Bulgaria

Proving resilient to shocks

| GDP | USD89.0bn (World ranking 70) |

| Population | 6.5mn (World ranking 109) |

| Form of state | Parliamentary Republic |

| Head of government | Nikolai Denkov (PM) |

| Next elections | 2026, Presidential |

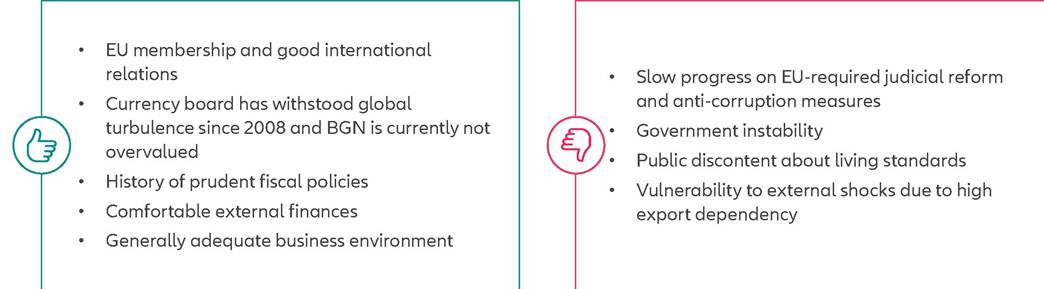

Strengths & weaknesses

Economic overview

Moderate growth and gradually declining inflation in 2024

Bulgaria's economic prospects have deteriorated as a result of Russia's invasion of Ukraine.

The country's economy is very export-oriented, including the export of services (tourism), which makes it vulnerable to external shocks. Moreover, prior to the war, Bulgaria was heavily dependent on naturalgas imports from Russia. As a result, it has been markedly impacted by the European energy crisis and EU trade sanctions against Russia. Following a strong post-Covid-19 recovery with +7.7% real GDP growth in 2021, economic activity in Bulgaria slowed down markedly in 2022-2023 amid surging inflation, higher interest rates, weakening external demand and deteriorating business confidence. The latter affected investment in particular, which dropped substantially last year, while domestic fiscal stimulus was dialed down due to rising financing costs. Nonetheless, growth remained positive at around +2% in 2023 on the back of resilient private consumption, thanks to strong wage growth and a positive contribution of net trade as imports contracted much sharper than exports. Going forward, we expect another year of moderate growth in 2024. Consumer spending will be more restrained due to lower wage increases and higher projected interest rates for households. Investment activity should rebound in the next two years, driven by public investment, including NGEU funded projects. Meanwhile, Bulgarian exports should recover gradually in parallel with export markets but imports will rebound more strongly so that the contribution of net trade will turn negative. Overall, we expect full-year real GDP to expand by around +2% in 2024 and +2.5% in 2025.We expect currency stability to be maintained but price stability will not be fully regained before 2025. Bulgaria's currency board (BGN1.95583:EUR1) should remain stable since foreign exchange (FX) reserves continue to clearly cover the monetary base (a requirement for a currency board; over 150% at end-2023). However, the currency board largely neutralizes monetary policy, preventing its use to counter upward price pressures since 2021. Headline consumer price inflation surged to a peak of 18.7% y/y in September 2022 and averaged 15.3% in 2022 and almost 10% in 2023, owing to markedly higher food and energy prices, as well as ongoing supply-chain and labor-market disruptions. Since mid-2023, these effects have been gradually fading and we expect this to continue in the next two years. We forecast annual average inflation of about 4% in 2024 and 2.7% in 2025, which compares to an average 1.5% in the 2010s.

Public and external finances will remain comfortable, by and large

Bulgaria's public finances will remain unproblematic despite some impact from the recent crises. The country has had a long-lasting commitment to fiscal prudence, reflected in many years of fiscal surpluses or acceptable deficits. Following annual surpluses in 2016-2019 (+1.2% of GDP on average), fiscal stimulus measures, lower revenues and declining nominal GDP in the wake of Covid-19 resulted in annual fiscal deficits of around -4% of GDP in 2020-2021 and gross public debt rose from 20% of GDP in 2019 to 24% in 2021.

Further fiscal shortfalls of approximately -3% of GDP were posted in 2022-2023 as a consequence of fiscal stimulus in order to mitigate the impact of the war in Ukraine on the Bulgarian economy. Looking ahead, we forecast the annual fiscal deficit to remain close to -3% of GDP in 20242025 as public investment is expected to pick up. The public- debt-to-GDP ratio is projected to edge up to around 26% by2025. However, this will still be a very favorable ratio by EU standards.

As a result of its long-standing prudent economic policies, Bulgaria was admitted to the Exchange Rate Mechanism II (ERM-II), the “waiting room” for eventual adoption of the EUR, in July 2020. In conjunction with ERM-II membership, Bulgaria also joined the European banking union in October 2020. We expect the country to adopt the EUR in 2025 at the earliest.

Bulgaria's external finances will remain favorable. After seven years of current account surpluses from 2013 to 2019, reflecting a continued solid export performance and a balanced account in 2020, Bulgaria posted manageable annual external deficits in 2021-2022, mainly as a result of lower exports of services (tourism). Softening external goods demand also played a role in 2022. A sharp drop in imports moved the current account back to a moderate surplus in 2023 and we forecasts further small surpluses in 2024-2025. Meanwhile, the steady downtrend in the gross external debt- to-GDP ratio was only briefly interrupted in 2020 in the wake of the Covid-19 crisis. It has declined from a peak of 107% of GDP in 2009 to around 45% in 2023 and is on course to fall further in the coming years. In the meantime, Bulgaria has one of the lowest ratios among the 11 EU member states in CEE.

Bulgaria's FX reserves have increased substantially since end-2013 and stood at EUR35bn at end-2023, a comfortable level with regard to import cover (around eight months). Moreover, in other terms, reserves cover about 190% of the estimated external debt payments falling due in the next 12 months, a favorable ratio and a significant and steady improvement from 80% in 2011.

Above average business environment

Bulgaria's business environment is generally adequate though spots of weaknesses remain. The World Bank Institute's annual “Worldwide Governance Indicators” surveys suggest that the regulatory framework is generally business-friendly while weaknesses remain with regard to perceived corruption and the legal framework. The Heritage Foundation's Index of Economic Freedom survey 2023 assigns Bulgaria rank 32 out of more than 180 economies, reflecting strong scores with regard to property rights, tax burden, business freedom and trade freedom. Weaknesses remain in the areas of judicial effectiveness and government integrity. On our proprietary Environmental Sustainability Index, Bulgaria is ranked 69th out of 210 economies, reflecting strong scores for energy use and CO2 emissions per GDP, water stress and general vulnerability to climate change. However, there are still weaknesses regarding renewable electricity output and the recycling rate.