FRAMEWORKS TO ANALYZE THE IMPACT OF INNOVATION

To examine how innovation spreads in the market and how companies should react to innovation by competitors, we find the following three frameworks the most helpful: Rogers' concept of the Diffusion of Innovations, Gartner's Hype Cycle, and Big Bang Disruption put forward by Downes and Nunes.

Let's briefly examine what each of these ideas is about and then explore their usefulness for marketplace lending and the hybrid financial sector. As a guide to these frameworks, Figure 15.1 outlines the different relevant aspects in analyzing innovations that are common to all these models. This includes the timing of market entry, types of customers, adoption rates, diffusion and market share, hype and disillusionment, the reactions of competitors, maturity and staying relevant.15.2.1 Thediffusionofinnovations

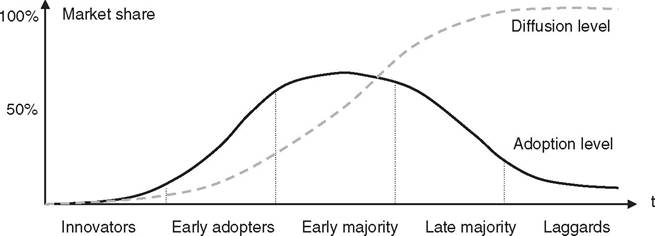

In 1962, author Everett Rogers formulated the theory of the diffusion of innovations.1 Figure 15.2 shows the well-known graph that most companies and entrepreneurs have adopted as tried and true.

FIGURE 15.1 Analyzing the impact of innovation

FIGURE 15.2 Diffusion of innovations curve

Adaptedfrom: Rogers, Everett

According to the diffusion of innovations theory, companies that introduce new technology slowly build their market share over time. Innovators and early adopters are among their first customers who beta-test the unfinished technology and iron out its bugs and shortcomings. When the technology has spread wider, customers in the early majority embrace it, followed by the late majority. Finally, at the point where the technology is nearly ubiquitous, laggards jump on board as well. This approach gives companies some breathing room to roll out and improve new technology.

When they see adoption picking up in the market, they know that they are on the path to greater market penetration and can scale operations accordingly. The theory is also useful when segmenting customers.15.2.2 The hype cycle

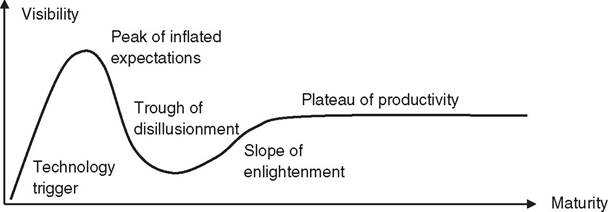

Gartner's hype cycle, another well-known methodology, describes how technology matures in the market.2 This concept is a staple in technology marketing. Despite several shortcomings, the model is relevant in the context of FinTech and marketplace lending as one way to forecast the adoption by the market, and eventually the market share of a technology. When venture capital is flowing into lending platforms at unprecedented rates, the sector might be in the run up to the peak of inflated expectations. Figure 15.3 shows the hype cycle.

The hype cycle starts with a technology trigger, a potential technology breakthrough that makes headlines in the market. At this stage, the product is often still buggy and unproven.

FIGURE 15.3 Hypecycle

Adapted from: Gartner

In the following peak of inflated expectations, early success stories mix with false alarms and accounts of fatal flaws in the new technology. When it fails to deliver, interest in the technology decreases, and it descends into the trough of disillusionment. Some early supporters fold their operations, others help improve the technology. If they succeed, useful applications of the new technology become more obvious on the slope of enlightenment, and ancillary products emerge. More and more investors fund pilot projects and, finally, when the technology reaches the plateau of productivity, the mainstream—the late majority and laggards—adopt it. At this point, the technology has established a level of visibility that remains fixed.

Even though they are well-known and make sense intellectually, the theories of the diffusion of innovation and the hype cycle have one flaw: they fail to take into account exponential growth.

