Confronting Deflation and the Asian Financial Crisis in the Late 1990s

In contrast to the short-lived monetary tightening that helped reverse the 1988-1989 inflation surge, the contractionary policy initiated to combat the later 1993-1994 episode was followed by an extended downtrend in money supply growth.

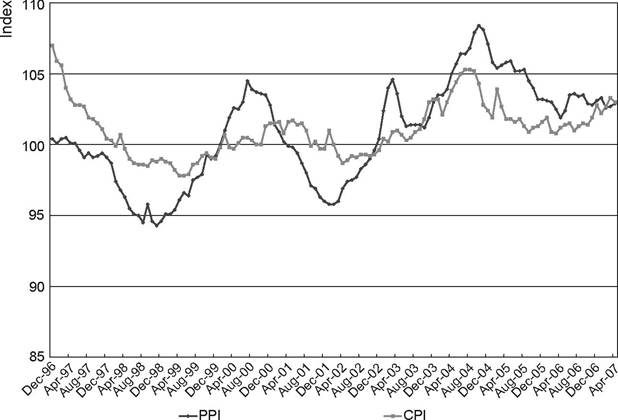

M2 growth actually declined continuously from 42.8% in 1993 to 12.3% in 2000. 1998 was the first full year of deflation. Meanwhile, output growth appeared to flatten out after 1994 and China’s sharp monetary tightening was also accompanied by a sizeable stock market decline in that same year. The cumulative overall consumer price deflation of approximately 10% between 1998 and 2002 occurred even as the price of services rose by more than 50% (Zheng, 2002). On the other hand, the rate of decline of commodity prices and production materials outstripped the relatively mild descent of consumer prices - falling by average rates close to 2% and 4%, respectively, in the first half of 2002 even while consumer prices declined by an average of less than 1% (Yuan, 2002). The considerably sharper decline in producer prices, both in 1998-1999 and 2001-2002 is evident in Figure 3.1, which compares the growth rates of consumer and producer prices over the 1997-2007 period.The continued price declines after the initial monetary tightening in 1994-1995 may have been exacerbated by the banking sector problems discussed in Chapter 7 - with bank reluctance to lend reflected in an excess of savings over lending of approximately RMB 3.65 billion by 2002 (Zhu, 2002). Consumer spending also lagged behind income, consistent with the standard tendency under deflation for consumers to put off purchases of nonessential goods that they expect to be able to buy at still cheaper prices

Figure 3.1. Annualized Growth Rates of China's Producer and Consumer Prices, 19972007.

Note: PPI denotes Producer Price Index and CPI denotes Consumer Price Index. Source: Great China Database.in the future (cf. Burdekin and Siklos, 2004, chapter 1). In China’s case, concerns about the future direction of the economy also helped explain rising savings rates even in the face of successive interest rate cuts (Zhu, 2002).

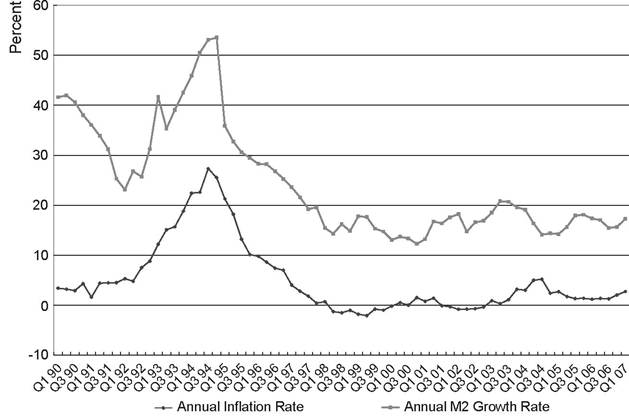

The fact that deflation, like inflation, is ultimately a monetary phenomenon seemed to be recognized by Chinese policymakers - with the People’s Bank of China raising its money growth targets to combat deflation and eventually restoring positive inflation rates in 2003. The close relationship between inflation and M2 money growth since 1990 is itself particularly striking in the Chinese case. In Figure 3.2, the monetary tightening aimed at combatting the 1993-1994 inflation spike is seen to be accompanied by declining inflation rates and, eventually, outright deflation. However, holding the renminbi exchange rate fixed against the US dollar, in spite of the depreciation pressure associated with the Asian financial crisis (Chapter 1), effectively handcuffed monetary policy at this time. In an indication of how severe an impact the crisis had on the Chinese economy, export growth dropped precipitously from 21% in 1997 to just 0.5% in 1998 (Lin, Cai, and Li, 2003, p. 274). At the same time, bank lending was being further curtailed by the need to reduce bad debts that were still conservatively estimated at

Figure 3.2. China's Inflation Rate vs. M2 Growth Rate, Quarterly Data, 1990Q1 to 2007Q1. Note: Inflation is measured by the year over year log difference in the Consumer Price Index. Source: Great China Database.

more than one-quarter of China’s GDP - even after the removal of RMB 10 trillion in nonperforming loans transferred to the asset management companies (Chapter 7). This left expansionary fiscal policy to carry most of the burden in combatting the initial outbreak of deflation in China.

