THE RESPONSE OF BANKS TO ONLINE LENDING

Before we wrap up this overview of marketplace lending, it is important once more to put it into context with lending in the formal financial sector. Whenever the topic of online lending and marketplace lending in particular comes up, most bankers will contend that the sector is tiny compared to the total amount of credit to the private sector.

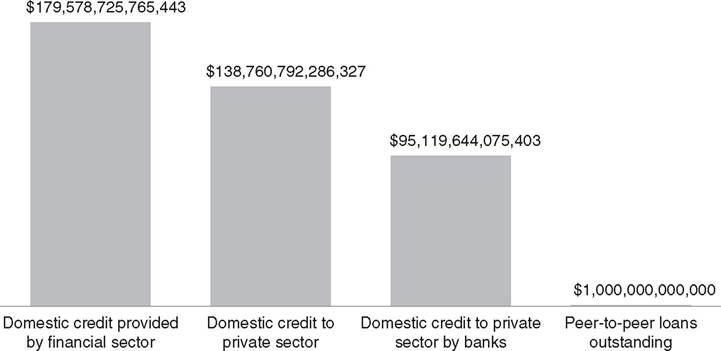

Figure 2.12 shows the proportion of credit by the financial sector to both private and public parties, private parties only, and lending to private parties by banks only in relation to marketplace loans outstanding, as predicted by author Charles Moldow for 2025.35 To extrapolate the amount of credit by banks in 2025, we have used nominal domestic credit provided by the financial sector, as reported by the World Bank,36 and extrapolated this number to 2025 with a constant growth rate of 3 percent, which lies below the current growth rate predicted by the IMF World Economic Outlook.37 Per definition by the World Bank, domestic credit provided by the aggregated global financial sector includes all gross credit to a variety of sectors, except credit to the central government, which is net. The financial sector includes monetary authorities and deposit money banks, finance and leasing companies, money lenders, insurance corporations, pension funds, and foreign exchange companies, where data is available.38It sounds impressive, but one trillion of marketplace loans outstanding in 2025 is small fry compared to the total amount of credit in the financial system—a mere 1 percent of bank lending to the private sector. However, this fails to take into account that marketplace lending as we know it today is still in its first generation. There may be innovations that evolve the sector rapidly, innovations we have no chance of predicting at the current time. A similar example of a disruptive trend that started small is the rise of cell phones.

Author Jon Agar found that in 1987, five years after launching the first mobile cell phones in Scandinavia, roughly 2 percent of the population in the region were subscribers. Truckers, engineers, andPrediction of global credit compared to peer-to-peer loans outstanding (2025)

other professionals on the go used these devices, but only few found application in private use.39 It took a lot of foresight to understand that these devices would proliferate like no other device before. The next generation of mobile phones—smartphones—are the latest outgrowth of a trend that started 20 years earlier with the first cell phone in the market. If banks are still on the sidelines when game-changing innovation takes place right under their nose, they may be up against a much bigger enemy than they can currently predict. They may be able to keep up for a while by simply buying up new ideas, but the knowledge gap between their in-house capabilities and the market will inevitably grow. This is dangerous and can be fatal: when misinformed incumbents make a desperate attempt to catch up with a market that they have missed, they often focus on technology that is precisely wrong. An example is Motorola’s debacle with Iridium, where a short-sighted bet with the wrong underlying assumptions cost investors billions of dollars.40 Dismissing a sector as too small and unimportant at the outset is hardly a good strategy in dealing with competition in the age of accelerating change.

Most importantly, the future of credit is unlikely to be an either/or proposition. Banks already have millions of small business customers and private customers. Without much effort, they could be important players in the emerging online lending market. In a sense, each new online lending platform tries to compete within a similar market segment by building its own financial network.

How much more effective would it be if they could simply plug into the existing network of banks? Proprietary information that banks have could be valuable for platforms, and there are exciting opportunities for the formal financial sector and newly emerging alternative lenders to collaborate. Banks could easily position themselves as part of the solution in shaping the future of credit jointly with digital customers and entrepreneurs. Instead, when it comes to reinventing lending, they are being part of the problem. We will investigate this claim further in Chapter 5, where we examine why innovation in lending takes place outside of the established financial sector.For the time being, banks have their own balance sheets to lend from and they hardly need to raise expensive capital from private parties in the current low-interest rate environment. However, financial services firms already make investments in potentially disruptive FinTech. Most likely, banks will hardly adapt the business model of marketplace lending by themselves in the near term, but they definitely want to be part of innovative startups when they take off. Banks have already acquired some promising FinTech startups when they fit into their operations. Mergers and acquisitions activity could rapidly pick up when FinTech business models mature. In marketplace lending, it is still unclear which companies and business models will be the game changers of the future. The reason that marketplace lending has emerged at this time in history is by no means a coincidence: the credit sector is ripe for innovation. In the next chapter, we look into the unique circumstances that have made the rise of online lending possible.