EXTENDING CREDIT ENHANCEMENTS IN MARKETPLACE LENDING

Just as in the established credit sector, credit enhancements in marketplace lending take two principal forms: securitization via simple to advanced credit derivatives, and use of collaterals.

Securitizing credit portfolios originating from marketplace lending platforms have some additional challenges. We know that many counterparties who are applying for credit

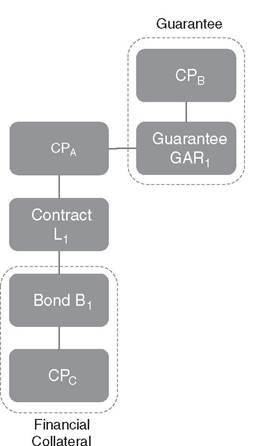

FIGURE 10.6 Exampleof

applying multiple credit enhancements in a credit exposure

using marketplace lending systems may be those with limited or no other access to credit from established financial institutions. This implies that the expected default rate is higher. In addition, as marketplace lending is most attractive when markets are volatile, some additional market and behavior risks will have an additional impact on counterparty risk.

The above gives rise to products for securitizing bundles of loans provided by marketplace lending; e.g. against counterparty defaults and credit losses, which can then be sliced into “tranches” and sold to the market. By securitizing their portfolios, marketplace lenders can allow creditors access to funding for loans at lower rates. Banks, including Citigroup, Capital One, Bank of Montreal, Barclays and Deutsche Bank, are exploring how to finance or securitize such loans into large bundles that can then be sold to big investors.9 Even though the loan volumes that marketplace lending platforms originate are still small, they nonetheless feed into the relatively unregulated and opaque shadow banking sector. There is a fear that credit institutions outside of the formal financial sector may end up repeating the mistakes that helped fuel the subprime mortgage crisis.

On the other hand, financial collateral and other types of guaranties have not been used so far.

In other words, credit exposures are fully ««collateralized. This means that lenders are exposed to the full amount of the principal provided to borrowers, which equates to expected credit losses. This also implies a higher default probability, especially under stress conditions, as the willingness and priority for fulfilling the agreed-upon obligations is expected to be less than in instances where collateral is in place. In simple terms, when obligors post a valuable asset as collateral, they make a strong effort to keep the promise, even in times of stress. In any event, guarantors prefer not to have to cover credit losses and are therefore enforcing obligors to fulfil their obligations. For this reason, when valuable collateral is in the mix, borrowers have skin in the game and loans perform better across the board.Alternative ways to attach credit enhancements in marketplace lending credit exposures could be also applied. Let's look at some of them in more detail in the following paragraphs. Before we do this, let's agree on the fact that virtually anything could in theory serve as collateral for a loan as long as both parties agree that it is valuable. For collateral to be valuable—which is a prerequisite for it to serve effectively as a credit enhancement—the borrower needs to have an attachment to the asset he pledges as a security for a loan. Of course, the most obvious choice here is real estate. Borrowers will be in real pain when the bank forecloses on their house, so they will in most instances go the extra mile to avoid repossession. Another prerequisite for collateral is a recognized and indisputable value. If an asset has no value whatsoever, it will yield no additional cash flows when it should compensate for cash flows that a default has cancelled out. When the value is in the eye of the beholder, similar issues arise. For example, someone may see enormous value in his collection of vinyl records, but objectively assessing and transferring this value to a new owner will be a challenge.

A situation may exist where both the lender and the borrower agree to accept collateral that is hard to value and enter into a contract. For the sake of argument, we will only focus on situations where the value of collateral is relatively straightforward. Whenever there is an official record, such as in a real estate registry, or a contract that outlines fees and services, collateral will be easier to value. Also important is that existing analytics apply to new kinds of collateral. With the examples we discuss here, this would be possible. We should classify collateral into asset-based and counterparty-based, and then feed them into the same analytics that already exist with more conventional kinds of collateral.With this in mind, let's think about other situations where potential collateral has both characteristics—attachment and value. Examples we will discuss here are real estate, phone contracts, membership points, life insurance, and personal guarantors.