In addition, in contrast to the policy reversals seen in Japan, for example, China’s fiscal policy remained in a consistently expansionary mode even after the conclusion of the Asian financial crisis.Deflation also emerged in Hong Kong, which, despite its return to Chinese rule in 1997, is treated as a separate economic entity.[50] Hong Kong consumer prices fell by an overall 12% between September 1998 and January 2002 (Schellekens, 2005, p. 244). In persevering with a fixed exchange rate policy during the Asian financial crisis, Hong Kong faced speculative attacks on the Hong Kong dollar and was forced into tight monetary policy that took a severe toll on the real economy. Hong Kong endured a 5.1% contraction in real GDP in 1998, for example (see Jao, 2001). Real exchange rate appreciation hurt Hong Kong’s economy, just as it strained mainland China’s, at a time when almost all other Asian currencies were undergoing large depreciation. Schellekens (2005) emphasizes that the parallel developments in mainland China and Hong Kong reflected their exposure to the same shocks and maintenance of similar fixed exchange rate regimes, rather than any mechanical price convergence effect.[51]

Hong Kong’s deflation was worsened by the negative wealth effects of falling property and stock prices that reduced the collateral available for new loans, just as had been the case in Japan following the bursting of that nation’s stock and land price bubble at the beginning of the 1990s (cf. Bur- dekin and Siklos, 2004). By comparison, the negative effects of China’s own prior 1994 stock market decline were limited by the much lesser importance of mainland China’s stock exchanges relative to the overall economy at that time.[52] The Hong Kong Monetary Authority itself resorted to direct stock purchases in 1998 as part of their attempt to ward off speculation against the Hong Kong dollar that was being spearheaded by short selling of Hong Kong stocks by a group of prominent hedge funds (see Krugman, 1999; Jao, 2001).

This intervention did help Hong Kong maintain its currency peg but may have been rather a pyrrhic victory. Jao (2001, p. 205) concludes that, although the policy was “quite successful in protecting the integrity of the currency and the banking sector, a heavy price was paid, in terms of the worst recession in 40 years.”Expansionary policy to combat deflation in mainland China was not only fueled by the pressures of the Asian financial crisis but also the need to address the problems with the state enterprises sector and recapitalize the large state-owned banks that had accumulated vast bad debts from these same loss-making state-owned enterprises. After the 1997 15th Party Congress, for the first time, provided for the sale (or bankruptcy) of many of China’s state enterprises, the authorities targeted 2,000 to 3,000 enterprises for bankruptcy, merger, or acquisition in 1998 - a year when 49% of large- and medium-sized state enterprises suffered losses (World Bank, 1999, p. 30). The layoffs associated with these moves certainly led to some worker unrest, however, and Kathy Chen (1997, p. A16) draws attention to the 50% increase in labor protests in 1997.[53] InJune 1998, JiangZemin gave a speech urging “caution in the sell-off of small state-owned companies, which were perceived as disturbing the orderly redeployment of laid-off state workers and harming workers’ interests” (World Bank, 1999, p. 31).19

The financial weakness of the state enterprises prior to the 1997 initiative was reflected in an officially reported ratio of liabilities to assets that reached 85% in 1995. Lardy (1998, pp. 39-43) argues that this ratio was actually considerably understated and equivalent to a better than 500% debt-to-equity ratio. The upshot of this is that, as state-owned enterprises borrowed up to the hilt, the state banks that lent them the money were faced with vast levels of nonrecoverable loans. The financial burden on the economy arising from the state-owned enterprises was characterized by Dorn (1998, p. 133) in terms of a “terminal disease... eating up China’s scarce capital.” As discussed in more detail in Chapter 7, the Chinese government issued $32.5 billion in bonds in 1998 to help recapitalize the four state-owned banks and in 1999 the government established four financial asset management companies to purchase and manage bad loans from these banks.