CHAPTER TWO The Shape-Shifting, Never-Changing World of Fraud

Since the earliest years of American independence, the most prevalent business frauds have occurred over and over again, even if dressed up in different garb or framed in newfangled terms.

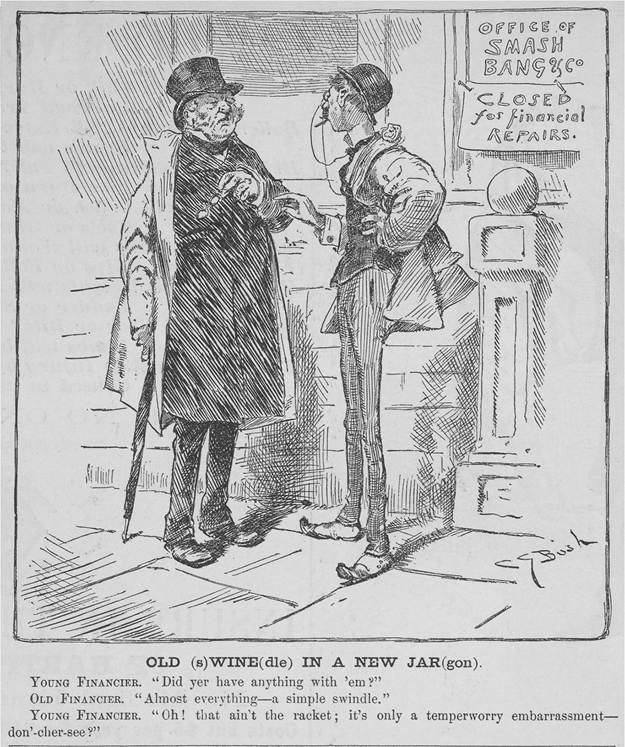

The “new smooth sell,” an observer of the American business scene noted in the early 1960s, “often consists of ancient gimmicks in shiny new packages, tailored to the modern age”1 A Harper’s Weekly cartoon captured this key insight nicely the better part of a century earlier, in the spring of 1884 (Figure 2.1). It depicted two “financiers” conversing about the recent failure of “Smash Bang & Co.” a reference to the celebrated collapse of Grant & Ward, a New York City brokerage firm that included former President Ulysses Grant as a passive senior partner. Promising high returns from investment schemes and intimating that it had the inside track on lucrative government contracts, Grant & Ward attracted millions in capital from prominent investors. Two of the partners—Ferdinand Ward and James Fish—along with several confederates, appropriated the firm's assets to maintain lavish lifestyles, finance their own stock and real-estate speculations, and cajole big loans from banks and financiers, even as their financial positions became more and more desperate. To the cartoonist, the bankruptcy of “Smash Bang” was nothing but “An Old (s)Wine(dle) in a New Jar(gon)” a repetition of a long-established style of financial perfidy by business insiders.2The Harper’s Weekly caricaturist, Charles Green Bush, had good reason to expect his readers to get the joke. For the previous two decades, Americans had encountered a steady dose of scandals involving corporate officers or partners of investment firms who deceived the public about their businesses' financial condition while lining their own pockets. Transcontinental railroads, investment banks, and insurance companies all followed the basic script, even if not every incident culminated in the worst examples of “Smash Bang”3

This chapter peers into the “Old Wine” forever occupying these and other American marketplaces, offering a compendium of the major varietals of business fraud.

The staying power of the dominant forms of deception reflects enduring dilemmas about whom and what to trust in a complex, integrated economy shot through with inequalities of access to information. It also speaks to

Figure 2.1: Smash, Bang & Co., Harper’s Weekly, May 24, 1884, courtesy of David M. Rubenstein Rare Book & Manuscript Library, Duke University.

the cognitive and emotional dimensions of economic decision-making in modern capitalist societies, themes that in recent years have attracted a rich experimental and analytical literature in behavioral economics. Once we have grappled with the persistent psychological dynamics of modern business fraud, we will be much better positioned to explore the shifting currents of American antifraud policies.

Persistence in Flim-Flammery

Old Swindles in New Jargon recur throughout American history. But they have been especially evident in sectors dominated by complex products or services and characterized by transactions among strangers. Four domains convey the key patterns: the selling of investment opportunities; goods retailing; the marketing of personal economic opportunities, whether for education/training, employment, or credit; and the managerial looting of companies.

From the rise of stock-j obbing in late seventeenth-century England, the quintessential capitalist investment scam has been the “pump and dump.”4 This type of fraud preyed on public fascination with some novel outlet for investment—in nineteenth-century America, stock in a land company that intended to sell off pieces of the Ohio Country or the Yazoo region of the Mississippi Valley, or maybe shares in a Gilded Age industrial corporation operating in some promising field. Its perpetrators stoked public expectations about the new terrain for money-making, while directing attention to a specific enterprise that served as the vehicle of deception.

Once all the vociferous pumping had elicited sufficient investment to drive up land prices or the value of a target company's stock, insiders dumped their assets onto the market.5This basic strategy has had innumerable variants. Sometimes the goal was less to sell at the top then to create favorable conditions for selling a stock short, using futures contracts to bet on a fall in value. At other moments, the plan was reversed, as market manipulators spread rumors that, if true, would presage big declines in the worth of some company or sector. Once the “hypocritical growling of the bears” had prompted “simulation of things dark instead of bright,” operators bought up shares on the cheap (or used futures contracts to bet on rising values).6 Furthermore, the specific means of “pumping” has evolved over the centuries. In the nineteenth century, fraudulent stock promotions relied heavily on duplicitous pamphlet literature and planted puffs in metropolitan newspapers.7 During most of the twentieth century, the chief conduits of manipulating market sentiment were mass-marketed tip sheets and telephone boiler rooms—offices crammed with desks, phones, and a battalion of stock salesmen who spent long days imploring prospects to take a plunge.8 In recent decades, the internet chat room has become a leading instrument for the marketing of dodgy securities.9 Yet the mode of operation remains little changed. First, use strategies of deception to influence public opinion about a financial asset, thereby shifting demand for it. Second, take the contrarian, and profitable, side of the ensuing trades, ahead of inevitable price corrections.

A second type of investment fraud, the pyramid scheme, also has retained its fundamental structure. Americans have named this type of swindle after the Italian immigrant Charles Ponzi, whose short-lived Boston finance firm, the Securities Exchange Company, dominated national headlines in the summer of 1920.

A charismatic charmer, Ponzi offered Bostonians 50 percent interest for the use of their money for between forty-five and ninety days, a return supposedly made possible by arbitrage in an obscure financial instrument, international postal reply coupons. For several months, Ponzi fulfilled his promises, stimulating a torrent of deposits attracted by word of mouth from ecstatic early investors. He soon became a celebrated Boston entrepreneur, acclaimed by the public and able to purchase a major stake in a venerable local bank. Ponzi, however, paid off older investors with funds provided by new ones, a practice that could only work as long as the influx of deposits exceeded maturing obligations. This form of financial engineering invariably collapses under its own weight. In Ponzi's case, a series of newspaper stories in the Boston Post exposed his scheme's rickety underpinnings, triggering criminal investigations and a panicky rush by depositors to reclaim their capital. Only briefly able to stem the now-outgoing financial tide, Ponzi's company soon failed.10Ponzi has had numerous emulators since 1920, with a spate of pyramid schemes emerging in the first decade of the new millennium, none bigger or more notorious than that engineered by Bernard Madoff, the New York City capitalist whose promise of steady returns through mysterious hedging strategies attracted thousands of investors, and billions of dollars of investments, from the early 1990s through 2008.11 But Ponzi also had sundry predecessors. Scores of nineteenth- and early twentieth-century stock promoters adopted this path, promising lofty dividend payments and then delivering them through capital furnished by later investors. So too did a series of financiers operating outside the formal banking system.