10.5.1 Real estate titles

Just as in established mortgage finance, real estate is a powerful asset-based credit enhancement that can provide security for lenders against default. We won't go into the mechanics of this here, also because real estate is already widely accepted as credit enhancement in deals. Still, for marketplace lenders to accept real estate as collateral, they will have to change their business model significantly. At this point, most platforms have purely digital processing of cash flows with a limited capacity for servicing physical collateral. Their structure for contracts is relatively simple and standardized. When real estate enters the picture, this has to change. Marketplace lenders have to add a physical component to their operations, where they have to manage recoveries more closely. Accepting real estate is therefore a low priority for most platforms, even for the big ones. Nevertheless, in small and closely regulated markets, accepting real estate comes with fewer obstacles.

Their high valuations aside, the real estate markets in, for example, Hong Kong, Singapore, and Switzerland are closely regulated and relatively transparent. Marketplace lenders in these markets may have a better opportunity to accept real estate titles as physical collateral than those in fragmented and opaque markets.10.5.2 Phone contracts as stores of value

Other situations where people have stores of value or commitments sitting in accounts unused are more common than we think. A mobile phone, for instance, may have a certain number of minutes of airtime or bandwidth available either in a long-term contract or in prepaid plan. These minutes can serve as collateral and asset-based credit enhancement for any loans a counterparty may take out. If this seems ridiculous, just think about it from a different angle: Apple lists the price of the iPhone 6 between $199 and $399 with a two-year contract at the time of this writing. The device is quite useless unless you connect it to a mobile network and data, and the cost of doing so is far less transparent. In the U.S., depending on the operator, two years of iPhone use costs between $470 and $1,120.10 Any smart phone contract has therefore a potential value of up to $900. Imagine now that a phone company made loans from marketplace lending available to their subscribers. As a requirement for borrowers, it could demand they pre-pay their accounts partially, and it could take the device as physical collateral. The company could then relatively easily net the value of subscribers’ contracts with their loans. If a borrower is late, the phone company simply forfeits the prepaid amount to the borrower and turns off the phone service. When a loan defaults, the company could repossess the phone. We can also imagine a situation where borrowers and lenders connect on a platform operated by a third party, independent from the phone company. For this to work, the phone company should recognize that subscribers may want to use their accounts as loan collateral, so it could offer a service to process collateral assignment and transfers of contracts to new owners.

Does this seem far-fetched to you? Perhaps in the developed world, but in emerging markets, there exists a vibrant market for pre-owned smart phones with stalls selling them at most shopping malls. Mobile payments made on cell phones and smart phones have already taken off. Large players like Apple and Google have entered the mobile payments market, but functional services have been in operation for many years already. For example, take M-Pesa, a mobile-phone based money transfer service launched by Vodafone in 2007 in Kenya and Tanzania. Now also available in Afghanistan, South Africa, India, and Eastern Europe, M-Pesa allows users with a national ID card to deposit, withdraw, and transfer money easily with a mobile device.11 Mobile payments extend financial services to the so-called “unbanked,” up to 50 per cent of the world’s adult population.12 These services could expand their offering from payment to lending and, because they have collateral built into their existing business model, may actually be ideal candidates to do so. Of course, it is a stretch to use $10 or even $100 in collateral for a loan that is many times that amount. But for small loans that cover single small expenses, it may suffice.

We realize that thinking of collateral in this way might be a bit of a stretch. Most people would hardly recognize a cell phone contract as collateral, and a $900 value seems paltry compared to the size of most loans. We won’t even go into the headache and switching cost that is currently in place with most phone companies. However, to imagine new ways of extending credit, let’s put these doubts aside for a minute and explore some ideas without pretending we have all the answers. Not all ideas will be brilliant, but at least they will form a basis for the discussion in the third part of this book where we will explore solutions for the hybrid financial sector. Of course, there needs to be an additional infrastructure in place for this new kind of collateral to serve as a feasible and credible credit enhancement.

