The start of modern banking

Imagine you are a wealthy Londoner in the 17 th century. You have a problem: much of your wealth is in metal coins and you need somewhere safe to keep these. You have heard of a group of merchants known as goldsmiths who have long experience, strong vaults, high reputation and the latest technology to keep valuables safe.

They've been dealing in gold for decades. You could strike up a deal with them whereby they looked after your gold and silver for a small fee.The goldsmith gives you a written receipt. This piece of paper states the value of the coins deposited. If you wanted to buy something in a shop you could take your piece of paper to your goldsmith to receive coins to spend. But what happened next led to the development of goldsmiths as banks. The shop keeper, as likely as not, would deposit your coins with a goldsmith for safekeeping, receiving a receipt in return. It did not take long for shopkeepers to realise that a receipt from a reputable goldsmith was worth taking from a customer rather than insisting on the usual merry-go-round of collecting coin and depositing it again. The shopkeeper could simply accept the receipt and collect the coins at a later date (or get them transferred to their account at the goldsmith). The paper receipts increasingly became accepted as a form of money.

These private depositories of coin got a real boost when the rival depository, the Royal Mint, on Tower Hill, was raided by Charles I at the start of the civil war. He decided to ‘borrow' the huge sum of £200,000. He later repaid, but the damage was done, trust was gone. The goldsmiths not only had higher reputations but paid interest.

Fractional-reserve banking

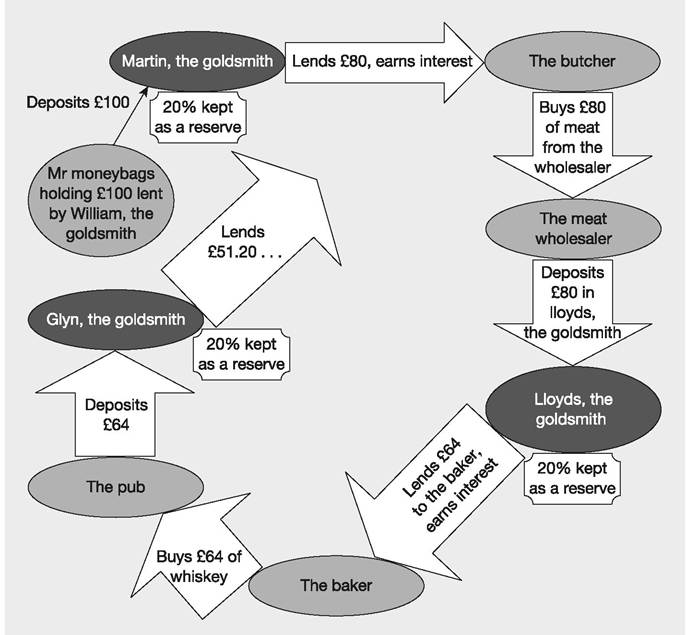

Goldsmiths noticed that most of the deposited coins were never taken out. On a typical day, or even a typical month, only a very small proportion of depositors turned up to demand their coins.

So, reasoned the bankers, if for every £100 deposited only around £20 would need to be kept in the vault to satisfy those who turned up at the bank, why not lend out the other £80 and gain some interest? Hence only a fraction of the money deposited is held in reserve: fractional-reserve banking.Money creation

Now we can move to another stage, we can actually create money. The borrowers of the money from goldsmiths were usually content to take a piece of paper - call it a bank note - instead of taking coins out of the bank. They could then use that as currency to buy things. The goldsmith could just create these pieces of paper off their own bat. Thus, a goldsmith-bank might have a total of, say, £1,000 deposited, but hand out £500 of the coin as loans and issue another £5,000 or £6,000 of new paper money to borrowers.

You can see the obvious danger here: depositors might all come at the same time to demand their money - they want £1,000 back when there is only £500 in the vault. Illiquidity! But what are the chances of a high proportion of depositors wanting cash back at the same time? Minuscule, thought the bankers, and so they carried on lending beyond their deposit base - and this is what bankers do today. They create money out of thin air (just so long as there is a deposit base on which to build) - see Figure 16.1. Initially there is only £100, after seven actions there is £100 + £80 + £64 + £51.20 = £295.20 in the economy.