Indeed, if historical priority determined idiomatic expression, Americans might well have reacted to the Madoff scandal by describing it as yet another “Franklin Syndicate,” “Fund W” or “Ladies Deposit,” rather than the latest Ponzi scheme.

The Franklin Syndicate was the moniker of an 1899 pyramid scheme based in Brooklyn, for which a twenty-one-year-old clerk, William Miller, served as front man. Fund W operated out of Chicago earlier that decade, attracting over $1 million in deposits from investors all over the United States and Canada. Based in Boston from 1877 through 1880, the Ladies Deposit Savings Bank was run by Sarah Howe, a respectable-looking New Englander in her fifties. The Ladies Deposit only permitted investments from unmarried women of modest means, the total of which exceeded $500,000 by 1880. Each of these enterprises, with the exception of Sarah Howe's Savings Bank, advertised as mutual funds that would pool the savings of small investors, and then rely on access to inside information to earn enormous profits through speculation on the nation's exchanges. (Howe claimed that bequests by wealthy Quakers had created a surplus fund from which to pay interest to thrifty single females.) Each concern guaranteed ample payoffs (interest of 8 percent per month by the Ladies Bank, the ability to double or triple one's money within a year by Fund W, dividends of 10 percent a week by “520% Miller”), honored at first through the kind intercession of investing latecomers.12 For at least 135 years, purveyors of pyramid schemes have followed a common script. Promise attractive, and often spectacular, returns. Rely on injections of capital to make good on those promises. Then sit back and watch as early investors become pied pipers, attracting exponential growth in investments, which those in charge skim off the top.Such constancy in the scripts for business frauds applies as well to duplicitous retail marketing, which has involved mainly variations on the “bait and switch.” Whether through reliance on window displays, newspaper advertisements, marketing circulars, catalogue copy, radio spots, television commercials, websites, or spam, this routine has begun with the same opening gambit—bombast.

Amid the bustle and clutter of daily life in a capitalist society, find a way to grab consumers' attention, to persuade them to invite a salesperson into their homes, or to drive traffic into a store—sometimes located in a customer's own neighborhood, sometimes in a call center, and by the late twentieth century, in cyberspace. The bait involves some fabulous deal, a discounted price or a claim of fantastic quality that may seem too good to be true. In the most straightforward of these deceptions, consumers purchase the advertised good or service, only to discover a yawning gulf between promised attributes and actual value.All too often, however, the initial come-on has served as prelude. Once consumers crossed the threshold of a retail establishment or invited some hawker into their living room, salespersons moved on to the “switch.” The advertised sewing machine, or refrigerator, or set of dancing lessons, or MP3 player, inexpensive to be sure, was out of stock, no longer available, or really not a good deal after all because of its inferior quality or functional limitations. At this juncture, the goal became convincing customers to prefer a costlier alternative, which represented, when considered from every relevant angle, a much better value. In making this case, salespersons used all the wiles of the hard sell.13 Known as “trading up” in the discourse of mid-twentieth-century consumer marketing, and “upselling” since the 1980s, this tactic often raised complicated questions about how to differentiate aggressive selling practices from inten-

tional deceit. Was the advertised special completely unavailable, or only available to a lucky few? Did salespersons sing the praises of more expensive models, or deprecate the advertised item as a shoddy, even worthless imitation? As observers of the commercial scene periodically noted, “there is a fine line between a bait and switch and a trade up.”14

No such ambiguity surrounded a related sales tactic—the making of oral promises at odds with the fine print of written sales contracts or the quality of provided goods and services. Such divergence has proved common in the vending of high-ticket goods and services on credit terms, in part because of a longstanding precept in American law, known as the “holder in due course” doctrine. From the 1842 case of Swift v. Tyson through the mid-1970s, this doctrine shielded innocent third-party holders of debts created by the sale of consumer goods. If the original creditor committed fraud in enticing a consumer to sign a contingent sales contract or a promissory note, and then sold that financial instrument to another person or firm who remained unaware of the original deceit, then the consumer could not avoid payment to the new creditor on the grounds that the original transaction was tainted by fraud. Sale or transfer wiped clean any legal stain left by sales misrepresentations.15

The holder in due course doctrine encouraged aggressive misrepresentation by sellers of consumer goods on credit. Salespersons and agents could shade the truth or lie outright in order to wheedle contractual signatures out of consumers, knowing that the contract imposed different terms and conditions. Perhaps the fine print incorporated fees or expensive insurance coverage, or specified a different base price, order quantity, or interest rate. Alternatively, customers who might think that they had taken merchandise on a trial basis left stores, according to the documents they had signed, as contingent owners who had just agreed to sales on installment plans. Once customers signed their name to a sales contact, firms could then transfer the resulting financial obligations to a loan broker or finance company at a heavy discount, leaving consumers to fend off uncompromising debt collection from these financial intermediaries.

Such schemes bedeviled the twentieth-century consumer marketplace. They became commonplace amid the explosion of debt-financed durable goods during the 1920s, sending streams of disgruntled urban consumers to seek the help of the country's new legal aid societies.16 After World War II, American suburbia and the older terrain of small-t own rural districts each spawned scores of home improvement companies and auto dealerships that worked versions of this racket; so did inner cities, with furniture stores, home security companies, electronics retailers, and sellers of frozen-food plans all garnering notoriety in this regard.17

The template for such duplicitous extension of consumer credit, however, reached well back into the nineteenth century. As early as the 1860s, scores of businesses in the emerging home improvement sector had embraced the mix of false oral promises, tricky fine print, and reliance on the holder in due course doctrine, carrying off schemes of misrepresentation every bit as sophisticated as those undertaken by their latter-day counterparts. The key players were lightning-rod companies, whose traveling representatives bombarded town and countryside with dire warnings about the risk of fire from every summer storm, while touting the new metal devices that could protect dwellings and outbuildings from heaven's angry bolts.

