for a specific date or several specific dates over, say, a four- year period, or any time between two dates. The company may have the option to redeem the bonds before maturity.Case study

Ford Motor Co

The Ford Motor Co issued 30-year convertible bonds in 2006, raising $4.5 billion. The bonds were sold at a premium of 25% above the share price at the time of $7.36. That is, the conversion price was at $9.20 per share. The bonds will mature in 2036 if they have not been converted before this and were issued at a par value of $1,000. The coupon was set at 4.25%. They are non-callable for the first ten years. From this information we can calculate the conversion ratio:

_. x. Nominal par value of bond $1,000

Conversion ratio =------------------------------------------- = —-------- = 108.6957 shares

Conversion price $9.20

Each bond carries the right to convert to 108.6957 shares, which is equivalent to paying $9.20 for each share at the $1,000 par value of the bond.

In November 2010 Ford, desperate to reduce its corporate debt and try to regain a better credit rating (move up to investment grade), after having had its commercial paper downgraded in 2005, persuaded holders of $1.9 billion of convertibles (this issue together with some other convertibles due for redemption in 2016) to swap debt for shares in the company. Ford gave the holders of the 2036 convertibles 108.6957 shares plus a cash payment equal to $190 for every $1,000 in principal amount, along with accrued and unpaid interest.

Box 6.2

Technical terms for convertibles

Conversion ratio

This gives the number of ordinary shares into which a convertible bond may be converted:

Conversion price

This gives the price of each ordinary share obtainable by exchanging a convertible bond:

Conversion premium

This gives the difference between the conversion price and the market share price, expressed as a percentage:

The length of time to maturity affects the conversion premium: the longer it is, the greater likelihood the share will rise above the conversion price and therefore the more an investor will pay for the option to convert.

Conversion value

This is the value of a convertible bond if it were converted into ordinary shares at the current share price:

Conversion value = Current share price ? Conversion ratio

The value of a convertible bond (a type of equity-linked bond) could be analysed as a ‘debt portion', which depends on the discounted value of the coupons and principal, and an ‘equity portion', where the right to convert is an equity option. Generally, the value is strongly influenced by the equity option value, which rises or falls with the market value of ordinary shares, at a lower percentage rate. They can therefore be quite volatile. But convertibles with large conversion premiums trade much like ordinary bonds because the option to convert is not a strong feature in their pricing. They are therefore less volatile and offer higher yields.

A convertible bond has two values forming lower bounds through which it should not fall: (1) it must sell for more than its conversion value, otherwise an arbitrageur could buy bonds and immediately convert them to shares, selling the shares, making a quick low-risk profit; (2) the value as a straight bond (ignoring the conversion option) (see Chapter 13 for such valuations). When the share price is low, the straight bond value is the effective lower bound, with the conversion option having little impact. When the share price is high, the bond's price is overwhelming driven by the conversion value.

To illustrate convertible bond price movements consider the Ford bond selling at $1,000, which can be converted to 108.6957 shares at $9.20 per share when shares are currently trading at $7.36:

1 If you bought shares and then they double to $14.72 you would make 100% return.

2 If, instead, you bought a convertible for $1,000 and shares double your return will be 60% (the convertible rises to 108.6957 ? $14.72 = $1,600). The lower return than in (1) is due to you effectively paying $9.20 per share rather than $7.36. In reality, the value of the convertible would be slightly higher than this because it will tend to trade at a slight premium to its conversion value (it still has the safety feature of the straight debt, and a timing option on the conversion).

3 Conversely, if the share price falls, say, to $5 and you made a pure share investment, you will be down by 32%, that is $2.36/$7.36. The conversion value on the bond falls from $800 to $5 ? 108.6957 = $543.4785.

4 However, its price does not go down that low because the minimum price is the greater of its conversion value or its value as straight debt. Assuming the value of comparable straight debt is $750 given current yields to redemption in the bond markets, the convertible will fall by a maximum of only 25%. Again, it is very likely to trade at more than this, a premium to its straight value, because the conversion right is still in place, even though conversion has become a more distant prospect. Thus a convertible offers the benefit of a reduced downside risk compared with equity, but also a reduced upside potential because the premium per share is paid.

5 Of course, if the share price is constant but market-determined redemption yields rise, then the value of the convertible will fall, as will its floor, being determined by its value as straight debt.

6 If the credit rating of Ford deteriorates, then the convertible price will fall, as will the straight-debt floor level.

If the share price rises above the conversion price, investors may choose to exercise the option to convert if they anticipate that the share price will at least be maintained and the dividend yield is higher than the convertible bond yield. If the share price rise is seen to be temporary, the investor may wish to hold on to the bond. If the share price remains below the conversion price, the value of the convertible will be the same as a straight bond at maturity.

Advantages for investors of convertibles

1 Investors are able to wait and see how the share price moves before investing in equity. They may take advantage of the upside.

2 In the near term there is greater security for their principal compared with equity investment, and the annual coupon is usually higher than the dividend yield.

3 For companies that do not pay dividends the investor can gain a regular income stream through a convertible and then (possibly) make a capital gain via conversion.

Disadvantages for investors of convertibles

1 The yield on the bond will be less than on a comparable straight bond. If the option value never materialises because the share does not appreciate, the holder may regret choosing a convertible over a vanilla bond.

2 There is a greater risk of default than for ordinary bonds because they are usually subordinated - down the pecking order upon administration and liquidation than most other bonds, but above equity.

3 Interest rate risk (see Chapters 4 and 13) is greater because the fixed interest rate offered is lower than for vanilla bonds; thus an increase in market interest rates causes a greater decline in price in the convertible compared with the non-convertible. This problem may be compounded if general market interest rate rises are accompanied by declines in the equity market reducing the chance of the share price rising above the conversion price and the bond being converted.

4 The bonds might be called by the company to the detriment of the holder, i.e. when the price has risen above the call rate.

5 Disadvantage for share owners: conversion of these bonds into shares may have the effect of diluting the value of individual shares - there is an increase in the number of shares as more are created, but not necessarily any increase in the profits/value of the company.

Advantages to the issuing company of selling convertible bonds

1 Lower interest than on a similar debenture. The fact that a firm can ask investors to accept a lower interest rate because the investor values the right to conversion was a valuable feature for many dot.com companies when they were starting out, e.g. Amazon and AOL could pay 5-6% on convertibles - less than half the amount they would have had to pay on vanilla bonds. Great Portland issued a convertible offering a coupon of only 1% - see Article 6.8.

2 The interest is tax deductible. Because convertible bonds are a form of debt, the coupon payment can be regarded as a cost of the business and can therefore be used to reduce taxable profit.

3 Self-liquidating. When the share price reaches a level at which conversion is worthwhile the bonds will (normally) be exchanged for shares so the company does not have to find cash to pay off the loan principal - it simply issues more shares. This has obvious cash flow benefits. However, the disadvantage is that the other equity holders may experience a reduction in earnings per share and dilution of voting rights.