Figure 16.1 Money creation by bankers

This new money is actually debt. And it works only if people are willing to accept bankers' promissory notes. They do this because these notes are perceived as being ‘payable on demand'. If you turned up at a bank you would have been able to swap your notes for coins. Today UK notes still state ‘I promise to pay the bearer on demand the sum of twenty pounds'.

However, unlike in the 17 th century, if you went to collect from the Bank of England today you would only get another note in exchange - we have moved right over to pure fiat money. Paper money is called fiat money - it is money simply because it is declared as such by a government to be legal tender. It is money without intrinsic value other than the potential for others to trust it and accept it as money. To be useful the notes issued then and now have to carry a legally enforceable unconditional right to payment. Also, they should be negotiable - that is, transferable - between people.Of course, there is another danger: if you are working off a deposit base of £1,000 and you lend £4,000, and then 30% of your borrowers are unable to pay, you are bankrupt. This thought should limit the amount you lend given your deposit base (a capital reserve is kept), but bankers occasionally misjudge this.

Many of the goldsmith-bankers developed into famous banking firms of today, such as Coutts & Company.

The cheque is invented

If a depositor wanted to make a payment he could write a letter to his goldsmith-bank asking that the person named in the letter be allowed to receive in cash the sum stated in the letter. Alternatively, the letter could authorise the transfer from one deposit account at the goldsmith to another. The earliest handwritten cheques appeared after the English civil war. The early 1700s saw the first fully printed cheques, and the first personalised printed cheques were produced in 1810.

A clearing house

But what if the payee banks with another goldsmith-bank? Then there had to be a way of communicating between the two. At first this process would have been laborious, as clerks from each bank would visit all the other banks to exchange cheques and then settle between them, but in 1770 the London bankers got together in one place (a tavern) to handle the cheques from many banks. This eventually became the Bankers' Clearing House in the early 19th century.

When the railways linked up the rest of the country in the 1840s the cheque system really took off, linking up more than 150 banks.More on fiat money

The first modern fiat paper money issued by a government was by Massachusetts in 1690. To pay off soldiers who had contributed to the latest round of plundering expeditions in Quebec, £7,000 was printed. The pieces of paper handed out were to be redeemed in gold or silver out of tax receipts in a ‘few years' (in fact, they had to wait 40 years). Massachusetts' politicians loved this way of paying for things and so kept issuing paper - by 1748 there was £2.5 million in circulation. By the late 1750s all the other colonies had followed suit. It was only natural that the Continental Congress chose the tool of fiat paper money to finance the Revolutionary War (1775).

Paper money in the UK

Britain was somewhat slower in gaining government control over the issue of paper money. In 1694 the Bank of England (BoE) was founded but at this stage its job was to act as the government's banker (managing its account) and to raise money for it. It immediately raised £1.2 million for the government by getting people to subscribe to a share issue to set up the new bank (the government needed to pay for a war with France). The subscribers became the Governor and the Company of the Bank of England. While other banks were restricted in size by being limited to six partners (if they were to issue currency), the BoE, being a joint-stock company with shareholder limited liability, could issue shares to investors around the country to raise capital. Also, being so big and strong it attracted plenty of deposits. Its strength meant that by the 1780s it was acting as banker to other banks.

During the Napoleonic wars the government was borrowing so much paper money from the BoE that it ran out of gold to back the notes. The government thus declared that the notes need no longer be convertible to gold. The result of all this spending and the creation of so much fiat money was high inflation.

The lesson was learned: you need to limit the quantity of paper money.There continued to be many small banks issuing bank notes. Many were unsound, irresponsibly creating notes. In 1844 the BoE was emphasised as the main issuer of notes. From then on, there were to be no new issuers of notes and those whose issues lapsed, or that were taken over, forfeited their right to issue. Other issuers gradually died out. The notes issued by the BoE were mostly backed by its holdings of gold or silver bullion, but another £14 million was permitted (equal to the BoE capital raised from shareholders). The backing of gold (the gold standard) created a long period of price stability. However, today in most countries currency notes are not backed by anything other than a promise to pay - pure fiat systems.

In addition to the issue of notes and being banker to the government the BoE took on roles such as being lender of last resort to the banking system and was called on to stabilise the banking system in crises, which happened pretty often.