Repurchase agreements

Repurchase agreements (repos) and reverse repos are collateralised agreements used mainly by banks to borrow from or lend to each other with cash that is available for a short time (usually overnight or for a few days).

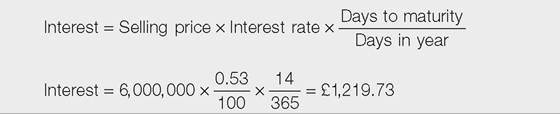

Repo rates are calculated for a variety of maturities.Example 14.6

Repurchase agreement

A high street bank has the need to borrow £6 million for 14 days. It agrees to sell a portfolio of its financial assets, in this case government bonds, to a lender for £6 million. An agreement is drawn up (a repo) by which the bank agrees to repurchase the portfolio (or an equivalent portfolio) 14 days later for £6,001,219.73. The extra amount of £1,219.73 represents the interest on £6 million over 14 days at an annual rate of 0.53%. Using an actual/365-day count convention, the calculation is:

Note that the agreement is to ‘sell' securities and thereby borrow on a particular date. The value date is when the transaction acquires value. This is not always the same as the settlement date - when the amounts are actually transferred, i.e. ‘settled' or ‘cleared' - because the value date may fall on a non-business day such as a weekend.

Example 14.7

Repo bond equivalent yield

A financial institution borrows £26 million through a repo for 14 days. The difference between the amounts in the first and second legs is £5,285.48, therefore the annual rate of interest (bey) is:

In some markets, e.g. the US, the repo yield or repo rate of interest is calculated based on a 360-day year:

Of course, this is not the bond equivalent yield, but merely the convention used in some places to work out yields and prices of repurchases, strangely enough. The repo rate is the one that will be most quoted in these markets, so you need to remember that this is not even close to the true annualised interest rate.

Example 14.8

Repo interest paid

A bank lends £45 million overnight at an annual bey rate of 0.42%. The actual amount of interest is:

Example 14.9

A repo buy-back amount

A company owning £20 million worth of Treasury bills wishes to raise cash on 28 February and enters into an agreement to sell the bills and buy them back in one week's time. The agreed buy-back price would be £20 million plus the accrued interest. The bond equivalent yield on 28 February for a one-week repo is 0.52167%:

This is not quite what happens in the markets because they impose ‘haircuts'.