WILL BANKS NOTICE THE NEXT FINTECH BREAKTHROUGH?

It is possible but unlikely that a bank or another market leader in the established financial system will produce the next FinTech breakthrough. At this point, most banks look at FinTech startups as a cheap R&D lab from which they can mix and match services that might be useful to them to increase margins.

This is the major reason they sponsor FinTech innovation labs around the globe in the first place. But by now we know that there are two different categories of FinTech services out there: those that emerge with sustaining innovation that makes the existing operations of the established financial sector easier. Examples are Big Data analytics that make sense of financial patterns or customer behavior, or other tools that banks already use in one form or another. The second category has to do with disruptive innovation—things banks have not thought of, but that are potentially extremely useful to their customers. Banks are good at spotting sustaining innovation. They are already highly technical operations, with a long history of working with technology providers to streamline and improve their operations. Where exactly this innovation is coming from—a garage in Silicon Valley or the shiny office of a consulting firm in the City of London—matters less and less to banks. When they can get hold of solutions that help them do their work more efficiently, they are likely to acquire them. FinTech companies offering sustaining innovation can therefore expect that banks willhave an interest in integrating their services. We might see a large number of acquisitions of such FinTech startups in the near future.

Things are different for disruptive financial technology startups. Integrating a disruptive startup into the fabric of an established bank is much more complex, as it inherently cannibalizes a bank's existing profit centers. Marketplace lending has the potential to be a disruptive innovation.

A new approach to lending in the trillion-dollar credit market might make a big dent in how the financial sector works. Regardless, banks have little interest in changing their business model when offering credit, at least for the time being. On top of that, most banks doubt that marketplace lending will be serious competition for their loan business, and some of them believe that the disruptive innovation in the sector already happened years ago when the concept of peer-to-peer lending was first announced in 2005. The ticket size of individual loans currently tops out at $35,000. This might be fine for consumer loans, but the much larger and more interesting markets for real estate credit and corporate lending require a different scale. Marketplace lending will have to grow out of its marginal appeal to be a real game changer in the established financial sector. Until that happens, it is very likely that banks will dismiss it as either immature or not interesting enough to be a serious competitor.When looking at the business models and strategies of banks and established credit institutions today, it is clear that they have little leeway to support innovation from within. They all portray themselves as innovators, but simply projecting something does not make it so. As a result, disruptive financial innovation breakthroughs will take place at the fringes of the established system, without the incumbents noticing. Success rarely relies on getting it right at the first try. Instead, it hinges on continuing experimentation until the approaches that work emerge. Only a lucky few companies start off with a strategy that ultimately leads to success. There are other reasons banks will probably fail to notice those FinTech innovations with the biggest potential in the long term, as the next paragraphs will examine.

4.2.1 Incentive misalignment between the short term and the long term

Imagine your job is to spot and carry out the innovations that improve the operations of a big bank.

What projects are you most likely going to support? If you take a long-term perspective, you would support new products and processes that will be key to a bank's success in five to ten years in the future. However, the results of those efforts will only become evident many years later, after they have swallowed millions of dollars in trial and error. When they have finally proven their worth, you might have already moved to another division or another bank and whoever is at the helm at that time will claim credit for the innovation you stuck your neck out for. Even if you are still around to harvest the fruits of your labor in five to ten years, if you lose money nine years out of ten—even one year out of ten—you will have a hard time staying the course. Instead, if you focus on delivering results that are visible and measurable within six to twelve months—even with an inferior approach—you know that those assessing the innovation program will reward you. This is just how incentives in business work. You see each project as a stepping stone. With something to show for your good ideas and efforts, you hope to get a shot at an even bigger and better assignment the next time around.An incentive system that rewards decision makers for short-term thinking often undermines the company's success in the long term. Investor Frank Rotman points out that big corporations have “long organizational memories” when it comes to failures. Failures are often pinned on executives for a long time, which makes matters even worse. If an executive can build a track record of success, he may be able to afford taking more risks and try something that may fail once in a while. In essence, the formula for career progression is to fail on smaller projects and succeed on the bigger ones. These bigger projects are those for which your boss is holding his boss responsible.14

It is important to reiterate that we have no intention of lambasting the financial sector, or banks in particular.