For example, phone companies need to have a process for “liquidating” contracts in case of a default. We will skip this discussion in this book. Regardless, we should recognize that the ancillary infrastructure also yields business opportunities in the hybrid financial sector. Just as mortgages need a servicer who deals with the physical property, new assets pledged as collateral will only work when the market has processes in place to liquidate or transfer them.10.5.3 Loyaltypoints

Just as in the example with the phone contract, loyalty points could serve as some kind of asset-based credit enhancement. Most people collect membership points of some kind, be it airline miles, points from paying with a credit card, or loyalty points from a grocery chain. The evolution of such points is a simple form of analytics to see the performance of a counterparty. When someone has many points, we can get a picture of that person quite easily. Just imagine someone who has amassed 1 million air miles: you immediately have a picture of that person as a cool frequent flyer who zips in and out of airport lounges and flies at least business class, or first on upgrades. Naturally, this person must have a high-paying job, perhaps as an executive or successful entrepreneur. One glance at the point score triggers all these associations. This is much more efficient than reading between the lines of a person's salary history or job description. There already exist several marketplaces for loyalty points. Several companies specialize in loyalty commerce transactions with the goal of enhancing the monetization of loyalty currencies, including airlines and hotel chains.13

When a lender and a borrower connect through a marketplace lending platform, loyalty points could serve as collateral. They could easily transfer to the lender in case of delinquency or default. Of course, a borrower would have to find a lender to whom such collateral is valuable, but isn't this what marketplace lending is all about? When lenders and borrowers agree that a certain number of membership points fulfils the requirements for collateral in a default event, they have a deal. Again, servicing and facilitating the transfer of points is another story that still needs to be streamlined.

10.5.4 Life insurance

Most people have insurance of some kind, with life insurance policies being the most valuable. Life insurance already serves as collateral in credit agreements, and some businesses will accept life insurance as collateral. Processes to assign the policy to another party are already in place. A collateral assignment of a life insurance policy appoints a lender as the beneficiary of an insurance benefit. If the borrower fails to pay back a loan, the lender can cash in the life insurance policy and recover the outstanding loan balance. If a borrower passes away before repaying the loan in full, the lender receives the amount owed out of the death benefit. The remaining balance then goes to other listed beneficiaries. Such an arrangement effectively insures lenders against credit risk.

Lenders can accept any kind of life insurance policy for asset-based credit enhancement as long as the insurance company allows assignment of the policy. A permanent life insurance policy with a cash value is the most useful credit enhancement because it allows the lender access to cash immediately without having to wait for the policy to pay off. For this to work, the owner of the policy should have restricted access to the cash in the insurance policy to protect the collateral as long as the loan is current. As soon as the loan has been repaid, any restrictions or assignment to a third party are removed and the lender has no more claims on the insurance payouts. Not all insurance companies like to deal with collateral assignment and they are often slow to update changes of beneficiaries. Still, life insurance would be an ideal asset that should enhance the quality of loans significantly.

10.5.5 Guarantor systems

The ability and willingness to pay back a loan can drastically improve when a third party guarantees to step in to cover losses or exert pressure on delinquent borrowers. In small villages, for example, people lend to each other more efficiently than to strangers. When all people know each other well and do business with each other on a regular basis, a loan default will have repercussions that borrowers need to avoid at all costs to save their social standing in the community. Many societies use guarantor systems, most prominently the Japanese. When renting a flat in Japan, the leasee, the landlord, the real estate agent, and a personal guarantor are necessary to complete the contract. Without the personal guarantor in the deal, no transaction takes place. The leasee and the guarantor are jointly responsible for liabilities to the landlord that may arise. If a leasee fails to pay the rent, the landlord can legally seek payment for rent from the guarantor. This arrangement goes still farther: if the lease causes any trouble with neighbors, the guarantor steps in as an intermediator. Traditionally, family ties and other strong relationships served as guarantors. However, being on the hook for the behavior of a third party can quickly become a headache for a guarantor and, naturally, an industry has formed to turn this pain into profit. Guarantor services for rental contracts are available for a fee; typically one month of rent and an annual fee of 10,000 yen (about US$80 at the time of this writing).14 It is easy to see how this arrangement could extend to providing personal guarantees for borrowers as well.

