Article 5.2 Turning point for European debt ratings

By Ralph Atkins and Keith Fray

Financial Times March 31, 2014

The financial crises of the past seven years drove sweeping changes in the global credit ratings map. The US and European governments were downgraded.

Emerging markets rose.The story of the past 12 months has been more complex. The rating performance of developing economies has been at best mixed. But signs are appearing that Europe has reached a possible turning point.

‘What we have tried to emphasise is how much divergence there is in terms of exposure to the turning tide in global capital,' says Moritz Kraemer, chief sovereign ratings officer at Standard & Poor's. ‘It is really country-specific policy actions that are likely to overshadow rating actions, rather than global factors.'

Credit ratings guide investors' decision making by indicating the likelihood of defaults.

Top performers compared with a year ago in terms of rating upgrades are Mexico and the Philippines. Near the bottom, unsurprisingly, is Ukraine, which has come close to financial collapse.

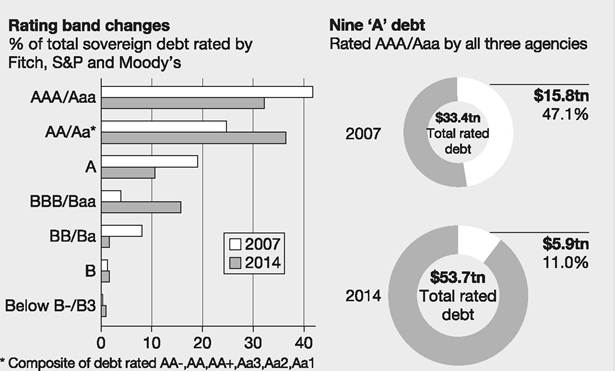

By weighting countries according to the size of their outstanding debt, the FT's analysis also shows the changing size of bond markets by credit rating category. Downgrades in the past year have thrown the Netherlands out of the shrinking club of economies rated triple A by all three agencies.

But, overall, average credit ratings in the developed world stabilised in the past year, although with significant country-by-country variations.

With Europe still reeling from its debt crisis and recession, France and Italy were downgraded. But Spain and Greece headed in the opposite direction, and there are signs that the 18-country eurozone trend is no longer downwards. Rating ‘outlooks' - which indicate possible future actions - have been switched from negative to stable by at least one agency for six eurozone countries, including Germany and Portugal.

‘At the beginning of last year, we had two-thirds of the eurozone on negative outlook. Now it's just one-third,' says James McCormack, at Fitch. ‘If you'd known before the crisis that a third would be on negative outlook, you would have rightfully thought that was pretty bad, but it has stabilised. Relative to where we were, things have certainly improved.'Any turnround in European credit ratings will be slow, however. Mr Kraemer at S&P points out that when Sweden and Finland lost their triple A status in the early 1990s, it was a decade before it was regained.

Similarly, France and the UK are unlikely to see a quick return to triple A status, warns Mr McCormack. ‘We have suggested that debt ratios need to come down in a more meaningful way - there has to be a track record of fiscal adjustment.'

Ratings in emerging markets over the past year have improved in Asia, central and eastern Europe and the Caribbean. But African, Middle East and Latin American

| Averaoe ratinα chanaes bv reaion. 2007-14 government debt - modified from FT chart | - countries weighted by size of |

| Developed Europe | DOWN 2.4 notches |

| Eurozone | DOWN 2.9 notches |

| Caribbean | DOWN 0.1 notches |

| All developed markets | DOWN 0.8 notches |

| Africa | DOWN 1.1 notches |

| M East and N Africa | DOWN 2.6 notches |

| CIS | DOWN 1.4 notches |

| Latin America | UP 1.9 notches |

| Central and E Europe | UP 0.8 notches |

| Developing Asia | UP 1.4 notches |

| All emerging markets | UP 1 notch |

countries have seen downgrades on average.

Brazil was downgraded by S&P last week.As well as country-specific factors, the future performance of emerging markets could depend on China's prospects. ‘China has generated a lot of economic activity, which has driven a lot of trade and improved the fiscal position of a lot of countries in, say, Latin America,' says Mr Oosterveld (head of sovereign ratings] at Moody's. ‘Things look very different if you assume, in a downside scenario, China is going to grow by 4% a year rather than 8%.'

But changes in the global ratings map do not necessarily reflect what happens on the ground. Economists at UniCredit argued that the subjective part of rating decisions often blurred their predictive powers. ‘History is littered with countries being over- and underrated by the rating agencies, with - at times - dramatic consequences,' they wrote. ‘The biggest casualty was the eurozone periphery, which was downgraded far too heavily during the 2009-11 sovereign debt crisis.'

FT

Source: Atkins, R. and Fray, K. (2014) Turning point for European debt ratings, Financial Times, 31 March.

While corporate borrowers' credit ratings are generally of great concern to them, because those with lower ratings tend to have higher costs, some companies are fairly sanguine, particularly if they regard the CRAs as using unreasonable methods and they can persuade finance providers of their point of view - see Article 5.3 for the example of Rio Tinto.