For these firms, bait and switch became standard operating procedure. Their agents lowballed estimates of installation costs and misrepresented any insurance coverage accompanying the sale of a rod system, while tucking expensive terms into sales contracts. In rural counties, salesmen explained to farm families that because their firms had just entered the area, they required a fine set of well-located buildings to demonstrate the quality of their rods, and so were willing to erect them for a big discount. (This enticement would be emulated a century later by purveyors of aluminum siding, swimming pools, and other home improvements.) Once a lightning-rod man cajoled or frightened some farmer into signing a purchase agreement, he would be followed some days later by an installation crew, and then by the firm's collecting agent. The collector would demand a much greater sum than the one to which the owner thought he had agreed, point out clauses in the fine print of the contract, and threaten legal action if the owner did not pay, or at least sign a note for the amount due. If the farmer agreed to the latter option, the company would sell the note to a local broker, leaving the farmer to grapple with the finer points of the holder in due course doctrine.18 The rod “game” was emulated by sellers of “plows, horse rakes, or almost any kind of a rake that will rake in its victims.”19

As with investment swindles and consumer rackets, the fraudulent marketing of educational courses, access to credit, and commercial openings has demonstrated great continuity. Such scams dangled some big opportunity before the public. It might be the chance to learn, in mere weeks, the essentials of bookkeeping or telegraph operation. It could be an opening for agents to represent some late nineteenth-century consumer goods manufacturer, with the chance not only to earn commissions from sales, but also royalties by recruiting other agents. Perhaps it involved an offer of a low-interest home loan in the years after World War I, the prospect of listing homes for sale with a real-estate agency that “guaranteed” results in the 1950s, or an exclusive franchise for an expanding national chain in the 1970s. In the midst of the exploding growth in household debt since the 1980s, it might involve the means to consolidate and refinance mounting credit card debt, or to furnish some form of “foreclosure rescue” to homeowners crushed by the housing collapse of 2008-09.

In all of these contexts, whenever a seeker of self-improvement, credit, business opportunity, house sale, or employment evinced interest by responding to an advertisement, details speedily followed. Without fail, the more extensive descriptions of the wonderful training course, generous loan terms, or well- remunerated employment would be accompanied by a notice of the need for some kind of payment up front—money for books and other materials, purchase of the exclusive right to sell a patented manufactured good in some rural county, a bill for a case of samples, charges for loan referrals or running a credit check. Such outlays, the “high pressure... big promise boys” would explain, constituted minimal, but unavoidable, investments in opportunity. Upon remittance of these “advance fees,” as antifraud professionals have termed them since the early twentieth century, duped Americans soon experienced the bitterness of dashed expectations. Sometimes the “opportunity” turned out to be inferior to advertised promises. The exclusive license to sell a patent right would only confer the privilege of vending a useless invention. Guarantees of home sales, in the end, translated only into guaranteed listings in a real-estate brochure with no circulation. At least as frequently, fly-by-night enterprises took the money and ran.20

The reoccurrences of managerial fraud have followed comparable storylines. Amid the late-antebellum frenzy to build railroads and develop Appalachian coal mines, the officers of several companies staved off their own looming financial difficulties by selling thousands of shares of unauthorized stock. In the 1870s, the failure of several New York City life insurance companies brought revelations that they had placed fake policies on their books in order to paper over worsening finances, and so legitimate handsome salaries and ongoing dividend payments. During the great Florida real-estate boom of the 1920s, developers gained control of key banks in both Florida and Georgia, and proceeded to shower loans upon themselves and their associates, all the while insisting, often with the help of bribed state bank examiners, that their institutions remained paragons of financial prudence. Toward the end of the Great Depression, the American business establishment was rocked by an accounting scandal at the drug company McKesson & Robbins, in which corporate insiders faked inventories and purchase orders from a Canadian subsidiary as a way to appropriate the parent firm's profits.

The citadels of American capitalism continued to confront high-profile managerial control frauds in the decades following World War II. In the immediate postwar period, financial wheeler-dealers such as Lowell Birrell and Alexander Guterma made a fine art of looting the midsized industrial corporations that they controlled through complex stock and loan machinations associated with mergers. One crucial tactic for both was to use corporate stock as collateral for loans from high-interest moneylenders and then to default, allowing the creditors to dump shares on the market without public disclosure. During the Savings and Loan crisis of the 1980s, dozens of financial institutions relied on inflated appraisals of real estate to maintain a faςade of strong earnings, which provided cover for huge salaries and bonuses. And around the turn of the millennium, a slew of large telecommunications, energy, and consumer products companies, among them WorldCom, Enron, and Sunbeam, manipulated their reports of financial performance to meet stock analysts' predictions and buoy stock prices. The most common tactics involved immediately booking expected streams of future revenue, shaving cost tallies, and even pretending that some ongoing liabilities actually constituted capital assets. In most cases, this fiddling was abetted by external auditors whose firms had come to depend on consulting contracts with the same companies.21

As these truncated descriptions indicate, the precise nature of deception varied from scandal to scandal, reflecting the evolution of corporate institutions, governance structures, and regulatory oversight. Whatever the details, the crux of deceit remained the same. Managers cooked the books to convey false impressions about corporate finances and prospects. Public misrepresentations provided rationales for munificent remuneration, as well as cover for self-dealing, the granting of sweetheart loans or contracts to cronies, and/or the unloading of shares controlled by executives. In the most egregious instances, such insider pilfering resulted in bankruptcy. Over and over, it was the tale of Smash Bang.

One might multiply these examples of recurrent motifs in deception within the history of American business, considering, for example, fictitious-pricing scams (the setting of falsely high “original” prices so as to create the appearance of bargains), the counterfeiting of branded goods, the running of mock auctions, or the tendency of some failing enterprises to defraud creditors, thereby transforming insolvency into a profitable enterprise. But the preceding overview suffices to establish the broad point. Most swindles have fallen into a discrete number of recognizable types, with little alteration of fundamental method.

The Modern Problem of Trust in the Marketplace

In light of such continuity, one might wonder about the inability of Americans to wise up over the past two-hundred-plus years. A Texas newspaper editor framed the issue in 1859 as he mused over the “perennial crop of fools” that fell for “plausible cheats”: how could it be that “the man of to-day, with all the lights of the past to guide him, is just as much of a credulous idiot as at any time since the fall of Adam?”22 This question should only be sharpened by Parts II through V of this book, which explore the substantial efforts to combat the problem of business fraud over two centuries, not least through strategies of public education. William H. Crosby, a lifelong swindler, encapsulated this historical puzzle in the 1923 book Confessions of a Confidence Man. “Every few months,” Crosby pointed out to journalist Edward H. Smith, who actually penned the Confessions, “the newspapers and periodicals expose some sort of bunko game. The courts are continually sending our fellows to jail. The people are much better educated than they used to be.... But the confidence game is greater than ever.”23

One crucial explanation involves the imperfect transmission of economic memory from generation to generation. In the short term, prevailing scams become so widespread as to gain notoriety, limiting their effectiveness. Such was the case with lightning-rod companies. By the 1870s the “lightning-rod man” had become an iconic character of commercial shiftiness and the hard sell, lampooned by writers such as Mark Twain, used by journalists and social commentators as a figurative emblem of economic trickery.24 But Americans coming of age do not necessarily imbibe the lessons that their parents have learned. Business frauds, moreover, have never needed to fool all of the people all of the time. They result in acceptable returns so long as even a small percentage of individuals take the bait. Duplicitous lightning-r od agents found customers to fleece through the end of the nineteenth century and beyond.25

At a deeper level, business frauds exhibited such striking strategic continuities in the United States because the individuals who carried them out recognized the implications of a key feature of economic life in industrialized societies—asymmetries of information. Such imbalances intensified an omnipresent sociological dilemma. When transacting business, whom should one trust?