Misaligned incentives and resource allocation are by no means reserved for banks. Governments, for example, are unable to change their social security and other entitlement programs, even though most of these programs are on the brink of bankruptcy. Why is that so? Politicians stand for re-election every few years. It is their conviction that it is in the best interest of the country to re-elect them, so they focus on delivering short-term results that stick in the minds of the electorate until the next vote. How entitlement programs could improve is widely known. Yet, so many people rely on these programs that a radical change would be highly unpopular. Anyone who cuts benefits for voters can be sure to lose the next election.Introducing change is never an easy game to win. Yet someone has to assume responsibility for taking risks and making unpopular decisions when it comes to fostering innovation that will prevail in the long term. Unfortunately, the people willing to do so have a difficult time standing up for what they believe in, or they opt out of the corporate career path entirely and start their own thing. The loss for corporations is immeasurable.

4.2.2 Forcing banks to collaborate with online lenders

When change refuses to grow organically from within companies, it is of course possible to legislate it from the outside. In the summer of 2014, the UK’s Chancellor of the Exchequer, George Osborne, revealed new rules under the Small Business, Enterprise and Employment Bill, that force banks that reject loan applications from SMEs to refer them to online lending platforms.15 Concurrently, bank Santander and the lending platform Funding Circle announced the first partnership between a UK bank and a peer-to-peer lending platform.16 In return for customers’ referrals from Santander to the online lender, Funding Circle promotes the bank’s current account and cash management service. In a similar move, the Royal Bank of Scotland (RBS) signaled plans to enter the peer-to-peer lending market in a tie-up with a third party operator.17

Is this good news or bad news for the future of the hybrid financial sector? A little bit of both.

Despite the new rules for online referrals and cooperation, banks bring in products from the outside into their business units instead of growing new ideas from within. They are distributing products that established online lenders have produced, still without investing in their own core competencies. Forced collaboration may be a start, to show that it is indeed possible to break down conventional barriers in the financial sector. Nevertheless, it still fails to address the underlying problems that prevent innovation from emerging from within the sector where it could make a difference for banking customers in the long run.4.2.3 Innovating in-house vs. buying innovation

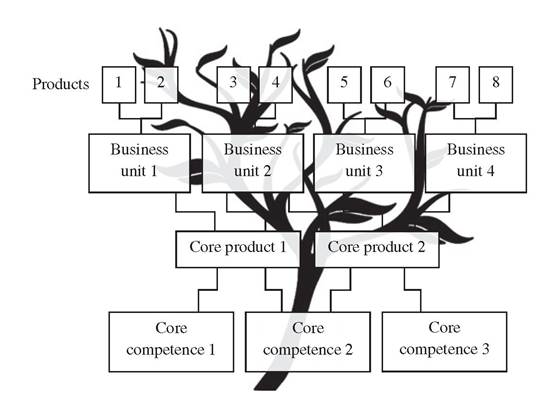

Authors CK Prahalad and Gary Hamel provide a useful framework to address innovation and competency of corporations. Even though their theory is close to 25 years old, it is still an excellent approach to see the advantages for companies to grow innovation in-house instead

FIGURE 4.2 The corporation as a tree

Adaptedfrom: Prahalad and Hamel

of purchasing it in the market. This is by no means the case with banks only. It applies to most large companies operating in mature markets. Prahalad and Hamel liken a company to a tree with several core competencies as its roots. These competencies are the “roots of competitiveness,” that will eventually decide if a company will end up a market leader or a follower. Out of these core competencies, core products emerge as the tree trunk. Business units spring from core products as branches that finally produce products, the leaves and fruits of the tree. These leaves and fruits are the parts of the business that customers will interact with. Just as roots need time to grow, corporations build core competencies through a continued process of improvement and enhancement that may take a decade or longer. Companies that have neglected investment in building their core competencies will find it difficult to enter an emerging market. As a result, they might serve as a distribution channel for the products of other companies.18 Figure 4.2 shows the structure of the corporation as a tree.19

The battle for leadership in a business sector takes place on the planes of core competence, core product, and products. An established corporation may win a battle on one plane but lose on another. With large investments, a company might be able to beat competitors to blue skies technologies, but it may still lose the race to build leadership with core competence. The only guarantee for a company to outpace its rivals in new business development is developing strong core competencies. This bottom-up strategy for innovation makes for a more resilient company than one that buys technology leadership piecemeal.20

4.3