Whenever a new FinTech service launches, the obvious first thing to do is to compare the new offering to those of the established financial sector.

However, banks are already working closely with tech companies on the backend to provide services to customers. As much as FinTech entrepreneurs often distance themselves from the formal financial sector, they depend on each other more than they like to admit.

For example, Apple Pay, the iOS app that turns the iPhone into a digital wallet, relies on deals with the three major credit and debit card providers: Visa, MasterCard, and American Express. In transactions, the credit card networks dynamically generate security tokens that are an essential part of the service and its security.1 Major banks such as Bank of America, Capital One, Chase, Citi, and Wells Fargo have also signed up.2 As a result of these commitments, Apple supports the cards that represent about 90 percent of the credit card purchase volume in the United States.3 It is easy to see the benefit of using mobile payments, and even though banks are often reluctant to embrace change, it is in their interest to collaborate with a company like Apple. On the other hand, the tech company also needs the established financial firms; their technology is part of the security backbone on which the service operates. Without partners who control existing financial networks, Apple Pay would have to build its solution from zero. Labeling Apple Pay as a disruptive innovation that will usurp the existing financial sector is therefore missing the point. It is more an extension of similar transaction services that existed for a while, adapting them for the convenience of consumers in tune with their digital lifestyle.Because they build on existing technology that is often in the hands of banks, FinTech services that improve existing solutions are less disruptive than they would like to appear. On the other hand, when advantages and market potential are less evident, entrepreneurs without a track record will have no chance convincing banks to give them a hand.

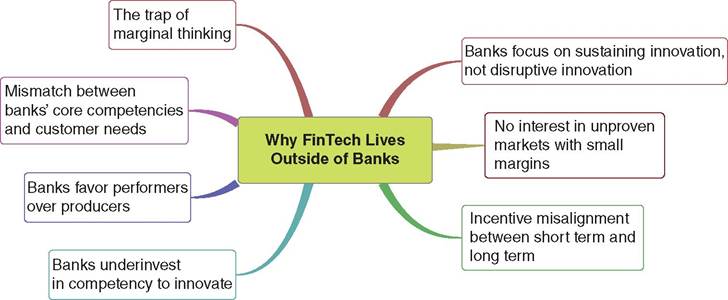

The ideas that take off in the future often find few nods in the present and, because of that, the companies that will eventually shape the future of finance might be completely off the radar, far removed from the media spotlight and the public consciousness. This is a bigger issue than it seems: even though banks are aware of the necessity to change with the times, they underestimate the disruptive impact of a FinTech ecosystem that lives completely outside of banks.Most banks have a digital strategy and their COOs are often knowledgeable about trends in FinTech. Many of them keep a close eye on developments in the financial technology innovation scene. In their view, whenever they see something interesting, they integrate it into their operations, with the goal of ensuring their long-term leadership in the financial sector. This might work while the FinTech ecosystem is still in its infancy and relatively immature.

FIGURE 4.1 Reasons why FinTech lives outside of banks

However, for the acquisition strategy of banks to continue to work, FinTech entrepreneurs must be willing to play along. What will happen if an entrepreneur refuses to sell to a bank and prefers to challenge the financial sector head on? It may be possible to freeze out such insurgents for a while—by pointing towards the need for a banking license and compliance with regulation. In the end, a walled garden is only safe as long as someone has yet to find a way to scale that wall. This chapter examines why FinTech innovation is bound to happen on the periphery, and why banks and other market leaders in the financial sector will most likely overlook innovations with the most disruptive potential. Later in this book, in Part Three, we will chart ways for banks and FinTech companies to work together to build the hybrid financial sector of the future. Figure 4.1 gives an overview of the main points we discuss in this chapter.

4.1