The dilemmas posed by differentials in relevant knowledge between counterparties, of course, have existed as long as there have been markets. Every premodern civilization had to grapple with the fact that sellers, and sometimes buyers, possessed informational advantages, and throughout most of recorded history, the mercantile classes have confronted popular resentments about a perceived penchant for misrepresenting wares. But the process of industrialization exacerbated inequalities in access to pertinent economic information. Technological complexity in the manufacturing of goods and the performance of services left consumers confronting daunting challenges of quality assessment. Revolutions in transportation and communication expanded the geographic scope of commercial activity, and so multiplied the quandaries associated with trading/investing at a distance and dealing with strangers. Innovations in financial instruments generated complex contracts whose legal implications often confounded the individuals and firms using them, while an explosive expansion in the use of credit generated tough questions about how to evaluate the trustworthiness of counterparties. And with the advent of the modern corporation, a growing proportion of transactions took place between large-s cale organizations, whose bureaucracies possessed much knowledge about goods, business practices, and legal precepts, and often far less about small businesses and individual consumers. Without the pervasiveness of uneven access to information, none of the most common strategies of business deception would have found a sustainable niche.26

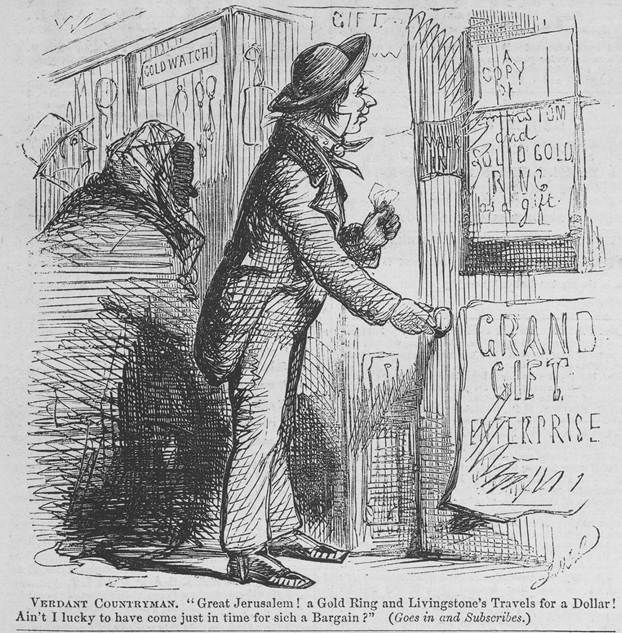

Practitioners of business fraud have often targeted demographic groups likely to suffer from informational gaps or to lack the savvy that accompanied long-term participation in modern transactional environments. In antebellum Eastern cities, operators of mock auction houses, gift enterprises (stores selling bundled discount goods that included prizes), and “bargain” stores licked their chops whenever newcomers from the country crossed their thresholds, a recurring scene captured in an 1858 Harper’s Weekly cartoon of a “verdant countryman” (Figure 2.2).27 As European immigrants poured into the United States during the nineteenth century, most encountered sharpers seeking to separate them from the savings with which they hoped to make a new start.28 The more recent upsurge in immigration since the 1960s engendered innumerable scams that singled out Hispanics, Asians, or other newcomers.29 From the Gilded Age onward, “work-at-home” schemes targeted poor women who lacked understanding of commercial law.30 In the post-World War II inner city, bait-and- switch retailers preyed on the urban poor, who possessed low levels of formal education and confronted local retail monopolies.31 Late twentieth-century financial and telemarketing fraudsters pursued America's growing elderly population; lonely and isolated, and sometimes facing cognitive impairments, a significant minority of the aged proved to be credulous about deceptively characterized goods, services, and investments.32 Even educated native-born Americans might be the preferred targets of financial scams, as degrees and

Figure 2.2: The antebellum “Verdant Countryman” enticed by the bargain. Harper’s Weekly, April 17, 1858, courtesy of David M. Rubenstein Rare Book & Manuscript Library, Duke University.

professional careers did not ensure familiarity with the securities markets. Teachers, ministers, doctors, and middle-class widows have long had a reputation among fraudulent promoters as prone to bite at a good investment pitch.33 In part, the history of American business fraud has constituted an unending search for economic novices.

Encounters with all the misrepresentations and swindles in the American marketplace, of course, spawned wariness, a dynamic well understood by the more adept practitioners of commercial and financial deceit. Many economic actors, including one-time greenhorns, came to recognize their disadvantages in access to relevant commercial information, as well as the pervasive threat of marketing falsehoods and exaggerations. Having witnessed or suffered through the indignities that came with a retail fleecing or a financial scam, they put up their guards.

This reality gave novel twists to the age-old imperative of earning trust. As the economy became ever more integrated on a continental and international basis, long-term profitability depended on reputations for reliability, quality, service, and value. From the mid-nineteenth century onward, Americans developed a slew of institutional strategies to assess the reputation for goods, services, assets, and business entities. These innovations ranged from trade journals, credit reporting firms, investment analysts, and bond rating agencies to product testing organizations, consumer groups, and corporate efforts to shape public associations with products and services, known as “brand management.”34 Yet the very success of these adaptations spawned new opportunities for misrepresentation and fraud. Within any modern process of fashioning trust lay a blueprint for how to simulate it, how to appear to possess some trusted mark of integrity so as to carry out fraud against economic neophytes and sophisticates alike.35

Again, the key patterns among swindlers and more legitimate firms that developed deceptive business practices recurred over time. Three stand out— social mimicry, personalization amid bureaucratization, and deflection. These strategies could overlap, as American firms that embraced deceit as a fundamental business strategy often relied on the first two, and sometimes on all three. Nonetheless, it is helpful to separate these economic charades.

To point out that American business frauds have depended on elaborate acts of impersonation risks belaboring the obvious. But Herman Melville’s 1857 novel The Confidence-Man furnishes an important clue about the deeper historical significance of this dimension of economic deception. Its setting, the steamboat Fidele, symbolizes the emerging commercial world of distant linkages and anonymous counterparties. As the Fidele—an invocation of the Latin root fides, meaning trust or belief—makes its way down the Mississippi River, crossing the regions of America’s midcontinent, it takes on hundreds of passengers from every racial and ethnic group and every social status, all milling together in one floating microcosm of a larger society. Aware of how difficult it has become to assess the trustworthiness of all the strangers and deal-making around them, passenger after passenger manifests an abiding skepticism about everything and everyone. The prevalence of deceit had left Americans of Melville’s time already inclined to look askance at wares and projects offered in the public marts, and the hawkers who pushed them. Thus as Melville’s Satanic (or, as some interpreters have argued, Christlike) Confidence Man saunters about the steamboat, he continually confronts the challenge of overcoming ingrained distrust. To prepare the way for the impositions that he visits on various passengers, he must perform one “masquerade” after another. From scene to scene, the Confidence Man seems to change shape, assuming the persona of a wizened and disabled African American man, a Mason fallen on hard times, a well-dressed traveling agent for a new charity for the Seminoles, the president of a coal mining company, and several others. In describing the serial misrepresentations that take place on the Fidele, Melville summons the world of theatre. As one distrustful character in the novel insists, “To do is to act; so all doers are actors.”36 Swindlers, Melville realized in the early years of America's encounter with economic relationships rife with information asymmetries, must look the part, possess the right props, know the right cues. This basic truth has structured business frauds from Melville's time to our own.

