As we mentioned in Chapter 9, the status of a borrower and his contract is either “default” or “non-default.”

The latter includes three possible cases that relate to the credit rating of the counterparty. It may remain steady, or it can either upgrade or downgrade. Whenever a lender transacts with a borrower, the risk of default exists.

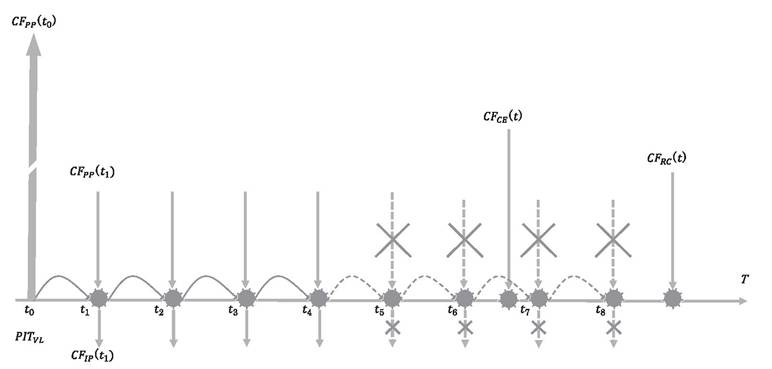

Changing the loan status to “default” or “downgrade” will most definitely cause credit losses. To compensate for this risk and any potential losses, we apply a spread over the risk-free rate in addition to credit enhancements.If a contract defaults, the contractual expected cash flows cancel out, and the value of the defaulted contract inevitably changes. However, credit enhancements as well as some expected recoveries generate new cash flows. Both credit enhancements and recoveries have the purpose of covering credit losses in full or in part. For instance, let's assume the case of a loan as illustrated in Figure 10.1 where the expected principal CFpp(t) and interest CFιp(f) cash flows cancel out after a default occurred at t5. Despite the default we expect new cash flows at a time t in the future because the credit enhancements CFce(t) and recoveries CFrc(t) start to be expected. We discussed recoveries in Chapter 8.

A non-default status indicates that no changes in expected cash flows will result from counterparty risks. However, an upgrade of the credit status of the counterparty will have a positive impact on the value of the contracts. On the other hand, a counterparty downgrade implies possible cancelation of the expected cash flows and credit losses, i.e., due to a higher default probability. In addition, it will negatively impact the value of the contracts. Any liquidation of such contracts will result in reduced expected trading cash flows. We could also expect a negative effect in the premiums of credit derivatives applied against a change in counterparty status.

In this chapter, we will go through the different types of credit enhancements named asset based and counterparty based. We examine what they are exactly and how they work going through the mechanics of credit enhancements. We will discuss why and how to allocate collateral and guarantees to different credit exposures, why asset-based credit enhancements could fluctuate, and how to measure such volatiles and what is the impact on credit exposures. We investigate the role of netting agreements and the challenges of employing credit derivatives. Then, we will explore some of the specific issues rising from the usage of credit enhancements including double default, specific and general wrong way risk, and maturity mismatch. Finally, we will propose some extending approaches for using credit enhancements in P2P lending models.

FIGURE 10.1 Cash flow cancellation and appearance after a default event

10.1