In corporate credit, guarantees are common. Typically, a related entity such as a parent company guarantees for loans of a subsidiary. When measuring net exposure, contracts with a guarantee become much stronger with very low default rates. The guarantor pushes a borrower to perform. In addition to asset-based and counterparty-based credit enhancement, guarantor systems use pressure on the counterparty to get them to comply with loan agreements.

Even though banks can use counterparty-based credit enhancements to shift the net exposure entirely to another party at no cost to them, guarantor systems come with a cost for borrowers. When formal ties or family ties exist, using guarantor systems may look like asking for a favor, but the economic cost can be significant. Unless a guarantor has an incentive to provide a guarantee, he will rarely shoulder the risk of having to step up to the plate when there is a default. A system that relies on guarantors to altruistically help their fellow community members will ultimately fail. Unless a deal fairly compensates all parties involved, the system will eventually unravel. When a third-party provides trust to a borrower, the system can become fuzzy very quickly. Guarantor systems therefore have more in common with insurance than actual trust. When insurance is not readily available, asset-based credit enhancements are therefore stronger than those relying on a counterparty.

10.6 Concludingremarks

Everybody agrees that credit enhancements are a wonderful tool to mitigate risk and reduce net credit exposure. Let's summarize what they do and why they are important. In regard to analytics, the asset-based credit enhancements (i.e., financial collaterals and close out netting), are driven by both market and credit risk factors. This implies that market fluctuations and counterparty risk can directly influence the credit exposures and credit losses. On the other hand, counterparty analysis is applied to guarantors and credit derivatives. Even though credit enhancements have great impact in exposure analysis, some important issues must be attended to, including the probability of double default, the identification and measurement of specific and general wrong way risk, and the management of maturity mismatch and time of default event. Even though the great majority of credit portfolios issued by the credit institutions are attached to credit enhancements, in the marketplace lending model they are missing. Some alternative approaches for using financial collaterals and guarantor systems are proposed in this chapter.

After all, credit enhancements are vital when mitigating credit risk exposure, minimizing and absorbing the credit losses and aiming to keep the financial system and markets steady. Therefore, they consume a great part of management and financial analysis. Both credit financial institutions and regulators ensure that most of the credit exposures are linked, fully or partially, with credit enhancements. The construction, selection and management of all types of credit enhancements play an essential role in counterparty credit risk management.

NOTES

1. For instance the U.S. and European CDS Indices define credit events differently: for the U.S. indices, only bankruptcy and failure to pay trigger a default; restructuring is not deemed a credit event, even though most underlying single-name CDS contracts treat restructuring as a credit event; European indices trade with the same credit events as the underlying CDS contracts, including modified restructuring, bankruptcy, and failure to pay.

2. Book value accounting ignores these.

3. For instance, market leader Lending Club recommends they diversify across at least 100 contracts.

4. E.g., credit default swaps.

5. See BIS paper BCBS189 §101/58.

6. E.g., Interest Rate Contracts, cross-currency swap, FX Contracts, Commodity SWAP, etc.

7. Adjustment factors are also proposed by regulatory bodies.

8. Referred to also as “grapes.”

9. Eaglewood Capital, a New York-based hedge fund manager, completed a $53 million securitization of Lending Club loans in October 2013 in a first-of-its-kind transaction. A large global reinsurance company bought all the senior tranches.

10. Bott, Ed (2014) “How much does an iPhone 6 really cost? (Hint: It's way more than $199)” (ZDNet, 18 September 2014), http://www.zdnet.com/article/how-much-does-an-iphone-6-really-cost-hint- its-way-more-than-199/.

11. M-Pesa (2014a) home page, https://www.mpesa.in, accessed 12 November 2014.

12. Demirguc-Kunt, Asli; Klapper, Leora (2012) “Measuring Financial Inclusion” (World Bank, Policy Research Working Paper 6025, April 2012), http://elibrary.worldbank.org/doi/pdf/10.1596/1813- 9450-6025.

13. Points.com (2015a), website, https://www.points.com/.

14. University of Tokyo (2015a) Japanese Culture specific Guarantor System, http://dir.u- tokyo.ac.jp/en/topics/0804housing/1-06.html.