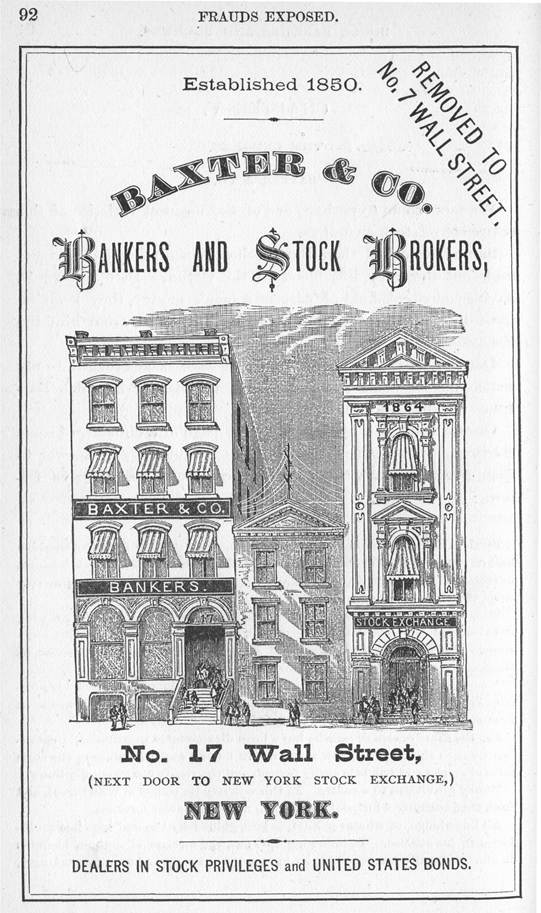

The simplest forms of dramatic imitation appropriated name and place. As soon as nineteenth-century manufacturers began to develop brand awareness among consumers, opportunists passed off counterfeit goods as the original. Many businesses tried to siphon off trade by adopting a commercial moniker that resembled that of a well-regarded enterprise, or that communicated an image of solidity and respectability. For the same reason, architects of business frauds appreciated the marketing power of location. If the public associated an industry with a single city, or neighborhood, or street, then it made good sense to set up shop there—or at least appear to do so. Up until the 1920s, for instance, New York's financial district was home not only to the nation's leading investment banks and brokerages, but also a motley assortment of short-lived bucket shops and dodgy mutual funds that touted their geographic respectability. A Wall Street address, like the one that the bogus New York City brokerage house Baxter & Co. trumpeted on the front of its 1870s marketing circulars (Figure 2.3), usually paid dividends.37

More subtle techniques of emulation concentrated on the general trappings of commercial success, rather than the specific markers of well-regarded firms. Promoters of financial swindles were especially inclined toward such tactics. Like the leading characters in the 1973 movie The Sting, most maintained offices “fitted up with great elegance” and lived the high life in order to convey an aura of wealth and social standing.38 Before the adoption of the New Deal, dodgy financiers frequently enticed local dignitaries to serve as company directors, with “deacons of churches, bank presidents, provost marshals, and eminent lawyers” serving the purpose, should ex-governors or former Civil War generals not be available. These “decoy ducks” would receive a few thousand dollars' worth of shares in exchange for the use of their names. The hope, often realized, was that potential investors would view these celebrities' participation as endorsements of legitimacy and credibility, and so “bring others near

Figure 2.3: Front page of Baxter & Co. circular, circa 1878, in Anthony Comstock, Frauds Exposed: How the People Are Deceived and Robbed, and Youth Corrupted (New York, 1880), 92. Note that the image at once emphasizes the firm's proximity to the New York Stock Exchange and depicts the NYSE as housed in a smaller and less substantial structure.

enough to be made game of.”39 In some cases, even a bogus prominent person could do the trick. One fraudulent Texas oil trust estate in the 1920s used as its public face “General” Robert A. Lee, an elderly former janitor whom the enterprise claimed to be related to Robert E. Lee. By sending out a torrent of courtly letters from “General Lee” and placing his stately image on every trust certificate, this outfit lured thousands of white Southerners to throw away their savings by investing in the venture.40

The most powerful means of getting people to view a fraudulent investment as legitimate, however, remained the payment of initial dividends and the manufacture of upward price movements. Since the advent of modern securities markets, nothing has persuaded investors to take a flyer on a corporation, place their funds at the disposal of a brokerage house, or jump into a pyramid scheme more than beguiling evidence of its capacity to generate returns. Whether in the form of capital appreciation or payments dressed up as income distributions, tangible markers of market sentiment and earnings struck many Americans as economic omens that commanded respect, even when accompanied by warnings that past results offered no guarantees of future prospects.41

The deceptive firms that turned to social mimicry exploited modern badges of upright economic conduct. They forged a trademark, appropriated the high standing that a firm had built up with credit bureaus, traded on the esteem enjoyed by renowned directors, basked in the protection of “independent” audits, or simulated the behavior of successful businesses. By contrast, the method of personalization harkened back to much older means of demonstrating trustworthiness. This technique still required satisfying dramatic performances. But alongside attention to convincing backdrops and costumes, many practitioners of fraud recognized the value of having key actors carry off roles with emotional plausibility.

For a host of American businesses that relied on deceitful practices, oral communication and person-to-person encounters remained crucial tactics of misrepresentation. Almost every version of the bait and switch incorporated this approach. Whatever the nature of the bait, the switch depended on personal interactions between salespersons and customers. The pivotal assertions and assurances came through rehearsed lines and gestures. Artful pitches had the aim of eliciting confidence, not just in the goods or services for sale, but first and foremost in the flesh and blood sellers. When nineteenth-century lightning-rod agents worked their magic, 1950s used-car salesmen touted different and more expensive sedans from those featured in television spots, or early twenty-first-century mortgage brokers dangled exotic subprime mortgages before prospective homeowners, the first rule of selling was always in effect: before deceptive economic actors could sell the product or service, they had to “sell themselves,” to “gain the friendship” of the customer or client and convey the air of someone whose word deserved credit.42 The effective pitchman of phony investment vehicles, a Midwestern newspaper noted in 1910, was not only “always well groomed, always redolent of the fragrance of daily tubbing, massaging, and the barber shop route,” but also possessed of a “dazzling smile and ingratiating manners.” As the German sociologist Niklas Luh- mann has put it with regard to the more general problem of gaining social confidence, “whoever wants trust must take part in social life and be in a position to build the expectations of others into his own self-presentation.”43

