WHAT IS FINTECH?

Even though the term FinTech describes applications beyond online lending, it makes sense to define the term. The acronym arrived on the tech scene sometime in early 2013. A combination of the words “financial” and “technology,” the term broadly describes innovation in financial services through software and innovative uses of technology.

It is used for a wide variety of firms including peer-to-peer lenders, cryptocurrencies such as Bitcoin, but even online payment

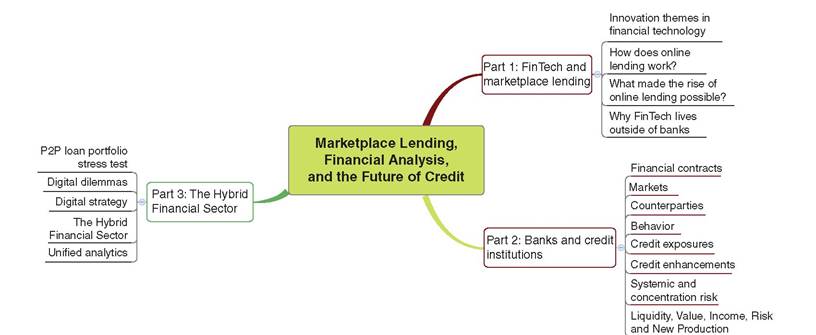

FIGURE I.1 Parts and chapters of this book

processors such as PayPal, which has been around since 1998. Even though established banks and credit institutions heavily push innovation through technology, FinTech often describes ideas that emerge outside the established financial sector. Services in this field are often called “alternative,” as in “alternative to the established financial sector.” For example, when we speak about online lending, this could mean loan origination via online channels by both established banks and new financial technology startups. Some authors therefore distinguish further by calling online lenders that are not banks alternative online lenders. In this book, we use online lenders to describe non-bank lenders. The kind of online lending we are interested in here is always an alternative to established channels of credit in the formal financial sector.

Silicon Valley is a hotbed for tech startups, and financial technology startups in particular. But in terms of FinTech, new additional innovation centers have emerged that attract entrepreneurs. Because of their proximity to the financial sector, New York and London have also become platforms for startups in this field. Established banks have begun to support FinTech accelerators and innovation labs, funding startups for a certain amount of time and giving them access to their networks.

Their goal, of course, is to spot innovative solutions and talent before anybody else. As a consequence, the sale to a bank is a valid exit strategy for a FinTech startup, but only if their technology has proven worthwhile and profitable in the market in a relatively short amount of time. Unless banks can capitalize immediately on their investment, they are unlikely to nurture and develop disruptive ideas in their midst any time soon.I.2.1 Distinction between Financial Technology Innovation and Financial Innovation

It is important to point out that this book is about something other than what financial professionals understand by the term “financial innovation.” To be clear, financial technology innovation (FinTech) and financial innovation are different animals. Both are sometimes used interchangeably, and they certainly overlap. Financial innovation mostly describes innovation from within the established financial sector. Examples of financial innovation are structured products, such as credit default swaps (CDS) or collateralized debt obligations (CDOs). Credit cards and ATMs are also examples of financial innovation, as they grew out of banks that already existed. Products of financial innovation are rarely widely adopted at the very beginning, but they have a place somewhere in the established financial sector. Financial technology innovation, or FinTech, on the other hand, comes out of left field and aims to unseat the existing players in the financial sector. Even though ex-bankers and lawyers have founded some FinTech startups, many of them are venture-capital funded startups founded by entrepreneurs with good ideas but little experience in finance and investment. These ventures have technology at their core, and they have their roots outside of the established financial sector.

Software and technology is at the heart of almost everything in finance. So, on which areas of the financial system do FinTech startups focus? The most important ones are:

■ Alternative online lending

■ Crowdfunding and crowdinvesting

■ Transactions and payments

■ Personal finance management

■ Digital currency and cryptocurrency

■ Mobile point of sale (mPOS)

■ Online financial advisory

■ Mobile-first banks

All of these areas share the common requirements of data analytics, security, cloud computing, and customer relationship management (CRM) platforms. Those components are prerequisites for FinTech startups to make use of the technological possibilities that are available today.

I.3