Capital adequacy management

How much capital should the bank hold? In deciding this managers need to trade off the risk of bank failure by not being able to satisfy its creditors (depositors, wholesale market lenders, etc.) against the attraction of increasing the return to the bank's owners by having as little capital as possible relative to the asset base.

The fear here is of insolvency - an inability to repay obligations over the longer course of events - rather than illiquidity, which is insufficient liquid assets to repay obligations falling due if there is a sudden outflow of cash (e.g. large depositor withdrawals on a particular day, unexpectedly drawing down on lines of credit, or large payments under derivative deals). To understand the difficulty with this trade-off we can compare BarcSan's situation with a less well-capitalised bank, Mercurial.BarcSan's opening balance sheet

| Assets | Liabilities |

| Required reserves £800m Excess reserves £1,300m Loans £5,700m Securities £3,100m | Deposits £10,000m Bank capital £900m |

BarcSan's capital to assets ratio is £900m/£10,900 = 8.3%. Mercurial has exactly the same assets as BarcSan, but it has only £400 million in capital. It has an extra £500 million in deposits. Its ratio of capital to assets is 3.7% (£400m/£10,900m).

Mercurial's opening balance sheet

| Assets | Liabilities |

| Required reserves £800m Excess reserves £1,300m Loans £5,700m Securities £3,100m | Deposits £10,500m Bank capital £400m |

Now consider what happens if we assume a situation similar to that in southern Europe in 2013.

Both banks invested £500 million in bonds issued by Cypriot financial institutions. These now become worthless as the borrowers stop paying.[33] BarcSan can withstand the loss in assets because it maintained a conservative stance on its capital ratio.BarcSan's balance sheet after £500 million losses on Cypriot bonds

| Assets | Liabilities |

| Required reserves £800m Excess reserves £1,300m Loans £5,700m Securities £2,600m | Deposits £10,000m Bank capital £400m |

Its capital to assets ratio has fallen to a less conservative 3.8% (£400m/ £10,400m), but this is a level that still affords some sense of safety for its providers of funds. (Some writers refer to the capital to assets ratio as the leverage ratio, others take its inverse as the leverage ratio.)

Mercurial is insolvent. Its assets of £10,400 are less than the amount owed to depositors.

Mercurial's balance sheet after £500 million losses on Cypriot bonds

| Assets | Liabilities |

| Required reserves £800m Excess reserves £1,300m Loans £5,700m Securities £2,600m | Deposits £10,500m Bank capital - £100m |

A course of action is to write to depositors to tell them that it cannot repay the full amount that was deposited with the bank. They might panic, rush to the branch to obtain what they are owed in full. More likely is for the regulator to step in to close or rescue the bank. Occasionally the central bank organises a rescue by a group of other banks - they, too, have an interest in maintaining confidence in the banking system. In 2009 Royal Bank of Scotland and Lloyds Banking Group, following the sudden destruction of balance sheet reserves when the value of their loans and many securities turned out to be much less than what was shown on the balance sheet, were rescued by the UK government, which injected money into them by buying billions of new shares.

This was enough new capital to save them from destruction, but the banks are still clawing their way back to health and still trying to rebuild capital reserves.Why might banks sail close to the wind in aiming at a very low capital to assets ratio?

The motivation to lower the capital to assets ratio is to boost the returns to shareholders. To illustrate: imagine both BarcSan and Mercurial make profits after deduction of tax of £150 million per year and we can ignore extraordinary losses such as the sub-prime fiasco. A key measure of profitability is return on assets (ROA).

ROA- Net profit after tax

Total assets

Given that both firms (in normal conditions) have the same profits and the same assets, we have a ROA of £150m/£10,900m = 1.376%.[34] This is a useful measure of bank efficiency in terms of how much profit is generated per pound of assets.

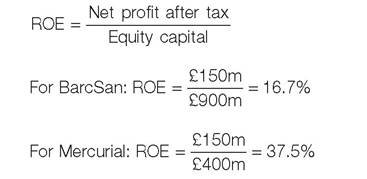

However, what shareholders are really interested in is the return for each pound that they place in the business. Assuming that the capital figures in the balance sheet are all provided by ordinary shareholders then the return on equity (ROE) is:

Mercurial appears to be super-profitable, simply because it obtained such a small proportion of its funds from shareholders. Many conservatively run banks were quizzed by their shareholders in the mid-2000s on why their returns to equity were low compared with those of other banks, and ‘couldn't they just push up returns with a little less caution on the capital ratio?' Many were tempted to follow the crowd in the good times only to suffer very badly when bank capital levels were exposed as far too daring. You can understand the temptation, and that is why regulation is needed to insist on minimum levels of capital.