Adding a personal touch to schemes predicated on deception was a straightforward matter for firms that conducted business face to face. But this approach also beckoned to entrepreneurs who hoped to pull off misrepresentations from a distance. During the first several decades of mail-order selling, the voluminous marketing literature unleashed by fraudulent firms struck a familiar tone, emulating the down-to-earth communications of the era's most successful firms.44 Several promoters of fraudulent stocks in the early twentieth century cultivated close relationships with their investors. In pamphlets, market letters, and editorials, they portrayed any trials and tribulations that afflicted their companies as shared troubles, and solicited investments on the basis of emotional bonds forged through years of mutual risk-taking.45 Most pyramid schemes pursued a more indirect approach to cultivating trust through personal links, relying on either the marketing skills of commission agents, who tapped their own social circles, or the cadre of satisfied early depositors. After receiving the first round or two of promised dividends, the latter made themselves into informal investment barkers who bragged about their good fortune and encouraged friends and family to follow their lead.46

Ties born of shared social circumstance or worldview facilitated such strategies. Members of an ethnic or racial group, religious organization, profession, or political persuasion have proven vulnerable to scams perpetrated by individuals with the same demographic characteristics or cultural markers. In the late 1980s, regulators and financial journalists termed this pattern “affinity fraud.” As one California state official explained in 1992, “normally suspicious people substitute their faith in their group for their own independent judgment on the merits of a deal.” Pyramid schemes in the late twentieth and early twenty-first centuries exploited this tendency to rely on the supposed wisdom of one's social networks. In its early years, Bernard Madoff's fake hedge fund, Ascot Partners, cultivated Jewish investors, both individuals and institutions; similar, if less gargantuan, frauds ensnared Seventh-Day Adventists, African American Baptists, Utah doctors, Masons, conservative Republican activists, Hispanic and Indian immigrants, even alumni from and parents of students attending elite universities.47

There is some evidence that the incidence and scope of affinity fraud increased during and after the 1980s, a phenomenon perhaps related to the growing fragmentation of American society and the related sharpening of social identities. Extensive immigration and expansion in the number of tightly bound religious communities each fostered the development of closeknit social worlds that defined boundaries between trusted insiders and the rest of society. Such circumstances heightened opportunities for individuals within a given communal circle to lure their fellows into some commercial or financial trap.48

This kind of chicanery, however, had numerous precursors. The depredations of Sarah Howe's Ladies Deposit Savings Bank fit this pattern, as female depositors manifested enormous faith in their benefactress.49 So too did a decades-long string of religiously based investment frauds.50 Every burst of immigration also generated scams perpetrated against particular nationalities by their countrymen.51 The early twentieth-century racket in bogus remittance banks represented a ruthless example of this type of fraud. Focused on one ethnic group, these businesses advertised their capacity to transfer funds across the Atlantic in the foreign-language press and used immigrant agents from the region in question. Each year, as one Western newspaper reported in 1905, these fake firms “filch millions of dollars out of the pockets of the most ignorant and helpless immigrants.”52 Even if the term “affinity fraud” emerged only toward the end of the twentieth century, the practice had a venerable American lineage.

The third and least common method of garnering reputation for integrity pursued the most indirect tactics, cloaking deception behind a public posture of fraud-fighting. In a sector that had gained notoriety for legerdemain, such as the installation of lightning rods, sales agents might, as some did, begin their pitch by deprecating “the trickery of some agents” and proclaiming that, unlike their competitors, their firm did “business on the square.”53 Similarly, ads by nineteenth-century purveyors of quack medicine might caution consumers to beware of unscrupulous competitors who injured patients with spurious elixirs, even while explaining that their in-house physicians made “a specialty of all chronic diseases of men and women,” and had great skill in diagnosing and treating individuals by mail (Figure 2.4).54

Far more elaborate efforts to demonstrate probity emerged in the nation's securities markets. Several early twentieth-century promoters of fraudulent stocks and commodity-investment vehicles circulated market letters and fi-

CAUTION

Beware of Fraudulent AdverUsIner Doctors and Medical Companies who Advertise to Give Free Samples of Medicines, Free Prescriptions and Cheap MedIoaI Treatment

Tlio Uett Ia th î CliOftpogt-SkIII, Iloneaty. Ilgperienee anti Ilellftbillty in YourPhynIoiiina la XMiat You Aecd- l>r, Ifathawiiy&Ca Are PeriiianCntIy Looated in Title City Jinro Been for Yeara, anti Hnve the Co»Iftlenco of the Publlo.

Figure 2.4: Segment of Dr. Hathaway & Co. advertisement, San Antonio Express, Feb. 12, 1899, 12, courtesy of America's Historical Newspapers, Digital Edition published by Readex, a division of NewsBank, Inc.

nancial publications that warned investors about bogus companies, in addition to pushing worthless companies they themselves owned. Thus the Bankers’ and Merchants’ Guarantee Credit Exchange (BMGCE), a fraudulent New York City brokerage firm that operated around the turn of the twentieth century, boasted in its pamphlets that its mission was to “crush out all unprincipled concerns and direct the public to reliable firms.” To identify the duplicitous, BMGCE explained, “we employ men of sterling integrity who are virtually detectives.” The brokerage further directed its subscribers to a fake mercantile agency, the Investors Protection Bureau, which for two dollars would send out “a report on brokers, merchants, and manufacturers,” enabling investors “to protect [themselves] against loss by fraud, failure and otherwise.”55 This technique of “concealing [one’s] own sins by a loud denunciation of the sins of others” became commonplace among the financial tip sheets of the 1910s and 1920s.56 The idea with such diversions was to fend off potential charges of knavery against one’s own business by casting aspersions elsewhere. Consumers and investors, the thinking went, would let down their guard when dealing with a firm that furnished such clear evidence of public-spirited concern for fair dealing.

These three strategies for solving the problem of trust recurred because they tended to work in the short term. Successful practitioners of deceit recognized that Americans, facing so many information asymmetries, developed rules of thumb to distinguish businesses in which one might place some degree of confidence from those best left alone. By embracing the poses of commercial mimicry, personalized salesmanship, and/or deflection, these operators took advantage of such informal guideposts. Success in commercial deception, then, required an appreciation for the psychology of coping strategies amid the dizzying hurly-burly of modern economic life. Indeed, in every era since the United States gained its independence from Great Britain, business fraud has required a keen grasp of human sentiment and behavior. As the secretary of the Colorado State Horticultural Society noted in an 1887 paper about duplicitous tree peddlers, swindlers who thrived at their craft were not only unscrupulous, shrewd, and “endowed by nature with the ‘gift of the gab' ”; they were also “well versed in all the foibles of human nature.”57 Those foibles deserve some exploration in their own right.

Deceptive Practices and the Psychology of Economic Decision-Making

Over the past decade, a growing number of historians have made emotional life a central subject of inquiry. The emotions, these scholars have shown, have a history—they are contingent upon social and cultural context and are learned as well as experienced, perhaps in equal measure. Transformations in society and culture, such as the French Revolution and its aftermath, can so powerfully remake public touchstones of value that they refashion the very sensation and awareness of sentiment.58 But the fact of some, or even much, emotional change does not imply processes of wholesale emotional transformation. A further explanation for the tendency of the same basic frauds to bedevil American marketplaces across the centuries lies in the ability of their perpetrators to rely on a fixed set of psychological nudges. From the age of P. T Barnum to that of Bernard Madoff, social commentators have identified an enduring set of affective tendencies that made Americans susceptible to humbug and imposition.