Some digital businesses take a while to take off, but once they have reached critical mass, a large number of customers switch to the new service without ever reverting back to the competition. The pace of gradual customer adoption and slow market penetration hardly accounts for impulse decisions. A good example is the emergence of social networks. One of the earlier social networks, Myspace, attracted 75.9 million monthly unique visitors in the United States at its peak in December 2008. NewsCorp had bought Myspace for $580 a few years earlier3 but, in 2011, NewsCorp sold the social network again for $35 million. It had roughly 30 million monthly unique visitors then.4 In a short period of time, Myspace had ceded most of the market share to Facebook, which currently boasts more than double the monthly users of Myspace at its peak and a valuation of over $200 billion.5,6 The transition looks like it unfolded slowly, but when customers feel they better abandon a sinking ship in favor of the next trend, firms will rarely know what hit them until it is too late.Another shortcoming is the notion of the plateau of productivity in the hype cycle. This phase is hardly a plateau but a slippery slope in the digital world. If market leaders rely on these frameworks to assess their prospects, they will be at a disadvantage when combatting aggressive new entrants.

15.2.3 Big Bang Disruption

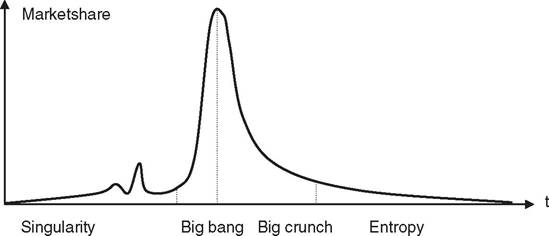

Instead of the slow diffusion of innovation and the gradual slope of enlightenment, we need a better way to chart disruption. Frameworks that accurately describe gradual—nonexponential—adoption of technology have trouble describing innovations that follow the law of accelerating returns. For those innovations, we need a more complex framework: enter Big Bang Disruption.1 The approach greatly speeds up Rogers' diffusion of innovations curve. When competitors disrupt a market with innovative technology, established companies may lack the time to leisurely tweak their business models.

Before they know what happened, their market share has eroded and they find themselves without a working business model in a new reality. Figure 15.4 shows what Big Bang Disruption looks like.A big bang that unseats incumbents seldom comes without warning signs. Disruptors, who often come from outside the sector, make their entry into the market as failed experiments in the first stage of the singularity. Market leaders may discount these occurrences as random, but they often foreshadow trouble for established business models. Today's experiments may not be scalable, but an unprecedented disruption could lurk behind them all. As those disruptive experiments unfold, entrepreneurs may happen upon a winning formula. In the ensuing big bang, customers across all market segments—from innovators to laggards—quickly embrace the technology and abandon legacy products. Incumbents struggle to stay relevant. In the big

FIGURE 15.4 BigBangDisruption Adaptedfrom: Downes and Nunes

crunch, incumbents rapidly crumble. At the same time, the disruptors mature themselves. Their innovation is no longer disruptive but incremental and sustaining. Finally, entropy sets in: the disrupted incumbents who are struggling to stay relevant in the new ecosystems may or may not find uses for their remaining assets and their intellectual property. The next disruption is already on the horizon, and those who unseated the incumbents now find themselves at risk of disruption themselves.

Each of the three frameworks to chart innovation has its shortcomings. However, when FinTech entrepreneurs and those responsible for digital strategy in banks analyze their options, all three theories come in handy to frame the discussion about the way forward. When we talk about marketplace lending and the future of finance, we might still be in the early stages. The market share of marketplace lending platforms is but a small drop in the ocean of the entire credit sector. However, startups in the lending sector have managed to generate significant interest from the media and investors, and innovators and early adopters are already flocking to the sector. In recent years, we have seen some singularities, such as high valuations of marketplace lending platforms in the public markets or announcements for high profile collaborations between startups and established banks. The longevity of marketplace lending is still up for debate, but banks have had more than one wake-up call to get busy with a digital strategy of their own.

15.3