Comparing interest rates

Despite money market instruments having maturities of less than one year (mostly), it can be seen from the FT table in Table 11.1 that they can have remarkably different interest rates depending on the length of time to maturity.

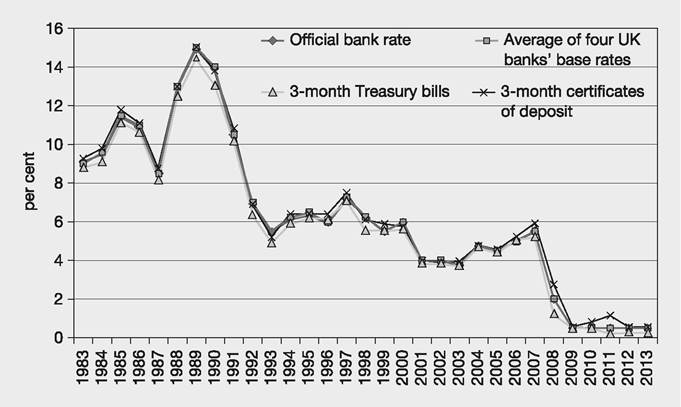

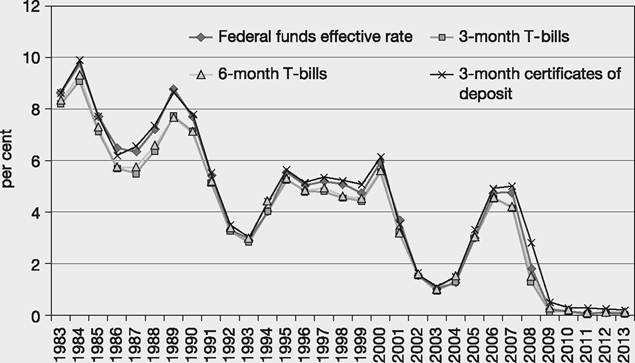

For example, on 12 September 2014 a sterling interbank loan for one month cost 0.50438% (annualised) whereas a loan of similar default risk, but lasting for one year, cost more than double that, at 1.04744% for the year. From Table 11.2 we can also see that repo rates can change significantly over time, for example the European Central Bank targeted overnight repo rates at 0.75% in early 2013, which was reduced to 0.5% in May 2013 and fell to a tenth of that level (0.05%) in September 2014.Figures 11.3 and 11.4 show comparative interest rates from the UK and the US over a 30-year period. A number of observations can be made about the interest rate on different money market instruments:

• Generally, investors require extra return for longer lending periods because of the extra risk involved, so overnight rates will normally be less than rates on longer-term instruments (although this is not always the case). Notice in Figure 11.4 US six-month T-bill rates are slightly higher than those for three-month T-bill lending.

• The creditworthiness of the borrowing institution has a strong influence on the rate of interest charged. The rate offered by reputable national

Figure 11.3 UK average interest rates 1983-2013, % annualised rate

Source: Data from www.bankofengland.co.uk

governments will usually be lower than the rate offered by a corporation wishing to raise cash by issuing commercial paper, or by a bank issuing certificates of deposit (see the higher rates on three-month CDs than on three-month Treasuries in both Figures 11.3 and 11.4).

However, there are some governments that are required by the financial markets to pay higher interest rates than many corporates - e.g. Greece, Portugal and Ireland in 2011 paid more than many banks in the years following the financial crisis.• When expectations about future inflation rise, interest rates rise accordingly, which leads to a decrease in the market price of money market instruments. Conversely, when inflation expectations are lowered, interest rates fall and the market price of the instruments rises. Thus we see that interest rates across the board tend to rise and fall together over time. The high rates of interest offered in the 1980s largely reflect the high inflation of the time.

• Supply and demand - for example, if banks need to borrow large sums of money quickly, they will sell more shorter-term instruments. This will have the effect of increasing market supply of these instruments and therefore pushing down their price, which in turn will increase the rate of interest, the yield to maturity.

Figure 11.4 US average interest rates 1983-2013, % annualised rate

Source: Data from www.federalreserve.gov

• Money market interest rates with similar terms to maturity stay close together and move up or down with quite a high degree of correlation over time. These rates are all low risk and all short term, thus there is a reasonable amount of substitutability between them for potential lenders. So if interest rates in, say, the CD market fell abnormally below that in, say, the commercial paper market, those banks needing to attract deposits might have difficulty doing so because potential lenders will put more money in the CP market. The banks will have to raise CD interest rates to attract deposits while the commercial paper borrowers will find they can lower rates - thus some degree of convergence takes place.

• Short-term interest rates can be lowered by central banks intervening in the markets when they judge that the economy is in need of a boost. You can see this sort of action in the figures in the years after the shock of the dot.com bust at the turn of the millennium and following the financial crisis of 2007-2008.