Some of the psychological impulses that show up again and again in the history of business fraud reflect widespread aspirations or anxieties. None received more attention, either from swindlers or observers of market behavior, than the passion for easily attained wealth. Investment frauds catered to this dream and the gambling instinct that it fostered, celebrating “the desire for gain,” which, as a circular by one fraudulent Gilded Age brokerage put it, was “the strongest impulse of the human heart.” In a society that produced overnight fortunes and disseminated rags-to-riches narratives, promoters could count on interest in plausible schemes to “sweep [individuals] to riches” and render investors “independent for life.”59 Many investment cons intensified such appeals by offering a way to become “insiders” within the byzantine world of finance. The fake blind pool around the beginning of the twentieth century, like the sham hedge fund around its conclusion, claimed to take advantage of special market intelligence or investment opportunities that were not readily available. “We employ SPECIAL CROP EXPERTS,” screamed one New York City brokerage firm's 1897 advertisements for participation in a “SPRING WHEAT POOL” that was privy to “EXCLUSIVE INFORMATION” and operated “for the sole benefit of our active customers.” Such swindles promised exclusivity as well as routes to wealth.60 Healthcare swindles, by contrast, played on fundamental fears. Bogus nineteenth-century patent medicines, like quack mid-twentieth-century cancer cures, dangled hope in front of those laid low by disease, correctly anticipating that the afflicted desired talismans of optimism.61 Whether conjuring up visions of Easy Street or medical miracles, swindlers exploited proclivities toward fantasizing and wishful thinking.

Findings within psychology, and especially within the burgeoning literature of behavioral economics, point the way toward a more refined understanding of why so many venerable frauds have maintained niches within American business culture. Since the 1970s, behavioral economists have conducted psychological experiments all over the world to assess how subjects choose between economic alternatives. This research has documented patterns of behavior that diverge from the expectations of “rational” economic decision-making. Such conduct, the researchers argue, suggests an array of cognitive tendencies and emotional dispositions that do not fit longstanding assumptions about motivations for economic action. The relevance of this research for the history of business fraud lies in the striking correspondence between these modes of thinking/feeling and recurring features of economic deceit.

Behavioral economists explain nonrational modes of economic assessment in terms of biases (filters that shade how individuals make sense of experience) and heuristics (mental shortcuts that people use when confronted with a massive amount of information to process).62 None of the habits of mind identified by behaviorists represents a full picture of economic decision-making. They encompass a set of common intuitions and initial impressions, which interact with other cognitive perceptions, emotional responses, and perceived norms, and which individuals often revise or reject in light of analysis and sober second thought. A number of scholars argue that these biases and intuitive shortcuts emerged over the long history of human evolution because they allowed people to cope with complex social situations.63 Regardless of whether such cognitive tendencies originated in the deep past or emerged with more complex civilizations, and whether or not they reflect the hard-wiring of brain chemistry or cultural processes of learning, they have made modern humans vulnerable to deception.

The pervasive faith in “social proof,” for example, helps to account for the nature of investment frauds. A key element of most pump and dump swindles and all pyramid schemes is that once a critical mass of suckers takes the bait, their example prompts others to follow in their wake, often after hearing about the opportunity from acquaintances who exult in their good fortune. Most latecomers place their faith in the investigation done by those who preceded them (going along with the herd), especially, as in the case of affinity fraud, when the people they emulate come from the same trusted social group.64

Strategies of commercial imitation dovetail with a thought process that behaviorists refer to as the “representativeness” heuristic. This mental habit leads individuals to emphasize anecdotal social cues and markers when making judgments of economic value, particularly when access to alternative kinds of evidence is limited, or that evidence requires extensive and complicated analysis. Whenever these signals have a salience—whenever, that is, initial impressions are strong because of effective presentation—many people assume that they convey all the information they need to know. They presume, in other words, that the signals stand for or represent underlying reality.65 In any social environment characterized by extensive reliance on this cognitive benchmark, some percentage of economic actors will remain susceptible to fraudulent schemes that pull off convincing shows of social mimicry.66

A third mental shortcut, the “availability” heuristic, encourages individuals assessing the merits of economic alternatives to place great weight on easily recalled events and memorable personal experiences. Several abiding characteristics of investment frauds track this method of cognitive evaluation. Promotions of spurious companies invoke examples of firms whose rapid growth brought tremendous fortunes to investors who had the good sense to get in early. The choice of exemplars shifted from era to era, from mining and oil ventures, to the daring speculative exploits of the late nineteenth-century financier Jay Gould, to Bell Telephone and Ford Motor, to Microsoft and Intel. But the goal remained that of associating the fraudulent firm with others that had burst into prominence and extraordinary profitability by laying out precise, often exaggerated calculations of the returns earned by those who purchased shares in such companies at the earliest opportunity.67 Early dividend payments by fraudulent investment schemes have similarly taken advantage of the availability heuristic, which gives investors or depositors a strong nudge toward seeing the enterprise as legitimate.

The prevalence of this cognitive tendency further helps to account for investment swindles' cyclical character. Every speculative boom since the American Revolution has invited financial frauds, from phony early nineteenthcentury land companies to the creation of supposedly AAA-rated collateralized debt obligations amid the housing bubble of the early 2000s. This same correlation has emerged elsewhere since the seventeenth century. Whenever asset values shoot up, fantastic claims find more receptive audiences, because investors see evidence of rapid accumulations of wealth all around them.68

Many retailing frauds have taken advantage of a fourth cognitive rule of thumb, the “anchoring” heuristic, through which individuals fix a value to some asset, opportunity, or situation, and then use that value as a reference point for later assessments. Pervasive reliance on evaluative anchors helps to account for the psychological pull of sales and discounts, including offers of “free” bonuses; the special deal appears to require much less of consumers than does the anchored price.69 Anchoring similarly helps to explain the longstanding capacity of dodgy retailers to pull off fictitious pricing or “bait and switch” techniques. With the former practice, retailers construct an artificially high “normal” price, whether through claims about manufacturers’ list prices, misleading comparisons to prices at other retailers, or inflated presale “original prices.” So long as consumers lack awareness of prevailing prices, the fictitious values set a mental reference point, encouraging sales that would not have otherwise occurred.70

In the case of “bait and switch” tactics, the “bait” invokes economic reference points that already exist, such as customary prices, attracting attention because of the dramatic difference between those anchors and advertised specials. The “switch” seeks, in part, to exploit the psychological expectations created by the bait. Firms carrying out this bit of chicanery hope that consumers who have already invested time and effort, and who have convinced themselves that they have located special deals, will be loath to walk away empty- handed. This emotional investment makes them susceptible to the switch. There is always, of course, the opposite possibility: that consumers will be so angered by manipulative tactics that they leave in a huff. But bait and switch operators have calculated that any harm to their reputations would not stem the influx of more malleable shoppers.

Behavioral economists refer to this last example of mental anchoring as “loss aversion.” In experiments that ask subjects to make choices that involve assessments of risk, most people view economic losses as more painful and memorable than equivalent gains. As a result, consumers and investors often prove susceptible to how marketers frame opportunities and risks, demonstrating greater motivation to act if they see themselves as avoiding or preventing monetary harm rather than pursuing reward.71 In some contexts, such as real-estate development or securities investments, loss aversion would seem to complicate rather than assist fraudulent promoters’ efforts. Leeriness about losing what one has would hardly appear to encourage chasing after the latest road to riches. Yet even in the realm of speculative investment, savvy marketers have exhibited an intuitive grasp of psychology. They priced the stock of bogus companies or misrepresented home-sites cheaply, and allowed investors to purchase on the basis of margin or installments. Sometimes they drew suckers in with offers of “bonus shares” of some security as a means of inculcating a sense of ownership.72 All of these maneuvers lowered perceptions of cost. They also framed sales pitches around the avoidance of regret alongside the attainment of gain. A postbellum ad for town lots in some new Western settlement, or a prospectus for an early twentieth-century airline company, might plead with readers not to miss out on that rare chance to get in early, when the really huge gains were possible. As the early twentieth-century journalist Arthur H. Gleason recognized, this kind of pitch could sound like a revivalist sermon. The fraudulent promoter, Gleason argued, was

a professional trafficker in spasms. He must create an emotional crisis in a multitude of persons, and must repeat the same intensity of effect many hundreds of times. He deals in breathless excitement, the peremptory demand for an immediate decision from sinner or sucker, the Last Chance for Salvation or Big Profits, To-Night and Now the Time.73

To hold back, to keep the checkbook in one's breast pocket, was to court regret, or as one promoter framed the issue in 1917, to miss out on the “Foresight [that] makes Millionaires,” to identify oneself as a “groveling WISHER, always wishing for something BIG to turn up,” who, “when the chance does come never [has] the COURAGE to grasp that chance.”74

Even after a fraudulent investment failed, promoters dangled analogous rationales for throwing good money after bad. Such techniques, known as “reloading,” emerged during the post-World War I Texas oil boom. Promoters would explain to loyal followers that even though the oil company in which they held shares had entered bankruptcy, there was a fantastic opportunity to recoup losses by launching a new company that would buy the old one's assets on the cheap, as well as those of other insolvent oil firms. So long as investors provided additional capital, surefire profits remained only a gusher or two away. Thousands of defrauded investors responded to such appeals, which allowed them to put off psychological acceptance of losses, and to retain faith that their initial decisions would be vindicated.75

Throughout the nineteenth century and most of the twentieth, the Americans who adopted deceptive business practices obviously did not craft their misrepresentations with the research findings of behavioral economists in mind. Even toward the end of the twentieth century, few if any architects of deceptive marketing practices or unambiguous business fraud were conversant with the technical language of “mental accounting” and “cognitive heuristics.” But over the decades, outright swindlers and firms that practiced forms of deceit carried out their own investigations into consumer and investor psychology, testing which tactics and messages worked with a sufficient number of targets to make chicanery pay. As Bates Harrington put it in his 1878 book How ,Tis Done (which portrayed itself as an expose of the various con games visited upon the American countryside, but reads in many respects as a how-to guide for aspiring swindlers), the most adroit practitioners of economic deceit had reduced their endeavors to “a science. Every possible weakness of human nature, every loophole of ignorance, every assailable point where advantage may be gained, is studied with utmost care.”76 These informal marketing trials generated techniques that dovetailed with the economic psychology revealed by the more rigorous studies of the past two generations.

An episode from the history of Gilded Age financial speculation suggests that at least some Americans grasped the significance of cognitive guideposts such as the availability heuristic. After one fraudulent New York City brokerage had invested large sums to entice people from across the continent to speculate in its investment pools, it received numerous letters from individuals offering to serve as local agents. Many of these enterprising souls, like one Presbyterian minister from rural Pennsylvania, proposed that they would send in an increasing series of investments, with the brokerage sending out a series of even-larger checks in turn, demonstrating its capacity to live up to all the wondrous promises of its circulars. As the minister recapped his plan:

If I send you immediately $20, will you in 30 days send me your check for $40? Then if I send you as another operation $50, will you send me in 30 days $100? Next, if I send you as a third operation $100, will you send me in the end of thirty days, $200? If you will do this, I can have sufficient grounds to go upon, in my efforts to arouse some of my rich farmers who would not listen unless the evidence perfectly satisfactory and sure while they were yet ignorant of the method and details.77

This correspondence leaves unclear whether the minister intended to shear his parishioners, or rather hoped only to fleece the fleecers with a bit of their own technique. Either way, the proposition speaks to a keen appreciation of how bait dividends could inspire trust.

****

The affective dimensions of economic life changed enormously as Americans moved from farm to city to suburb, uprooted the institution of slavery, helped to fashion and learned to cope with large-scale corporations and unions, and encountered the technologies that spilled out of industrial research facilities, the increasingly sophisticated campaigns cooked up by advertising agencies, and the ever-greater abstractions of financial markets. As the United States evolved from a nineteenth-century society predicated on production to a twentieth-century society structured around consumption, to take just one far- reaching process, the emotional texture of Americans’ daily economic endeavors underwent huge transformations.78

The most captivating purveyors of business fraud have always remained attuned to these shifts, recognizing that deceptive marketing rests on plausible storytelling. Credible mimicry, charismatic personalization, and persuasive deflection all presume a deft grasp of social context, a capacity to tap into personal aspirations and set people at ease. One cannot pull off such masquerades without careful updating so that sales pitches evoke the lived experiences and emotional realities of targeted consumers and investors. The character of Robert A. Lee, for example, would have brought little demand for oil shares in the 1850s or the 1970s; amid the early twentieth-century flowering of Lost Cause ideology and entrenchment of segregationist white supremacy, this figure struck thousands of white Southerners as the sort of regional capitalist to whom they should deliver modest investments.79 The inventiveness and social adeptness among the perpetrators of business fraud has left its mark on American language. As they applied longstanding modes of deception to new economic and social situations, they fashioned slang to describe their practices. Each generation has produced an argot of fraud, a wealth of evocative terms that convey prevailing practices of imposition and intentional misrepresentation.

For all of the narrative specificity that marked business frauds as characteristic of specific times, and often specific demographic and geographic communities, the psychological structures of misdirection did not shift much. These consistent strategies point to cognitive vulnerabilities that endured underneath shifting sensibilities, reconstructed economic lives, and the always-fresh storytelling that underwrote the most effective fraudulent schemes. The extent to which American policymakers recognized these cognitive vulnerabilities, however, did not remain constant. Nor did prevailing judgments about how much policymakers should be concerned about business fraud, or ideas about how the government and other institutions should try to constrain it. In the early nineteenth century, which the rest of this book takes as its point of departure, American law contained numerous formal restrictions on deceitful economic behavior, which were rooted in centuries-old Anglo-American legal precepts. It also contained some specialized regulatory institutions charged with the responsibility of safeguarding reputations for commercial truthfulness. But on the whole, and for the individuals who possessed the full rights of democratic citizenship, the antebellum legal system expected people to look sharp.